Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

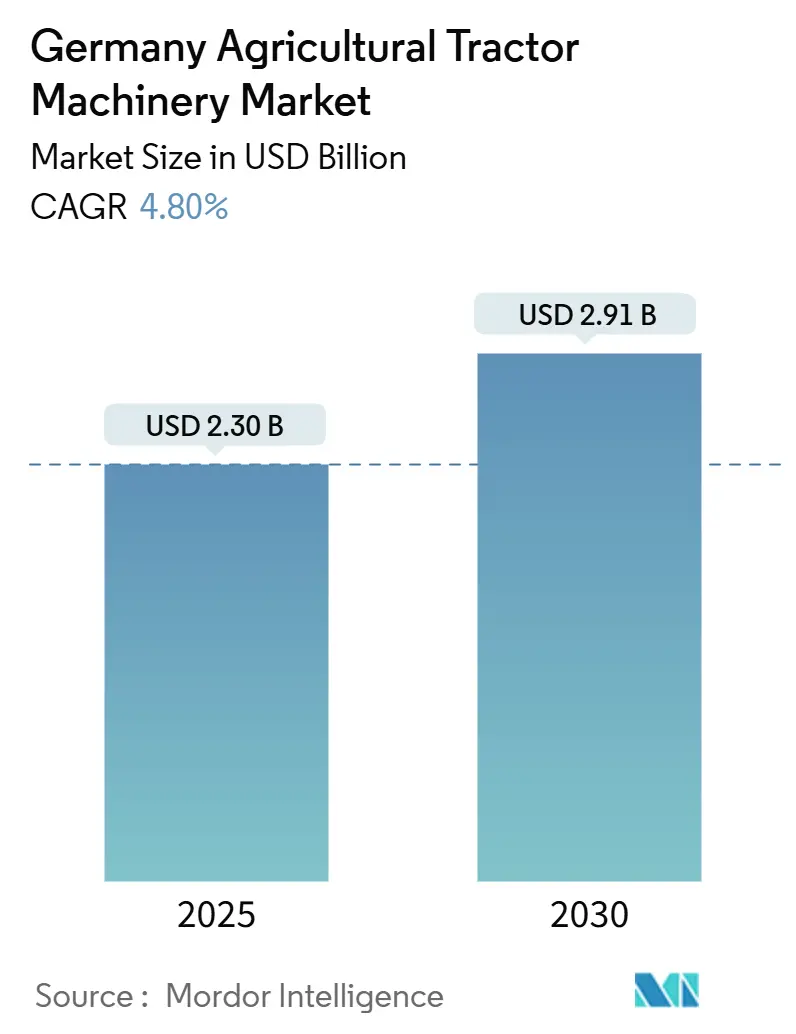

| Market Size (2025) | USD 2.30 Billion |

| Market Size (2030) | USD 2.91 Billion |

| Growth Rate (2025 - 2030) | 4.80% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Germany Agricultural Tractor Machinery Market Analysis by Mordor Intelligence

The Germany agricultural tractor machinery market size is valued at USD 2.30 billion in 2025 and is projected to reach USD 2.91 billion by 2030, advancing at a 4.80% CAGR during the forecast period. This steady trajectory conceals a strategic shift toward premium implements, Stage V-compliant powertrains, and data-driven retrofits that lift average selling prices, even as total tractor registrations slipped to 27,595 units in 2024 [1]Source: CEMA, “Tractor Registrations 2024,” cema-agri.org. Policy-induced replacement cycles, underwritten by USD 5.1 billion in annual Common Agricultural Policy (CAP) direct payments and targeted Agri-Investment Program grants, continue to anchor demand for technology-rich assets. High biogas-plant density, tightening emissions rules, and dealer-subsidized financing at rates below 3% catalyze the uptake of connectivity-ready machinery across various farm sizes [2].Source: Renewable Energy Agency, “Biogas in Germany 2025,” renewable-energy.de In parallel, the European Union Carbon Border Adjustment Mechanism adds cost pressure on steel and aluminum components, reinforcing the Original equipment manufacturer (OEM) moves toward domestic sourcing and design modularity.

Key Report Takeaways

- By product type, plowing and cultivating machinery accounted for 37.5% of Germany agricultural tractor machinery market size in 2024, and sprayers are forecast to expand at a 7.9% CAGR through 2030.

Germany Agricultural Tractor Machinery Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy boost from German Agri-Investment Program | +1.20% | Bavaria, Lower Saxony, and North Rhine-Westphalia | Medium term (2-4 years) |

| Expansion of biogas maize acreage | +0.80% | Bavaria, Baden-Württemberg, and Lower Saxony | Long term (≥ 4 years) |

| Demand for low-HP tractors from smallholdings | +0.60% | Southern mixed-farm regions | Short term (≤ 2 years) |

| Original Equipment Manufacturer (OEM) financing below 3% interest | +0.90% | National, and dealer network dependent | Short term (≤ 2 years) |

| Edge-Artificial Intelligence (AI) retrofits for autonomous tillage | +0.70% | Brandenburg, Saxony-Anhalt, and Mecklenburg-Vorpommern | Medium term (2-4 years) |

| Soil-health-linked insurance rebates | +0.50% | North Rhine-Westphalia, and Schleswig-Holstein | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subsidy Boost from German Agri-Investment Program

Germany’s Agri-Investment Program channels part of the USD 5.1 billion the Common Agricultural Policy (CAP) payments into Stage V tractors, precision sprayers, and reduced-tillage implements, linking reimbursements to telemetry-verified environmental performance through the Farm Sustainability Data Network [3].Source: European Commission, “Farm Sustainability Data Network Overview,” AGRICULTURE.EC.EUROPA.EU Co-funding rates reach 75% for climate-smart machinery, shortening depreciation cycles and steering buying criteria toward connectivity rather than horsepower. The program’s data-reporting mandate accelerates platform adoption, such as AGCO Fuse and Deere & Company Operations Center, shifting competitive advantage to ecosystem interoperability. European Investment Bank credit lines, worth USD 3.2 billion between 2024 and 2027, further reduce borrowing costs for machinery rings and cooperatives, reinforcing group purchasing power.

Expansion of Biogas Maize Acreage

Germany operates 9,500 biogas plants, totaling 6.2 GW, half of the feedstock comes from 2 million hectares of maize silage. Despite lower feed-in tariffs, repowering of legacy units secures steady forage demand through 2030. Contractors servicing these plants purchase high-throughput harvesters with kernel processors capable of processing over 400 metric tons per hour, along with precision slurry injectors that recycle digestate. Grandfathered tariffs ensure stable cash flow, allowing equipment investment to focus on uptime and payload efficiency rather than fleet size. Consequently, haying and forage implements remain a stable anchor within Germany agricultural tractor machinery market even as new plant construction slows.

Demand for Low-HP Implements from Smallholdings

Farms under 50 hectares represent 68.5% of holdings but rely on 30 to 75 horsepower power units for daily work. Compact plows, rotovators, and modular planters allow diversified operations to mechanize irregular fields while complying with Stage V emission mandates. Lease-to-own programs from AGCO Finance and CNH Capital, offering interest rates below 3%, reduce monthly payments to less than the cost of seasonal labor. This affordability catalyzes the uptake of ISOBUS-ready implements, driving incremental gains in the Germany agricultural tractor machinery market through 2027.

Original Equipment Manufacturer (OEM) Financing below 3% Interest

Manufacturer-backed loans tie reduced rates to sustainability covenants, which are financed via European Investment Bank credit lines. Bundled telematics, extended warranties, and carbon-credit facilitation transform credit offers into service platforms. Preferential pricing steers buyers toward precision-enabled equipment whose verified savings meet policy metrics, thereby strengthening attachment rates and reducing default risk for lenders.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining average farm size | -0.60% | Bavaria and Baden-Württemberg | Long term (≥ 4 years) |

| Volatile commodity prices | -0.80% | Lower Saxony and Saxony-Anhalt grain belt | Short term (≤ 2 years) |

| High procurement cost of Stage V engines | -1.10% | National | Medium term (2-4 years) |

| Battery-raw-material sourcing risks | -0.40% | National,and electric-powered equipment initiatives | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Declining Average Farm Size

The average German holding is approximately 18 hectares, and 62% of the land is leased, which discourages capital-intensive equipment purchases by tenant farmers [4]Source: Federal Ministry of Food and Agriculture, “Guidelines for Autonomous Field Operations 2024,” BMEL.DE. Small plots favor multi-purpose or shared implements over dedicated fleets, limiting unit volumes for high-capacity machinery. While modular platforms and leasing soften the blow, persistent fragmentation subtracts momentum from Germany agricultural tractor machinery market.

High Procurement Cost of Stage V Engines

Stage V rules require diesel particulate filters and selective catalytic reduction, which increases the prices of compliant power units and any implements that must integrate electronically. Farmers often must replace both the tractor and the implement simultaneously to secure subsidy eligibility, pushing expenditures beyond their immediate budgets. Carbon Border Adjustment compliance raises steel and aluminum costs by USD 1.1-1.7 million for the Original equipment manufacturers (OEMs), further inflating retail prices.

Segment Analysis

By Product Type: Precision Sprayers Outpace Traditional Tillage Equipment

Plowing and cultivating machinery accounted for 37.5% of the Germany agricultural tractor machinery market size in 2024, reflecting broad interest in strip-till and no-till practices that qualify for soil-health insurance rebates. Sprayers are forecast to expand at a 7.9% CAGR to 2030, outstripping every other product category. Variable-rate nozzles and camera-based weed detection allow users to cut herbicide usage by 66% while meeting European Union pesticide reduction targets.

The sprayer segment’s acceleration hinges on forthcoming record-keeping mandates under the Sustainable Use of Pesticides Regulation, projected to require telemetry audits for commercial field work. The Original equipment manufacturers (OEMs) position themselves accordingly, AGCO’s PTx Trimble leverages a mixed-fleet retrofit library covering more than 10,000 models, while German specialists Amazone and Horsch roll out modular sprayers that accept third-party sensor kits. With regulatory drivers and demonstrable input savings converging, precision spraying remains the brightest growth pocket within Germany agricultural tractor machinery market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

The Germany agricultural tractor machinery market exhibits significant regional disparities, driven by variations in farm structure, cropping patterns, and policy priorities. Southern states such as Bavaria and Baden-Württemberg are characterized by small, fragmented farms, many of which operate on hilly terrain. This structure sustains demand for lower-horsepower tractors and compact implements, including plows and planters designed for maneuverability and slope stability.

In contrast, northern and eastern regions, such as Lower Saxony, Saxony-Anhalt, and Brandenburg, are characterized by large-scale grain and energy crop farming. These areas host a high concentration of biogas-linked operations, driving demand for high-capacity forage harvesters, slurry management equipment, and other heavy-duty machinery. Farmers in these regions are also among the earliest adopters of autonomous and semi-autonomous implements due to field size and labor efficiency requirements.

The western and northern coastal regions, including North Rhine-Westphalia and Schleswig-Holstein, are more heavily oriented toward dairy farming. Dense livestock populations and growing emphasis on soil health and nutrient management are encouraging investment in precision slurry applicators and conservation tillage equipment. At the same time, subsidy-supported income stability sustains machinery replacement cycles, although recent market conditions indicate farmers are prioritizing essential upgrades while postponing non-critical purchases. Regulatory intensity further amplifies regional segmentation. States with a strong focus on organic and environmentally regulated farming are accelerating the adoption of digitally enabled sprayers and compliance-oriented equipment. Meanwhile, regions with expansive field structures continue to favor high-horsepower, four-wheel-drive, and automation-ready machinery, reinforcing differentiated demand patterns across Germany agricultural tractor machinery market.

Competitive Landscape

The Germany agricultural tractor machinery market operates as a moderately concentrated market, with the top five companies collectively holding a significant market share. This high level of concentration highlights significant scale advantages in manufacturing, distribution, financing, and technology integration, while still fostering intense competitive rivalry.

AGCO Corporation secures a leading position through its extensive implement portfolio and robust digital strategy, bolstered by its PTx Trimble joint venture. This collaboration enhances mixed-fleet compatibility and accelerates the adoption of precision agriculture. Deere & Company competes vigorously with advanced automation, autonomous tillage solutions, and integrated digital platforms that prioritize continuous operation and input efficiency. CNH Industrial N.V. differentiates itself by integrating agronomic data, soil testing, and risk-management tools with its equipment sales, offering a comprehensive value proposition beyond machinery. Claas KGaA mbH maintains a strong foothold in high-capacity harvesting and forage equipment, leveraging long-standing relationships with professional German farmers. Kubota Corporation remains competitive in the compact and mid-horsepower segments, catering particularly to smaller and mixed-use farms.

Outside the top tier, companies such as SDF Group S.p.A., Yanmar Co., Ltd., Argo Tractors S.p.A., Iseki & Co., Ltd., Lindner Traktorenwerk GmbH, JC Bamford Excavators Ltd., and HTC Holdings a.s., Daedong Corporation play significant niche or regional roles. These companies often compete based on price, specialization, or compact equipment offerings. Competitive dynamics in the market are increasingly influenced by digital ecosystems rather than mechanical differentiation. Factors such as open ISOBUS compatibility, data monetization, and autonomous readiness are becoming critical purchase considerations, particularly among younger farmers. Additionally, regulatory compliance costs related to emissions and carbon policies favor well-capitalized incumbents, further consolidating the market. However, these dynamics also raise churn risks as brand loyalty diminishes in favor of technological flexibility.

Germany Agricultural Tractor Machinery Industry Leaders

-

Deere & Company

-

CLAAS KGaA mbH

-

Kubota Corporation

-

AGCO Corporation

-

CNH Industrial N.V.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2025: Horsch unveiled sensor-enabled precision tillage tools at Agritechnica 2025, strengthening Germany’s transition toward data-driven, precision-ready agricultural machinery that improves soil management and tractor efficiency.

- July 2025: Claas KGaA mbH introduced the ROLLANT 630 RC round baler, featuring a 25-knife cutting rotor, reinforced drive components, and ISOBUS connectivity. This launch highlights the increasing adoption of digitally enabled, high-efficiency forage equipment in the German agricultural tractor and machinery market.

- March 2023: Bosch BASF Smart Farming introduced camera-based sprayers integrated with Herbert Dammann equipment, enabling real-time weed detection and targeted application. The system improves herbicide efficiency by about 66% and supports the Germany agricultural machinery market’s shift toward precision, digital, and input-efficient solutions.

Germany Agricultural Tractor Machinery Market Report Scope

An agricultural tractor is a vehicle specifically designed to deliver a high tractive effort at slow speeds for the purposes of hauling a trailer or machinery. Germany's agricultural tractor market is segmented by horsepower (Less than 50 HP, 51-100 HP, 101-150 HP & Above 150 HP). The report offers market estimation and forecasts in value (USD) for the above-mentioned segments.

Plowing and Cultivating Machinery

| Plows |

| Harrows |

| Rotovators and Cultivators |

| Other Plowing and Cultivating Machinery |

Planting Machinery

| Seed Drills |

| Planters |

| Spreaders |

| Other Planting Machinery |

Haying and Forage Machinery

| Mowers and Conditioners |

| Balers |

| Other Haying and Forage Machinery |

| Plowing and Cultivating Machinery | Plows |

| Harrows | |

| Rotovators and Cultivators | |

| Other Plowing and Cultivating Machinery | |

| Planting Machinery | Seed Drills |

| Planters | |

| Spreaders | |

| Other Planting Machinery | |

| Haying and Forage Machinery | Mowers and Conditioners |

| Balers | |

| Other Haying and Forage Machinery |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is Germany agricultural tractor machinery market in 2025?

The Germany agricultural tractor machinery market size is USD 2.30 billion in 2025.

What is the projected growth rate for equipment sales through 2030?

The market value is projected to rise at a 4.80% CAGR, reaching USD 2.91 billion by 2030.

Which product segment is growing fastest?

Sprayers lead with a 7.9% CAGR on stronger regulatory push for pesticide reduction.

What role do subsidies play in equipment demand?

The German Agri-Investment Program can fund up to 75% of precision implement costs, stimulating rapid replacement cycles.

Page last updated on: