Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

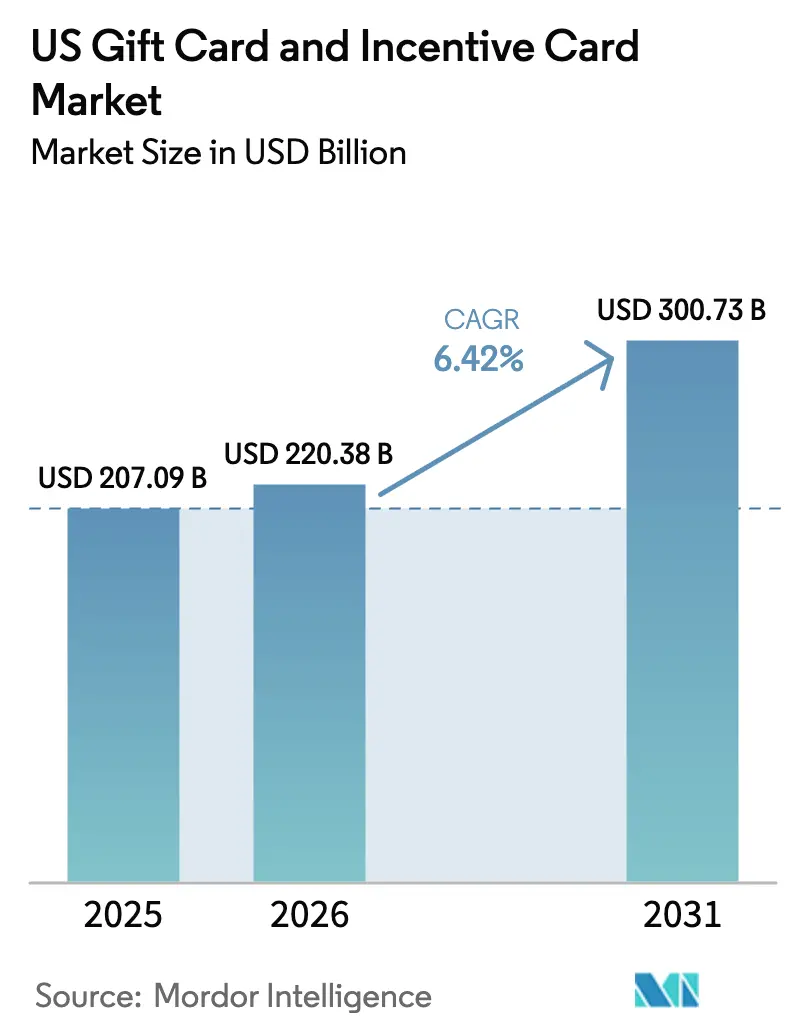

| Base Year Market Size (2025) | USD 207.09 Billion |

| Market Size (2026) | USD 220.38 Billion |

| Market Size (2031) | USD 300.73 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Gift Card And Incentive Card Market Analysis by Mordor Intelligence

The US gift card and incentive card market size was valued at USD 207.09 billion in 2025 and estimated to grow from USD 220.38 billion in 2026 to reach USD 300.73 billion by 2031, at a CAGR of 6.42% during the forecast period (2026-2031). Corporate bulk purchasing, digital wallet integration, and omnichannel retail adoption collectively push card load volumes higher as enterprises embed cards into loyalty, payroll, and HR recognition workflows. Digital formats progress at double-digit speeds, while state-level fraud prevention laws raise compliance costs that favor larger, technology-focused issuers. Platform consolidation accelerates because scale lowers per-card fraud losses and simplifies multi-state regulatory reporting. Continued economic resilience, strong consumer demand for experiential spending, and the proliferation of white-label SaaS solutions sustain broad participation across brands and industry verticals.

Key Report Takeaways

- By card type, closed-loop cards held 61.75% of the US gift card and incentive card market share in 2025, whereas open-loop cards are projected to grow at 8.62% CAGR through 2031.

- By format, digital cards captured 58.35% of the US gift card and incentive card market revenue share in 2025; the segment is expected to post a 11.86% CAGR to 2031.

- By consumer type, corporate B2B purchases accounted for 64.85% of the US gift card and incentive card market size in 2025 and are forecasted to expand at 8.74% CAGR through 2031.

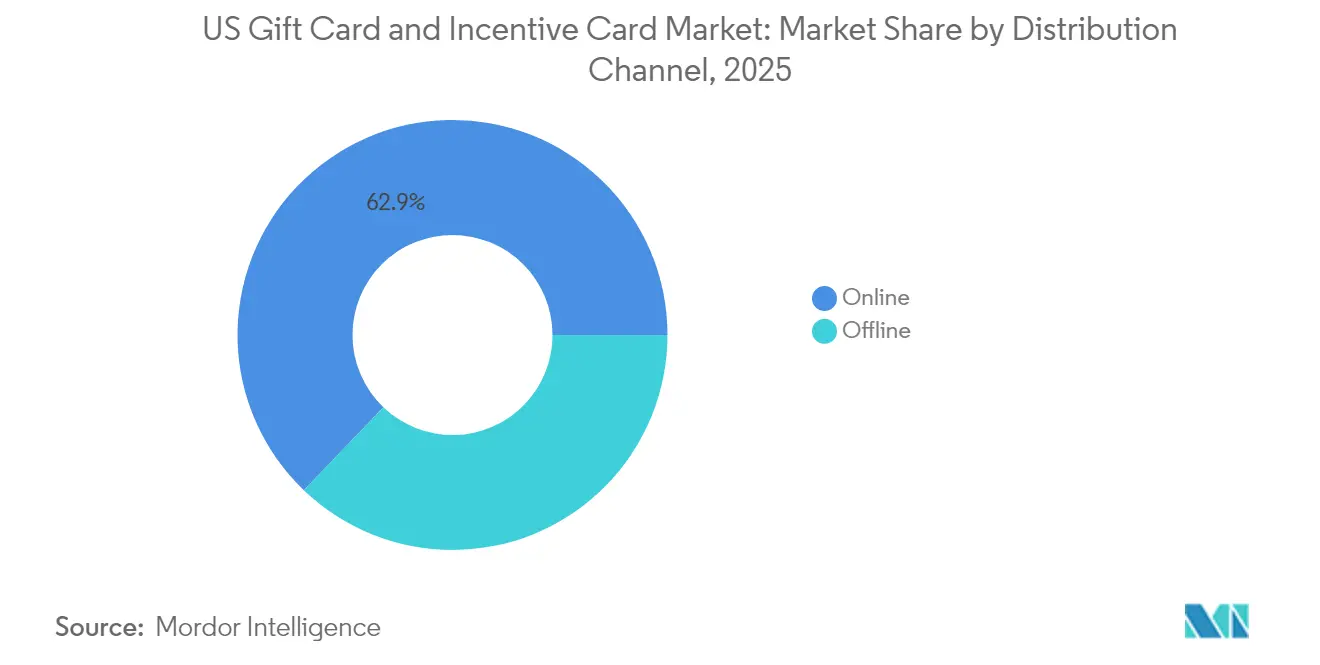

- By distribution channel, online platforms led with 62.85% share of the US gift card and incentive card market size in 2025, while the same channel is expected to advance at 10.78% CAGR to 2031.

- By industry of application, food and beverage dominated with 26.15% share of the US gift card and incentive card market size in 2025; health, wellness, and beauty is the fastest-growing vertical at 9.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Gift Card And Incentive Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift to digital & mobile-wallet gift cards | +1.8% | National, urban concentration | Medium term (2-4 years) |

| Corporate demand for incentive cards in HR & loyalty programs | +2.1% | National, corporate hubs | Long term (≥ 4 years) |

| Omni-channel retail expansion boosts card load volumes | +1.2% | National, retail-dense areas | Short term (≤ 2 years) |

| Gen-Z “self-use” gift-card budgeting trend | +0.9% | National, youth-dense markets | Medium term (2-4 years) |

| State escheatment-law changes spurring bulk B2B issuance | +0.7% | State-specific, national spillover | Long term (≥ 4 years) |

| Rise of white-label SaaS platforms for mid-market brands | +0.6% | National, tech-enabled markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid shift to digital & mobile-wallet gift cards

Mobile wallets have become the default redemption method as Apple Pay and Google Pay acceptance removes the friction of plastic cards at checkout. The Consumer Financial Protection Bureau’s 2024 large-participant rule formalized oversight of payment apps that process at least 50 million transactions, underscoring the systemic role of digital gift cards[1]Consumer Financial Protection Bureau, “CFPB Finalizes Rule to Ensure Big Tech Firms Comply With Consumer Financial Protections,” consumerfinance.gov. Retailers gain higher engagement by embedding brand-specific cards in their own apps, while corporate buyers appreciate the instant fulfillment and audit trails that digital delivery provides. This interplay drives a 12.34% CAGR for digital formats and encourages issuers to prioritize real-time balance updates, partial redemption tools, and loyalty integration features.

Corporate demand for incentive cards in HR & loyalty programs

Enterprises treat cards as flexible, tax-efficient benefits that avoid payroll complexities. Spot bonuses and milestone rewards grow in relevance for remote staff, and loyalty managers increasingly swap physical merchandise for digital gift card redemption. Target’s loyalty revamp, which quadrupled membership and delivered 350 million incremental guest trips compared with 2019, illustrates how card integration lifts visit frequency. High-volume corporate contracts provide forecastable revenue and dampen seasonality for issuers.

Gen-Z “self-use” gift-card budgeting trend

Younger consumers allocate digital cards as category-specific spending envelopes for dining, entertainment, and wellness. PwC’s 2024 holiday survey found 65% of shoppers still planned to buy gift cards, yet Gen Z tilted toward experiences over tangible goods. Retailers respond by marketing cards for budgeting rather than gifting, flattening seasonal peaks, and improving cash-flow predictability.

State escheatment-law changes spurring bulk B2B issuance

Idaho’s 2024 repeal of a de minimis exemption and Maryland’s 2025 packaging mandates illustrate tightening state oversight. Corporations bulk-load cards, then engage recipients before dormancy periods expire to minimize unclaimed balances. Sophisticated tracking software alerts HR teams ahead of escheatment deadlines, benefiting vendors that provide integrated compliance dashboards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating gift-card fraud & scam losses | -1.4% | National, fraud-prone regions | Short term (≤ 2 years) |

| CARD Act & multi-state compliance costs | -0.8% | National, state variation | Medium term (2-4 years) |

| Retailers’ breakage-revenue accounting risk | -0.6% | National, large retailers | Long term (≥ 4 years) |

| Interchange-fee-cap debate on open-loop prepaid cards | -0.4% | National, network dependent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating gift-card fraud & scam losses

Organized fraud rings siphon USD 5.7 billion each year through card-draining tactics that exploit open-loop anonymity[2]Jenna McLaughlin, “Gift Card Theft Is Soaring,” propublica.org. Maryland’s Gift Card Scams Prevention Act now requires tamper-evident packaging and staff training from June 2025, and other states are drafting similar rules. Compliance raises costs for retailers, yet stronger security standards also improve consumer confidence, especially for digital formats that avoid on-shelf exposure.

CARD Act & multi-state compliance costs

Federal limits on fees and expirations combine with a patchwork of state laws covering disclosures, packaging, and employee education. Iowa, Nebraska, and West Virginia introduced statutes mandating fraud warnings on racks, adding training expense for mid-market chains. Issuers must juggle divergent record-keeping protocols, prompting many to outsource compliance management.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Card Type: Open-Loop Growth Challenges Closed-Loop Dominance

Closed-loop programs maintained a 61.75% share of the US gift card and incentive card market in 2025 because branded issuers control pricing and harvest customer data. They rely on app-based balances that create direct engagement, and unit economics improve without network fees. Open-loop competitors nevertheless outpace overall growth at an 8.62% CAGR, propelled by corporate incentive demand for universal acceptance. Maryland’s 2025 security rules that single out network-branded plastics raise execution hurdles, yet Visa’s USD 15.7 trillion transaction backbone assures scalability.

Corporate bulk purchasers increasingly mix both formats, sending open-loop cards for cash-like flexibility and closed-loop cards when encouraging spend with preferred suppliers. Issuers calibrate fraud investments, as open-loop designs shoulder higher attack risk. Meanwhile, closed-loop leaders such as Starbucks deepen loyalty integration to lift reload frequency. The coexistence of formats ensures the US gift card and incentive card market remains segmented by use case rather than a winner-take-all scenario.

By Format Type: Digital Transformation Accelerates

Digital cards accounted for 58.35% share of the US gift card and incentive card market in 2025 and will expand at 11.86% CAGR, well above the overall US gift card and incentive card market. Low production costs, instant delivery, and mobile wallet compatibility drive adoption. Consumers appreciate partial redemptions that track residual value, and corporate administrators prefer downloadable CSV reports that simplify tax filings.

Physical cards continue serving gifting rituals in grocery aisles where tactile presentation still matters. Hybrid use cases abound, for example, QR-coded holiday cards that convert into app-based balances. Fraud mitigation benefits digital products since activation occurs server side rather than on store racks vulnerable to barcode skimming. Regulators now monitor large digital payment facilitators, which reduces perceived risk and stabilizes growth.

By Consumer Type: Corporate Dominance Reshapes Market Dynamics

Corporate buyers controlled 64.85% of the US gift card and incentive card market share in 2025 and are projected to advance at 8.74% CAGR to 2031. HR departments treat cards as morale boosters that bypass payroll taxes, and loyalty teams prize universal redemption that broadens appeal. Centralized procurement APIs link directly to expense-management suites, facilitating same-day distribution for remote staff.

B2C gifting still flourishes around holidays, yet new self-use budgeting behavior among Gen Z targets discretionary spending with brand-specific reloads. Issuers, therefore, personalize marketing by recipient type, offering corporate dashboards for bulk purchasers and gamified saving tools for individual users.

By Distribution Channel: Online Platforms Dominate Growth

Online outlets captured 62.85% share of the US gift card and incentive card market size in 2025 and will climb at 10.78% CAGR. E-commerce embeds card options at checkout, subscription upsells, and loyalty redemptions. These digital placements require near-zero incremental shelf space and enable A/B testing of promotional copy in real time.

Brick-and-mortar remains relevant for impulse purchases, especially in supermarkets where third-party racks host multi-brand cards. Retailers experiment with interactive kiosk displays that print on-demand codes, marrying physical presence with digital fulfillment. Omni-channel redemption supports buy-online-pickup-in-store journeys, tightening the loop between physical and virtual commerce.

By Industry of Application: Food Service Leadership Faces Wellness Challenge

Food and beverage applications held a 26.15% share of the US gift card and incentive card market size in 2025, with Starbucks alone loading USD 3.6 billion in Q1 2024, reinforcing its stature within the US gift card and incentive card industry. Frequent purchase cycles and loyalty tie-ins make restaurant cards sticky.

The health, wellness, and beauty segment is expected to register the fastest 9.32% CAGR as consumers prioritize self-care experiences. Spas, fitness studios, and skincare brands leverage white-label SaaS systems to deploy reloadable cards connected to booking apps. Retailers in electronics, apparel, and home improvement continue steady issuance, but experiential categories steal share as Gen Z budgets toward lifestyle services.

Geography Analysis

Metropolitan regions lead digital uptake because smartphone payments and contactless POS are ubiquitous. Cities such as New York, San Francisco, and Chicago record elevated mobile-wallet redemption, while rural and suburban zones display lingering preference for physical racks. Coastal states exhibit the highest wellness-sector penetration, tied to income levels and consumer health priorities. Midwestern and Southern shoppers still favor food service and general merchandise cards sold in grocery channels.

Corporate headquarters clusters drive B2B volume spikes. Silicon Valley and Seattle technology corridors offer large bundles of open-loop incentives for software engineers, whereas banking hubs like New York favor multi-brand digital catalogs aligned to compliance requirements. State legislation also shapes geography-specific cost structures. Maryland’s packaging mandate and Idaho’s escheatment revisions create early adoption curves for secure designs, with neighboring states monitoring outcomes before implementing copycat laws.

Cross-state workforces require issuers to enable redemption across all 50 states and to handle tax nexus complexities. National retailers, including Walmart and Amazon, leverage their distribution footprints to maintain even gift card availability, offsetting regional economic variability. Regional employment trends influence seasonal velocity; energy-heavy Southern markets swing with oil prices, whereas diversified coastal economies display steadier throughput.

Competitive Landscape

The competitive field is moderately concentrated. Blackhawk Network processed USD 28 billion in transactions and leverages a 220-country reach that few rivals can match. InComm Payments, Fiserv, and PayPal supply white-label or API-first issuance to thousands of brands, while card networks Visa, Mastercard, and American Express monetize open-loop flows. High compliance costs and sophisticated fraud tools raise entry barriers, encouraging M&A as smaller processors seek shelter within larger suites.

Strategic focus revolves around mobile-wallet integration, real-time analytics, and multilayer fraud detection. Visa and Mastercard partner with fintech fraud-intelligence firms, and issuers pilot AI-based transaction-scoring to cut draining attempts. Digimarc estimates a USD 900 million to USD 1.5 billion annual recurring revenue opportunity in secure card barcoding, illustrating vendor diversification toward security layers.

Retailers with sizeable closed-loop programs, such as Starbucks, Target, and Walmart, exploit brand loyalty and store footprints to maintain negotiating leverage with processors. Meanwhile, niche SaaS players like Tango Card and Factor4 focus on developer-friendly APIs targeting HR tech ecosystems. The regulatory burden will likely compress margins but also reduce fly-by-night competition, tilting power toward incumbents that can spread compliance overhead across massive volume.

US Gift Card And Incentive Card Industry Leaders

Blackhawk Network

InComm Payments

Fiserv

PayPal Holdings

Mastercard Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Target Corp announced 350 million more guest trips than 2019 levels during Q4 2024 earnings call, with Target Circle loyalty program membership quadrupling since relaunch, demonstrating gift card integration's role in customer engagement strategies.

- January 2025: Maryland's SB 760 law took effect, requiring merchants selling closed-loop gift cards to implement fraud prevention measures, including conspicuous warning notices and employee training on fraud identification.

- November 2024: Consumer Financial Protection Bureau issued a final rule defining larger participants in the digital payment applications market, requiring companies facilitating 50+ million annual consumer transactions to comply with federal consumer financial laws.

- February 2024: The US Department of Treasury published the National Money Laundering Risk Assessment, identifying gift cards as vulnerable financial instruments due to anonymity and transferability features exploited by criminal organizations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United States gift card and incentive card market as the annual value loaded onto open-loop and closed-loop prepaid cards issued for personal gifting, corporate rewards, and promotional programs, whether distributed in physical plastic or digital form. The figures exclude reloadable payroll cards, general-purpose prepaid debit, and unbranded stored-value products.

Scope exclusion: prepaid payroll and government benefit cards are not covered.

Segmentation Overview

- By Card Type

- Open-Loop Card

- Closed-Loop Card

- By Format Type

- Digital Card

- Physical Card

- By Consumer Type

- Individual (B2C)

- Corporate (B2B)

- By Distribution Channel

- Online

- Offline

- By Industry of Application

- Food and Beverages

- Health, Wellness, and Beauty

- Apparel, Footwear, and Accessories

- Consumer Electronics

- Other Industries

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured interviews and short surveys with card program managers at retailers, human-resource incentive planners, and leading processors across the Northeast, Midwest, and West Coast. These discussions validated average load values, seasonality curves, and the accelerating shift toward mobile-delivered codes, filling gaps left by desk research and confirming model assumptions.

Desk Research

We began with publicly available federal data sets such as Federal Reserve Payments Studies, U.S. Census retail sales tables, and FDIC call-report statistics, which anchor consumer spending and merchant counts. Trade bodies, including the National Retail Federation and the Incentive Marketing Association, supplied annual survey results on card usage occasions, while the Federal Trade Commission's fraud loss statistics helped size breakage and inactive balances. Company filings from listed card processors, plus select insights from D&B Hoovers and Dow Jones Factiva, rounded out issuer revenues, distribution margins, and program launches. This catalogue is illustrative; many additional secondary sources were reviewed to cross-check figures and trends.

Market-Sizing & Forecasting

A top-down spend-pool build begins with household retail outlays and corporate reward budgets, which are then multiplied by verified penetration ratios for gift and incentive cards. Results are corroborated with selective bottom-up checks, sampled processor gross-load volumes, and typical digital card average selling prices to fine-tune totals. Key drivers in the model include: share of online retail sales, corporate employment headcount, average reward spend per employee, closed-loop versus open-loop mix, and digital card adoption rates. Multivariate regression, tested for autocorrelation, forecasts each driver to 2030; scenario analysis overlays unexpected regulatory or fraud shocks. Where bottom-up inputs are sparse, gaps are bridged with midpoint estimates agreed during expert calls.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance screens, peer-analyst cross-checks, and senior sign-off. Reports refresh every twelve months, and we trigger interim revisions if transaction data or major rule changes shift any core variable. Before publication, an analyst revalidates figures so clients receive the latest view.

Why Our US Gift Card and Incentive Card Baseline Commands Reliability

Published market values differ because publishers select varied card types, assume distinct load-to-spend ratios, and refresh at uneven cadences.

Key gap drivers include the inclusion of payroll or benefit cards by some firms, blanket mark-ups for inactive balances, differing digital-to-physical conversion factors, and update cycles that skip recent e-gift surges.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 207.09 B (2025) | Mordor Intelligence | - |

| USD 234.14 B (2025) | Regional Consultancy A | Bundles prepaid debit and store credit balances, inflating base |

| USD 342.95 B (2024) | Industry Tracker B | Applies uniform retailer multipliers and counts loyalty-point breakage as spend |

| USD 223 B (2024) | Consulting Firm C | Projects global growth rates onto U.S. totals and refreshes triennially |

Taken together, the comparison shows that Mordor's disciplined scope selection, annually refreshed variables, and dual-layer validation give decision-makers a balanced, transparent baseline they can trace back to clear assumptions and readily reproduce with publicly available data.

Key Questions Answered in the Report

What is the current value of the US gift card and incentive card market?

The market stands at USD 220.38 billion in 2026 and is forecast to rise to USD 300.73 billion by 2031, reflecting a 6.42% CAGR.

Why are corporate purchases so important to this market?

Enterprises account for 64.85% of the 2025 market size because HR and loyalty teams use cards for tax-efficient rewards that avoid payroll complexity and enable digital delivery.

How quickly is the digital gift card segment growing?

Digital formats already hold a 58.35% share and are projected to expand at a 11.86% CAGR, benefiting from mobile-wallet integration and lower fulfillment costs.

Which industry vertical shows the fastest momentum?

The health, wellness, and beauty segment is expected to lead growth at a 9.32% CAGR as consumers channel discretionary budgets toward self-care experiences.

What are the main regulatory challenges facing issuers?

Rising fraud losses, multi-state compliance expenses under the CARD Act, and new state escheatment rules all elevate operating costs and favor large, tech-savvy providers.

How does fraud legislation affect open-loop and closed-loop cards differently?

Maryland’s 2025 law imposes earlier deadlines for open-loop packaging changes, reflecting higher attack surfaces, whereas closed-loop programs face the same rules four months later.

Page last updated on: