Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

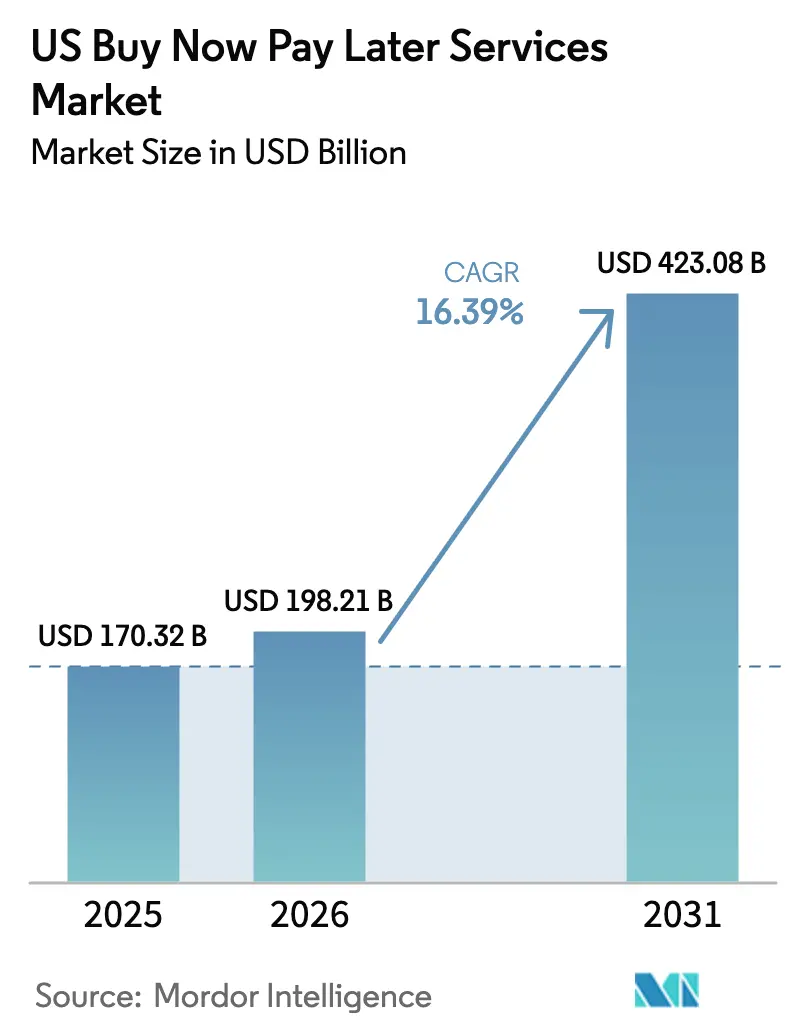

| Base Year Market Size (2025) | USD 170.32 Billion |

| Market Size (2026) | USD 198.21 Billion |

| Market Size (2031) | USD 423.08 Billion |

| Growth Rate (2026 - 2031) | 16.39% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Buy Now Pay Later Services Market Analysis by Mordor Intelligence

The buy now, pay later (BNPL) services market size in the United States was valued at USD 170.32 billion in 2025 and estimated to grow from USD 198.21 billion in 2026 to reach USD 423.08 billion by 2031, at a CAGR of 16.39% during the forecast period (2026-2031). Expansion is being fueled by younger shoppers gravitating toward short-term, interest-free installments, merchant demand for higher conversion at checkout, and the steady migration of embedded finance tools into sectors such as healthcare, travel, and home improvement. Fintech incumbents continue to lead on user experience, yet banks are quickly matching their reach by embedding installment functionality into existing card portfolios. Heightened competition is spurring investment in advanced underwriting models, data-driven loyalty programs, and omnichannel acceptance that ties together e-commerce sites, mobile wallets, and physical terminals.

Key Report Takeaways

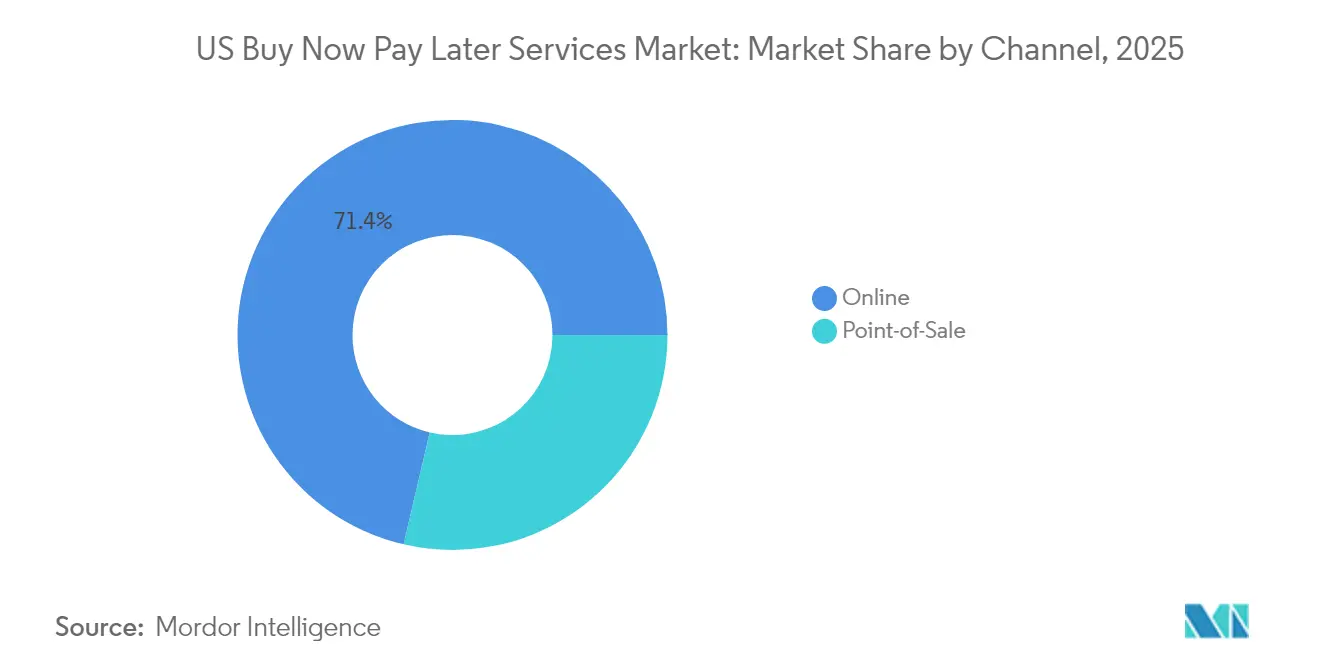

- By channel, online commerce commanded 71.35% of the United States BNPL market share in 2025, while in-store transactions are expected to post the fastest growth at 19.15% CAGR through 2031.

- By end-use industry, fashion and apparel led with 27.85% share of the United States BNPL market in 2025; healthcare and wellness is projected to expand at a 19.88% CAGR through 2031.

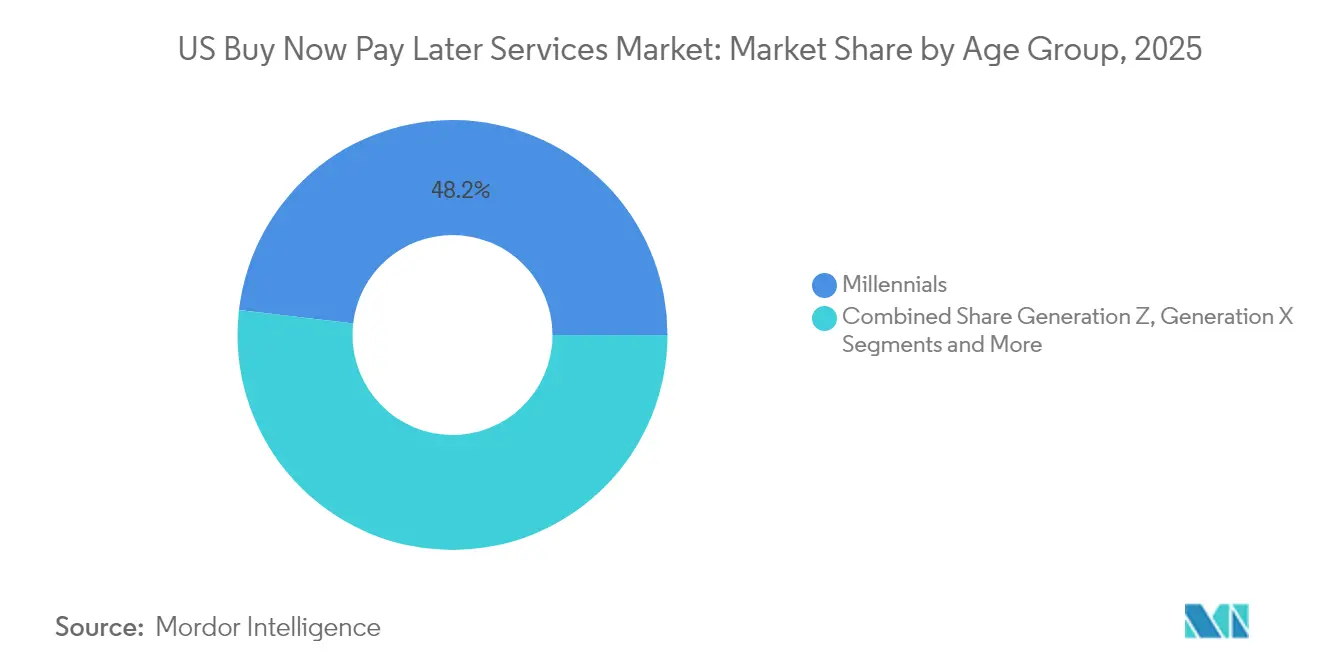

- By age group, millennials accounted for 48.15% share of the United States BNPL market in 2025, whereas Generation Z adoption is forecasted to climb at a 21.52% CAGR through 2031.

- By provider type, fintech companies held 56.95% of the BNPL market size in 2025; banks are the fastest-growing cohort with a 21.19% CAGR outlook.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Buy Now Pay Later Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Millennial & Gen Z Preference for Interest-Free Short-Term Credit | +4.2% | National, higher in urban centers | Medium term (2-4 years) |

| Expansion into Non-Retail Verticals such as Healthcare & Travel | +3.8% | National, early adoption in metropolitan areas | Long term (≥ 4 years) |

| Deep Integration with Digital Wallets and POS Systems Boosting Merchant Adoption | +3.1% | National, concentration in tech-forward regions | Medium term (2-4 years) |

| Strategic Partnerships with Major Card Networks Enhancing Distribution Reach | +2.5% | National | Short term (≤ 2 years) |

| Rising Demand from Sub-prime and Near-prime Consumers Excluded from Traditional Credit Cards Accelerating BNPL Penetration | +2.1% | Medium term (2-4 years) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Millennial & Gen Z Preference for Interest-Free Short-Term Credit

Close to 46% of Gen Z consumers used a BNPL option in 2025, nearly doubling their 2023 participation. Short-term installment plans align with young adults’ budgeting style, which values predictable repayment schedules and zero-interest costs over revolving balances. Eighty-one percent of Gen Z customers state they will abandon brands that provide poor payment experiences, underscoring the competitive stakes for merchants. The same cohort also ranks payment flexibility as critical in business relationships, signaling spill-over effects into B2B commerce. As Gen Z’s earnings rise, their entrenched preference for BNPL is likely to steer broader payment behavior for decades.

Expansion into Non-Retail Verticals such as Healthcare & Travel

Rising out-of-pocket medical expenses have turned healthcare into the fastest-growing vertical for BNPL. Sunbit, for example, partners with roughly 7,300 healthcare providers to fund treatments valued between USD 60 and USD 10,000. Travel has mirrored this momentum, registering a 289% jump in BNPL booking volume in 2024[1]AFM, “Installment Payments in Travel Bookings 2024,” afm.nl. Consumers using installments spend 70% more per trip, lifting airline, hotel, and OTA revenues. By catering to essential and high-ticket purchases, BNPL platforms diversify revenue beyond discretionary retail and mitigate cyclicality.

Deep Integration with Digital Wallets and POS Systems Boosting Merchant Adoption

Digital wallets captured a 50% share of US transactions by 2025, up from 36% in 2023. Embedding BNPL choices inside wallets lowers technical barriers for merchants and lets shoppers tap a single interface across online and in-store checkouts. Retailers report conversion lifts of 20-30% and average-order-value gains of 30-50% once installments are enabled. Payment processors are extending this reach by integrating BNPL rails directly into existing terminals, accelerating omnichannel uptake.

Strategic Partnerships with Major Card Networks Enhancing Distribution Reach

Card-network programs such as Mastercard Installments and Visa Installments insert BNPL functionality into cards already carried by millions of Americans. The share of issuers offering such plans rose to 36% in 2024. These alliances give fintech brands exposure to entrenched merchant networks while helping networks boost transaction volume. Klarna’s collaboration with JPMorgan ahead of its US IPO illustrates the credibility lift and distribution leverage that card-network ties confer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| CFPB and State-Level Regulatory Scrutiny of BNPL Fee Structures is Escalating | -2.30% | National, varying by state | Medium term (2-4 years) |

| Rising Delinquency Rates Impacting Provider Profitability | -1.80% | National, higher in lower-income regions | Short term (≤ 2 years) |

| Intensifying Competition from Traditional Card Issuers’ Installment Products | -1.50% | National, concentrated in urban markets | Medium term (2-4 years) |

| Shrinking Merchant Service Fees Squeezing BNPL Profit Margins | -1.20% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating CFPB & State-Level Regulatory Scrutiny on Fee Structures

In May 2024, the Consumer Financial Protection Bureau (CFPB) classified certain digital BNPL loans as “credit cards” under Regulation Z[2]Consumer Financial Protection Bureau, “Buy Now, Pay Later: Market Trends and Consumer Impacts,” consumerfinance.gov, compelling providers to handle disputes, refunds, and billing statements similarly to card issuers. Although the CFPB announced in April 2025 that it would not prioritize enforcement while reviewing the rule, providers still face compliance investments and potential state-level measures such as New York’s proposed Buy Now Pay Later Act. Smaller firms may struggle with added costs, quickening consolidation.

Rising Delinquency Rates Impacting Provider Profitability

Roughly 30% of BNPL installments were past due in January 2025. Economic stress is pushing borrowers toward late payments, especially on zero-interest plans that lack price buffers. Klarna has refined its underwriting to stem credit losses in the United States. Providers are pivoting to hybrid models that mix short, no-interest terms with longer, interest-bearing options, enabling risk-based pricing and diversified income.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Channel: Omnichannel Acceptance Lifts In-Store Momentum

The BNPL market size for online commerce totaled 71.35% revenue share in 2025. In-store usage, however, is growing faster at a 19.15% CAGR through 2031, signaling merchants’ push to mirror digital flexibility on the sales floor. Retailers deploying unified checkout flows report double-digit conversion gains as shoppers opt for installments on high-ticket items. Hardware integrations with major payment processors simplify rollouts, yet continued user education is required to lift in-aisle visibility.

Omnichannel solutions allow customers to pre-qualify via mobile apps and complete transactions at staffed lanes or self-checkout. The practice is particularly popular in consumer electronics and furniture showrooms where financing decisions occur near physical inventory. The BNPL market stands to capitalize on blended journeys as shoppers browse online, reserve products, and conclude purchases in store. Bridging channels also serves older demographics that prefer brick-and-mortar environments but welcome flexible pay options.

By End-Use Industry: Healthcare Surges Ahead of Fashion Leader

Fashion and apparel retained a 27.85% share of the BNPL market size in 2025. Healthcare is expected to surpass other verticals with a 19.88% CAGR to 2031 on the back of rising medical deductibles and elective-care demand. Sunbit’s network of 7,300 dental and medical offices showcases early traction. High-value travel bookings follow closely, benefiting airlines and OTAs that see ticket sizes jump once installments appear at checkout.

Broadening into non-retail arenas stabilizes volume during retail cycles. Home improvement chains are integrating BNPL for appliance replacements and renovation projects, while streaming and gaming brands use installments to lower subscription churn. Such diversification reduces reliance on discretionary apparel spend and positions providers in sectors with structural financing needs.

By Age Group: Generation Z Sets the Growth Pace

Millennials accounted for 48.15% of US BNPL users in 2025. Generation Z is forecast to compound at 21.52% annually through 2031 as new workforce entrants favor budgeted, interest-free schedules over revolving credit. Nearly 42% of Gen Y and Gen Z consumers used installments in 2025 compared with 21% of older cohorts.

Generation X typically leverages BNPL for larger purchases such as home upgrades, while baby boomers participate less frequently but register higher average values when they do. Peer influence and social-shopping features embedded in BNPL apps continue to expose older customers to installment culture, underlining long-term demographic upside for the BNPL market.

By Provider: Banks Narrow the Gap with Fintech Leaders

Fintechs secured 56.95% of transaction volume in 2025, reflecting early entry and digital design. Banks, however, are expanding at a 21.19% CAGR as they fold installments into mainstream cards and mobile apps. Issuers benefit from low funding costs and decades of underwriting data, allowing competitive pricing and instant approval within existing customer portals.

Card networks amplify this trend by offering issuer-agnostic BNPL rails. Retailers are also testing proprietary frameworks that tie financing to loyalty rewards, creating a multilayer ecosystem. Intense rivalry is prompting M&A as scale advantages grow more important for funding, compliance, and data analytics.

Geography Analysis

Metropolitan areas such as San Francisco, Seattle, and Austin show the highest penetration, driven by large cohorts of tech-savvy millennials and Gen Z consumers. Yet the regional gap is shrinking as nationwide retailers roll out omnichannel BNPL and smaller towns adopt digital wallets. States with larger underbanked populations exhibit above-average usage, reflecting the product’s appeal to credit-invisible borrowers.

Regulatory patchwork remains a top geographic variable. California, New York, and Massachusetts are evaluating bespoke disclosure and licensing rules, adding complexity for nationwide operators. Providers must calibrate compliance workflows while ensuring uniform customer experiences. Economic conditions also matter: regions with volatile employment records rely more on flexible installments to manage cash flow, a trend most evident in parts of the Southeast and Midwest.

Tourism-heavy states such as Florida and Nevada are benefiting from BNPL’s surge in travel spending. Healthcare-driven adoption is prominent in the Sun Belt, where population growth and out-of-pocket costs intersect. As providers partner with regional hospitals and clinics, penetration is expected to deepen in suburban and rural communities, broadening the BNPL market’s geographic footprint.

Competitive Landscape

The US BNPL market exhibits moderate concentration, leaving opportunities for niche disruptors to emerge. Leading fintechs are evolving into multi-service platforms that combine shopping feeds, debit cards, and budgeting tools. Klarna’s advertising revenue jumped from USD 13 million in 2020 to USD 180 million in 2024, exemplifying how monetizing data can offset fee compression.

Banks counter with balance-sheet strength and trusted brands, while card networks play ecosystem orchestrator. Strategic alliances—such as Klarna’s collaboration with JPMorgan—underscore the shift toward hybrid models that blend fintech agility with incumbent scale. White-space opportunities persist in healthcare, education, and B2B invoice financing, where specialized risk engines can command premium spreads.

Technology is the decisive differentiator: providers invest heavily in AI-driven credit scoring, real-time fraud detection, and personalized offers. Blockchain-based smart-contract platforms are emerging, promising lower operating costs and transparent repayment tracking, though mainstream adoption remains early. Competitive intensity is expected to spur consolidation as smaller firms struggle to absorb compliance overheads and shrinking merchant fees.

US Buy Now Pay Later Services Industry Leaders

Affirm Holdings Inc.

Klarna Bank AB

Afterpay Ltd (Block Inc.)

PayPal Holdings Inc.

Zip Co Ltd (Quadpay)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: CFPB stated it will not prioritize enforcement of its 2024 BNPL interpretive rule while considering rescission.

- March 2025: Klarna secured Walmart as a customer ahead of its IPO, expanding access to Walmart’s large shopper base.

- February 2025: Affirm posted a 47% revenue rise to USD 770 million and grew its user base to 21 million.

- February 2025: Block expanded its BNPL share through Cash App integration, intensifying competition with Affirm and PayPal.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study counts the US buy now pay later (BNPL) services market as the gross merchandise value of goods and services purchased by US consumers through short-term, interest-free or low-fee pay-in-installment or pay-in-30 plans offered at checkout by fintechs, card networks, and banks.

Scope exclusion: Post-purchase balance-conversion programs and loans longer than twelve months are not included.

Segmentation Overview

- By Channel

- Online

- Point-of-Sale (In-store)

- By End-Use Industry

- Consumer Electronics

- Fashion & Apparel

- Healthcare & Wellness

- Home Improvement

- Travel & Leisure

- Media & Entertainment

- Other End-Use Industries

- By Age Group

- Generation Z (18-28 Years)

- Millennials (29-44 Years)

- Generation X (45-60 Years)

- Baby Boomers (61-79 Years)

- Silent Generation (80 Years and Above)

- By Provider

- Fintechs

- Banks

- Others

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with BNPL platform executives, leading omnichannel merchants, payment-gateway integrators, and credit-risk consultants across the Midwest, West Coast, Northeast, and Sunbelt to confirm adoption curves, underwriting shifts, and delinquency ratios that secondary work could not fully explain.

Desk Research

We began with tier-one public datasets: US Census retail e-commerce sales, Federal Reserve consumer-credit tables, CFPB BNPL loan files, and Adobe Digital Index holiday spend metrics, which anchor total spend, borrower mix, and seasonality. National Retail Federation checkout-share surveys, Electronic Transactions Association white papers, and peer-reviewed credit-behavior studies refined channel splits and elasticity factors.

To size provider volumes and fees, our team parsed filings and press releases in D&B Hoovers and Dow Jones Factiva, while shipment data from Volza highlighted in-store terminal roll-outs. The sources named are illustrative; many additional public and paid references informed validation.

Market-Sizing & Forecasting

A top-down model applies BNPL checkout penetration, average ticket size, and purchase frequency to total US retail and travel expenditure; selective bottom-up checks provider disclosures and sampled average-selling-price × transactions adjust totals where gaps appear. Key inputs include Adobe basket values, CFPB default rates, Fed funds path, smartphone BNPL app downloads, and consumer-confidence scores. Five-year projections use multivariate regression tied to real disposable income, e-commerce share, and card-rate spreads, with scenario analysis for regulatory tightening.

Data Validation & Update Cycle

Outputs pass variance filters, senior analyst review, and cross-benchmarking before sign-off. Models refresh each summer, with interim updates triggered by material CFPB rulings or provider SEC filings.

Why Mordor's US Buy Now Pay Later Services Baseline Commands High Credibility

Published estimates diverge because some firms measure provider fee revenue, others quote GMV, and refresh cadences vary.

Recent publications illustrate the gap: one consultancy values 2023 US BNPL revenue at only USD 2.01 billion, another analyst house pegs 2024 GMV at USD 36.4 billion, while a data publisher cites USD 70 billion for 2023. Each applies differing scopes or outdated baselines, whereas Mordor reports GMV for transactions up to twelve months, harmonized to constant 2024 dollars and refreshed annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 170.32 B (2025) | Mordor Intelligence | - |

| USD 2.01 B (2023) | Global Consultancy A | Counts only provider fee revenue, omits GMV |

| USD 36.4 B (2024) | Industry Analyst B | Online GMV only; excludes bank/card-network plans |

| USD 70 B (2023) | Data Publisher C | Pandemic-era growth assumed forward; limited regulatory adjustment |

Taken together, the comparison shows that by unifying scope, currency, and timely inputs, Mordor Intelligence delivers a balanced, transparent baseline that decision-makers can depend upon.

Key Questions Answered in the Report

What is the current size of the US buy now, pay later market?

The market was valued at USD 198.21 billion in 2026 and is projected to reach USD 423.08 billion by 2031.

Which channel is expanding fastest in BNPL?

In-store, point-of-sale BNPL is forecast to grow at 19.15% CAGR between 2026 and 2031, outpacing online growth.

Why is healthcare seen as a key growth vertical for BNPL?

Rising out-of-pocket medical costs and the need for immediate financing are driving a 19.88% CAGR in healthcare BNPL through 2031.

How are banks competing with fintechs in BNPL?

Banks embed installment plans into existing cards and mobile apps, leveraging low funding costs and trusted brands while growing at a 21.19% CAGR.

What regulatory risks face BNPL providers?

The CFPB’s evolving stance on applying credit-card rules to BNPL and diverse state proposals introduce compliance costs that could slow growth.

Are delinquencies a major concern for BNPL firms?

Yes. Around 30% of BNPL installments were past due in early 2025, prompting providers to tighten underwriting and diversify revenue sources.

Page last updated on: