Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

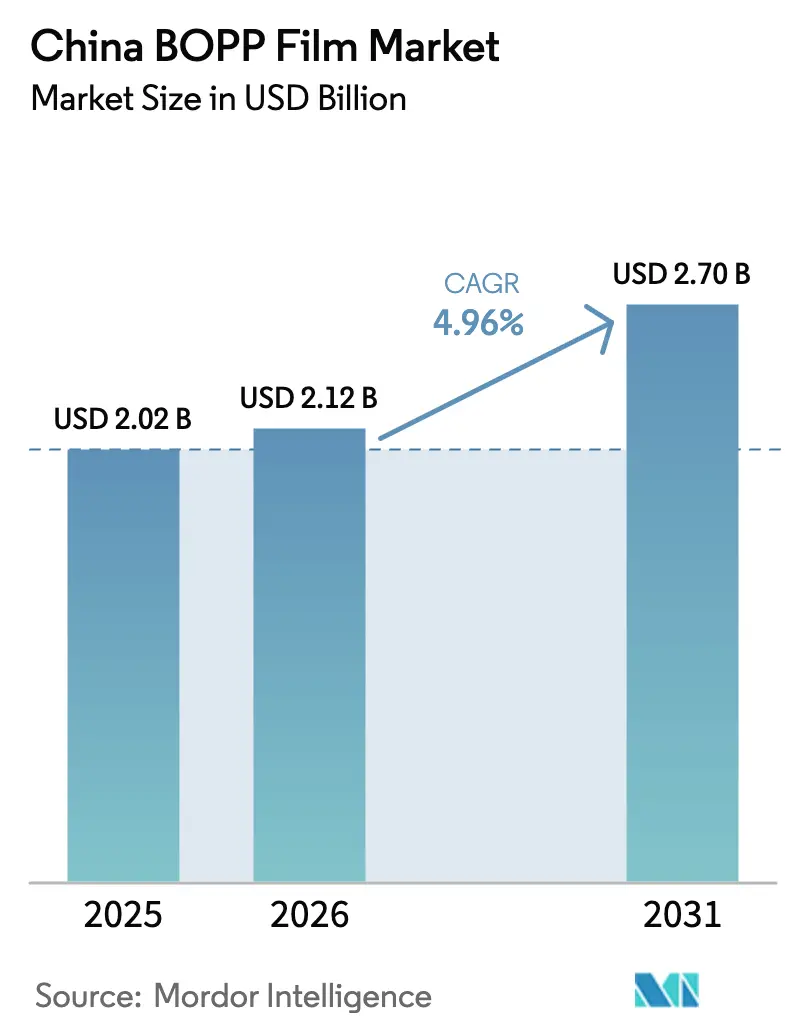

| Base Year Market Size (2025) | USD 2.02 Billion |

| Market Size (2026) | USD 2.12 Billion |

| Market Size (2031) | USD 2.7 Billion |

| Growth Rate (2026 - 2031) | 4.96% CAGR |

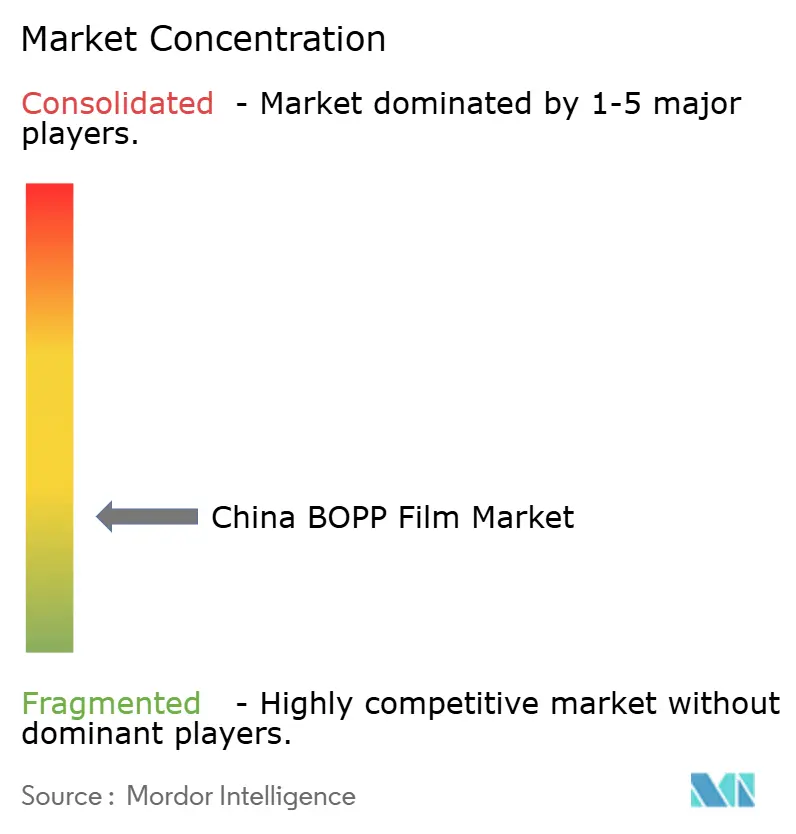

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China BOPP Film Market Analysis by Mordor Intelligence

China BOPP film market size in 2026 is estimated at USD 2.12 billion, growing from 2025 value of USD 2.02 billion with 2031 projections showing USD 2.7 billion, growing at 4.96% CAGR over 2026-2031. Continuing growth rests on strong domestic demand from food, beverage and e-commerce channels, steady upgrades of tenter-line technology and expanding investments in specialty grades such as lithium-battery separator film. Transparent grades keep wide adoption in mainstream laminations while metallized, opaque and high-barrier structures unlock new value pools in snacks, nutraceuticals and premium labels. Cost discipline remains critical as polypropylene resin still accounts for more than 70% of total production cost, prompting thin-gauge innovation and strategic feedstock sourcing. At the same time, regulatory momentum around food-contact safety and national recycling frameworks is nudging converters toward compliant, mono-material formats that are easier to recover at end-of-life.

Key Report Takeaways

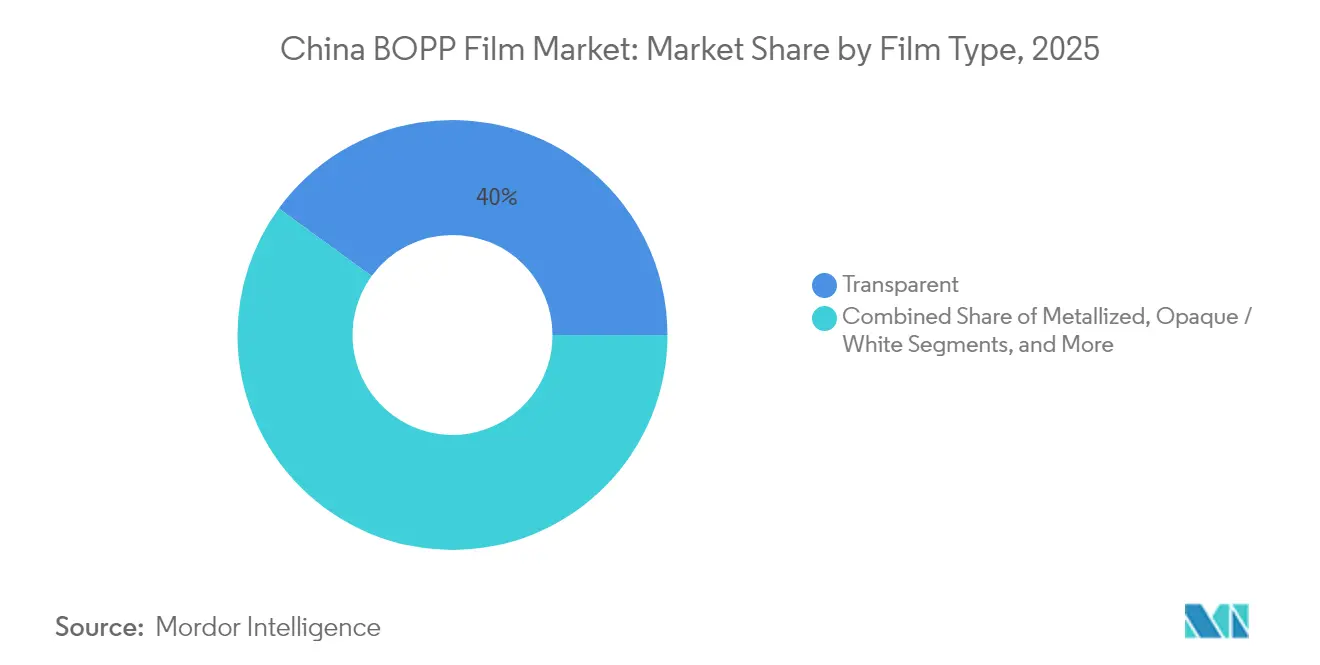

- By film type, transparent grades captured 39.98% of China BOPP film market share in 2025, whereas metallized films are poised to expand at a 6.23% CAGR through 2031.

- By thickness, the 15-30 micron range held 36.22% of the China BOPP film market size in 2025, yet films above 45 microns will advance fastest at a 5.94% CAGR.

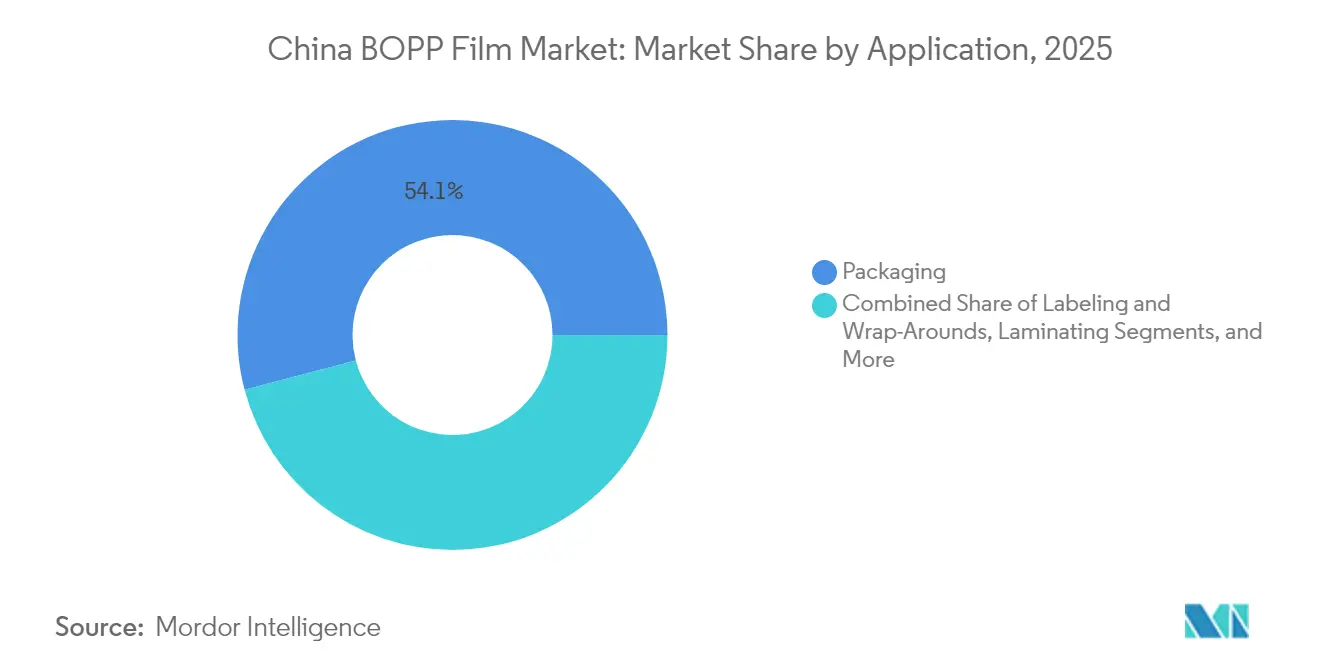

- By application, packaging accounted for 54.10% of 2025 demand and is set to grow at a robust 6.85% CAGR to 2031.

- By end-user vertical, food held 28.37% market share in 2025, while pharmaceutical and medical packaging will outpace all others at a 7.21% CAGR.

- By geography, Jiangsu, Zhejiang and Guangdong collectively housed more than half of national capacity in 2025 and continue to register the highest provincial utilization rates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China BOPP Film Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging e-commerce packaging demand | +1.2% | National; tier-1 cities lead | Short term (≤ 2 years) |

| Government push for high-barrier food safety standards | +0.8% | National; stricter in major cities | Medium term (2–4 years) |

| Shift from PVC to BOPP labels in beverages | +0.6% | National; multinational brands lead | Medium term (2–4 years) |

| Rising demand for low-gauge cost-saving films | +0.7% | National; cost-sensitive sites | Short term (≤ 2 years) |

| Expansion of BOPP-based lithium-battery separator films | +0.4% | Battery manufacturing hubs | Long term (≥ 4 years) |

| Investments in high-speed domestic tenter lines | +0.3% | Major manufacturing provinces | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Surging E-commerce Packaging Demand

Rapid growth of online retail continues to lift shipment volumes for courier bags, mailers and single-serve product packs that favor thin, printable BOPP substrates. Converters serving grocery delivery and pharmaceutical fulfillment increasingly request co-extruded films engineered for low-temperature seal initiation to protect temperature-sensitive goods. Producers reply with 12–15 micron transparent grades that retain puncture resistance while shaving resin use, thereby protecting margins even as freight costs stay elevated. Ink-receptive surface chemistries and improved anti-static packages shorten press setup time, a decisive edge for short-run personalization programs popular on livestream platforms.

Government Push for High-Barrier Food Safety Standards

Implementation of GB 4806.15-2024 for food-contact adhesives compels lamination houses to tighten migration controls and to document every batch of inks, primers and tie-layers. [1]Food Packaging Forum Team, “China developing or updating many food safety standards in 2024,” foodpackagingforum.org Large-scale China BOPP film market producers have responded by installing multi-layer on-line thickness gauges and investing in ISO 17025-accredited labs so they can issue certificates of analysis within 24 hours. The new rules favor high-barrier metallized and coated grades that extend shelf life under stricter distribution temperatures, especially for ready-to-eat meals and dairy snacks sold via convenience stores.

Shift from PVC to BOPP Labels in Beverages

Brand owners targeting bottle-to-bottle PET recycling are moving away from PVC label stock toward polyolefin mono-material solutions that float and separate cleanly. Chinese label printers now specify pearlized or cavitated BOPP for heat-shrink sleeves that must survive 50 cycles of caustic wash yet detach without adhesive residue. The transition forces resin formulators to fine-tune shrinkage curves and dyne levels, spurring collaboration across the value chain and accelerating qualification cycles with global soft-drink giants.

Rising Demand for Low-Gauge Cost-Saving Films

Intensified price competition in snacks and dry goods packaging places a premium on gauges below 15 microns. Domestic tenter lines equipped with automated decurlers and multi-segment pin ovens now hold ±1% thickness tolerance across 8.7-meter webs, unlocking efficient slit-edge yields. Cost-down initiatives also drive solvent-free lamination and digital varnish replacement to avoid over-lamination in certain promo packs, further promoting material savings.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in polypropylene feedstock prices | −0.9% | National | Short term (≤ 2 years) |

| Stringent single-use plastic waste regulations | −0.6% | National; regional variance | Medium term (2–4 years) |

| Capacity overbuild causing price compression | −0.5% | Major production regions | Short term (≤ 2 years) |

| Emerging bio-based film alternatives | −0.3% | Premium application pockets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Polypropylene Feedstock Prices

Spot PP resin hovered in a USD 740–755 per-ton band during early 2025, but order lead times shortened to one week as traders hesitated to build stocks amid uncertain macro conditions. Larger China BOPP film market producers now hedge up to 50% of their forward resin requirements under term contracts indexed to China-created benchmarks, while midsize players rely on syndicated purchasing pools to buffer weekly swings. Nonetheless, abrupt spikes can still compress film margins by 300–400 basis points in a single quarter.

Stringent Single-Use Plastic Waste Regulations

China’s phased bans on non-recyclable single-use plastics force retailers to prove yearly reduction targets and to submit recycling audits to municipal bureaus. [2]Detpak, “China commits to phasing out single-use plastic items,” detpak.com BOPP is comparatively advantaged because it is a mono-material polyolefin, yet multi-layer pouches combining PET/PE or paper/PE remain under scrutiny. Converters accelerate trials of washable inks and easy-peel sealants designed for mechanical sorting, while producers of specialty metallized grades launch proprietary demetallization processes to ensure full circularity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Film Type: Metallized Films Drive Innovation

Metallized structures accounted for a modest slice of China BOPP film market size in 2025, yet their 6.23% CAGR signals accelerating traction in moisture-sensitive snacks, powdered beverages and over-the-counter medicines. Transparent films still held 39.98% China BOPP film market share in 2025, largely due to their versatility in horizontal form-fill-seal operations. Demand for metallized film rises where ≤0.5 g/m² oxygen transmission rate is non-negotiable, pushing suppliers to retrofit vacuum metallizers with plasma pretreatment for tighter adhesion. Brand owners also embrace clear barrier coatings as an alternative route to see-through, recyclable windows that maintain aluminum-equivalent barrier. The result is a premiumization path where converters secure higher per-kilogram profits while brand owners improve shelf appeal.

Second-generation coated metallized grades now combine half-mirror aesthetics with de-inkable surfaces, unlocking mainstream recyclability under APR guidelines. Pilot projects with beverage closures demonstrate that aluminum deposition as low as 300 angstroms still meets carbonation retention targets, proving viable across high-speed bottling. Multinational snack players structure two-year supply agreements to lock in capacity and reduce exposure to coated PET, signaling confidence that metallized BOPP will continue displacing incumbent substrates in rigid-to-flexible conversions.

By Thickness: Ultra-Thin Applications Accelerate

The dominant 15–30 micron band retained 36.22% China BOPP film market share in 2025, yet gauges above 45 microns will grow fastest at 5.94% over 2026-2031 on the back of stand-up pouch zippers, retort lids and industrial over-wraps. Producers strategically balance line mixes to capture both ends, dedicating older legacy widths to thin-gauge runs and saving new 10.4-meter assets for high-value thick products where output-per-millimeter is lower but price-per-ton higher. Inline IR cameras integrated with AI-driven feedback loops now deliver ±0.3 micron profiles, an essential requirement for converter uptime.

Demand for sub-12 micron transparent film grows in sachets and micro-pouches, but process windows tighten sharply; thus, only operators with high-precision chill-roll systems and positron thickness modeling can meet defect targets. Conversely, 60-micron oriented insulation tapes for motor windings draw interest from EV manufacturers because of dielectric strength and abrasion resistance. Together these trends illustrate how the China BOPP film market keeps diversifying thickness spectrums to fulfill disparate performance codes rather than converging on a single optimized gauge.

By Application: Packaging Dominance Intensifies

Packaging represented 54.10% of overall consumption in 2025 and will rise at 6.85% CAGR as China’s grocery retail continues its omnichannel pivot. High-barrier metallized snack wrap leads volume growth, while transparent over-wrap remains the workhorse in noodles, biscuits and condiment pouches. Meanwhile, label and wrap-around applications gain incremental share as beverage OEMs abandon PVC for floatable polyolefin skins—a shift that reinforces circular-economy compliance. Lamination houses diversify into retortable flexibles by deploying high-temperature adhesives compatible with BOPP/PET or BOPP/CPP stacks.

Pressure-sensitive tapes, though mature, sustain steady grade replacement: UV-cured acrylic adhesives call for tailored anchor coatings on BOPP backers, opening niche orders for surface-modified films. Online retailers also accelerate adoption of matte-finish bubble mailers utilizing opaque cavitated BOPP facestock to improve scuff resistance during last-mile delivery. Consequently, producers now juggle run schedules across multiple slit widths to keep pace with fragmenting SKU mixes in packaging.

By End-User Vertical: Pharmaceutical Surge Leads Growth

Food preserved its 28.37% share of the China BOPP film market size in 2025, fueled by continuous snacking demand and convenience meals. Yet pharmaceutical and medical packaging is positioned to expand at a market-leading 7.21% CAGR thanks to rising OTC volumes and post-pandemic cold-chain investments. Child-resistant and tamper-evident pouch formats increasingly specify 25-micron white opaque BOPP for back-panel printability coupled with superior delta-E stability under gamma sterilization. Beverage labels meanwhile remain a sizable demand node as polyolefin sleeves improve bottle recycling yield under Chinese PET roadmap targets.

Personal-care brands call for high-gloss pearlescent grades featuring controlled opalescence that masks fill lines without extra opaque masterbatch. Industrial tape and electronics reinforce moderate baseline loads but register sporadic spikes during construction booms or electronics refresh cycles. Across each vertical, compliance with national food-contact standards remains the universal gatekeeper, reinforcing the importance of robust migration-safe formulations tested under GB/31604 simulants.

Geography Analysis

Driven by proximity to polymer feedstock and port logistics, Jiangsu, Zhejiang and Guangdong collectively accounted for more than half of the China BOPP film market size in 2025. Jiangsu leads in specialty high-barrier output, leveraging integrated petrochemical complexes in Lianyungang and Suzhou that shorten resin supply chains and reduce in-plant inventory. Zhejiang anchors the largest concentration of privately owned tenter lines, many clustered in Jiaxing and Shaoxing, allowing shared solvent-recovery systems and skilled labor exchanges that heighten operational flexibility. Guangdong remains export-oriented; its producers routinely ship jumbo rolls through Shenzhen and Gaolan ports, serving converters across Southeast Asia and Latin America.

Inland expansion is accelerating under Western Development and Cheng-Yu Twin-City economic plans that subsidize advanced material projects. Chongqing and Sichuan now court BOPP producers with electricity tariffs 15% lower than coastal averages, offsetting freight penalties on finished rolls bound for eastern converters. Meanwhile, Hebei and Shandong focus on low-gauge commodity film, targeting regional food hubs in Henan and Anhui where logistics distances remain manageable. National rail upgrades facilitate back-haul opportunities, improving transport economics for bulky but lightweight film stock.

Regulatory enforcement intensity still varies by province. Coastal municipalities have adopted stricter post-consumer film-waste reporting, compelling local producers to pilot take-back schemes, whereas inland counties emphasize capacity utilization and job creation. Nevertheless, central government guidelines that benchmark recycling rates are closing the compliance gap, setting a common playing field for all players by 2027. Overall, regional specialization continues to sharpen comparative advantages while inter-provincial freight optimization buffers cost disparities, ensuring that the China BOPP film market maintains balanced growth across the nation.

Competitive Landscape

The China BOPP film market is fragmented. Scale remains meaningful, yet differentiation pivots more on technical agility and regulatory compliance. Leading state-backed enterprises operate multi-line complexes exceeding 200 kilotons per year, underpinned by fully integrated resin-to-film flows that shield against feedstock volatility. Privately owned innovators, in contrast, carve out niches in metallization, aqueous coating, and matte-frost finishes that command margin premiums.

Strategic differentiation increasingly emphasizes sustainability credentials. Several producers now market low-carbon “green-power” grades verified by third-party renewable-energy certificates, leveraging provincial incentives for rooftop solar adoption. Others tout closed-loop recycling pilots that reclaim trim waste and faulty rolls for depolymerization back into polypropylene feedstock. Early adopters of simultaneous-stretch technology, introduced through a landmark European acquisition in 2025, advertise superior biax uniformity and downgauging potential, appealing to converters aiming for line speed above 600 packs per minute. [3] Packaging Europe Editorial Team, “Toppan to acquire BOPP film manufacturer Irplast,” packagingeurope.com

M&A momentum remains lively. Cross-border deals focus on augmenting product portfolios and market access rather than pure tonnage. Domestic consolidation intensifies wherever cash-flow stress from capacity overbuild erodes working capital. Technology partnerships with downstream FMCG and pharmaceutical customers deepen, manifesting in joint innovation centers that co-develop barrier enhancements, printable recyclability markers and AI-enabled defect inspections. Collectively, these dynamics underscore a marketplace where operational excellence and customer intimacy often outweigh headline capacity when securing long-term contracts.

China BOPP Film Industry Leaders

-

Zhejiang Kinlead Innovative Materials Co., Ltd.

-

Gettel Group Co., Ltd.

-

Anhui Guofeng Plastic Industry Co., Ltd.

-

Guangdong Decro Film New Materials Co., Ltd.

-

Jiangsu Shuangxing Color Plastic New Materials Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Amcor pledged additional AI-related R&D investment at its Jiangyin hub, lifting cumulative China commitments to USD 2 billion since 2015.

- March 2025: Sichuan Zhuoqin New Materials Technology completed Phase I of its lithium-battery separator complex in Qionglai, investing CNY 60.8 billion (USD 8.4 billion) in what is slated to be the world’s largest single-site polyolefin separator facility.

- March 2025: Toppan Holdings acquired 80% of Italian BOPP specialist Irplast, importing simultaneous-biax technology with superior recyclability credentials.

- February 2025: GB 4806.15-2024 governing food-contact adhesives formally entered into force, demanding stricter migration testing for laminated BOPP webs.

China BOPP Film Market Report Scope

BOPP films (Biaxially Oriented Poly Propylene Films) are flexible plastic types produced by stretching polypropylene film in both transverse direction and machine direction. BOPP film applications range from its use in packaging, labeling, and lamination. BOPP Films are the preferred substrate for food packaging owing to their inherent moisture barrier properties, high clarity, seal ability, graphic reproduction, and shelf appeal, the possibility of the pack being a monolayer/homogeneous structure. For food packaging, it is prominently used as a co-extruded heat-sealable reverse printable film. In labeling, it is preferred owing to its yield benefit (lowest density of 0.55 for IML orange peel effect), recyclability with PP containers, etc.

BOPP Films has a strong demand globally which is driven by expanding flexible packaging industry. The market study scope is limited to packaging applications and tracks the demand through the revenue derived from the consumption and sales of BOPP film in the domestic market. The study also tracks the effects of regulations and market drivers on growth and factors restraining market growth. The market is segmented by end-user verticals (food, beverage, pharmaceutical and medical, industrial, and other end-user verticals). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Film Type

| Transparent |

| Metallized |

| Opaque / White |

| Pearlescent |

| Other Film Type |

By Thickness

| < 15 µm |

| 15 – 30 µm |

| 30 – 45 µm |

| > 45 µm |

By Application

| Packaging |

| Labeling and Wrap-Arounds |

| Laminating |

| Pressure-Sensitive Tapes |

| Other Application |

By End-user Vertical

| Food |

| Beverage |

| Pharmaceutical and Medical |

| Personal Care and Cosmetics |

| Industrial |

| Other End-user Vertical |

| By Film Type | Transparent |

| Metallized | |

| Opaque / White | |

| Pearlescent | |

| Other Film Type | |

| By Thickness | < 15 µm |

| 15 – 30 µm | |

| 30 – 45 µm | |

| > 45 µm | |

| By Application | Packaging |

| Labeling and Wrap-Arounds | |

| Laminating | |

| Pressure-Sensitive Tapes | |

| Other Application | |

| By End-user Vertical | Food |

| Beverage | |

| Pharmaceutical and Medical | |

| Personal Care and Cosmetics | |

| Industrial | |

| Other End-user Vertical |

Key Questions Answered in the Report

How large is the China BOPP film market in 2026?

The China BOPP film market size is USD 2.12 billion in 2026 and is projected to reach USD 2.7 billion by 2031.

What is the expected growth rate of China BOPP films through 2031?

The market is forecast to expand at a 4.96% CAGR from 2026 to 2031.

Which film type is growing fastest in China?

Metallized BOPP film is the fastest-growing type, with a 6.23% CAGR expected through 2031.

Which end-user vertical offers the highest growth potential?

Pharmaceutical and medical packaging shows the highest CAGR at 7.21% thanks to stricter safety demands and healthcare expansion.

How are regulations influencing China’s BOPP sector?

New GB 4806.15-2024 standards elevate food-contact compliance, while recycling mandates push development of mono-material and recycled-content films.

Where is most BOPP capacity located in China?

Jiangsu, Zhejiang and Guangdong hold more than half of national capacity, benefiting from established petrochemical infrastructure and port access.

Page last updated on: