Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

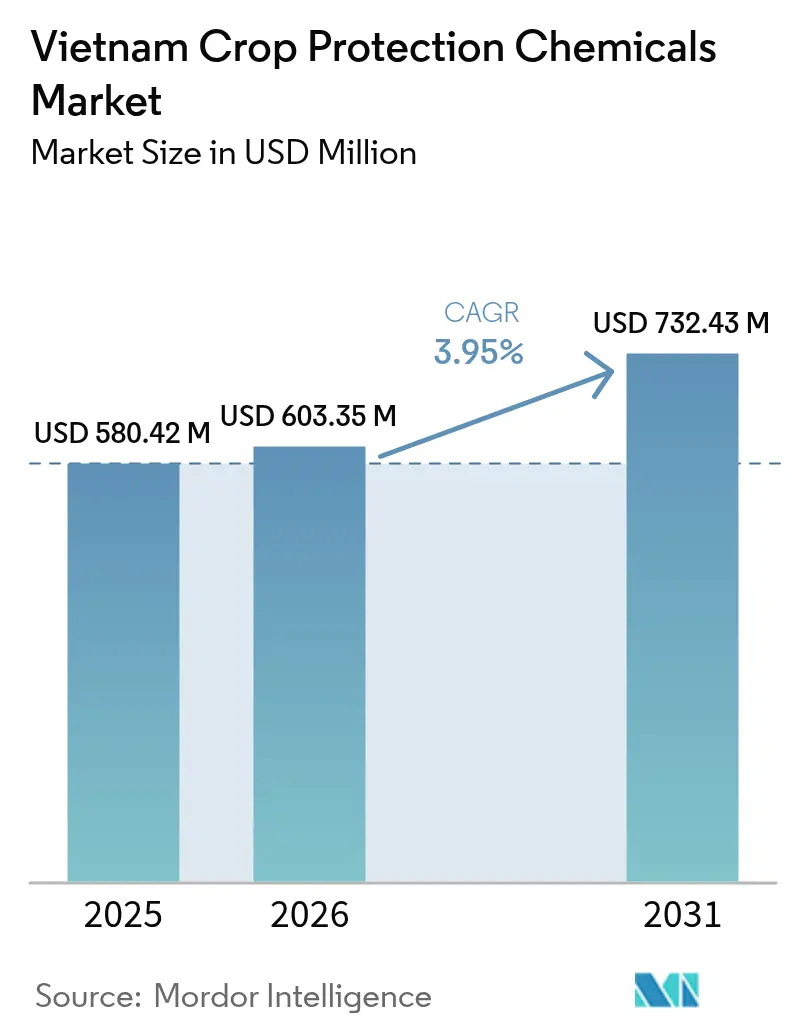

| Base Year Market Size (2025) | USD 580.42 Million |

| Market Size (2026) | USD 603.35 Million |

| Market Size (2031) | USD 732.43 Million |

| Growth Rate (2026 - 2031) | 3.95% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Crop Protection Chemicals Market Analysis by Mordor Intelligence

The Vietnam crop protection chemicals market size is expected to grow from USD 580.42 million in 2025 to USD 603.35 million in 2026 and is forecast to reach USD 732.43 million by 2031 at 3.95% CAGR over 2026-2031. Mounting export opportunities, fast-modernizing farms, and climate-induced pest loads combine to propel demand for both conventional and low-residue formulations. A nationwide pivot toward integrated pest management that blends synthetic and biological solutions is encouraging established brands to widen portfolios while domestic players scale generic lines. In parallel, digital contract-farming platforms streamline last-mile delivery, improving product traceability and locking farmers into branded input packages that underpin the Vietnam crop protection chemicals market. Government subsidy programs for rice-export compliance, specialty fruit orchard expansion, and herbicide-tolerant grain seed adoption collectively enlarge addressable acres, while counterfeit trade, residue-limit tightening, and rural labor scarcity temper the growth curve.

Key Report Takeaways

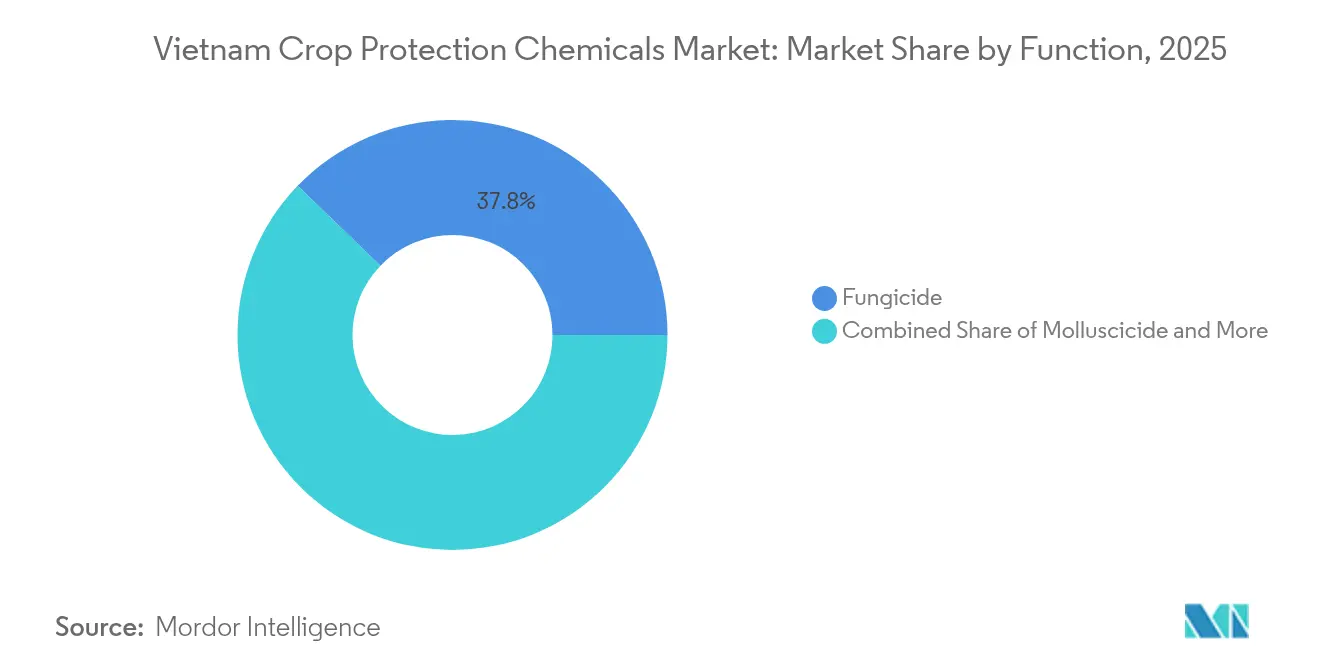

- By function, fungicides led with 37.80% revenue share in 2025; molluscicides are projected to advance at a 6.48% CAGR to 2031.

- By application mode, foliar applications commanded 50.90% share of the Vietnam crop protection chemicals market size in 2025, while soil treatment is forecast to grow at 4.32% CAGR through 2031.

- By crop type, grains and cereals accounted for 64.10% of the Vietnam crop protection chemicals market share in 2025 and are set to progress at a 3.92% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Crop Protection Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government incentives for rice-export quality compliance | +0.8% | Mekong Delta, Red River Delta | Medium term (2-4 years) |

| Rapid expansion of specialty fruit export orchards | +0.6% | Central Highlands, Southern regions | Long term (≥ 4 years) |

| Adoption of herbicide-tolerant hybrid rice and corn seeds | +0.5% | National, concentrated in major grain regions | Medium term (2-4 years) |

| Growth of contract-farming platforms is driving input packages | +0.4% | National, early gains in Mekong Delta provinces | Short term (≤ 2 years) |

| Climate-change-driven pest pressure in the Mekong Delta | +0.3% | Mekong Delta, spillover to the Central Coast | Long term (≥ 4 years) |

| Digitally enabled last-mile agro-dealer networks | +0.2% | National, urban-adjacent rural areas first | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Incentives for Rice-Export Quality Compliance

Vietnam's agricultural export strategy fundamentally reshapes crop protection demand through quality-linked financial incentives that reward farmers for meeting international standards. The Ministry of Agriculture and Rural Development's Circular 01/2024/TT-BNNPTNT establishes direct subsidies for farmers adopting certified crop protection protocols, with premium payments reaching 15% above market rates for rice meeting EU organic residue standards[1]Source: Vietnam Ministry of Agriculture and Rural Development, “Circular 01/2024/TT-BNNPTNT on Agricultural Export Quality Standards,” MARD.GOV.VN. Export quality compliance requirements drive adoption of integrated pest management protocols that combine biological and chemical solutions, expanding market opportunities for companies offering comprehensive product portfolios rather than single-active ingredient solutions.

Rapid Expansion of Specialty Fruit Export Orchards

Specialty fruit cultivation emerges as a high-value driver transforming Vietnam's agricultural landscape, with dragon fruit exports alone reaching USD 2.8 billion in 2024, representing 23% growth from previous year levels[2]Source: Vietnam Customs Department, “Agricultural Export Statistics 2024,” CUSTOMS.GOV.VN. Orchard expansion in the Central Highlands and southern provinces creates demand for specialized fungicides and insecticides tailored to tropical fruit production, where single pest outbreaks can destroy entire seasonal harvests worth millions of dollars. Premium fruit export markets in China, Japan, and South Korea enforce strict maximum residue limits that require sophisticated application timing and product selection, driving farmers toward higher-priced, low-residue formulations. The shift from subsistence farming to commercial orchard management introduces professional crop protection practices that favor established international brands over local generic products.

Adoption of Herbicide-Tolerant Hybrid Rice and Corn Seeds

Herbicide-tolerant seed adoption accelerates across Vietnam's major grain-producing regions, with hybrid rice varieties covering approximately 1.2 million hectares in 2024, representing 18% of total rice cultivation area[3]Source: Vietnam National University of Agriculture, “Hybrid Rice Adoption Report 2024,” VNUA.EDU.VN. These varieties enable farmers to use selective herbicides that control weeds without damaging crops, reducing labor requirements compared to traditional manual weeding methods. Corn cultivation benefits similarly from herbicide-tolerant hybrids, particularly in northern provinces where labor costs have increased annually since 2022 due to rural-urban migration patterns. The technology creates locked-in demand for specific herbicide formulations, as farmers must purchase compatible chemicals to realize the full economic benefits of their seed investments.

Growth of Contract-Farming Platforms Driving Input Packages

Digital contract-farming platforms revolutionize input distribution by bundling crop protection chemicals with seeds, fertilizers, and technical support services, creating predictable demand patterns that benefit established suppliers. These platforms guarantee product authenticity and provide application training, addressing two critical market barriers that previously limited the adoption of premium crop protection products. Contract farming arrangements typically specify exact product brands and application protocols, reducing farmer choice but ensuring consistent demand for participating chemical companies. The model proves particularly effective in rice and corn production, where standardized growing practices enable economies of scale in input procurement and distribution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating counterfeit pesticide trade | -0.7% | National, concentrated in border provinces | Short term (≤ 2 years) |

| Stringent residue limits from European Union/United States buyers | -0.5% | Export-focused regions, Mekong Delta | Medium term (2-4 years) |

| Rising labor migration is shrinking the farm labor pool | -0.4% | Rural areas nationwide, acute in northern provinces | Long term (≥ 4 years) |

| Increasing consumer preference for organic produce | -0.3% | Urban-adjacent farming areas, specialty crop regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Counterfeit Pesticide Trade

Counterfeit pesticide infiltration undermines legitimate market growth by offering substandard products at prices 30-50% below authentic formulations, creating unfair competition that pressures profit margins across the industry. Border provinces with China and Cambodia experience particularly acute counterfeit penetration, where cross-border smuggling networks exploit regulatory gaps and limited enforcement resources. Counterfeit products often contain incorrect active ingredient concentrations or banned substances, leading to crop failures that damage farmer confidence in chemical crop protection methods. The proliferation of fake products forces legitimate manufacturers to invest heavily in anti-counterfeiting measures and farmer education programs, reducing resources available for product development and market expansion.

Stringent Residue Limits from European Union/United States Buyers

Maximum residue limit enforcement by major export markets constrains product selection and increases compliance costs for Vietnamese farmers targeting premium international buyers. Compliance requires farmers to switch to more expensive, low-residue formulations or extend pre-harvest intervals that reduce crop protection effectiveness during critical growth periods. United States buyers increasingly demand residue testing certificates for imported Vietnamese agricultural products, adding USD 200-500 per shipment in certification costs that ultimately pressure farmers to minimize chemical inputs. The regulatory environment favors biological and organic crop protection methods, potentially constraining long-term chemical market growth as export-oriented farmers seek alternatives to traditional synthetic pesticides.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Fungicides Lead Amid Rising Molluscicide Demand

Fungicides captured 37.80% of the 2025 value as perennial humidity in paddies breeds blast, sheath blight, and brown spot. The Vietnam crop protection chemicals market size for fungicides remains anchored by triazoles and strobilurins, yet demand migrates toward low-residue SDHI blends that win export approvals. Molluscicides, propelled by golden apple snail incursions into 15 new provinces, headline growth at 6.48% CAGR. Farmers increasingly integrate metaldehyde alternatives with biological baits to satisfy residue audits while preserving efficacy.

Nematicides represent a smaller but growing segment, particularly in vegetable production areas where root-knot nematode pressure intensifies under climate change conditions. The functional mix reflects Vietnam's crop portfolio emphasis on rice and specialty crops that require intensive disease and pest management to meet export quality standards. Minor segments, namely nematicides for vegetable zones, enjoy niche expansion as root-knot outbreaks rise. Advances in mode-of-action rotation and resistance-management labeling bolster prospects for premium multi-active packs. International suppliers dominate patented fungicide and insecticide niches, while local firms thrive in single-active herbicide generics.

By Application Mode: Foliar Dominance Shifts Toward Soil Integration

Foliar application methods command 50.90% Vietnam crop protection chemicals market in 2025, reflecting traditional spraying practices that Vietnamese farmers understand and can implement with existing equipment, while soil treatment applications demonstrate the strongest growth trajectory at 4.32% CAGR through 2031. The shift toward soil-based applications reflects the adoption of systemic crop protection approaches that provide longer-lasting protection and reduce application frequency, addressing labor shortage constraints that make frequent foliar spraying increasingly impractical. Seed treatment applications gain traction in hybrid rice and corn cultivation, where pre-planting chemical protection ensures uniform crop establishment and reduces early-season pest pressure.

Chemigation systems, which deliver chemicals through irrigation infrastructure, represent an emerging application mode that addresses labor constraints while ensuring precise product placement. Fumigation methods remain limited to high-value crops and greenhouse operations, but show potential for expansion as Vietnam's protected agriculture sector develops. The application mode evolution reflects broader agricultural mechanization trends that favor methods requiring less manual labor and technical expertise while maintaining effectiveness. Regulatory influence from Vietnam's Plant Protection Department increasingly emphasizes application methods that minimize environmental exposure and worker safety risks.

By Crop Type: Grains Dominate Despite Diversification Trends

Grains and cereals maintain market dominance with a 64.10% share in 2025 and steady 3.92% CAGR growth through 2031, reflecting Vietnam's position as the world's third-largest rice exporter and expanding corn production for livestock feed markets. Rice cultivation alone accounts for approximately half of total crop protection chemical usage, driven by intensive production systems that require multiple applications per growing season to control the complex pest and disease pressures inherent in flooded field conditions. Corn production expansion in northern and central provinces adds incremental demand for herbicides and insecticides tailored to upland grain production systems.

Commercial crops, including coffee, rubber, and sugarcane, while pulses and oilseeds maintain a smaller but stable share. Turf and ornamental applications remain minimal in Vietnam's agricultural economy but show potential growth as urban landscaping and golf course development expand. The crop type distribution reflects Vietnam's export-oriented agricultural strategy that prioritizes high-volume grain production alongside high-value specialty crops targeting premium international markets.

Geography Analysis

Vietnam's crop protection chemicals market exhibits distinct regional patterns driven by agricultural specialization, with the Mekong Delta accounting for approximately 44.60% of national demand in 2025 due to its role as the country's primary rice-producing region. The delta's 2.5 million hectares of rice cultivation require intensive chemical inputs to manage pest and disease pressure exacerbated by year-round cropping systems and climate change impacts. Northern mountainous provinces represent 15.40% of consumption, primarily for corn and vegetable production, driven by coffee, pepper, and specialty fruit cultivation.

Regional growth patterns reflect agricultural development strategies and export market access, with southern provinces experiencing the fastest expansion due to specialty fruit orchard development and aquaculture integration. The Mekong Delta's growth trajectory remains steady, supported by government investments in irrigation infrastructure and export quality improvement programs. Central and northern regions show accelerating demand growth as farmers adopt mechanized production systems that rely more heavily on chemical inputs to replace traditional labor-intensive practices. Regulatory influence varies significantly across regions, with export-focused areas subject to stricter quality control measures and residue monitoring programs administered by provincial plant protection departments. Border provinces face unique challenges from counterfeit product infiltration, requiring enhanced enforcement cooperation between customs authorities and agricultural regulators. The geographic distribution of demand reflects Vietnam's dual agricultural economy, where subsistence farming coexists with export-oriented commercial production that drives the majority of crop protection chemical consumption and market growth.

Competitive Landscape

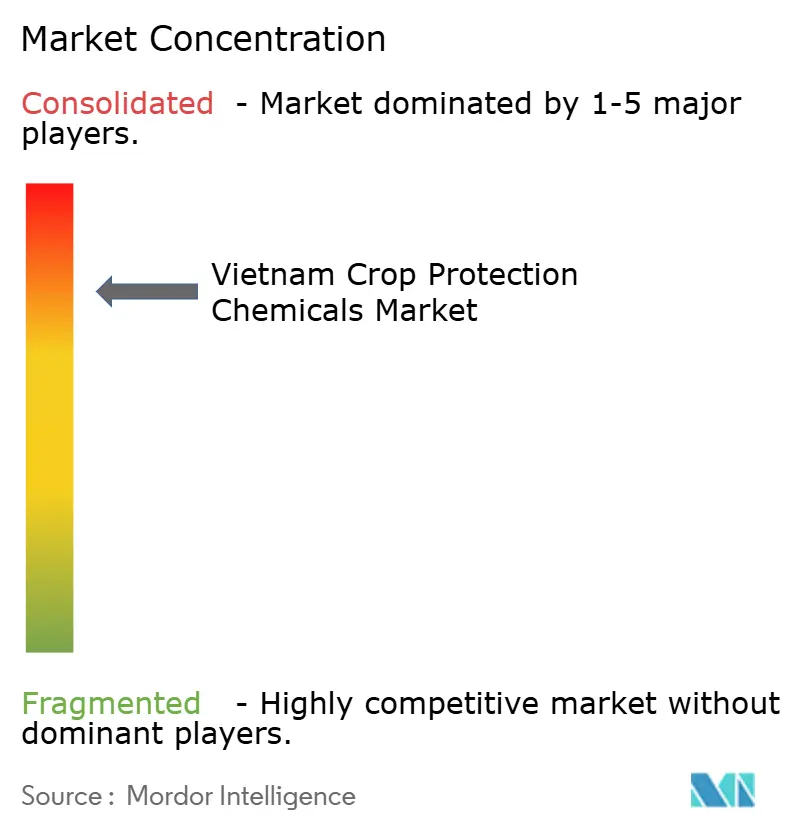

Vietnam's crop protection chemicals market exhibits consolidated. International players dominate premium segments, while domestic companies compete aggressively in price-sensitive generic markets. Market concentration remains relatively low, with the top five companies controlling a good share of total market value, creating opportunities for both global giants and nimble local competitors to capture market share through differentiated strategies. International companies like Nufarm Ltd, FMC Corporation, UPL Limited, Syngenta Group, and Bayer AG focus on high-margin, low-residue formulations that meet export quality requirements, while domestic players, including Vietnam National Chemical Group and Loc Troi Group, leverage distribution networks and local market knowledge to compete in volume segments.

Technology adoption emerges as a key competitive differentiator, with leading companies investing in digital platforms that provide farmers with application guidance, weather-based timing recommendations, and product authentication services. Loc Troi Group's integrated approach combining seeds, chemicals, and digital advisory services demonstrates how local companies can compete against international brands by offering comprehensive solutions rather than standalone products.

White-space opportunities exist in biological crop protection products and precision application technologies that address labor shortage constraints while meeting sustainability requirements from export buyers. The competitive landscape increasingly favors companies that can navigate Vietnam's complex regulatory environment while building direct relationships with contract farming platforms and large-scale agricultural cooperatives.

Vietnam Crop Protection Chemicals Industry Leaders

Bayer AG

FMC Corporation

Nufarm Ltd

Syngenta Group

UPL limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Corteva Agriscience launched its Pioneer brand herbicide-tolerant corn seeds in northern Vietnam, accompanied by a USD 8 million investment in farmer training programs and application equipment subsidies. The product introduction targets the expanding livestock feed market that drives corn cultivation growth in mountainous provinces.

- September 2024: Syngenta Group announced a strategic partnership with Vietnam National University of Agriculture to establish a USD 12 million research center focused on developing crop protection solutions for tropical rice and fruit production systems. The collaboration aims to create region-specific formulations that address climate change-related pest pressure while meeting international residue standards.

- January 2023: Bayer formed a new partnership with Oerth Bio to enhance crop protection technology and create more eco-friendly crop protection solutions.

Vietnam Crop Protection Chemicals Market Report Scope

Fungicide, Herbicide, Insecticide, Molluscicide, Nematicide are covered as segments by Function. Chemigation, Foliar, Fumigation, Seed Treatment, Soil Treatment are covered as segments by Application Mode. Commercial Crops, Fruits & Vegetables, Grains & Cereals, Pulses & Oilseeds, Turf & Ornamental are covered as segments by Crop Type.Function

| Fungicide |

| Herbicide |

| Insecticide |

| Molluscicide |

| Nematicide |

Application Mode

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

Crop Type

| Commercial Crops |

| Fruits & Vegetables |

| Grains & Cereals |

| Pulses & Oilseeds |

| Turf & Ornamental |

| Function | Fungicide |

| Herbicide | |

| Insecticide | |

| Molluscicide | |

| Nematicide | |

| Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| Crop Type | Commercial Crops |

| Fruits & Vegetables | |

| Grains & Cereals | |

| Pulses & Oilseeds | |

| Turf & Ornamental |

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms