Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

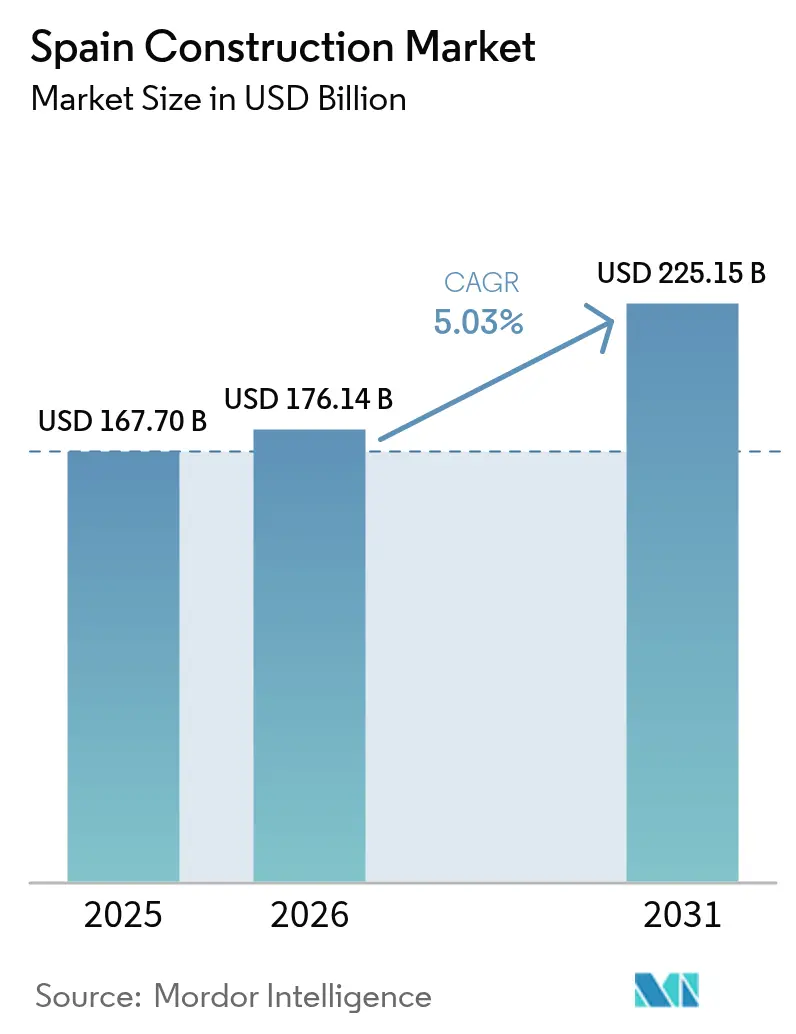

| Base Year Market Size (2025) | USD 167.70 Billion |

| Market Size (2026) | USD 176.14 Billion |

| Market Size (2031) | USD 225.15 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

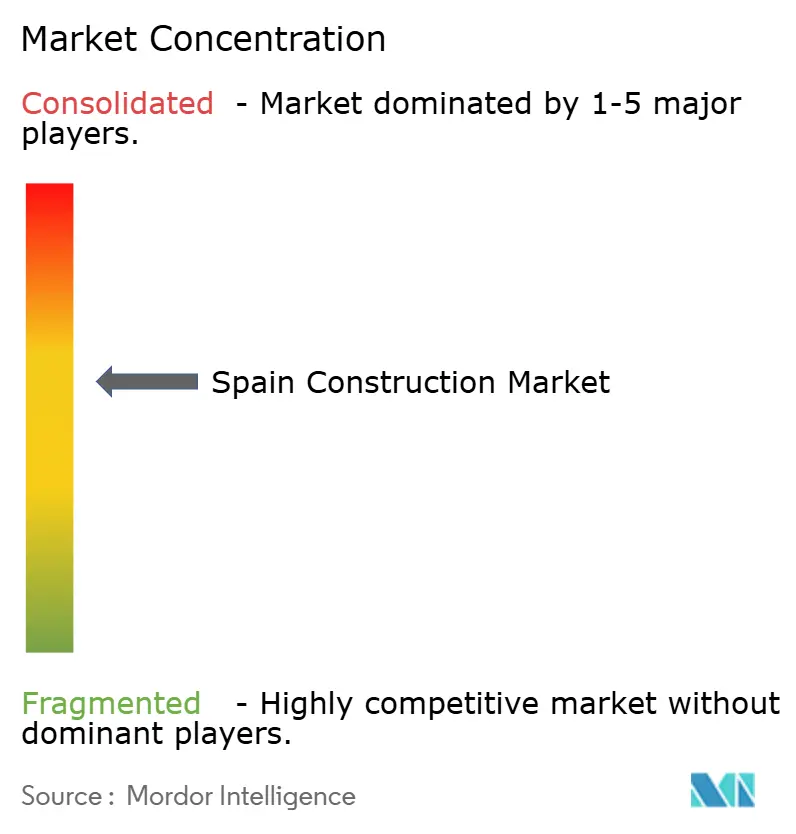

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Construction Market Analysis by Mordor Intelligence

The Spain construction market size is expected to grow from USD 167.70 billion in 2025 to USD 176.14 billion in 2026 and is forecast to reach USD 225.15 billion by 2031 at 5.03% CAGR over 2026-2031. This expansion is propelled by Spain’s access to USD 154 billion in NextGenerationEU resources, of which roughly 70% flows directly into construction-related programs spanning infrastructure, renewable energy, and building rehabilitation. Residential activity keeps demand resilient, while unprecedented public-sector spending anchors infrastructure outlays and crowds in private capital. Growing adoption of modern construction methods, extensive digitalization mandates, and the 2030 FIFA World Cup infrastructure program further widen the opportunity set. Nevertheless, labor scarcity and commodity-price volatility continue to weigh on margins, compelling firms to accelerate automation, off-site manufacturing, and strategic procurement actions.

Key Report Takeaways

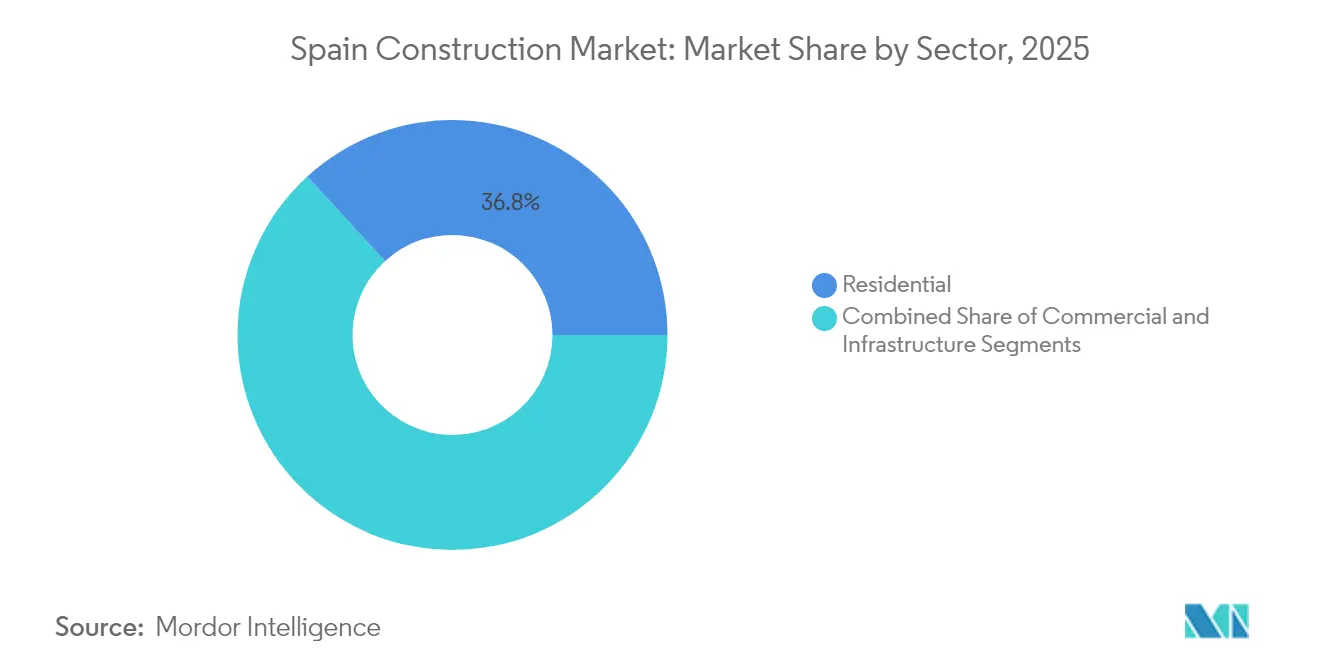

- By sector, residential construction led with 36.80% of Spain's construction market share in 2025, whereas infrastructure is forecast to expand at a 6.78% CAGR through 2031.

- By construction type, new construction accounted for 67.05% of the Spain construction market size in 2025; renovation is projected to grow at a 5.55% CAGR through 2031.

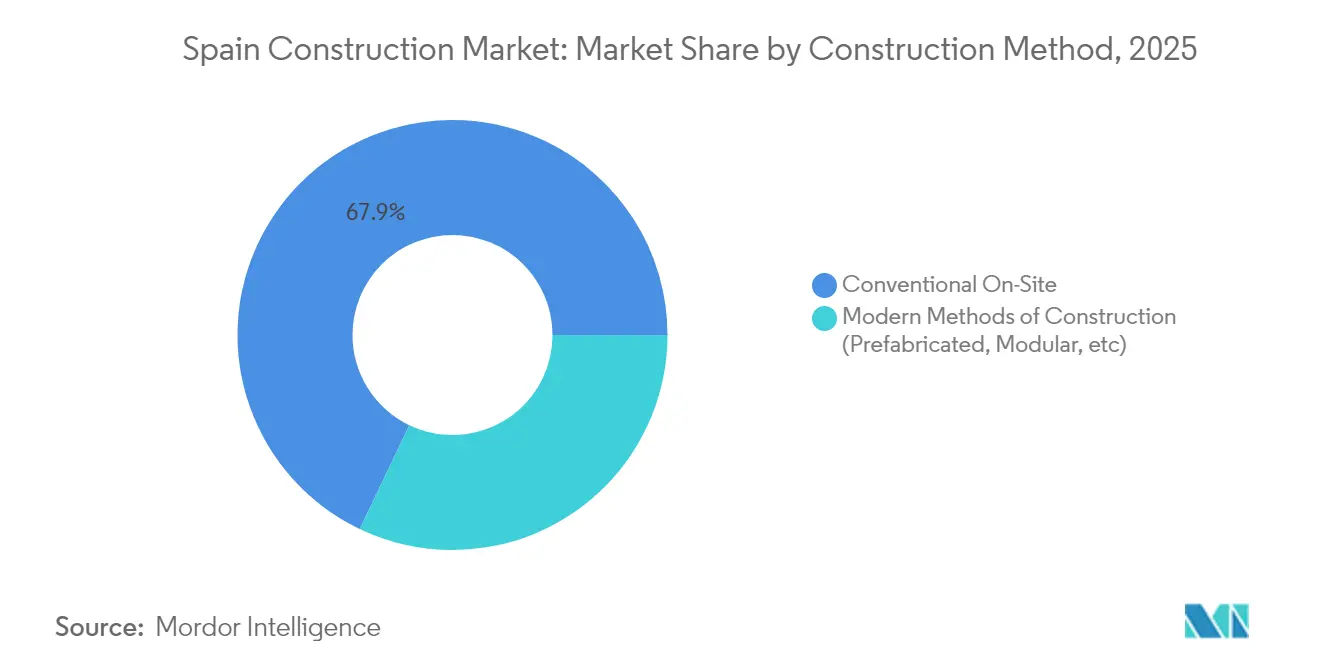

- By construction method, conventional on-site techniques held 67.90% share of the Spain construction market in 2025; modern methods are growing at 11.10% CAGR.

- By investment source, public expenditure accounted for 64.10% of the Spain construction market size in 2025, and private funding is rising at an 8.74% CAGR to 2031.

- By geography, Madrid captured a 23.30% share of the Spain construction market in 2025, while Andalusia is advancing at a 5.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Construction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-funded infrastructure modernization | +1.2% | Nationwide, Andalusia, Catalonia, Madrid, Valencia | Long term (≥ 4 years) |

| Renewable-energy build-out | +1.0% | Castile-La Mancha, Extremadura, Aragon | Long term (≥ 4 years) |

| Housing-demand recovery via favorable mortgage rates | +0.8% | National: early momentum in Madrid, Valencia, Barcelona | Medium term (2-4 years) |

| Tourism-led commercial real-estate rebound | +0.6% | Coastal zones, Madrid, Barcelona | Medium term (2-4 years) |

| Modular/industrialized construction in public tenders | +0.4% | Catalonia, Madrid, the Basque Country | Long term (≥ 4 years) |

| Water-scarcity adaptation projects | +0.3% | Mediterranean coast, Andalusia, Valencia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU-Funded Infrastructure Modernization

Spain secured USD 76.5 billion in grants, receiving an “excellent” rating from the European Commission for its recovery plan. Flagship rail schemes include the USD 919.6 million ADIF network renewal and the USD 3.3 billion Mediterranean Corridor upgrade, which converts single to double track and electrifies critical links. Complementary Connecting Europe Facility funding of USD 265.1 million supports 22 multimodal projects across eight regions. These works generate local employment, stimulate steel and concrete demand, and re-position Spain as a continental logistics hub.

Renewable-Energy Build-Out

National targets call for 62 GW of fresh renewable capacity by 2030, fuelling wide-ranging construction. The USD 770 million Teruel onshore wind contract for 125 GE Vernova turbines will deliver 760 MW and exemplifies portfolio scale-up. Iberdrola’s USD 550 million smart-grid expansion, part-financed by EU funds, is projected to support 10,000 annual jobs. Energy-storage investments such as the Valdecañas pumped-storage upgrade (USD 118.8 million) raise grid resilience and secure stable EPC pipelines[1]European Commission, “Spain’s BIM Public Procurement Plan,” ec.europa.eu.

Housing-Demand Recovery Via Favorable Mortgage Rates

Spanish developers benefit from a window of low mortgage costs that coincides with a housing shortage in major metro areas. Building permits totaled 107,934 in 2023 against 297,000 new household formations, underscoring supply gaps. Net-zero social-housing pilots, such as the 54-unit complex in Inca, Mallorca, highlight policy focus on affordability and sustainability. Foreign buyers continue to absorb prime units, providing liquidity even as domestic volumes fluctuate. As financing conditions gradually tighten, the pipeline front-loading observed in 2025 is expected to moderate, yet elevated demographic pressure maintains baseline demand.

Tourism-Led Commercial Real-Estate Rebound

Co-hosting the 2030 FIFA World Cup will unlock USD 1.57 billion in stadium and urban upgrades, generating an estimated USD 5.5 billion in economic value and 82,000 jobs. High-profile projects include the USD 1.9 billion Santiago Bernabéu redevelopment and the USD 1 billion Camp Nou overhaul, both integrating mixed-use retail components. Hotel pipelines expand, illustrated by Dalata’s 243-room Clayton Hotel Madrid, designed for LEED Gold certification and scheduled for 2029 completion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High labor cost & skilled-worker shortages | –0.9% | Madrid, Catalonia, Basque Country | Short term (≤ 2 years) |

| Volatile cement & steel prices | –0.6% | National | Short term (≤ 2 years) |

| Stringent biodiversity impact assessments | –0.3% | Protected coasts, mountain zones | Medium term (2-4 years) |

| Rising climate-risk insurance premiums | –0.2% | Mediterranean coast, flood areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Labor Cost & Skilled-Worker Shortages

Only 9.2% of Spain’s construction workforce is under 29, down from 25.2% in 2008, constraining execution capacity for EU-funded projects. Vocational-training enrolment declined 45.6% over 15 years, widening gaps just as renewables and digitalization require specialized talent. The sector lobby pushes for expanded dual-training programs under the Fundación Laboral de la Construcción, while recruiting abroad delivers incremental relief. Tight labor markets in Madrid and Catalonia drive wage escalation that jeopardizes bid competitiveness and strains fixed-price contracts.

Volatile Cement & Steel Prices

Cement producer-price indices hit 138.8 in 2024, and steel rose 11.2% year-on-year, eroding contractor margins. Price-revision clauses in public contracts remain rigid, forcing bidders either to absorb cost spikes or withdraw. Budget overruns deter smaller firms, reducing tender competition and delaying Recovery Plan milestones. Transport surcharges in island territories further inflate delivered prices, damaging regional project viability.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Infrastructure Momentum Challenges Residential Leadership

Residential construction held 36.80% of the Spain construction market share in 2025, sustained by unmet urban housing demand and a brisk foreign-buyer segment. Infrastructure, the fastest-growing component, is forecast to post a 6.78% CAGR through 2031 as Recovery-Plan disbursements front-load transport and energy upgrades. Metro Madrid line extensions, Mediterranean Corridor rail doubling, and Iberdrola grid expansions collectively shift contractor backlogs toward heavy civil works. Meanwhile, the 2030 FIFA World Cup injects marquee stadium and urban-mobility projects that further tilt growth toward infrastructure.

Despite the infrastructure’s surge, residential pipelines remain robust in Madrid, Barcelona, and Valencia, where land scarcity and policy incentives favor vertical development. Energy-efficient building codes catalyze demand for heat-pump installations and high-performance envelopes, spurring specialized subcontractors. Commercial real estate capitalizes on revived tourism flows, while industrial space rides the wave of near-shoring and e-commerce logistics, showcasing the sector’s diversified growth engines.

Note: Segment shares of all individual segments available upon report purchase

By Construction Type: Renovation Gains Momentum Through EU Energy Programs

New construction dominated with a 67.05% slice of the Spain construction market size in 2025, powered by green-field rail, highway, and utility megaprojects. Renovation, however, is expanding at a 5.55% CAGR on the back of USD 3.8 billion in EU subsidies targeting 510,000 residential retrofit actions by 2026. Grants covering up to 80% of eligible costs and mandating 30% energy-use cuts amplify homeowner uptake. Catalonia leads with more than 300 subsidized schemes, while 597 public buildings across 499 municipalities secure separate retrofit funding.

The renovation surge addresses Spain’s aging stock, with two-thirds of buildings older than 40 years. BIM-based energy audits and digital building permits streamline approval and encourage bundling of works, reducing unit costs. Contractors pivot to façade insulation, solar-ready roofing, and accessibility upgrades, creating niche opportunities for SME specialists. As utility bills climb, payback periods shrink, supporting a sustained retrofit wave beyond the grant window.

By Construction Method: Digital Technologies Accelerate Modern Methods Adoption

Conventional on-site approaches retained 67.90% market share in 2025, yet modern methods boast an 11.10% CAGR, spurred by labor shortages and BIM-mandate compliance. Public-sector clients now stipulate BIM deliverables on contracts exceeding USD 13.7 million, nudging supply chains to embrace digital twins and factory-precision modules. Projects like MOD4SMART cut the schedule by a quarter, evidencing measurable productivity gains.

Prefabricated volumetric units gain traction in social housing and education facilities, lowering waste by up to 45% and improving worker safety. Robotics, 3D concrete printing, and on-site drones support quality control and progress monitoring. Early adopters leverage these capabilities to differentiate in competitive bid evaluations that assign points for technology and sustainability, signaling structural change in how Spain builds.

Note: Segment shares of all individual segments available upon report purchase

By Investment Source: Private Sector Acceleration Complements Public Leadership

Public funds contributed 64.10% of Spain's construction market value in 2025, reflecting robust fiscal stimulus and EU grant inflows. Private capital, the fastest-rising pool at an 8.74% CAGR to 2031, intensifies in renewables and commercial real estate. Iberdrola’s USD 2.2 billion co-investment with Norges Bank for 2.6 GW of green capacity illustrates growing institutional appetite. Meanwhile, a USD 2.75 billion European Investment Fund guarantee program channels liquidity to more than 6,000 construction-linked SMEs.

Public-private partnerships (PPPs) gain renewed appeal as fiscal rules tighten after 2026. Concession models blending recovery-plan grants with user-fee revenue underpin upcoming highway and desalination assets. As private investors demand ESG-aligned opportunities, Spain’s decarbonization roadmap offers a deep pipeline of bankable projects across transport electrification, grid expansion, and energy-positive buildings.

Geography Analysis

Madrid captured 23.30% of the Spain construction market in 2025, underpinned by flagship rail, airport-access, and stadium undertakings that reinforce its role as an economic hub. The USD 1.9 billion Bernabéu refurbishment and the Clayton Hotel’s LEED-targeted design attract global contractors and green-finance providers. Strong public-investment flows and corporate headquarters presence keep office-fit-out demand intact, while high-rise residential towers proliferate along new metro axes.

Catalonia combines industrial prowess with pressing climate-adaptation needs. USD 126.5 million worth of desalination upgrades protect manufacturing output, and USD 115 million in retrofit grants kick-start deep-renovation clusters. Barcelona’s Camp Nou expansion re-energizes the commercial pipeline, while logistics developers capitalize on cross-border e-commerce traffic to France.

Andalusia is the fastest-growing region at a 5.12% CAGR through 2031, leveraging superior solar irradiation and coastal tourism assets. Large-scale PV parks in Cádiz and wind arrays in Almería dovetail with expanded cruise-port capacity, creating multi-disciplinary contract opportunities. EU Cohesion funding upgrades secondary roads and freight terminals, narrowing the region’s historical infrastructure gap and unlocking private-sector co-investments. Elsewhere, Valencia benefits from Mediterranean Corridor rail works, Galicia enhances maritime infrastructure, and Aragón cements its status as a renewables manufacturing hub, illustrating the varied regional contributions to national growth.

Competitive Landscape

Spain’s construction market features a moderately concentrated set of diversified champions. ACS, Acciona, Dragados, and Ferrovial leverage extensive international backlogs to hedge domestic cyclicality, while retaining deep local supply-chain relationships. The ACS merger of Flatiron and Dragados USA, creating a USD 6.4 billion civil-engineering giant, underscores the pursuit of geographic scale and cross-border synergies. Ferrovial’s U.S. mobility concessions provide stable cash flows that fund domestic bids, whereas Acciona’s early-stage modular housing subsidiary seeks to capture green-building opportunities[3]European Investment Bank, “Grid Expansion Loan to Iberdrola,” eib.org.

Technology adoption shapes competitive differentiation. Firms that embed BIM, IoT-based asset monitoring, and AI-driven scheduling win bonus points in quality-weighted tenders. Acciona deploys digital twins on desalination projects to optimize energy use, while Ferrovial trials autonomous equipment on highway upgrades. As public clients push for life-cycle cost visibility, contractors with integrated design-build-operate platforms capture expanding O&M revenues.

Strategic partnerships proliferate. Iberdrola teams with civil contractors for co-located PV and storage projects, offering bundled EPC packages. Spanish mid-tier builders co-invest with pension funds on student-housing and data-center assets, diversifying away from low-margin residential blocks. Foreign entrants eye modular and off-site niches, but stringent local labor-union requirements and language barriers underscore the value of entrenched domestic incumbents.

Spain Construction Industry Leaders

ACS, Actividades de Construcción y Servicios, S.A.

Dragados S.A.

Acciona Construcción S.A.

Ferrovial Construcción S.A.

FCC Construcción S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: European Investment Bank and Iberdrola signed USD 118.8 million loan for Valdecañas pumped-storage expansion, adding 313 MW pumping capacity and creating 665 jobs.

- February 2025: ACS completed the merger of Flatiron Construction and Dragados USA, forming the second-largest civil contractor in the U.S. with USD 6.4 billion revenue.

- December 2024: European Investment Bank approved USD 385 million financing for ADIF’s rail renewal program totaling USD 919.6 million in investment.

- November 2024: Iberdrola secured USD 550 million EU-backed loan for smart-grid upgrades across 12 regions, sustaining 10,000 jobs.

Spain Construction Market Report Scope

Construction is the process of planning, designing, and constructing infrastructure and buildings in Spain. It involves using a range of materials, methods, and technologies to create various structures, including roads, bridges, tunnels, dams, airports, and buildings.

The Spanish construction market is segmented by sector (residential, commercial, industrial, infrastructure (transportation), and energy and utilities). The report also analyses the Spanish construction market's key players and competitive landscape. The impact of COVID-19 has also been incorporated and considered during the study. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Sector

| Residential | Apartments/Condominiums |

| Villas/Landed Houses | |

| Commercial | Office |

| Retail | |

| Industrial and Logistics | |

| Others | |

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) |

| Energy & Utilities | |

| Others |

By Construction Type

| New Construction |

| Renovation |

By Construction Method

| Conventional On-Site |

| Modern Methods of Construction (Prefabricated, Modular, etc) |

By Investment Source

| Public |

| Private |

By Geography

| Andalusia |

| Catalonia |

| Madrid |

| Valencia |

| Rest of Spain |

| By Sector | Residential | Apartments/Condominiums |

| Villas/Landed Houses | ||

| Commercial | Office | |

| Retail | ||

| Industrial and Logistics | ||

| Others | ||

| Infrastructure | Transportation Infrastructure (Roadways, Railways, Airways, others) | |

| Energy & Utilities | ||

| Others | ||

| By Construction Type | New Construction | |

| Renovation | ||

| By Construction Method | Conventional On-Site | |

| Modern Methods of Construction (Prefabricated, Modular, etc) | ||

| By Investment Source | Public | |

| Private | ||

| By Geography | Andalusia | |

| Catalonia | ||

| Madrid | ||

| Valencia | ||

| Rest of Spain | ||

Key Questions Answered in the Report

What is the projected value of the Spain construction market in 2031?

The market is forecast to reach USD 225.15 billion by 2031, up from USD 176.14 billion in 2026.

Which segment is expected to grow fastest through 2031?

Infrastructure is set to expand at a 6.78% CAGR, outpacing residential and commercial works.

How large is the public spending share in Spanish construction?

Public funds represented 64.10% of total value in 2025, reflecting hefty EU-backed programs.

Which region shows the highest growth momentum?

Andalusia leads with a 5.12% CAGR owing to renewables and tourism-centered projects.

What role do modern construction methods play?

Modern methods are growing at 11.10% CAGR as BIM mandates and labor shortages accelerate prefab adoption.

How are material-price spikes affecting contractors?

Cement and steel volatility compress margins and deter bidding, prompting demand for better price-revision clauses.

Page last updated on: