Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

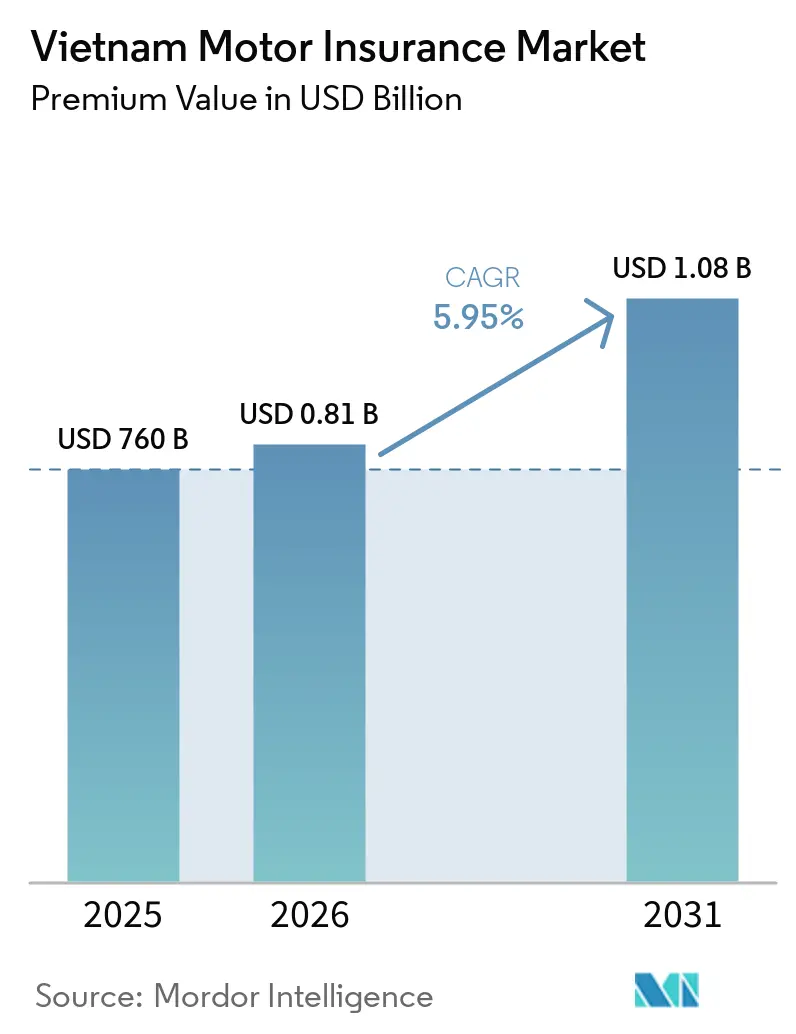

| Base Year Market Size (2025) | USD 760 Billion |

| Market Size (2026) | USD 0.81 Billion |

| Market Size (2031) | USD 1.08 Billion |

| Growth Rate (2026 - 2031) | 5.95% CAGR |

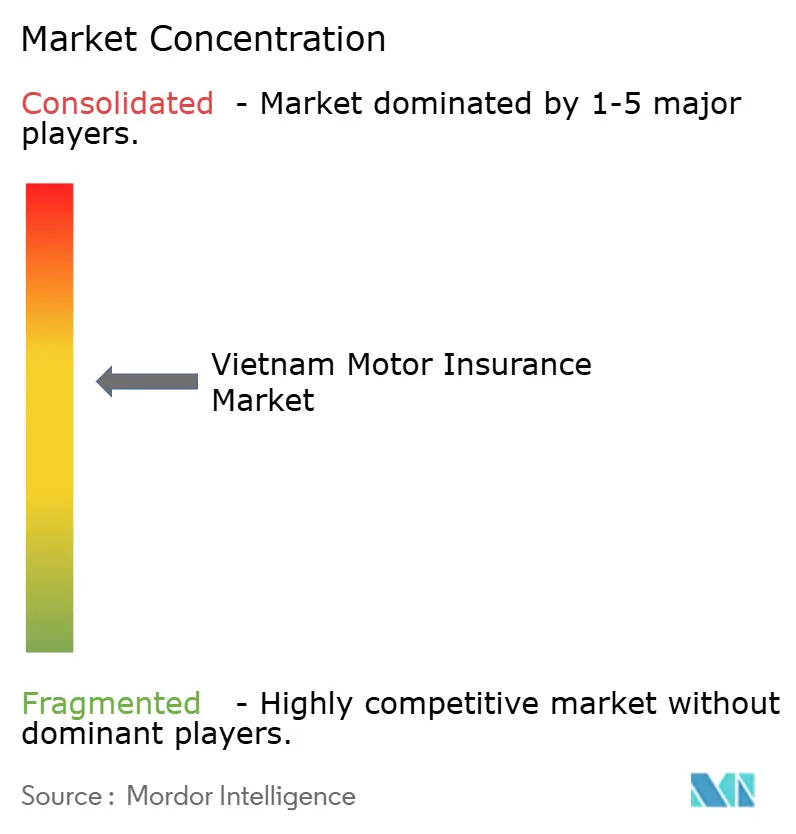

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Motor Insurance Market Analysis by Mordor Intelligence

The Vietnam Motor Insurance Market size in terms of premium value is projected to be USD 760 billion in 2025, USD 0.81 billion in 2026, and reach USD 1.08 billion by 2031, growing at a CAGR of 5.95% from 2026 to 2031.

Uptake is accelerating because tighter compulsory insurance rules, rapid motorisation in second-tier cities, and the government’s e-certificate platform are expanding the insured vehicle base while cutting administrative leakage. Foreign carriers are deepening competition by introducing telematics pricing and bundled products that raise service expectations and push incumbents to digitalise processes. Electric-vehicle adoption and expressway expansion are reshaping risk models, prompting carriers to invest in new actuarial tools, yet margin pressure remains intense as more than 30 insurers jostle for share in a market where price-sensitive retail customers dominate.

Key Report Takeaways

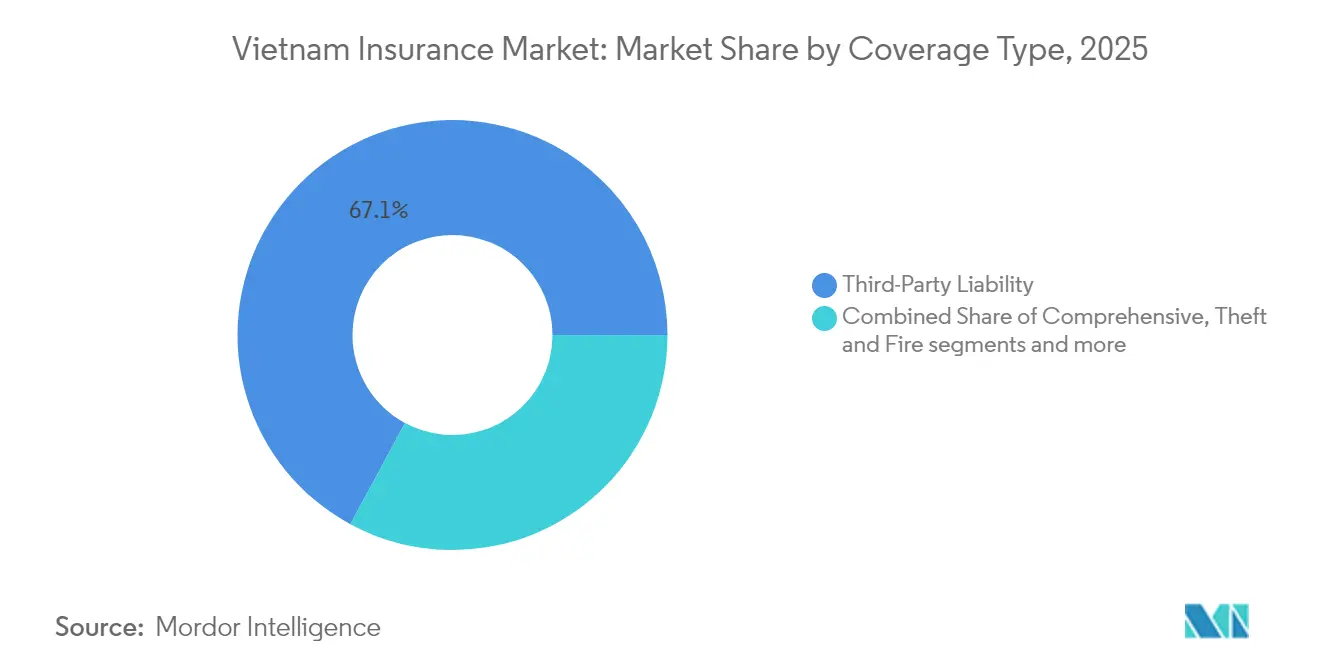

- By coverage type, third-party liability led with 67.12% of the Vietnam motor insurance market share in 2025, while comprehensive coverage is forecast to expand at an 8.01% CAGR through 2031.

- By vehicle type, passenger cars accounted for a 54.22% share of the Vietnam motor insurance market size in 2025; two-wheelers are projected to post the fastest 9.18% CAGR between 2026-2031.

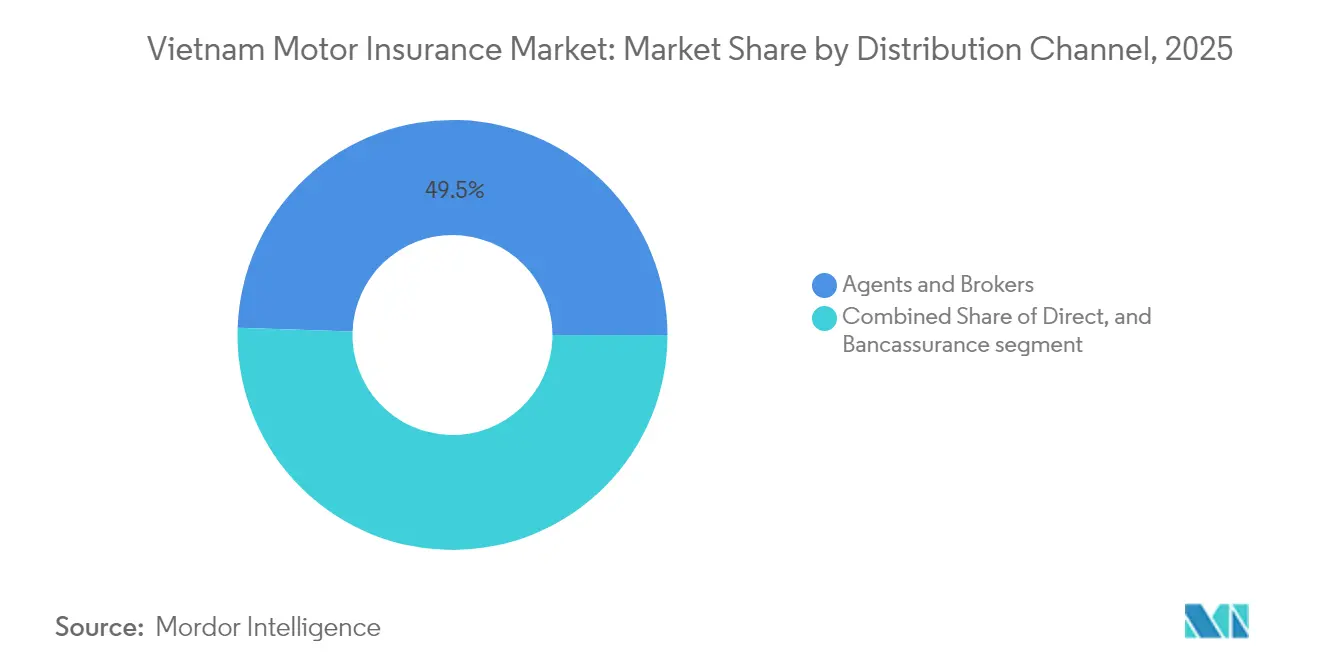

- By distribution channel, agents and brokers held a 49.46% share in 2025, whereas direct online platforms are set to rise at a 11.72% CAGR to 2031.

- By region, Southern Vietnam secured 44.35% of the Vietnam motor insurance market share in 2025; Central Vietnam is forecast to grow the fastest at 8.73% CAGR through 2031.

- By end-user, individual policyholders captured 74.12% share in 2025, while commercial fleets are expected to register a 7.39% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Motor Insurance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Compulsory third-party liability mandate driving policy uptake | +1.8% | Nationwide, higher in Northern & Central regions | Short term (≤ 2 years) |

| Rapid growth of vehicle ownership in tier-2 & tier-3 cities | +1.2% | Central and Northern Vietnam | Medium term (2-4 years) |

| Government-backed e-certificate platform accelerating digital policies | +0.9% | National, early adoption in South | Medium term (2-4 years) |

| Expansion of expressways increases the risk of long-distance driving risk | +0.7% | Central Vietnam, spillover to North | Long term (≥ 4 years) |

| Foreign Insurer Entry Catalyzing Product Innovation & Bundling | + 0.6% | Southern Vietnam, with gradual expansion nationwide | Medium term (2-4 years) |

| Usage-Based Insurance Pilots Supported by Telematics Sandbox | +0.4% | Southern Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Compulsory Third-Party Liability Mandate Driving Policy Uptake

The Vietnam motor insurance market has been reshaped by Decree 67/2023/ND-CP, which fixes premiums by vehicle class and imposes direct insurer accountability for agent conduct[1]Hoang Thai, “Premium Schedule for Compulsory Motor Liability Insurance,” LawNet, lawnet.vn. Compliance checks at registration points and cross-border standardisation under the ASEAN Compulsory Motor Insurance System are pulling previously uninsured vehicles into formal cover. Northern and Central provinces, where enforcement had lagged, are now posting double-digit policy growth as local authorities tighten verification. As compulsory uptake saturates, carriers are layering add-ons such as personal-accident and roadside assistance to widen average premiums per policy, sustaining revenue momentum beyond the short-term regulatory spike.

Rapid Growth of Vehicle Ownership in Tier-2 and Tier-3 Cities

Second-tier urban areas are powering the next wave of expansion for the Vietnam motor insurance market. Rising disposable incomes have lifted nationwide auto sales 12.6% in 2024 to 340,142 units[2]“Automotive Sales in Vietnam by Month,” MarkLines, marklines.com, with the sharpest increases in provincial capitals outside Hanoi and Ho Chi Minh City. New owners in these regions often purchase smaller-engine cars or electric two-wheelers, creating risk profiles that differ from metropolitan drivers. Insurers are extending agent networks eastward along coastal growth corridors while deploying app-based quote engines that reach customers where physical branches are scarce. The end of fee exemptions on domestically produced cars in late 2024 briefly cooled demand, underscoring the sensitivity of this growth engine to fiscal policy. Nonetheless, multi-channel carriers that craft lower-ticket, modular products for first-time buyers are winning share in these high-velocity locales.

Government-Backed E-Certificate Platform Accelerating Digital Policies

Electronic insurance certificates mandated by Decree 03/2021/ND-CP have turned procurement and verification fully digital, bolstering efficiency for the Vietnam motor insurance market. The platform interfaces directly with police and DMV databases, reducing fraudulent proof-of-cover incidents and enabling instant claims validation. Southern Vietnam, with higher smartphone penetration, shows the quickest adoption; several carriers report that over 60% of their new compulsory policies are now issued through mobile channels. These tools shorten quotation cycles from days to minutes and free up underwriting capacity for more complex lines. As digital IDs become ubiquitous across government services, embedded motor insurance within e-wallets and ride-hailing apps is set to unlock further premium growth.

Expansion of Expressways Increasing Long-Distance Driving Risk

The USD 66 billion North–South Expressway program is altering mileage patterns and claim severity across the Vietnam motor insurance market[3]Japan International Cooperation Agency, “Bien Hoa–Vung Tau Expressway Survey Final Report,” jica.go.jp. Freight operators and private motorists alike are clocking longer high-speed journeys, elevating collision intensity and raising spare-parts costs. Toll revenues currently fund only 35-40% of upkeep, so pavement degradation could heighten accident rates unless maintenance gaps are closed. Insurers are upgrading telematics propositions that monitor speed, braking, and route choice, rewarding safe driving with discounts while harvesting granular exposure data.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-sensitive rural customers undermine profitability | –0.7% | Northern & Central Vietnam | Medium term (2-4 years) |

| Fraudulent claims & parts counterfeiting inflate loss ratios | –0.5% | National, higher in South | Short term (≤ 2 years) |

| Margin Squeeze from Intensive Rate Competition Among 30+ Carriers | –0.4% | National | Medium term (2-4 years) |

| Limited Actuarial Data for New-Energy Vehicles | –0.3% | Southern Vietnam, with gradual expansion nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Price-Sensitive Rural Customers Undermine Profitability

Households in agrarian districts earn a median monthly salary of VND 7.7 million (USD 303), limiting capacity to buy anything beyond mandatory cover. For the Vietnam motor insurance market, low-ticket two-wheeler policies often carry fixed administration costs that erode margins. Insurers are stripping products to core benefits, deploying AI chatbots to cut servicing expense, and synchronising renewals with popular mobile-money apps to lift persistency. Longer term, rising rural incomes and broader credit access may enable upselling to comprehensive packages, but in the medium term, profitability hinges on operational frugality rather than rate increases.

Fraudulent Claims & Parts Counterfeiting Inflate Loss Ratios

Authorities are documenting the increasing number of insurance-fraud incidents. Insurance scams have also become more sophisticated. Counterfeit parts obscure damage origins, while staged accidents inflate bodily injury payouts. Loss-adjustment costs have climbed as carriers deploy forensic audits and AI image-recognition tools to flag anomalies. Collaboration platforms among insurers now share blacklists of suspect workshops, helping the Vietnam motor insurance market curb leakage. Nevertheless, short-term profitability remains under pressure until analytics coverage is universal and legal penalties deter orchestrators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Coverage Type: Mandatory Requirements Reshape Portfolio Mix

Third-party liability delivered 67.12% of the Vietnam motor insurance market share in 2025, anchored by the compulsory mandate and standardised tariff bands. Comprehensive cover, though starting from a smaller base, is forecast to grow at 8.01% CAGR through 2031 as vehicle values climb and lenders require broader protection. To capture that upside, carriers bundle collision, theft, and natural-catastrophe riders into competitively priced packages, cross-selling during renewal cycles. ACLI alignment across ASEAN corridors has also prompted fleets operating cross-border routes to augment base policies with extended limits, marginally lifting average premiums.

Consumers increasingly perceive the limits of compulsory policies, especially after Typhoon Yagi’s VND 10 trillion claim wave. This awareness fuels an upshift toward comprehensive and add-on personal accident covers, tightening the linkage between vehicle financing and insurance. Insurers deploy risk-based pricing that rewards safe-driving history captured via onboard diagnostics. As a result, the Vietnam motor insurance market registers a gradual mix shift that underpins premium growth even as policy counts plateau.

By Vehicle Type: Two-Wheelers Electrification Drives Innovation

Passenger cars commanded 54.22% of written premiums in 2025, representing the largest slice of the Vietnam motor insurance market size, but electric two-wheelers are poised to outpace with a 9.18% CAGR to 2031. Battery degradation, charger-fire risks, and higher torque profiles demand fresh underwriting parameters. VinFast, holding 43.4% of the electric two-wheeler segment, supplies telematics data to insurance partners, enabling behaviour-based premiums that could reduce claims frequency by up to 12%, according to pilot results shared with regulators. Commercial vehicles, though smaller in policy count, post superior average premiums due to cargo, driver liability, and downtime-loss extensions linked to expressway usage.

Market entrants capitalise on the data gap in new-energy segments by offering flexible deductibles that incentivise responsible charging practices. Early-adopter advantage is significant: the first insurers to launch comprehensive EV motorcycle cover have already secured 40% of issued policies in Ho Chi Minh City. As lithium-ion repair costs fall, actuarial uncertainty will ease, tightening rate bands and stabilising loss experience across the Vietnam motor insurance market.

By Distribution Channel: Digital Platforms Disrupt Traditional Networks

Agents and brokers retained half of all written business in 2025, but direct online sales are expanding at a 11.72% CAGR, underpinning a multi-channel transformation in the Vietnam motor insurance market. Mobile apps that auto-populate vehicle specs via licence-plate scans can quote compulsory cover in under two minutes, slashing onboarding friction. Bancassurance remains influential for comprehensive packages attached to auto loans, though tighter rules against tied selling could tame that stream. Embedded insurance at the point of vehicle purchase gained momentum after PTI and a leading e-commerce platform piloted one-click policy offers, yielding 25,000 new contracts in eight weeks.

Despite digital momentum, human intermediaries evolve rather than vanish. Hybrid models position agents as risk advisers empowered by AI pricing and paperless issuance. This interplay sustains customer trust in complex claims scenarios while allowing carriers to capture cost efficiencies. Over the forecast horizon, omnichannel proficiency will differentiate winners as the Vietnam motor insurance market balances reach with personalised service.

By End-User: Commercial Fleets Demand Sophisticated Solutions

Individual motorists generated 74.12% of premiums in 2025, yet commercial fleets are on track for a 7.39% CAGR through 2031, reflecting logistics growth and ride-sharing expansion. Fleet operators seek bundled policies covering cargo damage, driver liability, and vehicle downtime, supported by telematics dashboards that flag high-risk routes. Insurers integrate these dashboards with maintenance alerts that cut mechanical-failure claims, translating data analytics into underwriting credits.

The Vietnam motor insurance industry is embracing pay-as-you-drive for fleets, aligning premiums with mileage and driver behaviour. Early adopters report insurance cost reductions of 10% and accident frequency drops near 15%, underscoring the productivity-risk link. As expressway kilometres rise, long-haul trucking exposures will multiply, incentivising further uptake of connected-fleet insurance solutions that refine underwriting precision.

Geography Analysis

Southern Vietnam generated 44.35% of premiums in 2025, cementing its leadership in the Vietnam motor insurance market thanks to dense vehicle ownership around Ho Chi Minh City and a high concentration of foreign insurers. Carriers leverage the region’s strong digital literacy by rolling out mobile claims apps that expedite settlement times to fewer than three days. Uptake of usage-based insurance is highest here; Liberty and AIG have logged over 20,000 telematics policies that peg rates to real-time driving data. Typhoon Yagi’s heavy losses highlighted catastrophe sensitivity, spurring greater demand for natural-hazard add-ons that lift comprehensive policy penetration.

Central Vietnam, forecast to post a 8.73% CAGR to 2031, benefits from expressway corridors that stimulate vehicle purchases and tourism traffic. Insurers are opening satellite offices in Danang and Quy Nhon while harnessing cloud-based distribution to reach inland towns where agents were scarce. The government’s plan to elevate several coastal cities to second-tier status unlocks fresh premium pools, yet underdeveloped repair networks demand strategic partnerships with authorised workshops to guarantee quality parts and contain fraud.

Northern Vietnam, anchored by Hanoi, evidences slower digital migration but steady growth as infrastructure projects and metro expansion reshape mobility patterns. State-linked insurers retain stronger footholds, influencing pricing discipline and product design. Seasonal cold snaps elevate single-vehicle collision claims, prompting insurers to adjust comprehensive deductibles each winter. The e-certificate roll-out is accelerating under the national digital-transformation agenda, promising a pivot toward paperless issuance by 2026. As that transition completes, the Vietnam motor insurance market expects narrower regional variance in service standards.

Competitive Landscape

The top five carriers—PVI, Bao Viet, Bao Minh, PTI, and BIC—collectively control more than 50% of the Vietnam motor insurance market, signalling moderate concentration. Foreign strategic investors, notably HDI Global SE with a 42.33% stake in PVI, infuse capital and analytics expertise that raise competitive stakes. Digital transformation is a common theme: PTI’s adoption of machine-learning pricing shortens rate-filing cycles and sharpens segmentation, while Bao Minh pilots blockchain-based claims tracking to cut fraud latency.

White-space opportunities revolve around electric-vehicle and two-wheeler comprehensive cover, segments still under-penetrated despite ballooning unit counts. Insurtech disruptors such as Papaya streamline KYC and policy issuance through API connections with dealerships. Incumbents are countering by investing in venture units and forging partnerships with fintech players to embed motor cover into super-apps. As rate competition tightens, carriers differentiate through ancillary services—roadside assistance, on-site repairs and eco-driving gamification—that deepen customer stickiness within the Vietnam motor insurance market.

Regulation continues to shape rivalry. Decree 174/2024/ND-CP heightens agent-oversight liability, compelling firms to invest in compliance tech that screens sales practices in real time. Transparency upgrades improve customer confidence but raise cost barriers for sub-scale entrants. Consequently, the market is witnessing selective consolidation, with well-capitalised players eyeing smaller regional insurers to bulk up distribution footprints and claims networks.

Vietnam Motor Insurance Industry Leaders

PetroVietnam Insurance (PVI)

Bao Minh Insurance Corporation

BIDV Insurance Corporation (BIC)

Bao Viet Insurance Corporation

Post & Telecommunication Insurance Corporation (PTI)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: PTI partnered with Akur8 to deploy a machine-learning pricing platform, strengthening actuarial precision and speeding product launches.

- April 2025: Decree 174/2024/ND-CP took effect, imposing stricter agent oversight and mandating motor-liability sales .

- January 2025: PVI Holdings boosted charter capital to VNĐ 3.9 trillion (USD 153.22 million)

- November 2024: Vietnam joined the ASEAN Compulsory Motor Insurance System, harmonising cross-border liability rules.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Vietnam motor insurance market as all gross written premiums generated from policies that protect road-registered passenger cars, commercial vehicles, and two-wheelers against third-party liability and own-damage risks during the policy year.

Exclusions include micro-mobility, specialty motorsport, and inland marine covers that are kept outside the scope.

Segmentation Overview

- Segmentation by Coverage Type

- Comprehensive Coverage

- Third-Party Liability

- Theft & Fire

- Personal Accident Add-on

- Segmentation by Vehicle Type

- Passenger Cars

- Commercial Vehicles

- Two-Wheelers

- Segmentation by Distribution Channel

- Direct (Online & Company-Owned)

- Agents & Brokers

- Bancassurance

- Segmentation by End-User

- Individual

- Commercial Fleet

- Segmentation by Region

- Northern Vietnam

- Central Vietnam

- Southern Vietnam

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with underwriting heads, large agency principals, and fleet-risk managers across Hanoi, Ho Chi Minh City, and Da Nang clarified discounting practices, seasonality in renewals, and expected penetration of electric-vehicle covers. Follow-up surveys with digital aggregators provided early signals on price-comparison uptake, filling gaps left by published data.

Desk Research

We started by compiling five years of premium and claim statistics issued by the Insurance Association of Vietnam, monthly vehicle-registration data from the General Department of Vietnam Customs, and household disposable-income series from the General Statistics Office. Company 10-K filings, press releases, and investor decks supplied insured-vehicle counts and average selling prices that refine base-year estimates. Paid databases such as D&B Hoovers and Dow Jones Factiva helped us verify carrier financials, while Questel's patent feeds highlighted emerging usage-based products. This list is illustrative; many additional public and paid sources were tapped for validation.

Market-Sizing & Forecasting

A top-down model converts official premium totals into segment splits by mapping vehicle-parc counts, compliance rates, and average premium per vehicle. Sampled carrier roll-ups act as a bottom-up cross-check before figures are locked. Key variables like annual new vehicle registrations, compulsory-coverage compliance, average comprehensive premium, accident frequency, and consumer-price inflation drive both the historical reconstruction and the forecast. Multivariate regression, supplemented by scenario analysis for regulatory shocks, projects each variable through 2030; results are iterated with expert feedback until variance falls within a two-percent band.

Data Validation & Update Cycle

Outputs pass three layers of review that test arithmetic integrity, year-on-year logical movement, and alignment with independent macro and industry indicators. Models refresh every twelve months, with interim updates triggered by rate-filing changes, sudden shifts in vehicle demand, or catastrophic loss events.

Why Mordor's Vietnam Motor Insurance Baseline Commands Reliability

Published estimates often diverge because firms select dissimilar premium lines, assume different average selling prices, and refresh on contrasting cadences.

Key gap drivers include some providers bundling inland marine or personal-accident riders, many applying static exchange rates, and several relying on optimistic penetration leaps that our interviews did not confirm. Mordor analysts, by anchoring values to audited premium disclosures and reconciling them with vehicle-level metrics, avoid such distortions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.76 B (2025) | Mordor Intelligence | - |

| USD 0.83 B (2024) | Global Consultancy A | Includes inland marine riders and applies constant 2024 VND/USD rate |

| USD 0.75 B (2025) | Trade Journal B | Uses uniform premium per vehicle, no adjustment for regional mix |

In sum, Mordor's disciplined scope selection, variable-level reconciliation, and annual refresh cycle furnish decision-makers with a transparent, balanced baseline that can be traced back to clear public records and repeatable steps.

Key Questions Answered in the Report

What is the current size of the Vietnam motor insurance market?

The Vietnam motor insurance market size stood at USD 810 million in 2026 and is forecast to reach USD 1.08 billion by 2031.

Which coverage type dominates premium income?

Third-party liability commanded 67.12% of premium in 2025 owing to compulsory regulations, although comprehensive cover is catching up with an 8.01% CAGR outlook.

How fast are digital sales channels growing?

Direct online platforms for motor insurance are expanding at a 11.72% CAGR to 2031, supported by the national e-certificate system and rising smartphone use.

Why are electric two-wheelers important for insurers?

Electric two-wheelers are projected to record a 9.18% CAGR, creating demand for specialized battery and charger risk cover and opening a new actuarial frontier.

Page last updated on: