Zero Liquid Discharge (ZLD) Systems Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

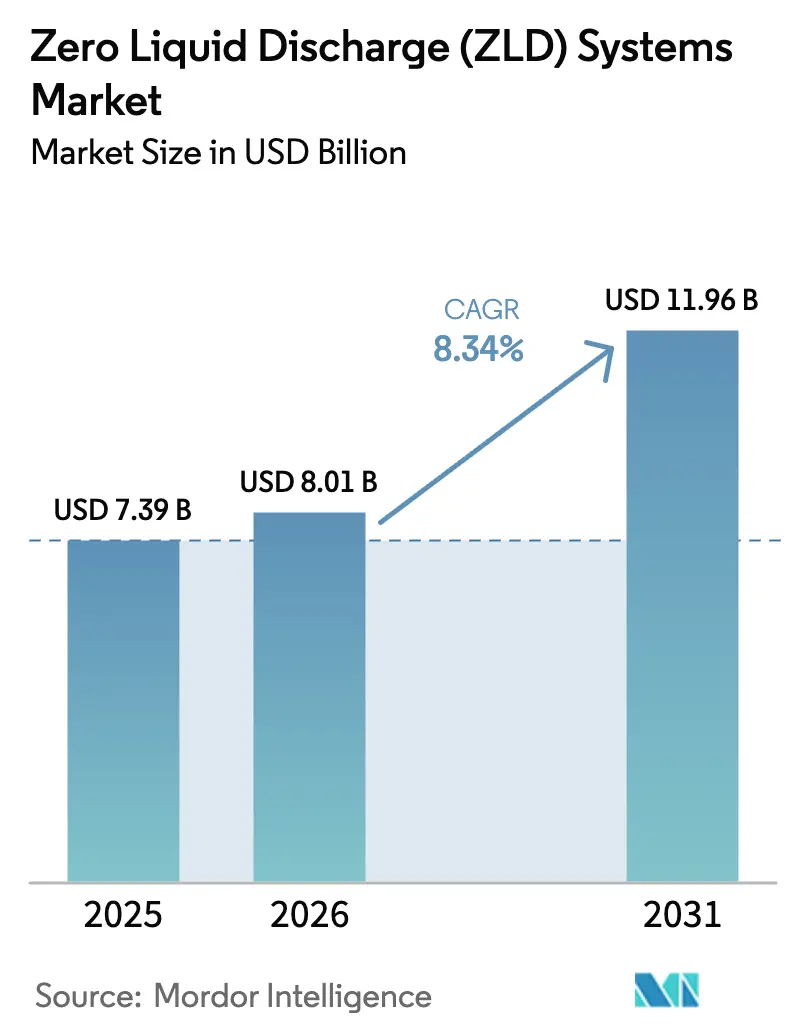

| Market Size (2026) | USD 8.01 Billion |

| Market Size (2031) | USD 11.96 Billion |

| Growth Rate (2026 - 2031) | 8.34% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Zero Liquid Discharge (ZLD) Systems Market Analysis by Mordor Intelligence

The Zero Liquid Discharge Systems Market size is expected to grow from USD 7.39 billion in 2025 to USD 8.01 billion in 2026 and is forecast to reach USD 11.96 billion by 2031 at 8.34% CAGR over 2026-2031. Rapid industrial growth in the Asia–Pacific, semiconductor water-reuse targets in East Asia, and upstream produced-water directives in the Middle East are amplifying demand, while hybrid membrane-thermal configurations are emerging as the preferred architecture where electricity costs are high. Competitive dynamics remain fluid: the top five vendors hold about 45% share, yet no single supplier exceeds 15%, creating scope for regional specialists that offer modular, rapid-deployment packages. At the same time, digital twins and remote monitoring are lowering the operations-and-maintenance expertise threshold, reducing downtime and improving levelized water costs. Although high capital outlay and energy use still restrain adoption - pushing levelized water costs above USD 5 per cubic meter in thermal-heavy plants - declining renewable-electricity prices are narrowing the gap with conventional treatment-plus-discharge.

Key Report Takeaways

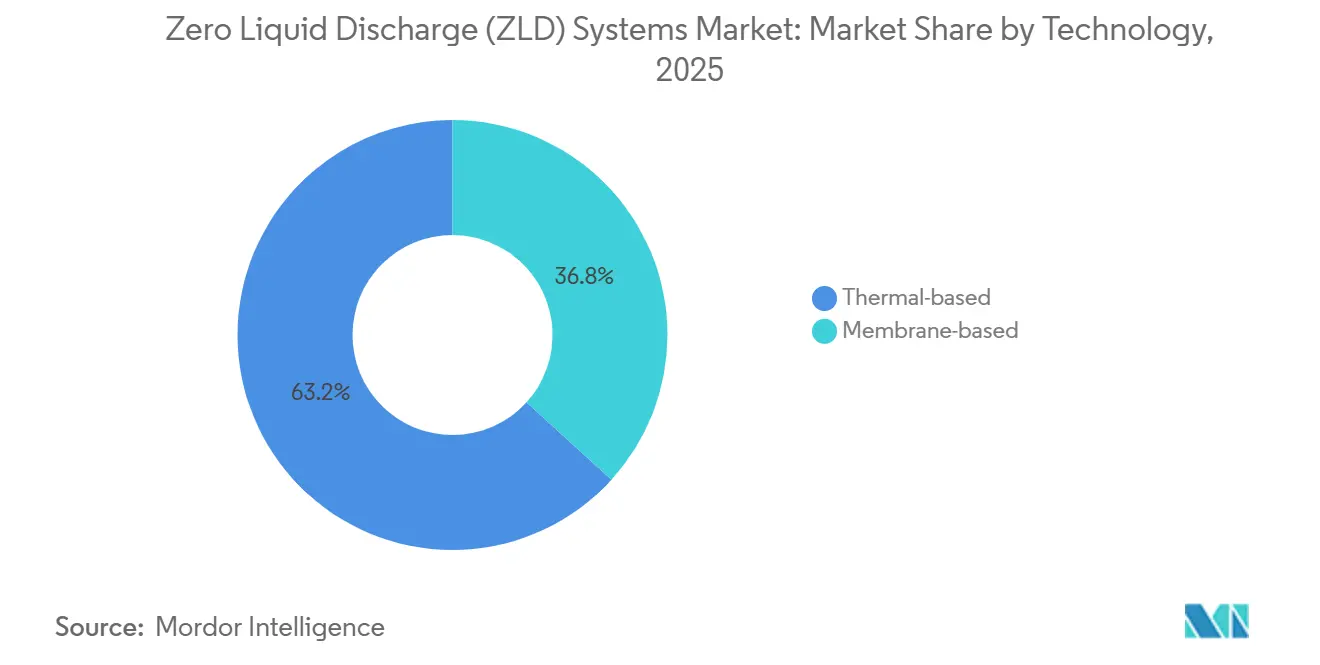

- By technology, thermal-based systems led with 63.24% revenue share in 2025; membrane-based configurations are forecast to expand at a 9.12% CAGR through 2031.

- By process phase, evaporation and crystallization accounted for a 49.48% share of the Zero Liquid Discharge systems market size in 2025, while pretreatment is advancing at a 9.35% CAGR to 2031.

- By end-user industry, power generation held 37.89% of the Zero Liquid Discharge systems market share in 2025, and it also records the highest projected CAGR at 9.42% through 2031.

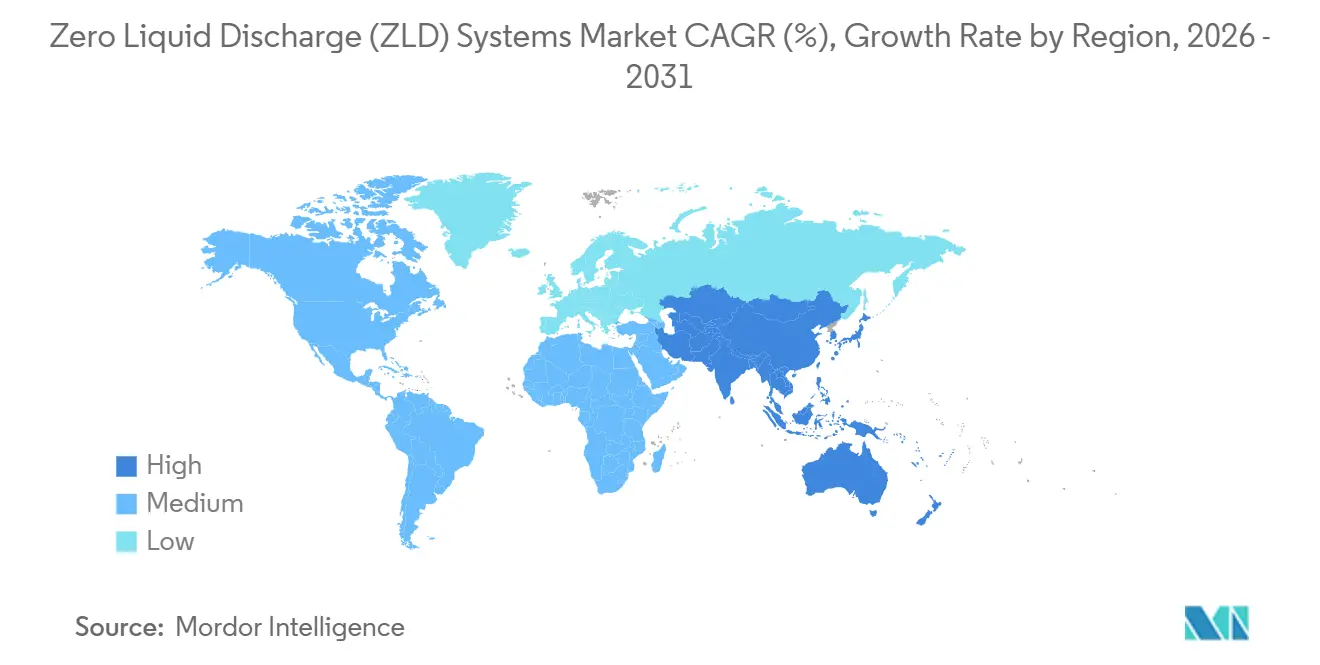

- By geography, Asia–Pacific commanded 32.67% revenue share in 2025 and is set to grow at a 9.69% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Zero Liquid Discharge (ZLD) Systems Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for freshwater in water-stressed regions | +2.3% | APAC, Middle East, Southern Europe | Medium term (2–4 years) |

| Semiconductor-grade brine-treat recycling targets | +1.5% | Taiwan, South Korea, Japan, United States | Long term (≥ 4 years) |

| Upstream produced-water reuse mandates in the Middle East | +1.2% | Saudi Arabia, UAE, Kuwait | Short term (≤ 2 years) |

| Tightening zero-effluent regulations in OECD and BRICS | +2.1% | Global, led by EU and China | Medium term (2–4 years) |

| Expansion of water-intensive process industries | +1.8% | India, China, Bangladesh, Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Freshwater in Water-Stressed Regions

Industrial withdrawals equal 19% of global freshwater use, but in basins such as the Indus, Yellow, and Murray–Darling, the share surpasses 40%, putting factories in direct competition with farms and cities[1]UN Water, “Water Use Statistics 2025,” unwater.org. Governments are responding with volumetric caps and escalating abstraction fees, making closed-loop systems financially attractive. India’s 2023 National Water Policy obliges thermal power stations in water-scarce zones to recycle 90% of process water by 2030, implicitly mandating ZLD for cooling-tower purge and flue-gas desulfurization blowdown[2]Government of India Ministry of Jal Shakti, “National Water Policy 2023,” jalshakti-india.gov.in. China’s Yangtze River Protection Law, tightened in 2024, bans new industrial discharges within 1 km of the river, pushing chemical parks toward membrane-thermal hybrids that cut steam demand by 60% compared with multi-effect evaporators. Hybrid ZLD designs that pair brine concentrators with mechanical vapor recompression crystallizers are therefore scaling fastest in water-short provinces. These configurations lower operating costs, raise water-recycling ratios, and secure plant permits, reinforcing demand for the Zero Liquid Discharge systems market across Asia–Pacific.

Semiconductor-Grade Brine-Treat Recycling Targets

Fabrication plants consume 2,000–4,000 L of ultrapure water per wafer, creating high-salinity reject streams rich in fluoride, ammonia, and silica. TSMC already recycles 92% of process water at its Hsinchu and Tainan fabs and has set a 98% target for 2028, requiring advanced ZLD pilots. South Korea introduced a semiconductor effluent limit of 500 mg/L total dissolved solids in 2025, effectively mandating brine concentration for new fabs. Intel’s Ocotillo complex in Arizona has demonstrated a forward-osmosis pretreatment that reduces reverse-osmosis energy usage by 30%, enabling cost-effective ZLD even at electricity tariffs of USD 0.08/kWh. Together, these actions anchor ZLD as a condition for fab permitting, strengthen local community support, and widen the addressable Zero Liquid Discharge systems market for high-tech manufacturing corridors.

Upstream Produced-Water Reuse Mandates in the Middle East

Saudi Arabia now requires oil producers to reuse or reinject 85% of produced water by 2027, up from 65% in 2023. Reservoir brines often exceed 150,000 mg/L total dissolved solids, necessitating thermal evaporation or high-recovery RO followed by crystallization. ADNOC awarded a USD 180 million contract in 2025 for modular ZLD units at five onshore fields, targeting zero discharge by 2029 and recovering salts for resale. Kuwait Oil Company is piloting solar-driven membrane distillation to offset the energy burden of thermal processes, leveraging intense insolation to lower operating costs. As mandates spread across Gulf Cooperation Council states, demand is shifting toward skid-mounted packages that can be relocated between wells, opening a fresh niche in the Zero Liquid Discharge systems market.

Tightening Zero-Effluent Regulations in OECD and BRICS

The EU Industrial Emissions Directive, revised in December 2024, lists ZLD as the reference technique for brine management in water-scarce member states. Germany’s Federal Environment Agency mirrored this stance in February 2025, guiding new chemical parks along the Rhine-Main and Ruhr toward ZLD adoption. China expanded its zero-discharge zone list in July 2025 to 47 industrial clusters in the Yellow River basin, enforcing compliance by 2028. Brazil tightened dissolved-solids limits for the São Francisco River basin in 2024, making conventional biological treatment obsolete for salinity control. Harmonization of discharge rules raises the compliance baseline worldwide, removing siting advantages that once favored lax jurisdictions and propelling the Zero Liquid Discharge systems market in developed and emerging regions alike.

Restraints Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and energy intensity of ZLD configurations | -1.4% | Global, acute in Sub-Saharan Africa and Latin America | Medium term (2–4 years) |

| Scarcity of skilled operations and maintenance personnel | -0.9% | APAC emerging markets, Middle East | Short term (≤ 2 years) |

| Limited fiscal incentives for water-circularity projects | -1.0% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Energy Intensity of ZLD Configurations

A 1,000 m³/day plant costs USD 8–15 million to build and consumes 50–80 kWh/m3, translating to USD 4–6/m3 operating costs at typical tariffs. Where electricity exceeds USD 0.10/kWh, and water tariffs sit below USD 1/m3 - as in South Africa - the ZLD payback stretches beyond 15 years, deterring investment unless regulators compel compliance. Argentina’s textile and tanning clusters face similar economics, with 2024 industrial water averaging USD 0.80/m3, far below ZLD break-even levels. Mechanical vapor recompression and hybrid membrane-thermal systems can cut energy consumption by 50%, but steep upfront premiums and sensitivity to fouling limit uptake to well-capitalized users. Consequently, financing hurdles remain a drag on the Zero Liquid Discharge systems market.

Scarcity of Skilled Operations and Maintenance Personnel

ZLD plants require tight control of scaling, antiscalant dosing, and crystallizer performance; yet 62% of operators in India, Indonesia, and Vietnam report difficulty hiring technicians versed in both membrane and thermal technologies. Saudi Aramco notes that ZLD facilities demand 30% more maintenance labor than conventional separators, driving its investment in predictive analytics. Veolia’s 2025 digital-twin platform trims on-site staffing by 20%, while Siemens and Xylem embed machine-learning algorithms that adjust antiscalant dosage and cleaning cycles automatically. Even so, greenfield projects often face commissioning delays as local teams ramp up skills, extending project timelines and curbing short-term growth in the Zero Liquid Discharge systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Hybrid Designs Erode Thermal Dominance

Thermal-based units retained 63.24% of the Zero Liquid Discharge systems market share in 2025 because multi-effect evaporators handle brines above 100,000 mg/L without membrane fouling. Waste-heat integration in power and petrochemical complexes further improves economics, anchoring continued demand. Nonetheless, membrane-centric packages are advancing at a 9.12% CAGR through 2031 as electricity costs rise and renewable power becomes abundant. Reverse osmosis coupled with forward osmosis or electrodialysis concentrates brine to 150,000 mg/L at just 30–40 kWh/m3, half that of conventional thermal routes. DuPont’s 2025 high-rejection RO element extends lifespan to seven years in Chinese dye-house pilots, lowering replacement cost and reinforcing the shift toward membranes. Hybrid RO-plus-crystallizer plants now dominate greenfield bids, offering lower levelized water costs and design flexibility, a trend that underpins growth in the Zero Liquid Discharge systems market across high-electricity regions.

Second-order impacts are equally material. Membrane adoption reduces steam-cycle complexity, enabling containerized and skid-mounted footprints that accelerate deployment in upstream oilfields. Vendors that integrate digital monitoring - predicting fouling and optimizing cleaning - are differentiating offerings without cutting prices, a strategy that shields margins even as membrane costs fall. Collectively, these factors point to a gradual but meaningful rebalancing of the Zero Liquid Discharge systems market size in favor of membrane-dominant configurations over the forecast horizon.

By Process Phase: Pretreatment Surges Amid Fouling Concerns

Evaporation and crystallization consumed 49.48% of the Zero Liquid Discharge systems market size in 2025 because they embody the capital-heavy end stage that converts concentrated brine into solids. Yet pretreatment spending is growing 9.35% annually, reflecting recognition that upstream fouling control governs downstream uptime and energy demand. Plants are deploying antiscalants, multimedia filtration, and ion-exchange polishing to shield RO membranes and heat-exchanger surfaces from calcium sulfate, silica, and organics. Brine-concentration steps - RO and electrodialysis - are expanding in tandem, minimizing the flow that reaches thermal units and thus trimming energy costs. Innovation is moving into solids handling: Saltworks Technologies launched eutectic freeze crystallization in 2025, enabling saleable sodium chloride and sulfate streams while slashing landfill fees. As operators chase value recovery and circular-economy goals, comprehensive lifecycle calculations increasingly favor investments beyond the traditional evaporator-focused core, a dynamic that broadens the addressable Zero Liquid Discharge systems market.

Upfront pretreatment also accelerates plant commissioning by standardizing feedwater quality, making modular plants feasible for small and medium users. Vendors that bundle chemical dosing, rapid media exchange, and cloud diagnostics are shortening payback periods, tilting procurement specifications toward integrated platforms. These shifts underscore why pretreatment now stands out as the fastest-growing internal segment of the Zero Liquid Discharge systems market.

By End-User Industry: Power Generation Leads but Pharmaceuticals Accelerate

Power generation captured 37.89% of the Zero Liquid Discharge systems market share in 2025 and continues to top growth tables with a 9.42% CAGR as India, China, and Indonesia build coal and combined-cycle stations under water-scarcity constraints. Integrated ZLD sidesteps retrofit headaches and secures water permits, making it standard in new projects. In oil and gas, modular systems shrink trucking mileage for produced water, aligning with carbon-reduction goals and lowering disposal fees. Chemicals and petrochemicals face converging EU REACH rules and Chinese park consolidation that embed ZLD within environmental risk management. Mining firms deploy ZLD to mitigate acid-mine drainage; BHP’s Escondida retrofit in 2025 eliminated 1.2 million m³/year of pond discharge, supporting community relations.

Pharmaceutical producers, a minor slice today, are scaling fastest after the U.S. Food and Drug Administration tightened effluent limits for endocrine disruptors in 2025, compelling active-drug separation before discharge. ZLD satisfies both compliance and corporate ESG targets, especially where plants rely on scarce municipal supplies. Food and beverage, along with pulp-and-paper operators, are piloting containerized units as water tariffs climb. This diversification reduces concentration risk and expands the Zero Liquid Discharge systems market size across a broader client base than a decade ago.

Geography Analysis

Asia-Pacific commanded 32.67% of global revenue in 2025 and is forecast to grow at a 9.69% CAGR through 2031, underpinned by stringent basin-wide discharge bans in China’s Yellow River corridor and India’s multi-river clean-up mission. China shut 23 non-compliant chemical plants in 2025, triggering retrofit orders across Shanxi and Inner Mongolia. India’s extension of ZLD mandates to facilities within 10 km of major rivers affects more than 4,200 plants, propelling domestic EPC order books. Japan and South Korea subsidize fab-level water reuse; Japan set aside USD 120 million in 2025 to reach 95% reuse by 2030, accelerating procurement of high-purity ZLD modules. ASEAN incentives, such as Vietnam’s 2 percentage-point corporate-tax discount for zero-discharge sites, extend growth to export-oriented clusters.

North America retains a large installed base owing to shale-gas water reuse and California’s 80% industrial-recycle mandate. Chevron recycled 78% of Permian produced water in 2025 and targets 90% by 2028 via ZLD pilots. California broadened recycled-water requirements to refineries and chemical plants in 2025, driving EPC backlog. Canada trials ZLD in oil-sands tailings ponds to shorten reclamation timelines. Mexico raised industrial water tariffs 35% in 2024, tipping brewery and auto-plant economics toward closed-loop recovery. Robust capital markets and mature EPC capacity accelerate deployment across the continent.

Europe’s uptake hinges on the Industrial Emissions Directive and local abstraction caps. Germany’s Rhine-Main chemical complex leads retrofits, while France’s variable salinity levy nudges inland firms toward ZLD. The UK tightened permits for coastal desalination concentrator brines in 2025, demanding either dilution or ZLD to protect marine ecosystems. Italy designated 12 zero-discharge industrial zones in the Po basin in mid-2025, giving incentives for textiles and ceramics plants. South America concentrates activity in Brazil’s São Francisco basin, where 18 mines added ZLD in 2025 to secure licenses. In the Middle East and Africa, Saudi Arabia and the UAE drive demand through produced-water mandates, while South African mines deploy ZLD to manage acid-mine drainage despite high electricity tariffs.

Competitive Landscape

The Zero Liquid Discharge systems market is moderately fragmented. Competition revolves around three axes. First, energy efficiency: vendors that leverage mechanical vapor recompression or integrate waste-heat recovery offer 25–40% lower operating costs, capturing premium margins. Second, modularization: skid-mounted units sized 250–750 m³/day allow rapid field deployment in oilfields and small chemical parks, an arena where Praj Industries and Saltworks Technologies excel through containerized designs financed on a water-as-a-service model. Third, digital integration: Siemens’ May 2025 AI-driven brine optimizer trims antiscalant use by 18% and extends membrane life, differentiating bids even when capex is higher. Longer term, digital twins and outcome-based contracts (volume-of-water-recovered pricing) may shift risk from owners to suppliers, boosting recurring revenue. Vendors expanding service portfolios position themselves to capture annuity streams while intensifying customer lock-in. Consequently, although consolidation has inched upward, competitive intensity remains high and innovation pipelines robust.

Zero Liquid Discharge (ZLD) Systems Industry Leaders

Veolia Water Solutions & Technologies

GEA Group Aktiengesellschaft

Aquatech

ALFA LAVAL

Xylem

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Veolia Water Technologies won a USD 95 million EPC-O contract for a 3,500 m³/day ZLD plant at a petrochemical complex in Jubail, Saudi Arabia, integrating RO, mechanical vapor recompression, and crystallization with 98% water-recovery targets.

- November 2025: Thermax Limited formed a joint venture with Mitsubishi Heavy Industries to co-develop modular ZLD units for ASEAN textile and food-processing plants; the first 500 m³/day pilot launched in Ho Chi Minh City in Dec 2025.

- September 2025: Aquatech International completed a USD 72 million ZLD retrofit at a coal-fired station in Gujarat, India, reducing freshwater withdrawal by 1.5 million m³ /year through 95% water recovery and salt crystallization.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the zero-liquid-discharge (ZLD) systems market as the revenue generated from complete, factory-built or field-assembled installations whose integrated pretreatment, concentration, and crystallization steps yield a solid residue and recyclable water stream that meets prevailing discharge norms. Associated engineering, commissioning, and aftermarket services tied directly to a specific ZLD unit fall inside the scope.

Scope exclusion: modular skid packages sold only for reverse-osmosis brine concentration without a crystallizer are left out.

Segmentation Overview

- By Technology

- Thermal-based

- Membrane-based

- By Process Phase

- Pretreatment

- Brine Concentration

- Evaporation and Crystallization

- Solids Handling and Disposal

- By End-user Industry

- Power Generation

- Oil and Gas

- Chemicals and Petrochemicals

- Metallurgy and Mining

- Pharmaceuticals

- Other End-user Industries

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Analysts spoke with plant engineers in power, chemicals, and textiles; EPC contractors that integrate ZLD trains; and regional regulators across North America, India, China, and the GCC. These dialogues verified typical capacity brackets, energy consumption benchmarks, and upcoming policy triggers, while also stress-testing pricing curves derived from desk work.

Desk Research

We first gathered foundational figures on industrial water withdrawal, power capacity additions, and effluent norms from tier-1 public sources such as the US EPA, India's Central Pollution Control Board, Eurostat Water Statistics, and UN Water. Trade association white papers from the International Desalination Association, American Chemistry Council, and World Steel Association supplied technology penetration and plant-level water intensity ratios. Company filings, investor decks, and reputable business media captured order backlogs and average selling prices. Subscription platforms, notably Dow Jones Factiva for deal flows and D&B Hoovers for vendor financials, enriched firm-side data. The sources cited above are illustrative; many additional references were consulted during validation.

Market-Sizing & Forecasting

A top-down construct starts with industrial wastewater volumes by sector and region, applies mandated or voluntary ZLD penetration rates, and multiplies by weighted capital cost per cubic meter per day capacity. Select bottom-up checks, supplier order books, channel interviews, and sampled ASP × volume for large projects refine totals. Key variables modeled include new coal and gas power capacity (GW), high-TDS chemical output (million tons), regional water-scarcity indices, average capital cost per m³/day, and grid electricity price trends influencing thermal versus membrane mix. Multivariate regression links these drivers to historical install revenue and projects through 2030; scenario analysis tests policy acceleration and energy price shocks. Gaps in bottom-up data, especially for privately financed plants, are bridged using regional analogs endorsed by interviewed experts.

Data Validation & Update Cycle

Outputs pass variance checks against independent water reuse ratios and vendor shipment logs. Senior analysts review anomalies, re-engage sources if deviations exceed preset bands, and approve only convergent ranges. Reports refresh each year, with interim updates triggered by large regulatory moves or megaproject awards.

Why Our Zero Liquid Discharge Systems Baseline Earns Stakeholder Trust

Published estimates often diverge because firms slice the wastewater universe differently, choose unique price decks, or refresh at uneven intervals.

Key gap drivers in this field include whether pharmaceutical and mining users are counted, how hybrid-system learning curves temper capital costs, and the cadence at which currency conversions and inflation resets are applied. Mordor's disciplined scope, variable selection, and annual refresh cadence minimize these skews, giving decision-makers a stable anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.98 B (2025) | Mordor Intelligence | |

| USD 7.80 B (2024) | Global Consultancy A | Excludes pharma and mining segments; regional split limited to three super-regions; update cycle every three years |

| USD 7.06 B (2025) | Industry Journal B | Uses install count × average cost only for thermal systems; keeps currency at 2020 rates |

| USD 9.03 B (2025) | Regional Consultancy C | Adds ancillary O&M services; assumes fast hybrid uptake without policy cross-check; single-scenario CAGR |

The comparison shows that when scope is either narrower or inflated with peripheral revenue, totals swing markedly. By anchoring calculations to clearly documented wastewater volumes, verified penetration ratios, and live price points, Mordor Intelligence delivers a balanced, transparent baseline clients can reproduce and defend.

Key Questions Answered in the Report

What is the projected value of the Zero Liquid Discharge systems market in 2031?

The market is projected to reach USD 11.96 billion by 2031, expanding at an 8.34% CAGR.

Which segment currently holds the largest Zero Liquid Discharge systems market share?

Thermal-based technology led with a 63.24% share in 2025.

Why is Asia–Pacific the fastest-growing region for Zero Liquid Discharge deployment?

Regulatory discharge bans and rapid industrialization drive a 9.69% regional CAGR.

How are semiconductor companies influencing Zero Liquid Discharge adoption?

Fab operators in Taiwan, South Korea, and the United States are targeting 98% water reuse, embedding ZLD into permitting.

What is the main restraint limiting Zero Liquid Discharge uptake?

High capital and energy costs push levelized water prices above USD 5/m³ in thermal-heavy plants.

Which technology trend is lowering operational barriers for Zero Liquid Discharge owners?

Digital twins and AI-driven control systems reduce skilled-labor requirements and cut downtime.

Page last updated on: