Tiny Homes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.42 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 4.68% CAGR |

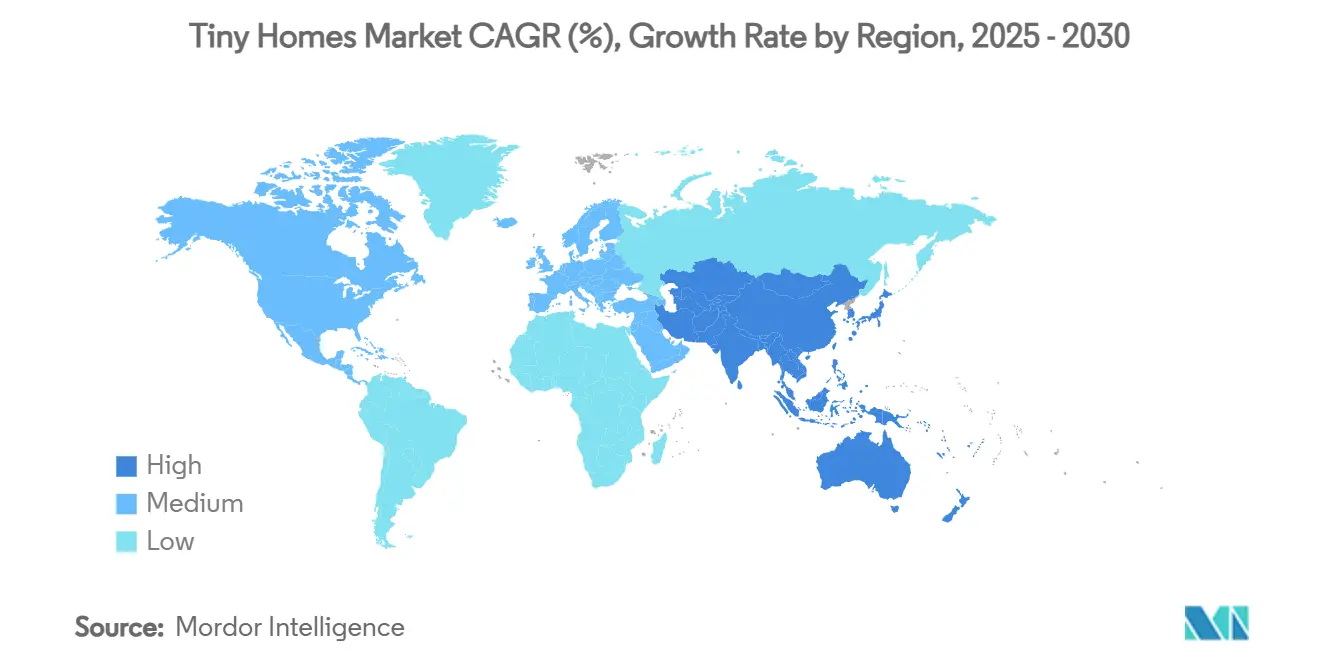

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

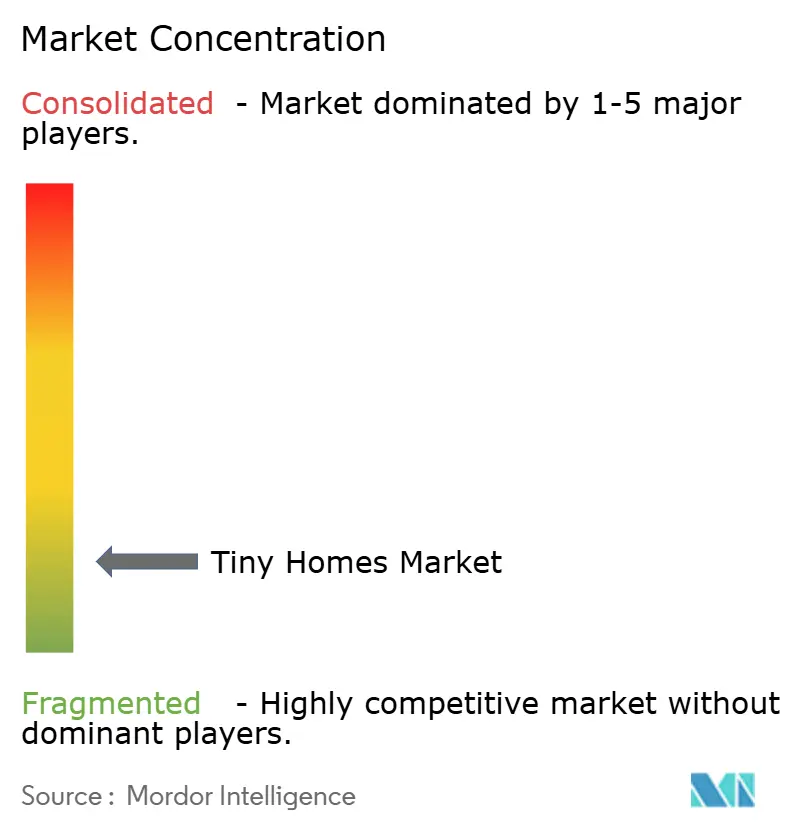

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tiny Homes Market Analysis by Mordor Intelligence

The Tiny Homes Market size is expected to increase from USD 1.36 billion in 2025 to USD 1.42 billion in 2026 and reach USD 1.79 billion by 2031, growing at a CAGR of 4.68% over 2026-2031.

Deepening housing-affordability gaps, median prices topped eight times median household income across major Organisation for Economic Co-operation and Development (OECD) cities in 2025, are steering first-time buyers and retirees toward sub-400-square-foot dwellings that bypass conventional mortgage underwriting. Concurrently, remote work stabilized at 28% of U.S. full-time employees in 2025, untethering location decisions from offices and enabling buyers to site units on lower-cost rural parcels. Corporate fleet procurement, especially from renewable-energy developers and mining firms, adds a volume channel previously absent from single-family residential sales. Timber remains the dominant build material, yet steel-framed designs are gaining traction, while hospitality deployments are emerging as the fastest-growing application. Overall, the tiny homes market is transitioning from a lifestyle niche to an affordability-driven housing substitute, supported by sustainability mandates and flexible work patterns.[1]OECD, “Housing Prices and Income Ratios,” oecd.org

Key Report Takeaways

- By product type, stationary/fixed tiny homes led with 54.10% of the tiny homes market share in 2025, while mobile tiny homes are expected to register a 5.45% CAGR through 2031.

- By material, timber commanded 65.44% of the 2025 value within the tiny homes market size, whereas metal units are forecast to record a 5.94% CAGR through 2031.

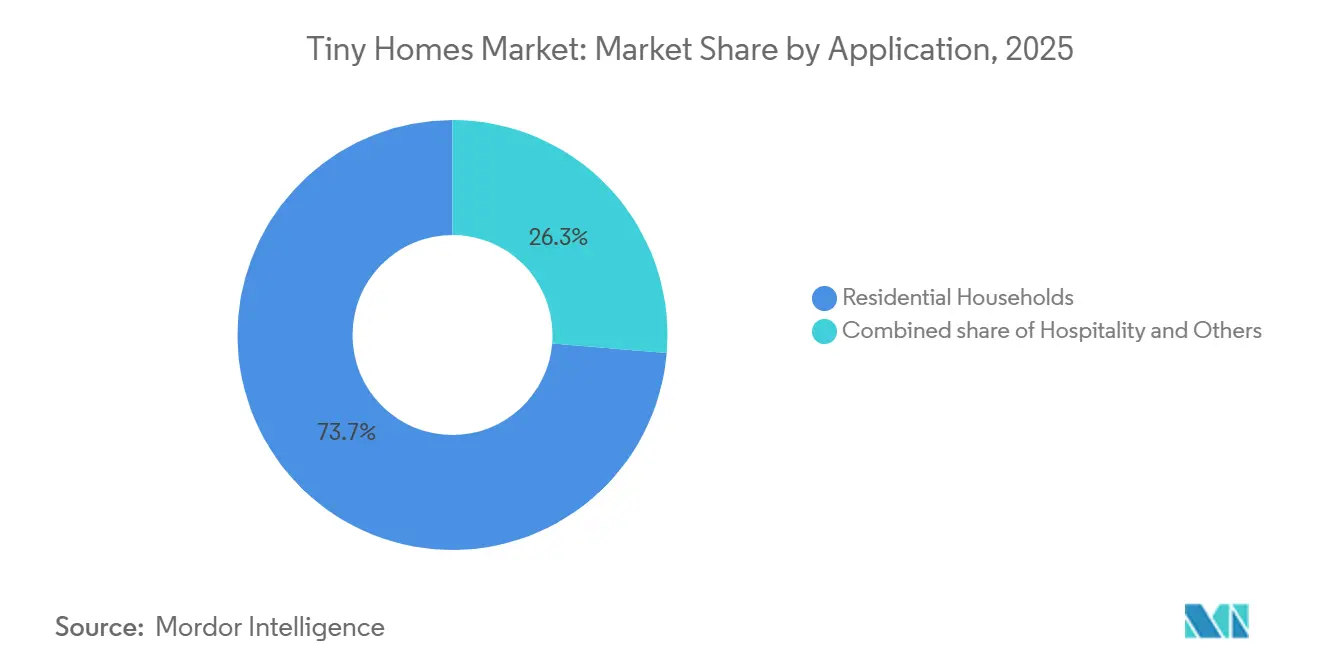

- By application, residential households commanded 73.66% of the tiny homes market share in 2025, while hospitality deployments are set to grow at a 6.16% CAGR through 2031.

- By geography, North America commanded 42.93% of the 2025 value within the tiny homes market size, while Asia-Pacific is anticipated to post the fastest regional growth at a 6.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tiny Homes Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising housing unaffordability drives demand for cost-effective downsizing solutions | +1.2% | Global, with acute pressure in North America, Europe, and the Asia-Pacific urban centers | Medium term (2-4 years) |

| Growing sustainability and net-zero housing initiatives accelerate tiny home adoption | +0.9% | Europe and North America lead; Asia-Pacific emerging | Long term (≥ 4 years) |

| Expansion of remote work enables geographic mobility and supports tiny home living | +0.8% | North America and Europe core; spill-over to Australia and New Zealand | Short term (≤ 2 years) |

| Increasing urban land scarcity in megacities encourages compact housing alternatives | +0.7% | Asia-Pacific megacities (Tokyo, Mumbai, Jakarta); secondary impact in Latin America | Medium term (2-4 years) |

| Corporate fleet adoption for temporary workforce site housing boosts tiny home demand | +0.6% | North America, Middle East (energy projects), Australia (mining) | Short term (≤ 2 years) |

| Inter-generational granny-pod installations rise with ageing populations and family care needs | +0.5% | North America and Europe; early adoption in Japan and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Housing Unaffordability Drives Demand for Cost-Effective Downsizing Solutions

Median purchase prices reached 8.2 times median household income across OECD economies in 2025, an unprecedented affordability gap that is pushing buyers toward USD 40,000–USD 80,000 turnkey tiny homes. Forty percent of U.S. adults under 35 could not cover an unexpected USD 400 expense in 2025, underscoring sensitivity to monthly housing payments. In coastal metros where land routinely exceeds USD 500 per square foot, sub-400-square-foot dwellings present one of the few ownership paths for median earners. Downsizers aged 55 and older, motivated by rising property taxes and the desire to monetize home equity, add a second major demand cohort, with 34% of U.S. baby boomers considering downsizing last year. The affordability wedge is no longer cyclical; it is reshaping the buyer profile, shifting tiny homes from an aspirational lifestyle option to a practical housing solution. [2]Federal Reserve, “Economic Well-Being of U.S. Households,” federalreserve.gov

Growing Sustainability and Net-Zero Housing Initiatives Accelerate Tiny Home Adoption

Twelve European Union member states mandated near-zero-energy performance for new homes by 2025, creating a regulatory tailwind for compact dwellings that naturally require less heating and cooling. International Energy Agency (IEA) studies show that sub-500-square-foot units consume 45% less annual energy than conventional houses. Timber-framed construction sequesters close to 1 metric ton of carbon dioxide per cubic meter of wood, aligning tiny homes with national decarbonization targets. California’s 2025 energy code extended rooftop-solar mandates to accessory units under 800 square feet, spurring manufacturers to bundle photovoltaic packages. Hospitality chains are also adopting tiny clusters to meet Leadership in Energy and Environmental Design (LEED) criteria, signaling that sustainability is now a structural growth driver rather than a marketing add-on.[3]European Commission, “Energy Performance of Buildings Directive,” europa.eu

Expansion of Remote Work Enables Geographic Mobility and Supports Tiny Home Living

Remote work accounted for 28% of U.S. full-time employment in 2025, a level that decouples residential choice from daily commutes. Buyers can now place units on rural land costing USD 5,000–USD 15,000 per acre instead of suburban parcels fetching USD 50,000–USD 200,000, slashing total homeownership outlay. Statistics Canada found that 22% of remote workers relocated to small municipalities between 2023 and 2025, a migration that dovetails with relocatable mobile tiny homes. Trailer-based models let owners follow seasonal work or family obligations without forfeiting their dwelling, thereby reinforcing the value proposition. Corporate policies at leading technology firms confirm remote-first status through 2026, supporting a durable demand base that extends beyond pandemic anomalies.

Increasing Urban Land Scarcity in Megacities Encourages Compact Housing Alternatives

Population densities top 10,000 people per square kilometer in the core districts of Tokyo, Mumbai, and Jakarta, straining land supply and elevating land values. Japan’s Ministry of Land, Infrastructure, Transport and Tourism (MLIT) launched a 2024 pilot allowing micro-units under 200 square feet in central wards, addressing a projected 1.2 million-unit shortfall by 2030. Australia’s New South Wales and Victoria waived parking mandates for secondary dwellings in 2025, unlocking backyard infill opportunities in Sydney and Melbourne, where median house prices exceed USD 650,000. Compact housing supports transit-oriented development, permitting higher densities without resorting to high-rise construction. With Asia-Pacific urbanization advancing toward 70% by 2035, regulatory pilots are expected to mature into permanent codes, scaling demand for tiny formats.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented zoning regulations and building codes restrict legal placement of tiny homes | -0.8% | North America and Europe; less acute in Asia-Pacific due to recent regulatory pilots | Medium term (2-4 years) |

| Limited mortgage options and financing avenues hinder large-scale consumer adoption | -0.6% | Global, with most severe constraints in North America and Europe | Long term (≥ 4 years) |

| Weak secondary resale market reduces long-term investment attractiveness for buyers | -0.5% | Global, particularly North America and Europe where real estate investment culture is established | Long term (≥ 4 years) |

| Perceived lack of space and privacy discourages potential homeowners from downsizing | -0.4% | Global, with cultural resistance strongest in North America and parts of Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Zoning Regulations and Building Codes Restrict Legal Placement of Tiny Homes

Local ordinances categorize tiny dwellings variously as recreational vehicles, accessory dwelling units, or manufactured housing, creating legal gray zones that complicate resale and financing. Fewer than 30% of U.S. counties explicitly addressed tiny homes in 2025 zoning codes, forcing variance applications or limiting placement to rural plots. Europe faces similar fragmentation; Germany’s state-level Bauordnung often requires permanent foundations that negate mobility benefits. Insurance carriers respond by classifying units as RVs, raising premiums. Until harmonized frameworks akin to California’s 2024 ADU reforms proliferate, regulatory friction will cap adoption and dampen investor confidence.[4]U.S. Department of Housing and Urban Development, “Manufactured Housing Codes,” hud.gov

Limited Mortgage Options and Financing Avenues Hinder Large-Scale Consumer Adoption

Conventional mortgages remain unavailable to units without permanent foundations, pushing buyers toward personal or recreational-vehicle loans at 7%–10% interest versus 5%–6% on standard mortgages in 2025. Loan-to-value ratios are difficult to set because secondary-market comparables are scarce, inflating perceived risk for lenders. Canadian banks largely exited the niche in 2025, leaving credit-union products that carry higher down-payment requirements. Manufacturer-backed financing eases some pressure but lacks scale. Without federally backed loan programs or standardized appraisal guidelines, financing will persist as a structural headwind.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Mobile Units Gain Momentum Even as Stationary Remains Dominant

Stationary/fixed tiny homes held 54.10% of the tiny homes market share in 2025, reflecting consumer preference for code-compliant foundations and easier utility hookups. Fixed installations appeal to buyers seeking long-term asset appreciation, yet they require land purchase or long leases, which limit flexibility. Mobile tiny homes, forecast to grow at a 5.45% CAGR through 2031, ride the wave of workforce mobility and seasonal hospitality demand, offering relocatability without sacrificing quality. Construction-sector data show that 12% of U.S. wind- and solar-project laborers used temporary on-site housing in 2025, a niche where mobile tiny homes compete effectively against standard trailers.

Hybrid designs are emerging units built on steel chassis that satisfy International Residential Code (IRC) Appendix Q once sited, allowing owners to retain mobility while meeting strict local codes. Hospitality operators favor mobile clusters that can be redeployed across resorts as seasonal demand shifts, minimizing stranded assets. For manufacturers, the faster-growing mobile segment diversifies revenue and extends addressable markets into events, disaster response, and corporate fleet housing, positioning it as a key growth pillar.

By Material: Timber Leads, Metal Scales on Durability and Transportability

Timber captured 65.44% share of 2025 revenue, leveraging automated saw-line production and favorable carbon accounting, while metal units are projected to advance at 5.94% CAGR to 2031. Wood-framed structures perform well thermally, an advantage in tight envelopes where wall thickness is limited, and they align with Forest Stewardship Council (FSC) certification pathways valued in Europe and North America. However, susceptibility to moisture, pests, and fire raises maintenance costs in humid or wildfire-prone regions.

Steel and aluminum frames deliver superior structural integrity, resist termites, and facilitate longer road transport spans, making them the go-to choice for hospitality chains in hurricane belts and mining operators in seismic zones. Nestron’s 2025 launch of steel-chassis models with anti-corrosion coatings illustrates the shift toward metal for commercial buyers. Recycled content above 80% mitigates embodied-carbon drawbacks, and modular steel systems shorten on-site assembly time. Going forward, material selection will remain use-case specific: timber for residential aesthetics and carbon sequestration, steel for rugged transport and longevity, and emerging composites such as structural insulated panels (SIPs) for energy-efficiency upgrades.

By Application: Hospitality Surges Amid Experiential Tourism Boom

Residential households commanded 73.66% of sales value in 2025, anchored by primary residences, backyard accessory units, and granny pods. Yet hospitality deployments, glamping resorts, eco-lodges, and farm stays are on track for a 6.16% CAGR through 2031, outpacing household demand as travelers seek nature-centric experiences without compromising comfort. U.S. operators added roughly 3,500 tiny-home keys in 2025 at nightly rates of USD 150–USD 250, delivering sub-three-year payback windows.

Rapid factory fabrication means a 10-unit resort can go from purchase order to guest check-in within three months, a fraction of traditional build timelines. Residential demand nonetheless sustains volume, buoyed by state-level fee waivers and streamlined approvals for accessory units in California, Oregon, and Washington. Disaster relief, workforce camps, and pop-up retail form a long-tail of niche uses, but hospitality’s faster growth signals that the tiny homes market is evolving from owner-occupied shelters into income-generating real-asset plays.

Geography Analysis

North America supplied 42.93% of global revenue in 2025 as elevated house prices, high remote-work incidence, and progressive state regulations converged. Approximately 15,000 units were shipped in the United States that year, with sales balanced between affordability seekers and hospitality operators expanding glamping capacity. Canadian growth derives from younger households relocating to smaller municipalities, spurred by provincial pilots relaxing minimum-size rules. Mexico’s coastal tourism sector is experimenting with tiny-home clusters as eco-friendly alternatives to concrete villas. Structural challenges remain chiefly fragmented zoning and scarce mortgage products, but model ordinances under review by the American Planning Association could catalyze a post-2027 acceleration.

Asia-Pacific is the fastest-growing region, poised for a 6.41% CAGR through 2031 thanks to urban land scarcity, supportive pilots, and a rising middle class. Japan’s MLIT micro-housing program in Tokyo and Osaka legalized sub-200-square-foot units, while Australia’s state-level code changes removed parking and lot-coverage hurdles for secondary dwellings. South Korea and China are exploring modular housing for retirees and migrant workers, though national standards lag. India and Indonesia offer longer-run potential once informal-housing norms yield to formal prefabrication. The tiny homes market size in Asia-Pacific could challenge North America’s lead if regulatory timelines stay on track.

Europe remains smaller but strategically vital because net-zero codes elevate the value of compact formats. Germany, France, and the United Kingdom head demand, leveraging state-level Bauordnung reforms and planning-code adjustments that welcome sub-50-square-meter dwellings on existing lots. Scandinavia records high per-capita uptake on environmental grounds, whereas Southern Europe adopts slowly except in agritourism hubs. Although slower population growth tempers upside, carbon-reduction mandates and energy-price volatility offer a durable pull. Beyond the core regions, Latin America and the Middle East & Africa are at an exploratory stage, with isolated projects in Brazilian eco-tourism and Gulf infrastructure camps.

Competitive Landscape

The tiny homes market is fragmented in nature, leaving ample headroom for regional builders and direct-to-consumer startups. Incumbents such as Skyline Champion Corporation and Cavco Industries Inc. leverage vertically integrated lumber mills, factory automation, and dealer networks to gain cost and distribution advantages. Production lines equipped with robotic welding and computer numerical control (CNC) saws trim labor by roughly 30% compared with site builds, reinforcing scale economies.

New entrants, including Nestron, Container Homes USA, and Viva Collectiv, employ modular steel platforms, parametric design software, and online configurators to compress design-to-order cycles and appeal to tech-savvy buyers who prioritize customization. Intellectual-property investments are rising; patent filings in transportable foundations and modular connectors suggest a nascent moat around engineering know-how. Commercial-fleet contracts, such as Cavco’s USD 30 million wind-farm deal announced in January 2026, highlight a strategic white space where volume, repeat orders can underpin factory utilization.

Mergers and acquisitions remain limited but are expected to accelerate as strategic acquirers seek national footprints and omnichannel reach. The possibility of institutional investors bundling hospitality-oriented tiny-home portfolios into real-estate investment trusts could inject fresh capital, further professionalizing the sector. Overall rivalry centers on balancing cost, customization, and code compliance; the competitive environment rewards agility, localized regulatory insight, and relentless efficiency improvements.

Tiny Homes Industry Leaders

Tumbleweed Tiny House Company

Skyline Champion Corporation

Cavco Industries Inc.

Berkshire Hathaway (Clayton Homes)

CargoHome

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Skyline Champion Corporation committed USD 25 million to expand its Sanford, North Carolina, plant, adding 120,000 square feet of robotic welding and automated material-handling capacity expected to yield 1,200 extra units yearly.

- January 2026: Cavco Industries Inc. signed a USD 30 million deal to supply 500 mobile tiny homes over two years for renewable-energy workforce housing across Texas and New Mexico.

- December 2025: Tumbleweed Tiny House Company earned the National Association of Home Builders innovation award for its net-zero Cypress model.

- November 2025: Nestron closed a USD 15 million Series B to expand Chinese production and open a German distribution hub aimed at delivering 800 steel-framed units in 2026.

Global Tiny Homes Market Report Scope

| Mobile Tiny Homes |

| Stationary/Fixed Tiny Homes |

| Timber |

| Metal |

| Concrete |

| Others |

| Residential Households |

| Hospitality |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Rest of Europe | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East and Africa | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific |

| By Product Type | Mobile Tiny Homes | |

| Stationary/Fixed Tiny Homes | ||

| By Material | Timber | |

| Metal | ||

| Concrete | ||

| Others | ||

| By Application | Residential Households | |

| Hospitality | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Rest of Europe | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How big is the tiny homes market in monetary terms?

The tiny homes market size stood at USD 1.42 billion in 2026 and is forecast to reach USD 1.79 billion by 2031.

What is the projected growth rate for tiny homes between 2026 and 2031?

Market value is expected to rise at a 4.68% CAGR during the 2026–2031 period.

Which product type is growing fastest?

Mobile tiny homes are forecast to expand at a 5.45% CAGR through 2031 due to demand from contract workers and hospitality operators.

Which region will post the highest growth?

Asia-Pacific is projected to record the fastest regional CAGR at 6.41% thanks to urban land scarcity and supportive pilot regulations.

What is the main restraint on wider adoption?

Fragmented zoning and limited mortgage products make legal placement and financing difficult, curbing mainstream uptake despite strong demand.

Who are the top market players?

Top market players in the tiny homes market include Skyline Champion Corporation, Cavco Industries Inc., Clayton Homes, Tumbleweed Tiny House Company, and ESCAPE Homes.

Page last updated on: