Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.82 Billion |

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 2.45 Billion |

| Growth Rate (2026 - 2031) | 5.22% CAGR |

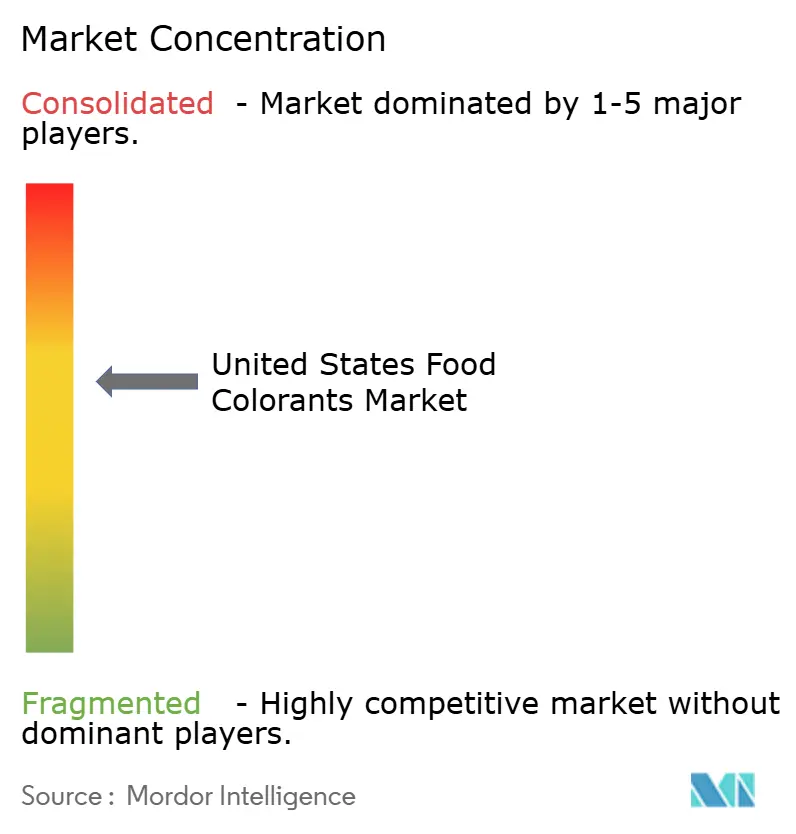

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Food Colorants Market Analysis by Mordor Intelligence

The United States food colorants market size is projected to be USD 1.82 billion in 2025, USD 1.9 billion in 2026, and reach USD 2.45 billion by 2031, growing at a CAGR of 5.22% from 2026 to 2031.Strong retail demand for clean-label products, retailer reformulation requirements, and regulatory clarity regarding plant-derived pigments are driving growth in the United States food colorant market. Natural colorants currently dominate the ingredient landscape, with their increasing application in yogurt, plant-based meat, and functional beverages compensating for the gradual decline in the use of synthetic dyes. Investments in precision-fermentation platforms are helping to reduce historical cost disparities, while advancements in microencapsulation technology are improving pigment shelf life and light stability, particularly in transparent polyethylene terephthalate (PET) bottles. However, supply chain fragmentation for botanicals such as butterfly pea and safflower is causing price volatility, which limits short-term margin growth. Competitive intensity remains moderate, as leading suppliers focus on application-specific innovations to maintain market share against emerging botanical extractors and fermentation-based start-ups.

Key Report Takeaways

- By product type, natural colors held 77.50% of the United States food colorants market share in 2025 and are forecast to grow at 5.81% CAGR through 2031.

- By form, liquids controlled 55.01% of the United States food colorants market size in 2025, whereas powders recorded an 7.92% CAGR over the same horizon.

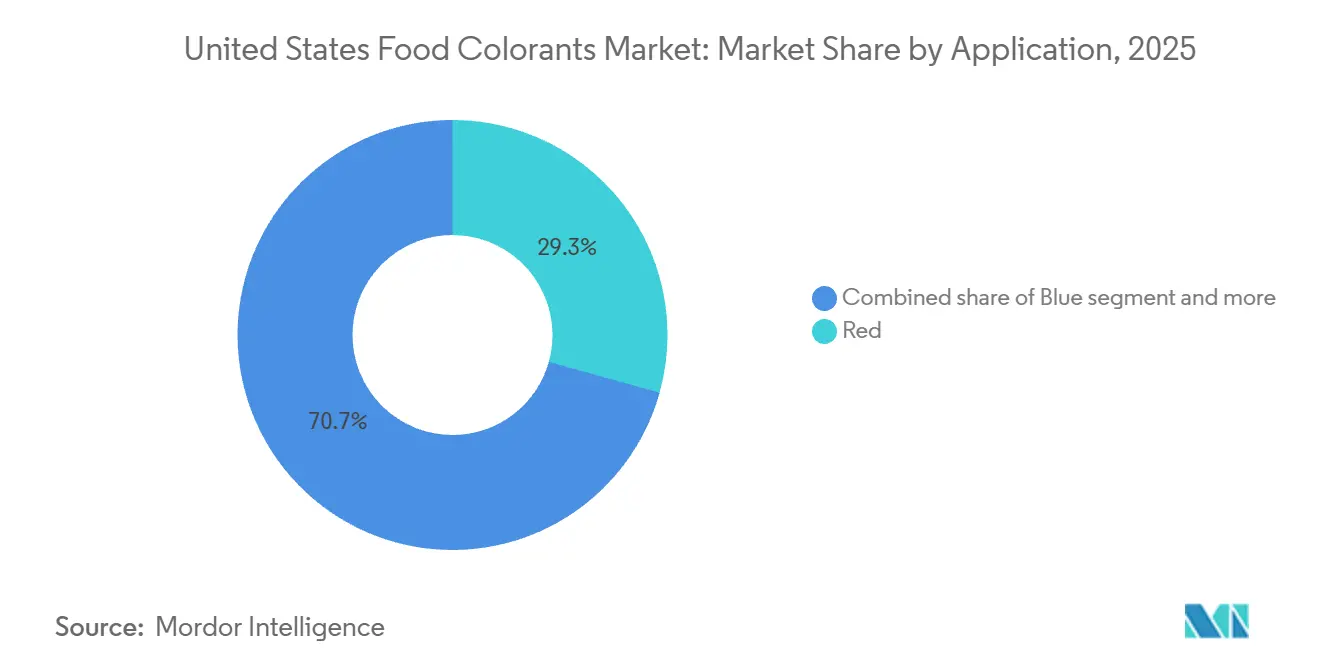

- By color, red dominated with 29.32% revenue contribution in 2025, while blue is set to expand the fastest at 8.58% CAGR to 2031.

- By application, bakery and confectionery represented 25.24% of the United States food colorants market size in 2025; dairy products advance the quickest at 7.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Food Colorants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for clean-label and "no artificial colors" claims | +1.2% | National, with strongest uptake in coastal urban markets | Medium term (2-4 years) |

| Loosening or clarification of "no artificial color" labeling rules for naturally derived colorants | +0.8% | National, FDA jurisdiction | Short term (≤ 2 years) |

| Growth of plant-based, vegan, and allergen-free food formats | +1.0% | National, concentrated in metropolitan areas | Medium term (2-4 years) |

| Strong growth of highly processed and convenience-food categories | +0.9% | National, with rural and suburban gains | Long term (≥ 4 years) |

| Demand from the beverage industry for stable, vivid hues | +0.7% | National, led by functional and sports drink segments | Medium term (2-4 years) |

| Advancements in extraction and formulation technologies improving yield and color intensity | +0.6% | National, R&D hubs in Midwest and Northeast | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising preference for clean-label and "no artificial colors" claims

Consumer demand for transparency has significantly impacted product offerings in grocery aisles. A recent survey revealed that many shoppers in the United States actively avoid artificial colorants when choosing packaged foods. This trend is particularly prominent among millennial and Generation Z households, who carefully review ingredient labels and favor brands utilizing plant-based sources such as beet juice, turmeric, and spirulina. In response, retailers have allocated more shelf space to clean-label stock-keeping units (SKUs), and major private-label programs now mandate natural colorants for new product development. As a result, synthetic alternatives have been largely excluded from high-demand categories like yogurt, granola bars, and refrigerated dips. Economically, this shift demonstrates a willingness to accept higher ingredient costs to achieve premium positioning and address reformulation risks as regulatory standards tighten. Smaller brands are leveraging this trend by using "no artificial colors" claims to compete with established players, securing distribution in natural-channel retailers and e-commerce platforms where such claims enhance click-through rates and drive repeat purchases. According to the International Food Information Council, in 2024, 26% of respondents in the United States identified "Natural" as the best definition of healthy food, while "NON-GMO" accounted for 14% [1]Source: U.S. Food & Drug Administration, “Color Certification Reports,” fda.gov.

Loosening or clarification of "no artificial color" labeling rules for naturally derived colorants

The United States Food and Drug Administration (FDA) issued updated guidance clarifying that colorants derived from fermentation processes using genetically modified microorganisms may qualify as "natural," provided the final product contains no recombinant DNA and the production method resembles traditional fermentation [2]Source: International Food Information Council, “Food Insight, 2024 IFIC Food & Health Survey”, foodinsight.org. This regulatory clarification has encouraged investment in precision-fermentation platforms, with several major suppliers announcing pilot-scale production of beta-carotene, lycopene, and anthocyanins. The guidance resolves a long-standing ambiguity that had deterred food manufacturers from adopting fermentation-derived pigments due to concerns over consumer backlash or regulatory challenges. It also creates a level playing field for suppliers who had invested in fermentation technology but lacked the regulatory certainty to commercialize at scale. The framework established by the Food and Drug Administration for evaluating "naturalness" now prioritizes source material and processing methods over molecular structure. This allows botanical extracts processed with enzymes or supercritical carbon dioxide to carry "no artificial color" claims, even when the extraction yield or purity exceeds that of traditional solvent methods. This change is speeding up reformulation timelines, as brands that were previously hesitant to move away from synthetic options now have access to a wider range of compliant, high-performance natural alternatives.

Growth of plant-based, vegan, and allergen-free food formats

The plant-based food market in the United States demonstrated significant growth in retail sales in 2025, marking a notable increase compared to the previous year. According to the Good Food Institute, 59% of U.S. households purchased plant-based foods in 2024 [3]Source: Good Food Institute, “U.S. retail market insights for the plant-based industry,” gfi.org. This growth is encouraging colorant suppliers to address new formulation challenges. Products such as meat analogs, dairy-free cheeses, and egg replacers require colorants that replicate the appearance of animal-derived products, such as the pink hue of salmon or the golden color of cheddar, without using carmine, which is derived from insects and excluded from vegan formulations. While paprika oleoresin and annatto are commonly used as solutions, their performance in high-moisture, high-fat matrices remains inconsistent. As a result, research and development teams are exploring fermentation-derived heme proteins and precision-fermentation pigments that provide both color and functional benefits. Additionally, allergen-free requirements add complexity, as traditional stabilizers like modified food starch or maltodextrin may cause sensitivities. This has led formulators to pair natural colors with clean-label carriers such as tapioca dextrin or rice syrup solids. The convergence of vegan, allergen-free, and clean-label demands is narrowing the pool of suppliers to those with advanced technical expertise and vertically integrated supply chains capable of ensuring traceability to the farm level.

Strong growth of highly processed and convenience-food categories

Frozen meals, microwaveable entrees, and shelf-stable snacks have significantly expanded their presence in the United States retail market, driven by time-constrained households and the normalization of hybrid work arrangements, which blur traditional meal occasions. These convenience formats present significant technical challenges for colorants, including retort sterilization at high temperatures for extended durations, freeze-thaw cycling, and prolonged ambient shelf life. Carotenoids, such as beta-carotene and annatto, demonstrate better stability under these conditions compared to anthocyanins, which degrade rapidly under heat and oxidative stress, explaining their prevalence in this segment. Microencapsulation is becoming a key solution, with spray-dried or lipid-encapsulated pigments helping to maintain color intensity during processing and storage. However, this technology comes at a cost premium compared to unencapsulated alternatives. The rise in convenience foods is also influencing packaging trends. Single-serve formats and transparent films expose colorants to more light and oxygen per unit volume than bulk packaging, which accelerates degradation. This has prompted suppliers to reformulate with higher initial dosing rates or incorporate light-blocking additives. The growth of this segment is geographically widespread, encompassing urban, suburban, and rural markets. It is also less sensitive to clean-label premiums compared to fresh or refrigerated categories. This has resulted in a bifurcated market where natural and synthetic colorants coexist, with selection driven by application-specific performance requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent FDA regulations and evolving guidance | -0.5% | National, FDA jurisdiction | Short term (≤ 2 years) |

| Technical challenges in matching brand-iconic synthetic hues | -0.7% | National, acute in beverage and confectionery | Medium term (2-4 years) |

| Sourcing-related sustainability and biodiversity concerns | -0.4% | National, with supply-chain exposure to Latin America and South Asia | Long term (≥ 4 years) |

| Supply-chain fragmentation and multi-tier sourcing for some niche botanicals | -0.3% | National, affecting specialty applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent FDA regulations and evolving guidance

The United States Food and Drug Administration's Color Additive Petition process requires manufacturers to provide detailed safety data, stability studies, and manufacturing protocols before approving a new natural colorant for food use. This process can take several years and involves significant costs per petition. Such regulatory requirements place a heavier burden on smaller suppliers and novel pigment sources, such as algae-derived astaxanthin or fruit-derived betalains, which lack the long history of safe use that simplifies approval for established colorants like annatto or carotene. The 2025 guidance from the United States Food and Drug Administration on fermentation-derived colorants, while clarifying certain approval pathways, introduced new labeling requirements. These include the disclosure of the microbial host organism and fermentation substrate, raising transparency concerns among brands cautious of consumer skepticism toward biotechnology. Additionally, evolving state-level regulations add further complexity. For example, California's Proposition 65 requires warning labels for colorants containing trace levels of heavy metals or other compounds, even when these levels are far below the safety thresholds set by the United States Food and Drug Administration. This creates a fragmented compliance landscape, increasing formulation and documentation costs. These regulatory challenges slow innovation cycles and discourage investment in novel colorant platforms, particularly for applications with narrow profit margins or uncertain market acceptance.

Technical challenges in matching brand-iconic synthetic hues

Achieving the vivid and consistent color of synthetic dyes remains the most significant technical challenge for adopting natural colorants, especially for brands whose identity relies on a specific shade, such as the electric blue of a sports drink or the bright red of a candy coating. Natural pigments are prone to batch-to-batch variations caused by factors like soil conditions, harvest timing, and post-harvest handling. This necessitates the use of spectrophotometric quality control and adjustments in dosing rates, which can vary significantly between production runs. Heat stability is another critical issue: anthocyanins degrade at high temperatures, limiting their application in baked goods and retorted products, while carotenoids are susceptible to oxidation during extrusion, leading to off-flavors and color fading. The cost of reformulation, including sensory testing, shelf-life studies, and regulatory filings, can be substantial, discouraging mid-sized brands from transitioning unless driven by significant consumer or retailer demand. Some companies are mitigating risks by maintaining dual inventories of synthetic and natural variants, switching between them based on regional regulatory requirements or customer preferences. While this approach adds operational complexity, it provides flexibility in a fragmented global market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Natural Dominance Reflects Clean-Label Momentum

Natural colorants accounted for 77.50% of the market share in 2025 and are projected to grow at a compound annual growth rate (CAGR) of 5.81% through 2031. This growth is driven by retailer requirements and consumer concerns regarding synthetic additives. Synthetic colorants, while still utilized in cost-sensitive applications such as hard candy and powdered drink mixes, are experiencing a decline in market share as brands reformulate products in anticipation of potential regulatory restrictions. The United States Food and Drug Administration's 2025 clarification that certain fermentation-derived pigments qualify as "natural" has blurred traditional distinctions, allowing suppliers to develop high-intensity, stable colorants that meet clean-label requirements without compromising performance. This regulatory change has spurred increased investment in precision-fermentation platforms, with at least two major suppliers initiating pilot-scale production of beta-carotene and lycopene in 2025.

Synthetic colorants continue to offer advantages in applications requiring extreme pH stability, high-temperature processing, or vivid neon hues that cannot be achieved with plant-based extracts, such as specific sports drinks and novelty confections. However, their use is increasingly limited to export-oriented products or private-label stock-keeping units (SKUs) targeting cost-conscious consumers. The cost disparity between natural and synthetic colorants has decreased from 300% in 2020 to approximately 150% in 2025, driven by advancements in extraction efficiency and economies of scale in botanical sourcing.

By Form: Liquid Leads, Powder Gains on Logistics and Shelf Life

Liquid colorants accounted for 55.01% of the market share in 2025, primarily due to their ease of dispersion in aqueous systems such as beverages, sauces, and dairy products, where uniformity and rapid solubility are essential. Beverage manufacturers, in particular, favor liquid formats as they integrate efficiently into continuous-flow production lines and eliminate the dust-handling challenges associated with powders. However, powder colorants are projected to grow at a Compound Annual Growth Rate (CAGR) of 7.92% through 2031, driven by their longer shelf life, lower transportation costs, and suitability for dry-mix applications, including baking mixes, seasoning blends, and instant beverage powders. A kilogram of powder colorant can replace 3 to 5 kilograms of liquid concentrate, reducing packaging waste and logistics costs, which is an important factor for sustainability-focused procurement teams.

Encapsulation technologies are improving the performance of powder colorants by protecting pigments from oxidation and moisture absorption, thereby extending shelf life from 12 months to 24 months under ambient conditions. Spray-drying and freeze-drying are the predominant encapsulation methods, with freeze-drying preserving more of the original pigment intensity but incurring costs that are 40% to 60% higher.

By Color: Red Dominates, Blue Surges on Functional Beverage Demand

Red colorants accounted for 29.32% of the market share in 2025, driven by carmine, annatto, and beet juice, which are widely used in meat analogs, strawberry-flavored dairy products, and tomato-based sauces. Carmine, derived from cochineal insects, offers exceptional intensity and heat stability but faces challenges due to vegan and allergen-related concerns. This has led suppliers to develop insect-free alternatives, such as lycopene from tomato extract and red radish concentrate.

Blue colorants, although starting from a smaller base, are projected to grow at a compound annual growth rate (CAGR) of 8.58% through 2031. This growth is fueled by spirulina-derived phycocyanin and butterfly-pea extract, which appeal to consumers seeking visually appealing functional beverages and plant-based desserts. However, blue pigments face challenges related to pH sensitivity. For instance, butterfly-pea anthocyanins shift to purple or pink below a pH of 4.0, restricting their use in acidic formulations unless stabilized through methods such as complexation with metal ions or encapsulation. Yellow colorants, primarily turmeric and beta-carotene, are versatile and widely used in applications ranging from cheese and butter to baked goods and snack coatings. They offer good heat stability and are cost-effective. Green colorants, typically created by blending blue spirulina with yellow turmeric or using chlorophyll from alfalfa, are gaining traction in plant-based products designed to replicate the appearance of pesto, matcha, or leafy vegetables. However, chlorophyll is prone to pH-induced color shifts, turning olive or brown in acidic conditions. This has driven research into copper-chlorophyll complexes, although regulatory approval for food use remains limited in the United States.

By Application: Bakery Leads, Dairy Accelerates on Innovation

Bakery applications accounted for 25.24% of the market share in 2025, emphasizing the significant role of colorants in enhancing the visual appeal of icings, fillings, and doughs. These colorants are widely used to signal flavor and freshness, which are critical factors in consumer preferences. Heat stability plays a vital role in baking processes, as oven temperatures often exceed 180°C. This makes carotenoids and annatto the preferred choices due to their ability to withstand high temperatures, unlike anthocyanins, which tend to degrade when exposed to prolonged heat.

Dairy-based products are anticipated to grow at a compound annual growth rate (CAGR) of 7.61% through 2031, representing the fastest growth among all application categories. This growth is primarily driven by advancements in yogurt, cheese, and plant-based dairy alternatives, which demand stable and visually appealing colors that can endure refrigeration and high-moisture environments. For instance, Greek yogurt brands are increasingly incorporating fruit preparations colored with natural ingredients such as beet juice and carrot extract. These additions provide consumers with natural visual cues for flavors like strawberry or peach, while also eliminating the need for artificial additives, aligning with the growing demand for clean-label products.

Geography Analysis

The United States is the sole geographic focus of this analysis, with regional dynamics shaped by consumer demographics, regulatory enforcement, and supply chain infrastructure. Coastal urban markets, particularly the Northeast corridor and West Coast metropolitan areas, exhibit the highest penetration of clean-label products. As of 2025, natural colorants hold a majority share in premium grocery channels within these regions. These areas are home to early-adopter consumers who place a high value on product transparency and are willing to pay premium prices for items that are free from artificial additives. This consumer behavior has driven significant growth in the adoption of clean-label products in these regions.

In contrast, the Midwest and Southern states show slower adoption rates, with synthetic colorants continuing to hold a significant share in value-oriented retail formats such as dollar stores and mass merchandisers. However, even these channels are beginning to introduce natural-colorant stock-keeping units (SKUs) as consumer preferences gradually shift toward more natural options. The supply chain infrastructure across the country varies significantly. Extraction and processing facilities are primarily concentrated in the Midwest and Northeast, leveraging their proximity to key agricultural inputs such as corn, beets, and soybeans. California's Central Valley remains a critical sourcing region for turmeric and paprika. However, challenges such as water scarcity and rising labor costs are encouraging some growers to explore alternative regions or transition to less water-intensive crops to ensure sustainability.

Distribution networks are increasingly optimized for just-in-time delivery to meet market demands efficiently. Liquid colorants, which require cold-chain logistics to maintain their stability, add between 8 and 12 percent to landed costs compared to ambient-stable powders. Regulatory enforcement is consistent at the federal level under the jurisdiction of the Food and Drug Administration (FDA). However, state-level initiatives, such as California's Proposition 65 warnings and New York's transparency mandates, are creating a patchwork of compliance requirements. These state-specific regulations favor suppliers who have robust documentation and traceability systems in place, enabling them to meet the varying requirements effectively and maintain compliance across different regions.

Competitive Landscape

The United States food colorant market exhibits moderate concentration, characterized by a competitive landscape dominated by a few multinational suppliers. These include Sensient Technologies Corporation, BASF SE (Badische Anilin und Soda Fabrik), International Flavors and Fragrances Incorporated, and Archer Daniels Midland Company. These leading companies hold significant market shares through vertically integrated supply chains, global sourcing networks, and extensive technical expertise in formulation and application support. They compete based on the speed of innovation, robust regulatory compliance capabilities, and the ability to co-develop customized solutions with large food manufacturers. This often involves deploying technical service teams at customer sites to address challenges related to color stability, dosing accuracy, and sensory interactions.

Mid-tier suppliers, such as Döhler Group, Oterra, and DSM-Firmenich, differentiate themselves through regional sourcing advantages, specialized botanical portfolios, and quicker time-to-market for emerging pigments like butterfly-pea and purple sweet potato. These companies are gaining traction in high-growth segments, including plant-based foods and functional beverages. Their ability to cater to niche demands and adapt to evolving consumer preferences has allowed them to carve out a significant presence in these expanding markets.

Opportunities are also emerging in the precision-fermentation colorants segment, where both startups and established players are leveraging microbial engineering to produce pigments with enhanced stability, intensity, and sustainability compared to agricultural extracts. For example, a 2025 patent filing by a leading supplier outlined a fermentation process for producing beta-carotene with 95 percent purity and no reliance on agricultural inputs. This innovation positions the technology as a safeguard against climate-induced supply disruptions, offering a more sustainable and reliable alternative to traditional agricultural methods.

United States Food Colorants Industry Leaders

Archer Daniels Midland Company

BASF SE

Sensient Technologies Corporation

Givaudan S.A.

International Flavors & Fragrances Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Oterra and Vaxa Technologies launched Arctic Blue, a spirulina-derived natural blue designed to meet the growing demand for clean-label and plant-based food colorants. This product was characterized by its neutral aroma, making it suitable for various applications, and its rapid dissolution, which enhanced ease of use in food and beverage formulations.

- January 2025: Döhler Group inaugurated a research and innovation center in Princetown, New Jersey. This facility was designed to enhance the company's capabilities in driving research and innovation, with a specific focus on discovering and developing new natural ingredients to meet evolving market demands and consumer preferences.

- December 2024: Oterra expanded its footprint in the United States with the opening of a 155,000-square-foot facility in Mt. Pleasant, Wisconsin. This facility integrated innovation and application laboratories with manufacturing and logistics, addressing the rising U.S. demand for natural colors. Notably, the site included an additional 40,000 square feet reserved for future expansions, new color products, and pilot production lines, supporting food and beverage manufacturers in their transition to natural color solutions.

- September 2024: Oterra unveiled six new vibrant variants to its I-Colors® line. The launch of I-Colors Bold catered to the rising appetite for intense hues, all while prioritizing consumers' preference for natural ingredients.

United States Food Colorants Market Report Scope

Food coloring, whether natural or synthetic, is a substance used to add or enhance color in food products. It serves multiple purposes, such as improving the natural appearance of food, adding color to otherwise colorless items, or differentiating between various flavors. The United States Food Colorants Market is segmented as follows: by product type, including natural colors and synthetic colors; by form, including powder and liquid; by color, including blue, red, green, yellow, and others; and by application, including bakery, confectionery, dairy-based products, meat and seafood, beverages, dietary supplements, snacks and cereals, and others. Additionally, the beverages segment is further divided into alcoholic and non-alcoholic beverages. The market sizing has been done in value terms in USD and volume in Tons for all the abovementioned segments.

By Product Type

| Natural Color |

| Synthetic Color |

By Form

| Powder |

| Liquid |

By Color

| Blue |

| Red |

| Green |

| Yellow |

| Others |

By Application

| Bakery | |

| Confectionary | |

| Dairy-based Products | |

| Meat and Seafood | |

| Beverage | Alcoholic Beverages |

| Non-Alcoholic Beverages | |

| Dietary Supplement | |

| Snacks and Cereals | |

| Others |

| By Product Type | Natural Color | |

| Synthetic Color | ||

| By Form | Powder | |

| Liquid | ||

| By Color | Blue | |

| Red | ||

| Green | ||

| Yellow | ||

| Others | ||

| By Application | Bakery | |

| Confectionary | ||

| Dairy-based Products | ||

| Meat and Seafood | ||

| Beverage | Alcoholic Beverages | |

| Non-Alcoholic Beverages | ||

| Dietary Supplement | ||

| Snacks and Cereals | ||

| Others | ||

Key Questions Answered in the Report

How large is the United States food colorant market in 2026?

The United States food colorant market size stands at USD 1.90 billion in 2026 and is on track to reach USD 2.45 billion by 2031.

Which segment grows fastest within United States food colorants?

Blue pigments lead growth at an 8.58% CAGR to 2031, driven by spirulina and butterfly-pea use in functional drinks.

Why are natural colorants gaining share so quickly?

Clean-label consumer demand and FDA guidance that fermentation pigments qualify as natural are shifting formulations away from synthetics despite higher costs.

What drives powder format adoption?

Encapsulation technology now delivers 24-month shelf life and lower freight weight, which fuels a 7.92% CAGR for powder colorants.

Which application will add the most incremental value?

Dairy-based products show the fastest 7.61% CAGR as yogurt and cheese lines seek vibrant stable hues for refrigerated displays.

Page last updated on: