Workplace Stress Management Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

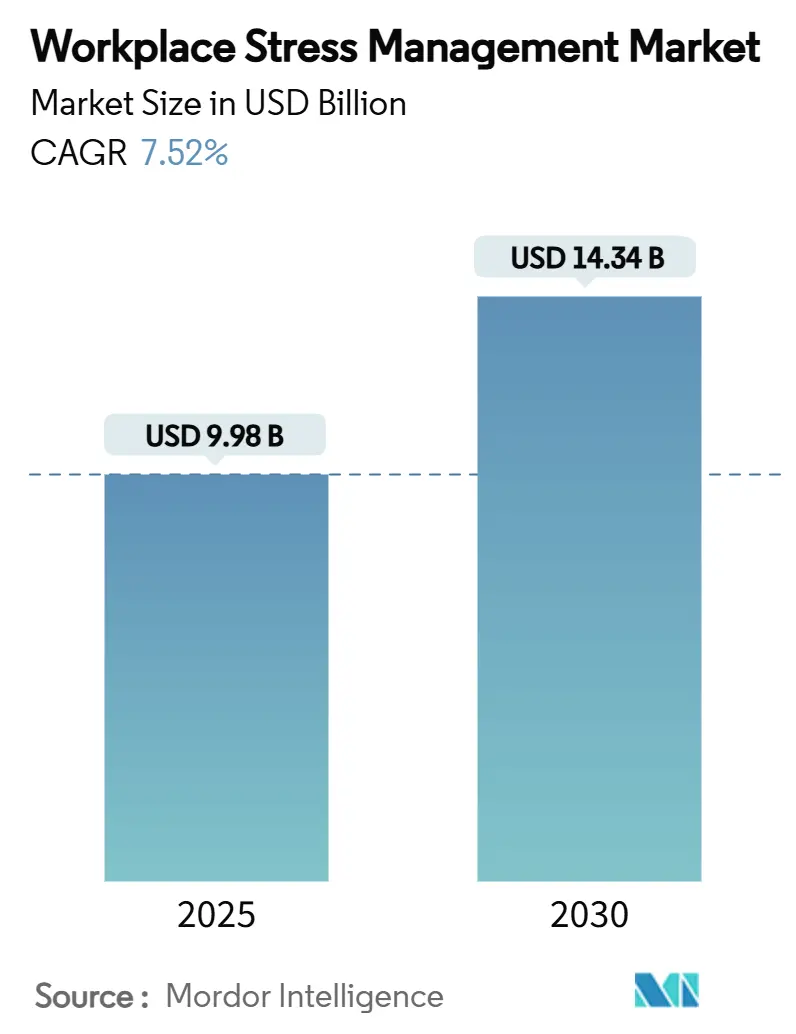

| Market Size (2025) | USD 9.98 Billion |

| Market Size (2030) | USD 14.34 Billion |

| Growth Rate (2025 - 2030) | 7.52% CAGR |

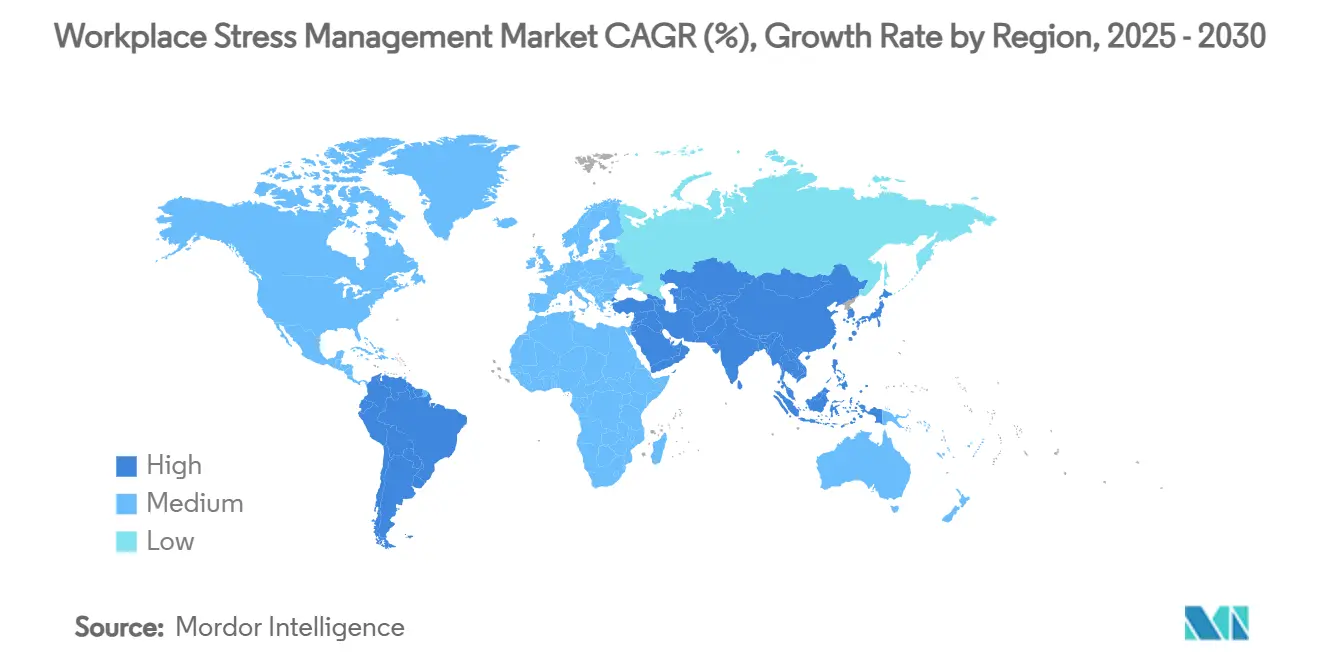

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Workplace Stress Management Market Analysis by Mordor Intelligence

The workplace stress management market size stands at USD 9.98 billion in 2025 and is projected to reach USD 14.34 billion by 2030, reflecting a 7.52% CAGR. Executive teams acknowledge that employee mental health shapes productivity, absenteeism, and healthcare outlays, so program budgets are moving from discretionary spending to strategic investment. Regulatory mandates on psychological safety, insurance premium incentives for wellness participation, and the spread of cortisol-detecting wearables are accelerating adoption. Return-on-investment studies show gains of USD 1.17–4.33 per dollar spent on wellness, reinforcing finance departments’ willingness to fund scalable platforms.[1]Ron Z. Goetzel, “Estimating the Return-on-Investment From Changes in Employee Health Risks,” Journal of Occupational and Environmental Medicine, journals.lww.com Meanwhile, high-profile data-privacy rulings prompt vendors to refine consent protocols, strengthening trust in digital solutions. Together, these forces fuel consistent demand across industries, company sizes, and regions, ensuring sustained expansion in the workplace stress management market.

Key Report Takeaways

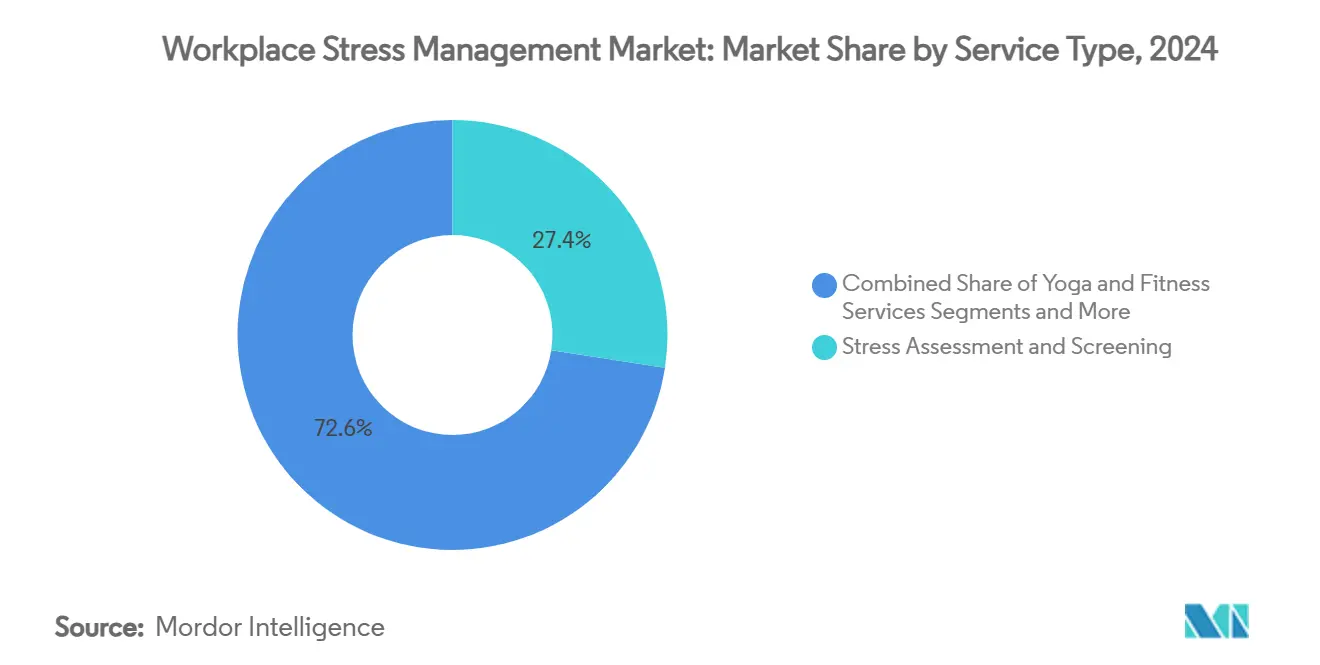

- By service type, Stress Assessment & Screening led with 27.44% of workplace stress management market share in 2024, while Digital Self-Help & Mobile Apps are forecast to advance at an 11.23% CAGR through 2030.

- By delivery mode, the On-site model accounted for a 44.37% share of the workplace stress management market size in 2024, yet Virtual and Digital-only services exhibit the fastest growth at 11.74% CAGR.

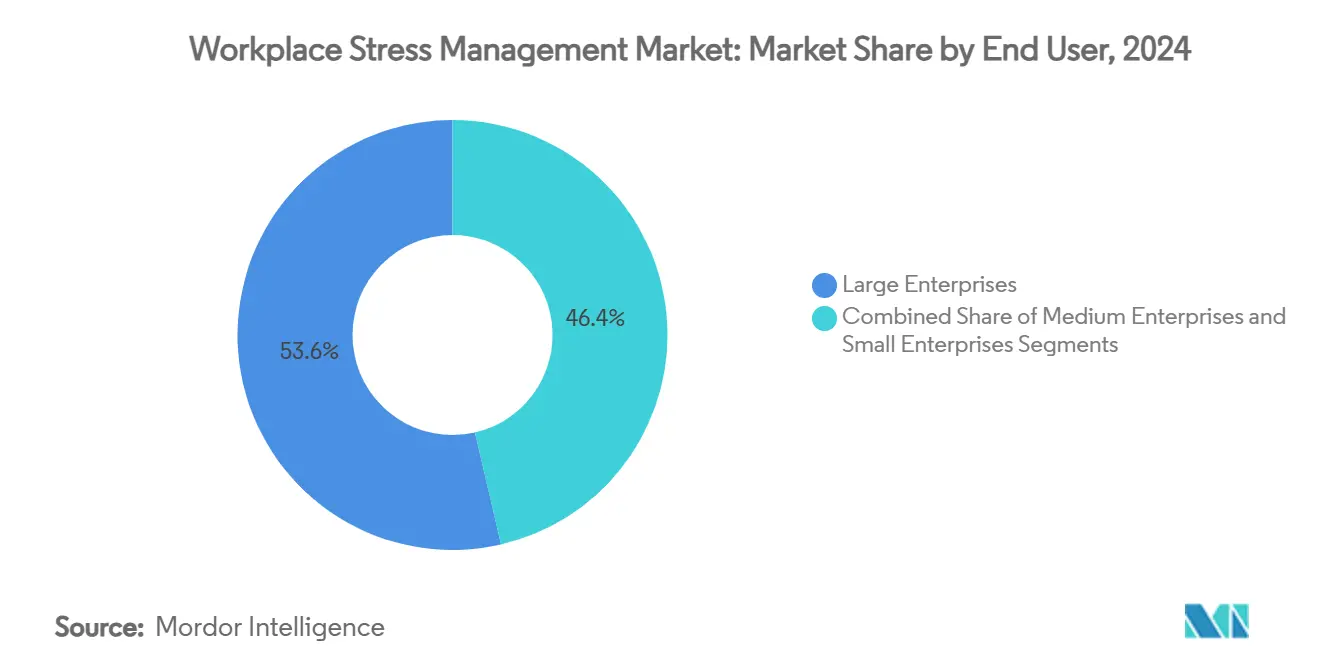

- By end user, Large Enterprises held 53.63% of the workplace stress management market in 2024, whereas Small Enterprises are expanding at a 9.46% CAGR to 2030.

- By industry vertical, IT & Telecom contributed 21.36% revenue share in 2024, while Retail & E-commerce is poised to grow at a 10.78% CAGR through 2030.

- North America captured 34.68% of workplace stress management market share in 2024; Asia-Pacific registers the highest regional CAGR at 9.62% through 2030.

Global Workplace Stress Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating healthcare costs of stress | +1.8% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| Mandatory H&S mental-wellbeing regulations | +1.2% | North America, Europe, Australia, expanding in Asia-Pacific | Long term (≥ 4 years) |

| Proven 3–4× ROI of corporate wellness spend | +1.5% | Global, led by developed markets | Short term (≤ 2 years) |

| Hybrid/remote work intensifying burnout | +1.1% | Global, especially North America and Europe | Medium term (2–4 years) |

| Wearable cortisol analytics in programs | +0.9% | North America and EU early adoption, Asia-Pacific following | Long term (≥ 4 years) |

| Insurer premium rebates tied to stress KPIs | +0.7% | North America leading, spreading to other developed regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Escalating Healthcare Costs Of Stress

Direct and indirect stress-related expenditures now approach USD 16,000 per covered employee, with lost productivity adding USD 530 billion annually to employer burdens.[2]“Worksite Wellness ROI,” UR Medicine, rochester.edu Absenteeism, presenteeism, and turnover equal 12–15% of payroll, prompting finance leaders to demand preventive action. Five-year program data show cardiovascular risk falling in 48% of participants, translating to significant claims deflection. As self-insured firms shoulder medical costs, the workplace stress management market becomes a fiscal safeguard rather than a discretionary perk. Leadership views these programs as a hedge against rising insurance premiums, cementing long-term funding.

Mandatory H&S Mental-Wellbeing Regulations

Legislators are elevating psychological safety to the same footing as physical safety. Australia’s 2024 psychosocial hazard code compels employers to mitigate fatigue and harassment. Victoria’s new regulations mirror this approach, while U.S. parity-act enforcement requires granular comparative analyses of mental-health coverage. Compliance audits and potential penalties convert optional wellness offerings into mandatory risk-management tools. Vendors that embed evidence-based protocols and audit-ready reporting gain preference, widening the workplace stress management market among regulated industries.

Proven 3-4× ROI Of Corporate Wellness Spend

Peer-reviewed case studies show USD 4.33 returned for each dollar invested at a regional grocery chain, saving USD 285,706 across three years. Highmark’s four-year evaluation found USD 1.66 saved per dollar spent, reinforcing consistent financial upside. Publications from the Society of Actuaries corroborate these findings, giving CFOs confidence. Quantifiable savings accelerate budget approvals, scaling adoption among cost-conscious sectors. The workplace stress management market therefore benefits from hard financial evidence as much as from social responsibility narratives.

Hybrid/Remote Work Intensifying Burnout

Flexible work promised balance but instead blurred boundaries, raised digital presenteeism, and heightened isolation. Studies show nearly half of remote employees report burnout from nonstop connectivity.[3]Leonie Hallo, “Experiences and Views on Hybrid Working,” MDPI, mdpi.com Hybrid teams face coordination strain and fairness perceptions between on-site and remote staff, further elevating stress. Employers now add virtual coaching and peer-support communities to Employee Assistance Programs, driving demand for platforms that seamlessly serve distributed workforces. This shift underpins rapid growth of virtual delivery modes across the workplace stress management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified stress counselors | –1.4% | Global, most acute in rural and underserved areas | Long term (≥ 4 years) |

| Low SME awareness in emerging economies | –0.8% | Asia-Pacific, Latin America, Africa | Medium term (2–4 years) |

| Data-privacy pushback on biometric tracking | –1.1% | Europe, North America, spreading globally | Short term (≤ 2 years) |

| Program fatigue reducing engagement | –0.9% | Global, particularly in mature markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Shortage Of Certified Stress Counselors

More than 152 million Americans live in mental-health shortage areas, leaving only one provider for every 350 individuals seeking help. Psychiatrist shortfalls could reach 31,000 by 2025, and three-quarters of current practitioners report burnout. Rural regions feel the pinch most, as low reimbursement rates deter specialists. Workplace programs therefore rely on AI chatbots, peer networks, and asynchronous platforms. Although these tools extend reach, clinical oversight remains essential, so supply constraints will weigh on the workplace stress management market for years.

Data-Privacy Pushback On Biometric Tracking

The UK Information Commissioner required Serco Leisure to halt unlawful biometric monitoring, setting a strict precedent on consent. EU rules mandate proportionality and consultation before collecting worker biometrics. Scholars warn that cognitive-monitoring devices may breach dignity rights. In response, vendors adopt privacy-by-design frameworks and granular opt-in mechanisms. However, fear of surveillance curbs uptake of the most data-intensive solutions, moderating growth in the workplace stress management market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Solutions Drive Market Evolution

The Stress Assessment & Screening segment commanded a 27.44% share of workplace stress management market size in 2024, yet Digital Self-Help & Mobile Apps are gaining fastest with an 11.23% CAGR. Enterprises appreciate app-based interventions because they fit varied shift patterns and allow anonymous access. Mindfulness and meditation libraries, CBT micro-modules, and AI-guided chat deliver high-frequency touchpoints at low marginal cost. Evidence from randomized trials shows clinically significant stress reduction, helping procurement teams defend investment decisions. Employers in IT, financial services, and healthcare increasingly insist on outcome dashboards that integrate biometric data, app usage, and survey scores.

Yoga and fitness classes hold moderate appeal but face commoditization as streaming options proliferate. Bio-feedback and wearable-integrated coaching are converging with software ecosystems, connecting cortisol sensors directly to personalized content queues. Employee Assistance Programs evolve into orchestrated care pathways that escalate cases from self-help to counseling, reflecting maturation of the workplace stress management market. Vendors able to curate a unified service stack that spans assessment, intervention, and outcome reporting win multi-year master contracts.

By Delivery Mode: Virtual Transformation Accelerates

The On-site model delivered 44.37% of workplace stress management market share in 2024, but Virtual and Digital-only platforms now register an 11.74% CAGR as hybrid work normalizes. Cloud-based video therapy, mobile push coaching, and VR-enabled relaxation labs remove geographic barriers and cut travel time. Procurement teams measure success by session completion rates and longitudinal biomarker trends, both facilitated by digital channels. Early adopters report participation rates doubling after shifting to virtual formats, especially among distributed engineering and customer-service teams.

Off-site retreats and boot camps see declining budgets because companies favor continuous micro-support over episodic events. Blended models gain traction, combining annual wellness days with year-round app access. Vendors refine content localization, time-zone scheduling, and accessibility features to reach multi-region workforces. As corporate real-estate footprints shrink, virtual delivery will account for a growing portion of workplace stress management market revenues.

By End User: Small Enterprise Adoption Accelerates

Large Enterprises accounted for 53.63% of workplace stress management market size in 2024 owing to established HR infrastructures and self-insured health plans. Small Enterprises, however, expand at a 9.46% CAGR as turnkey SaaS platforms lower entry barriers. Subscription tiers priced per employee simplify budgeting, and usage analytics justify renewals. Pilot programs among firms with fewer than 200 staff show turnover reductions of 12% within one year.

Case studies such as the Yokohama Linkworker Project prove that public-private outreach can lift small-business participation rates. Governments in Japan, Singapore, and Australia offer tax rebates for certified wellness spending, further spurring adoption. Vendors cater to small-enterprise needs with plug-and-play assessments, bite-sized training, and integrated payroll deductions for premium features. These developments widen the total addressable market for workplace stress management solutions.

By Industry Vertical: Technology Sector Leadership Evolves

IT & Telecom companies generated 21.36% revenue in 2024, reflecting high cognitive workloads, tight release cycles, and always-on support models. Top employers provide app-based mindfulness breaks, VR decompression pods, and data-driven workload balancing. These innovations help contain attrition in a competitive talent market. Retail & E-commerce, growing at a 10.78% CAGR, faces stress from customer-facing conflicts, seasonal demand spikes, and dispersed store networks. Employers deploy mobile counseling and shift-scheduling analytics to reduce overtime-induced burnout.

Healthcare and life-sciences firms show strong uptake as staff manage both patient care stress and regulatory audits. BFSI institutions integrate stress dashboards with risk-management systems, because trader fatigue can trigger costly errors. Manufacturing plants adopt wearable sensors to link stress levels with safety metrics, cutting incident rates. Education, government, and public-sector bodies invest to curb teacher and civil-servant burnout, which undermines service delivery. Cross-industry momentum underscores the universal relevance of the workplace stress management market.

Geography Analysis

North America holds 34.68% of workplace stress management market share due to parity-law enforcement, mature Employee Assistance Program ecosystems, and insurer rebate schemes. U.S. employers provide EAP access to 53% of workers, yet utilization averages only 7% because of stigma and awareness gaps. Canadian firms focus on productivity rather than cost shifting, given universal healthcare coverage. State-level rules in California and New York drive compliance spending, while federal audits intensify data-reporting needs across sectors. The region continues to pilot biometric analytics, reinforcing demand for integrated platforms in the workplace stress management market.

Europe shows steady growth anchored in GDPR-compliant wellness solutions and recognition of wellbeing as a labor right. Nordic employers pair generous leave policies with digital mindfulness coaching, achieving high engagement. EU directives require worker consultation when implementing monitoring tech, so vendors promote privacy dashboards and anonymized analytics. Brexit complicates cross-border service delivery, yet UK firms still push ahead with stress analytics to offset tight labor pools. The forthcoming AI Act will shape data governance, but most vendors have aligned roadmaps, sustaining momentum in the workplace stress management market.

Asia-Pacific posts the fastest CAGR at 9.62% through 2030 as rapid industrialization raises workforce stress. Japan and South Korea invest in digital counseling to support aging employees, while Australia enforces psychosocial safety codes, making compliance non-negotiable. In Southeast Asia, only 29.04% of staff know about EAP options, exposing vast unmet need. Cultural stigma steers demand toward anonymous mobile apps, and government SME digitalization grants fund onboarding. Advanced sensor exports from Taiwan and Korea further integrate hardware into software ecosystems, accelerating the workplace stress management market across the region.

Competitive Landscape

The workplace stress management market remains highly fragmented. Traditional EAP leaders such as ComPsych and ICAS World compete with digital-first entrants including BetterUp, Modern Health, and Headspace for Work. Insurers like UnitedHealthcare bundle mental-health modules with medical plans, leveraging claims data to refine offerings. Three strategic models emerge. End-to-end platform providers deliver assessment, intervention, and analytics under one contract. Point-solution specialists focus on niches such as VR-based CBT or biometric feedback. Integrated healthcare organizations embed stress management into primary care networks, simplifying patient referrals.

Technology partnerships drive differentiation. Wearable makers align with software vendors to offer real-time cortisol dashboards. Employers seek vendors that prove clinical efficacy through peer-reviewed trials and publish transparent privacy policies. M&A activity signals consolidation; Wellhub’s acquisition of Urban Sports Club extends hybrid wellness portfolios across Europe. Concentra’s SEC filing reveals a network of 547 centers and 151 onsite clinics, highlighting occupational-health players’ expansion ambitions. Price pressure intensifies, but vendors that document ROI and regulatory compliance secure multi-year renewals, shaping future leadership in the workplace stress management market.

Workplace Stress Management Industry Leaders

ComPsych Corporation

Personify Health

UnitedHealthcare

Lyra Health

TELUS Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Infosys partnered with Mental Health Foundation Australia to launch the “Supportive Mind” mobile app aimed at providing real-time mental health resources in Australia and New Zealand.

- March 2025: Wellhub completed the acquisition of Urban Sports Club, expanding European reach and integrating physical and mental wellness services to address rising employee stress.

- October 2024: Vail Resorts doubled mental-health benefit access for seasonal and permanent staff, signaling employer commitment to retention through wellbeing support.

Global Workplace Stress Management Market Report Scope

| Stress Assessment & Screening |

| Mindfulness & Meditation Programs |

| Yoga & Fitness Services |

| Cognitive Behavioural Therapy (CBT) Workshops |

| Employee Assistance Programs (EAP) |

| Digital Self-Help & Mobile Apps |

| Bio-feedback & Wearable-integrated Coaching |

| On-site (In-person) |

| Off-site Retreat / Boot-camp |

| Virtual / Digital-only |

| Blended / Hybrid |

| Large Enterprises ( > 1,000 employees) |

| Medium Enterprises (100-999) |

| Small Enterprises ( < 100) |

| IT & Telecom |

| Healthcare & Life-sciences |

| BFSI |

| Manufacturing |

| Retail & E-commerce |

| Education |

| Government & Public Sector |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Stress Assessment & Screening | |

| Mindfulness & Meditation Programs | ||

| Yoga & Fitness Services | ||

| Cognitive Behavioural Therapy (CBT) Workshops | ||

| Employee Assistance Programs (EAP) | ||

| Digital Self-Help & Mobile Apps | ||

| Bio-feedback & Wearable-integrated Coaching | ||

| By Delivery Mode | On-site (In-person) | |

| Off-site Retreat / Boot-camp | ||

| Virtual / Digital-only | ||

| Blended / Hybrid | ||

| By End User | Large Enterprises ( > 1,000 employees) | |

| Medium Enterprises (100-999) | ||

| Small Enterprises ( < 100) | ||

| By Industry Vertical | IT & Telecom | |

| Healthcare & Life-sciences | ||

| BFSI | ||

| Manufacturing | ||

| Retail & E-commerce | ||

| Education | ||

| Government & Public Sector | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current valuation of the workplace stress management market?

The workplace stress management market size is USD 9.98 billion in 2025 and is forecast to reach USD 14.34 billion by 2030.

Which region leads revenue generation for workplace stress programs?

North America contributes 34.68% of revenue due to parity regulations, insurer incentives, and mature wellness cultures.

Which service type is growing fastest?

Digital Self-Help & Mobile Apps are expanding at an 11.23% CAGR as employers favor scalable, on-demand tools.

Why are small enterprises adopting stress management platforms?

Turnkey SaaS pricing, tax incentives, and talent-retention pressures push small firms to embrace affordable wellness options.

How do regulations influence purchasing decisions?

New psychosocial safety codes and parity-law audits make structured stress programs a compliance necessity rather than a discretionary perk.

What role do wearables play in stress management?

Real-time cortisol and HRV data feed personalized coaching, improving early intervention effectiveness and program ROI.

Page last updated on: