United States Maize Market Analysis by Mordor Intelligence

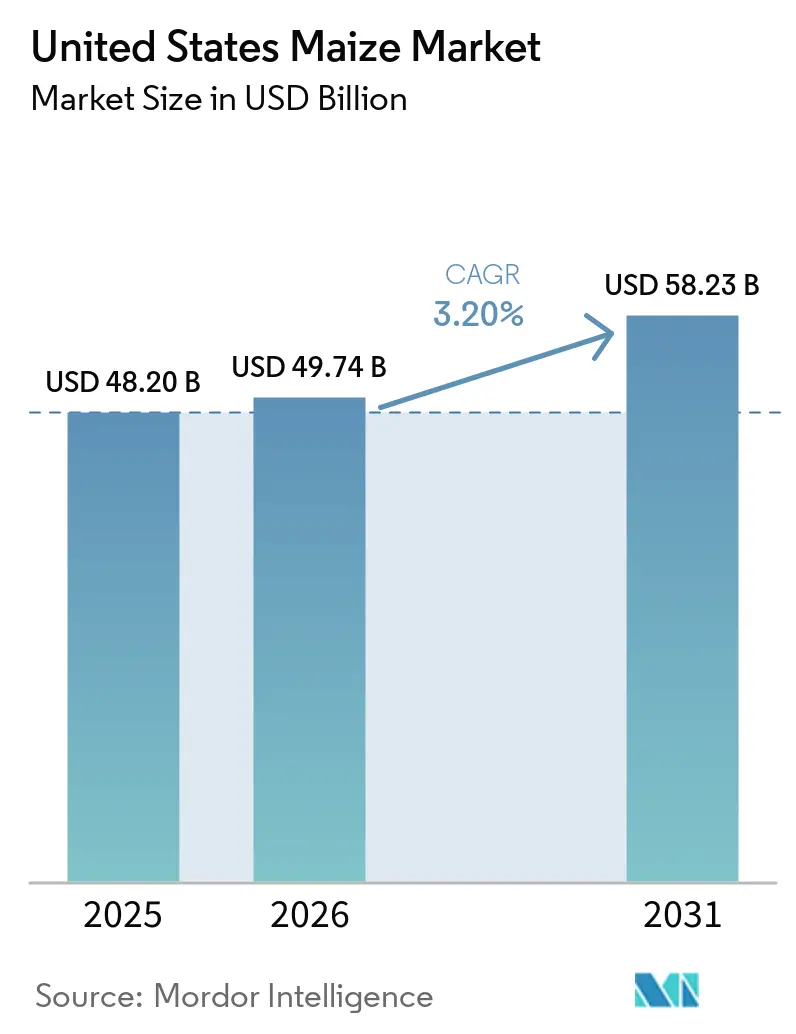

The United States maize market size is projected to grow from USD 48.20 billion in 2025 and 49.74 billion in 2026 to USD 58.23 billion by 2031, reflecting a CAGR of 3.20% during the period 2026-2031. Ethanol demand has risen following the Environmental Protection Agency's approval of year-round E15 sales in March 2026, which is estimated to add approximately 180 million bushels to annual corn consumption (EPA). The adoption of advanced trait stacks, approved in 2025, is enhancing per-acre returns in areas affected by corn rootworm, motivating growers to continue planting corn in tight rotations, even amid strengthening soybean prices. On the supply side, tar spot outbreaks and irrigation restrictions in the High Plains are influencing regional yield expectations, while record-high fertilizer prices are reducing margins in areas where variable-rate nutrient technology has not yet been implemented. Export competitiveness remains strong due to expanded rail and river infrastructure in the Midwest, which is lowering delivered costs to Gulf and Pacific Northwest ports.

Key Report Takeaways

- The United States is one of the largest global producers and exporters of maize, with production predominantly centered in the Midwest Corn Belt states, including Iowa, Illinois, Nebraska, Minnesota, and Indiana.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Maize Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift to high-protein meat diets sustaining feed demand | +0.5% | National | Long term (≥ 4 years) |

| Record E15 adoption boosting ethanol use | +0.6% | National, strongest in Midwest | Short term (≤ 2 years) |

| Biotech trait stacks increasing per-acre returns | +0.4% | Corn Belt | Medium term (2-4 years) |

| Expansion of Midwest rail and river export capacity | +0.3% | Midwest export corridors | Medium term (2-4 years) |

| AI-based variable-rate fertilization reducing input costs | +0.2% | National, early adoption in Midwest | Medium term (2-4 years) |

| Premiums for low-carbon corn via regenerative agriculture | +0.2% | National, pilot programs in Midwest | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift to High-Protein Meat Diets Sustaining Feed Demand

The increasing consumption of animal protein in the United States continues to drive maize demand through its use in animal feed, particularly in the poultry industry, which remains the leading meat category. Poultry production relies heavily on maize-based feed, establishing a direct connection between dietary trends and grain demand. According to the United States Department of Agriculture Economic Research Service, the per capita availability of broiler consumption reached 101.3 pounds in 2024, up by 0.7% over the last year, indicating sustained chicken consumption [1]Source: United States Department of Agriculture Economic Research Service, “Livestock, Dairy, and Poultry Outlook,” ers.usda.gov. This steady consumption level supports the inclusion of maize in feed formulations and underpins consistent demand within the United States maize market.

Record E15 Adoption Boosting Ethanol Use

The growing adoption of E15 fuel in the United States is boosting maize demand due to higher ethanol blending. Policy measures supporting year-round E15 sales and the expansion of fueling station infrastructure are contributing to the rise in ethanol consumption. According to the United States Environmental Protection Agency (EPA), the Renewable Fuel Standard requires the blending of 15 billion gallons of conventional biofuel annually, primarily sourced from maize [2]Source: United States Environmental Protection Agency, “EPA Finalizes Historic New Renewable Fuel Standards to Strengthen American Energy,” epa.gov. This regulatory framework provides a consistent demand for ethanol producers, enhancing maize utilization within the biofuel industry and bolstering overall market demand.

Biotech Trait Stacks Increasing Per-Acre Returns

The use of advanced biotechnology traits in maize cultivation is enhancing productivity and ensuring yield stability across the United States. Stacked traits that combine herbicide tolerance and insect resistance help minimize crop losses and improve farm efficiency under diverse agronomic conditions. These technologies are widely utilized due to their ability to optimize input use and ensure consistent production outcomes. According to the United States Department of Agriculture Economic Research Service, over 90% of corn production in the United States relies on genetically engineered varieties, indicating significant technology adoption [3]Source: United States Department of Agriculture Economic Research Service, “Adoption of Genetically Engineered Crops in the United States: Recent Trends in GE Adoption,” ers.usda.gov. This high level of adoption supports consistent maize production and strengthens the supply side of the market.

Expansion of Midwest Rail and River Export Capacity

Investments in rail networks and inland waterway infrastructure are enhancing maize export efficiency in the United States by facilitating grain movement from production areas to export terminals. Upgrades to locks, dams, and rail loading facilities are minimizing transit delays and improving supply chain reliability along critical corridors, including the Mississippi River system and Pacific Northwest routes. These logistical improvements contribute to faster turnaround times, improved inventory management, and reduced transportation bottlenecks. Such advancements ensure consistent export flows, strengthen global competitiveness, and reinforce the United States' position as a major maize exporter in international markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile global fertilizer prices pressuring margins | -0.5% | National | Short term (≤ 2 years) |

| Widespread tar spot outbreaks in Corn Belt states | -0.4% | Corn Belt (Illinois, Indiana, Ohio, Michigan, and Wisconsin) | Medium term (2-4 years) |

| Competition from soybeans in crop rotation | -0.3% | Midwest rotation belt | Medium term (2-4 years) |

| State-level water-use limits in the High Plains | -0.2% | High Plains (Kansas, Nebraska, and Texas Panhandle) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Global Fertilizer Prices Pressuring Margins

Fertilizer price volatility continues to create significant uncertainty in the United States maize market by directly impacting input costs and influencing farm-level decisions. According to Michigan State University Extension (2026), and the United States Department of Agriculture Agricultural Marketing Service, urea prices rose from USD 581 per metric ton on February 20, 2026, to USD 822 per metric ton on March 20, 2026. This sharp increase during the planting season places immediate financial pressure on farmers, often resulting in delayed purchases or reduced application rates. These adjustments directly affect yield potential and production consistency, contributing to supply fluctuations and overall market instability.

Widespread Tar Spot Outbreaks in Corn Belt States

The spread of tar spot disease poses an increasing challenge for maize production in the United States, particularly in key Corn Belt regions. The disease thrives in cool, humid conditions and can significantly harm crop health if not managed effectively. Addressing increased disease pressure requires timely fungicide applications and diligent field monitoring, adding complexity to crop management practices. The limited availability of fully resistant hybrids further heightens growers' vulnerability. The presence of tar spot also increases the risk of yield variability across regions, creating uncertainty in production outcomes and impacting the consistency of maize supply.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Maize production in the United States is highest in the Midwest, particularly in states such as Iowa, Illinois, Nebraska, Minnesota, and Indiana. This region benefits from favorable soil conditions, well-established farming systems, and the widespread use of advanced agricultural practices, enabling large-scale and efficient cultivation. However, this concentration also makes production vulnerable to regional weather variability. Adverse climatic events, such as droughts or excessive rainfall, can significantly affect yields, making the maize supply highly sensitive to conditions within this geographic area.

The Western region is becoming increasingly significant due to advancements in infrastructure and logistics that facilitate maize distribution and trade. Efficient transportation networks, including rail systems, inland waterways, and port facilities, are crucial in linking production areas with domestic processors and export markets. Continuous improvements in grain handling, storage, and terminal infrastructure are enhancing supply chain efficiency and minimizing transit delays. Improved regional connectivity supports smoother commodity flows, expands market access, and strengthens the competitiveness of United States maize in international trade.

Maize production in the South and parts of the Northeast reflects more diversified cropping systems and varying climatic conditions. These regions often prioritize crops such as soybeans, cotton, and sorghum, limiting the scale of maize cultivation compared to the core producing areas. Higher humidity levels and variable rainfall patterns influence planting decisions and yield stability. Additionally, infrastructure limitations and smaller farm sizes restrict large-scale maize production. Despite these challenges, these regions contribute to localized supply and support regional feed and processing demand within the broader market.

Competitive Landscape

The United States maize market is primarily driven by large-scale producers utilizing highly mechanized and technology-driven farming systems. Commercial farms, particularly in the Midwest, employ precision agriculture tools, advanced seed genetics, and optimized input management to maximize yields and maintain cost efficiency. Farm consolidation and contract farming models are enabling producers to expand operations and secure stable market access. Close coordination with input suppliers and buyers facilitates efficient production planning, while risk management strategies, such as crop insurance and forward contracting, help stabilize farm income in a volatile pricing environment.

Integrated players within the maize value chain are increasingly aligning production, storage, and distribution activities to enhance supply reliability and efficiency. Grain handlers, cooperatives, and merchandisers are investing in storage infrastructure, logistics networks, and digital platforms to streamline the procurement and movement of maize. Strong linkages between producers and downstream users, including feed manufacturers and ethanol producers, ensure consistent demand and better price realization. These integrators play a vital role in balancing regional supply and demand while improving market transparency through enhanced data and traceability systems.

Other stakeholders, such as agricultural service providers, input companies, and technology firms, are contributing to the competitiveness of the maize market by promoting productivity and sustainability. Innovations in digital agronomy, satellite monitoring, and climate-smart practices are helping farmers optimize input use and improve resilience to weather variability. Financial institutions and crop insurance providers are also strengthening risk management frameworks, encouraging continued investment in maize cultivation. This interconnected ecosystem fosters collaboration across the value chain, enhancing overall market performance and supporting long-term growth potential.

Recent Industry Developments

- March 2026: The Environmental Protection Agency issued a temporary emergency waiver permitting nationwide summer sales of E15 fuel. This measure aims to support increased ethanol blending demand, enhance corn utilization aiding the maize market.

- November 2025: Archer-Daniels-Midland Company has inaugurated the world’s largest bioethanol carbon capture and storage facility at its Nebraska corn processing complex. This development strengthens the United States maize market by improving the competitiveness of corn-based ethanol, supporting stable maize demand, and ensuring long-term offtake from the biofuel sector.

- May 2025: CHS Inc. finalized the renovation and expansion of its Myrtle Grove export terminal in Louisiana, enhancing maize export logistics within the United States. The upgraded facility increases grain handling capacity by 30%, including corn, improving throughput and reducing loading times for export vessels.

United States Maize Market Report Scope

Maize is a cereal grain crop widely cultivated for food, animal feed, and industrial uses such as starch and biofuel production. It is a staple crop globally due to its high yield, versatility, and role in food security and agro-industrial value chains. The United States maize market report includes production analysis (volume), consumption analysis (value and volume), import analysis (value and volume), export analysis (value and volume), wholesale price trend analysis and forecast, regulatory framework, logistics and infrastructure, and seasonality analysis. The market forecasts are provided in terms of value (USD) and volume (metric tons).

Production Analysis

| Production Volume |

| Area Harvested and Yield |

Trade Analysis (Value and Volume)

| Import Market Analysis | Import Value and Volume |

| Key Supplying Markets | |

| Export Market Analysis | Export Value and Volume |

| Key Destinations Markets |

| Production Analysis | Production Volume | |

| Area Harvested and Yield | ||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume |

| Key Supplying Markets | ||

| Export Market Analysis | Export Value and Volume | |

| Key Destinations Markets | ||

Key Questions Answered in the Report

How large is the US maize market in 2026 and where is it headed?

The market stands at USD 49.74 billion in 2026 and is forecast to reach USD 58.23 billion by 2031, expanding at a 3.20% CAGR.

What drives near-term demand for United States maize?

Year-round availability of higher ethanol blends is encouraging additional corn use in fuel production.

How are fertilizer prices affecting grower margins?

Anhydrous ammonia above USD 1,000 per metric ton in 2026 raised production costs by USD 50-80 per acre, pressuring profitability.

What technology offers the fastest payback for cost control?

AI-enabled variable-rate nitrogen application trims fertilizer use 8-12%, delivering payback in roughly four years on high-input farms.

Page last updated on: