Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

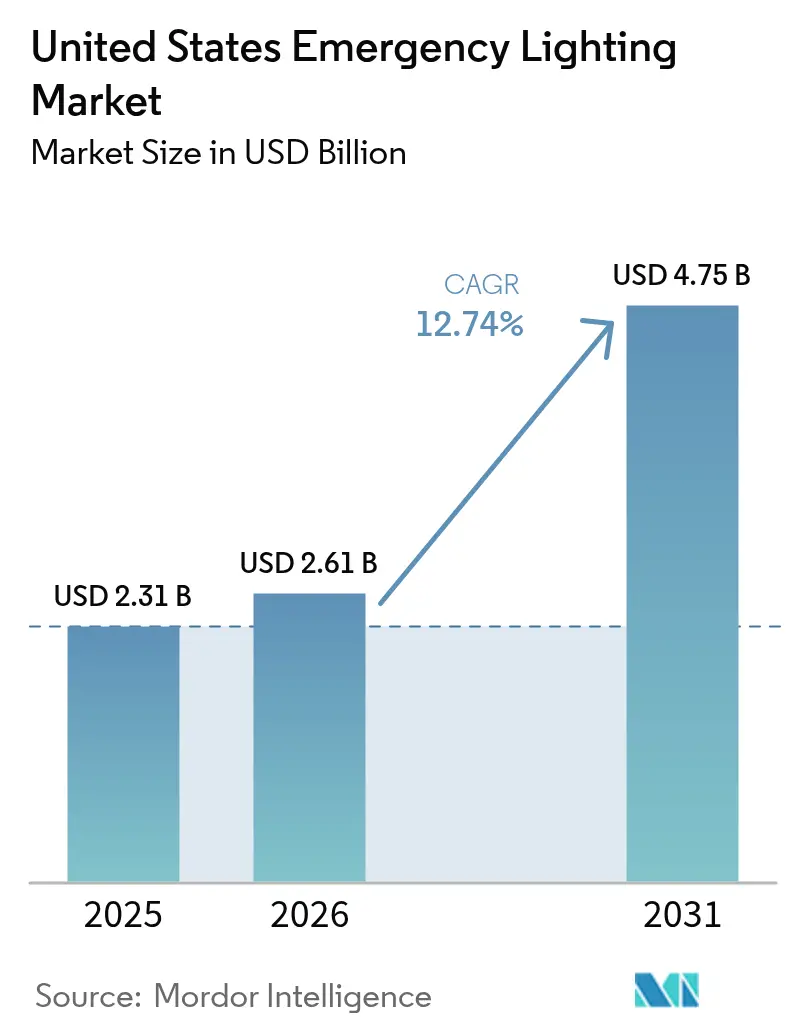

| Base Year Market Size (2025) | USD 2.31 Billion |

| Market Size (2026) | USD 2.61 Billion |

| Market Size (2031) | USD 4.75 Billion |

| Growth Rate (2026 - 2031) | 12.74% CAGR |

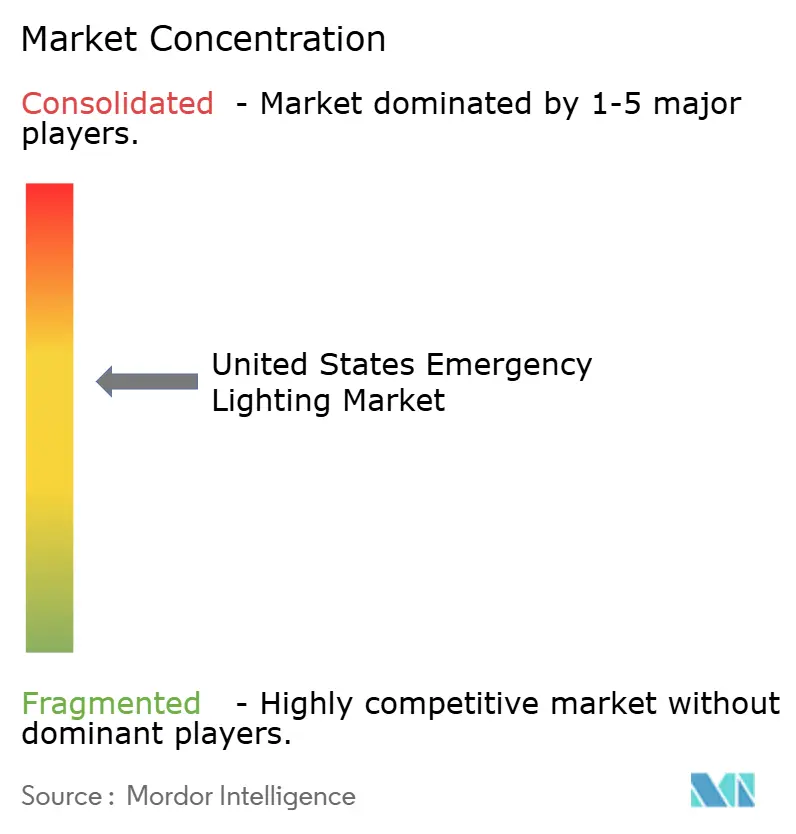

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Emergency Lighting Market Analysis by Mordor Intelligence

The United States emergency lighting market size was valued at USD 2.31 billion in 2025 and estimated to grow from USD 2.61 billion in 2026 to reach USD 4.75 billion by 2031, at a CAGR of 12.74% during the forecast period (2026-2031). Sustained growth is anchored in the Infrastructure Investment and Jobs Act (IIJA), ongoing LED price declines, the revised UL 924 standard, and stricter NFPA 70/101 enforcement that collectively accelerate retrofit activity across commercial, healthcare, and transit facilities. Federal funds obligated under IIJA reached USD 279 billion by April 2025, generating a steady bid flow for code-compliant lighting packages. LED fixtures now exceed 180 lm/W while lithium-iron-phosphate (LiFePO4) batteries lengthen service life, reducing total cost of ownership and reinforcing the rapid shift away from fluorescent systems. In parallel, IoT-ready platforms such as nLight AIR simplify compliance testing through wireless self-diagnostics, shrinking labor hours and wiring needs. Moderate market concentration allows incumbents to deepen share through acquisitions and smart-building offerings that embed emergency luminaires into broader energy-management ecosystems.

Key Report Takeaways

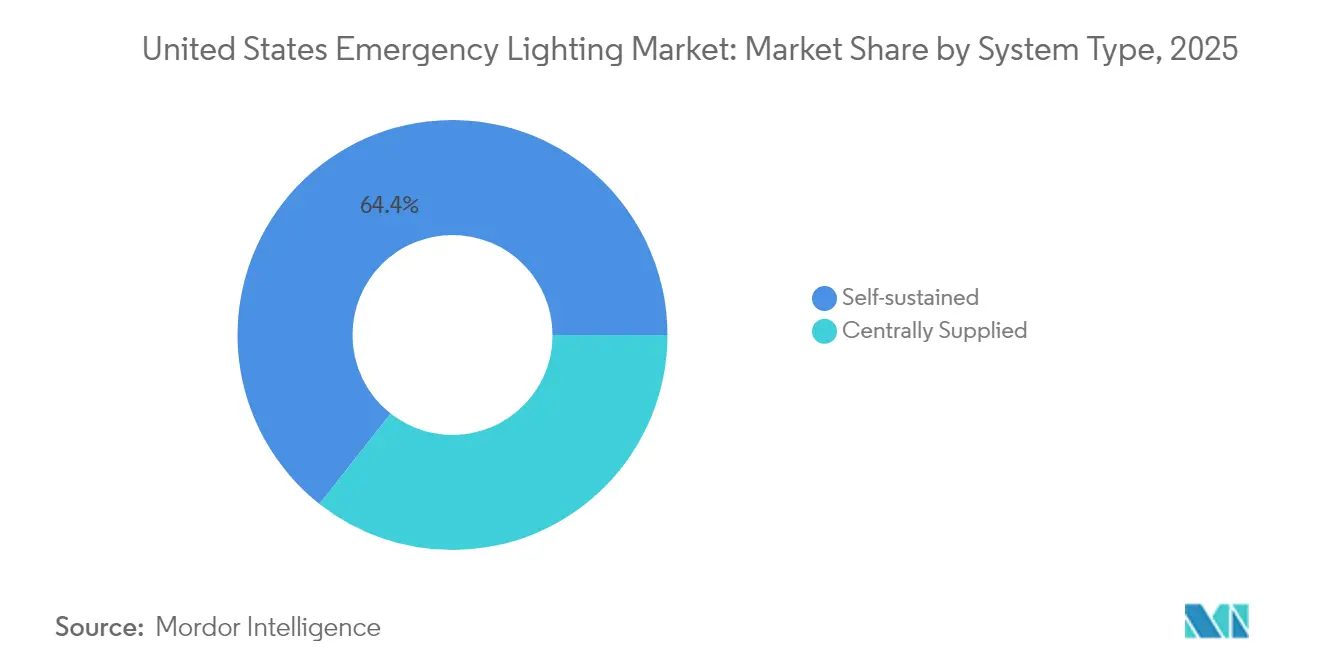

- By system type, self-sustained products held 64.38% of the United States emergency lighting market share in 2025 and will expand fastest at 13.92% CAGR through 2031.

- By light source, LEDs led with 78.02% revenue share in 2025, while the same segment is projected to post a 14.06% CAGR to 2031.

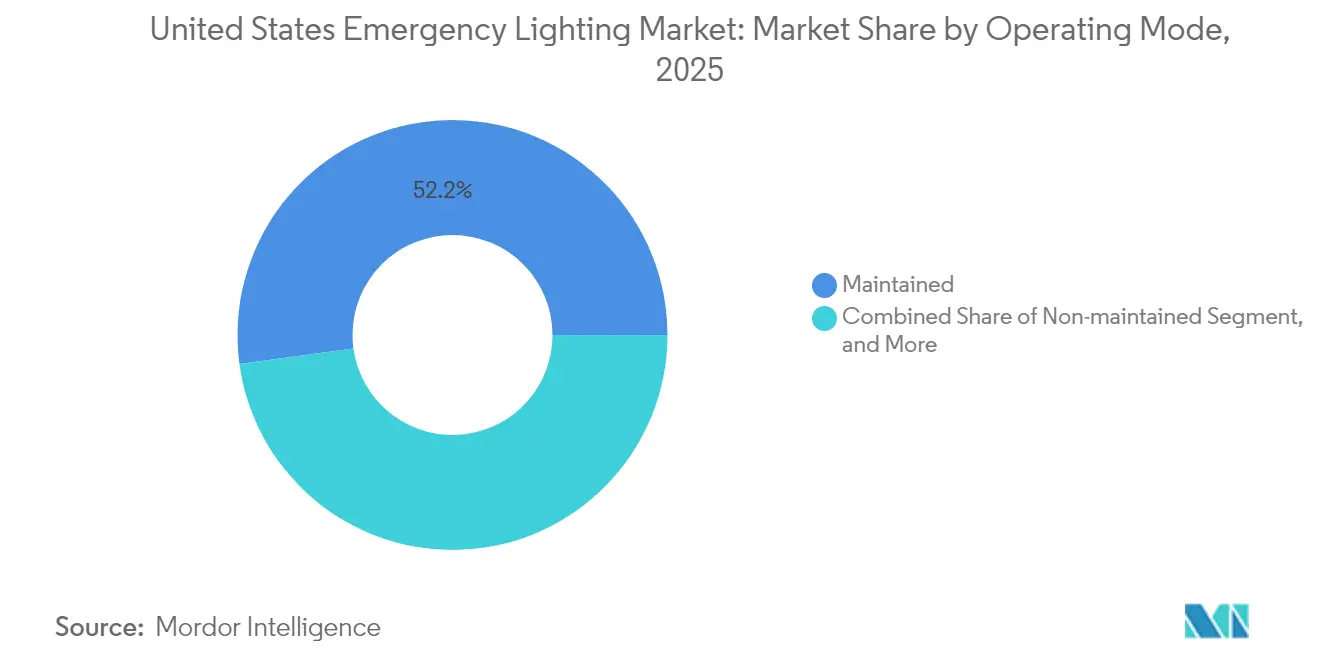

- By operating mode, maintained fixtures commanded a 52.15% share of the United States emergency lighting market size in 2025, whereas switched/multi-mode units are poised for a 15.33% CAGR over the forecast period.

- By end user, commercial facilities contributed 40.70% revenue in 2025; public infrastructure and transit venues represent the fastest-growing user group at 14.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Emergency Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing LED efficacy and price declines | +2.80% | Nationwide, strongest in commercial & healthcare | Short term (≤ 2 years) |

| Stringent NFPA 70/101 and OSHA compliance push | +3.20% | National high-occupancy buildings | Medium term (2-4 years) |

| Rise in smart-building retrofits (IoT integration) | +2.10% | Urban Northeast & West Coast | Medium term (2-4 years) |

| Federal infrastructure-upgrade funding (IIJA) | +2.90% | All states, focus on transportation hubs | Long term (≥ 4 years) |

| Climate-resilience mandates for severe-weather events | +1.70% | Coastal & tornado-prone regions | Long term (≥ 4 years) |

| Corporate ESG decarbonization targets | +1.40% | Fortune 500 campuses | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing LED Efficacy and Price Declines Drive Market Transformation

New-generation LED emergency luminaires now surpass 180 lm/W, allowing facility owners to cut energy use by up to 82% after retrofits. McLaren Health Care replaced 25,000 units across 11 hospitals and lowered annual utility costs by USD 1.6 million, confirming favorable payback periods despite code-driven battery upgrades.[1]Orion Lighting, “LED Lighting Case Studies – Colby Metal,” orionlighting.com Falling diode costs compress fixture pricing, pushing the United States emergency lighting market deeper into price-parity territory with fluorescent incumbents. High efficacy shortens battery sizing requirements, further trimming upfront spend. As a result, LED penetration is expected to exceed 90% of new installations before 2027. The technology leadership strengthens supplier bargaining power while widening adoption in budget-sensitive education and municipal projects.

Stringent NFPA 70/101 and OSHA Compliance Push Reshapes Installation Standards

The latest NFPA 101 edition mandates 1 fc minimum egress illuminance and 90-minute backup duration, driving facility managers to replace non-conforming fixtures during remodels. UL 924 (May 2022) now requires luminaires to sense normal power presence; wireless mesh offerings like nLight AIR satisfy this rule without extra control wiring.[2]nLight Acuity Brands, “UL 924 Emergency Solutions,” nlight.acuitybrands.com School districts leveraging performance-contract models, such as West Mifflin, anticipate USD 9.9 million in savings across 15 years by exceeding code baselines. Consistent monthly self-tests and annual discharge reports generated by smart drivers remove manual log-keeping, easing OSHA audits. Enhanced enforcement boosts replacement cycles and cements compliance features as table-stakes in bid specifications throughout the United States emergency lighting market.

Rise in Smart-Building Retrofits Accelerates IoT Integration

Airports, hospitals, and Class-A offices increasingly demand centrally monitored emergency networks. O’Hare’s rental-car center linked 7,000 LED fixtures to a campus-wide dashboard for predictive maintenance and daylight harvesting benefits. Bluetooth-mesh nodes permit remote firmware updates, cutting truck rolls and shrink burn-hour variance that formerly voided battery warranties. Facility executives treat luminaires as data endpoints that feed carbon-intensity dashboards for ESG reporting. The convergence of safety and analytics widens addressable value for vendors who bundle lighting, controls and software, reinforcing growth momentum within the United States emergency lighting market.

Federal Infrastructure-Upgrade Funding Creates Unprecedented Market Opportunities

IIJA’s USD 432.1 billion budget authority earmarks billions for rail, airport, and streetlighting projects, sustaining long-run backlog for specification-grade luminaires.[3]U.S. Department of Transportation, “Infrastructure Investment and Jobs Act Funding Status,” transportation.gov Ameresco’s USD 47 million Memphis retrofit converted 77,000 roadway fixtures, realizing 37 million kWh annual savings and validating mass-scale economics. Runway upgrades at Daytona Beach International Airport completed in May 2025 underscore accelerated adoption timelines for mission-critical aviation assets. Buy-America rules spur localized assembly investments, fostering supply-chain resilience and supporting the United States's emergency lighting market’s domestic value-addition objectives.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of code-compliant systems | −1.8% | Small commercial & K-12 facilities | Short term (≤ 2 years) |

| Competition from distributed micro-UPS & PoE lighting | −1.2% | Fiber-rich urban cores | Medium term (2-4 years) |

| Lithium-battery supply volatility | −1.5% | Nationwide | Short term (≤ 2 years) |

| Skills gap in low-voltage installation | −0.9% | Rural counties | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Code-Compliant Systems Constrains Adoption

Advanced self-test drivers, LiFePO4 packs, and wireless radios elevate the bill-of-materials up to 40% versus legacy fluorescent units, stretching payback horizons for cash-constrained owners. Smaller retailers and community colleges often postpone upgrades despite energy rebates, slowing total addressable volume in segments that collectively account for more than one-third of building stock. Nonetheless, as LED component costs retreat and utilities expand prescriptive incentives, cost barriers are forecast to soften, permitting latent demand to migrate into the active United States emergency lighting market.

Lithium-Battery Supply Volatility Threatens Cost Predictability

Lithium carbonate averaged USD 9,271 per metric ton in early 2025; any renewed price spike could inflate fixture costs because batteries contribute up to 25% of unit pricing. Geopolitical risk in raw-material processing and a still nascent U.S. cell-manufacturing base raise lead-time uncertainty, forcing contractors to stock higher safety inventory and eroding margin on fixed-price bids. OEMs that dual-source cells or open regional pack-assembly lines will insulate project timelines and preserve share in the United States emergency lighting industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Self-Sustained Designs Extend Leadership

Self-sustained units dominated with a 64.38% United States emergency lighting market share in 2025 and are projected to expand at a 13.92% CAGR to 2031, underscoring their ease of installation and resilience against single-point failures. Dispersed batteries embedded inside every luminaire simplify decentralized retrofits in offices, hospitals, and rail stations, eliminating the need for dedicated battery rooms. Centrally supplied systems retain a foothold in mega-campus healthcare projects where unified monitoring eases quarterly testing, but their cost-intensive wiring constrains new adoption.

The distributed-intelligence trend aligns with the broader digitization of commercial real estate, positioning self-contained fixtures as a backbone for building-wide sensor networks. Edge analytics within each light enable localized diagnostics, compressing mean-time-to-repair and enhancing compliance reporting that is critical for maintaining NFPA and OSHA certifications across the United States emergency lighting market.

By Light Source: LEDs Cement Market Supremacy

LEDs accounted for 78.02% of 2025 shipments and will remain the fastest-growing light source at 14.06% CAGR, reflecting superior efficacy, instant-on capability, and 50,000-hour lifetimes. The United States emergency lighting market size associated with LED luminaires is set to outpace fluorescent replacements by a factor of four during the forecast horizon as procurement managers chase double-digit energy savings and lower maintenance budgets. Industrial clients cite maintenance callouts falling by 60% after switching from T8-based battery packs to purpose-built LED exits.

Declines in component pricing are shrinking the LED premium, enabling quick paybacks even in price-sensitive municipal projects. Fluorescent and halogen options persist mainly in niche applications, but their combined unit share will likely dip below 5% before 2028, confirming LEDs as the de-facto standard throughout the United States emergency lighting market.

By Operating Mode: Maintained Fixtures Hold Majority while Multi-Mode Surges

Maintained fixtures represented 52.15% of the United States emergency lighting market size in 2025, owing to dual-use functionality that doubles as corridor illumination under normal power. Facility managers value the elimination of redundant fixtures, which frees ceiling real estate for sensors and improves aesthetics in LEED-certified buildings.

Switched or multi-mode units, however, are on track to register a 15.33% CAGR, spurred by smart-building retrofits that leverage occupancy data to dim during low-traffic windows while preserving emergency readiness. Integration with lighting-control software supports sophisticated scheduling and energy dashboards, resonating with ESG-driven corporate buyers. Non-maintained units continue to serve low-use egress areas but face muted growth as owners gravitate toward fixtures offering day-to-day utility inside the dynamic United States emergency lighting market.

By End User: Commercial Sector Leads; Transit Hubs Accelerate

Commercial real estate contributed 40.70% of 2025 revenue, reflecting steady tenant-improvement cycles and post-pandemic workplace refreshes. Retrofits increasingly bundle emergency lighting with HVAC and security upgrades to secure holistic ESG certifications and to meet WELL Building standards.

Transit and public infrastructure venues will exhibit the highest 14.98% CAGR as IIJA funds accelerate airport and subway modernization. Daytona Beach International Airport completed a 21-day LED runway upgrade in May 2025, validating rapid installation schedules that can be replicated at peer facilities nationwide. Healthcare chains and universities continue sizable retrofit programs driven by maintenance savings and resilience targets, maintaining a robust project funnel across the United States emergency lighting market.

Geography Analysis

California, Texas, New York, Florida, and Illinois collectively attract the bulk of IIJA grants, propelling concentrated demand in coastal and freight-corridor states. California alone approved USD 830 million for transportation in December 2024, a share that includes emergency egress lighting for bridges and interchanges. These allocations ensure steady order intake for OEMs with Buy-America-compliant SKUs, bolstering the United States emergency lighting market in high-population regions.

The Midwest benefits from logistics-park construction and tornado-resilient building codes that elevate battery-duration specifications above national minima. Illinois Department of Transportation’s USD 0.52 million 2025 highway-lighting contract exemplifies the wave of LED-centric maintenance programs beyond coastal metros. Rural districts struggle with limited certified electricians, but federal technical-assistance grants are beginning to offset the skills gap, gradually unlocking latent demand across the broader United States emergency lighting market.

Urban centers in the Northeast and Pacific Northwest lead smart-building pilots, deploying Bluetooth-mesh emergency networks that dovetail with carbon-intensity disclosure laws. Proxy ordinances in New York City and Seattle set the stage for statewide rollouts, positioning these markets as bellwethers for controls-heavy specifications that will diffuse nationally by the end of the decade.

Competitive Landscape

Acuity Brands, Eaton, and Hubbell together captured a major share in shipment value in 2024, indicating moderate concentration within the United States emergency lighting market. Acuity improved operating profit by 16.9% in fiscal 2024 through portfolio realignment and new software-centric acquisitions. Eaton’s Electrical Americas segment expanded backlog 29% year-over-year, leveraging infrastructure spending to scale UPS-integrated luminaires. Hubbell divested its residential Progress Lighting arm to sharpen focus on specification-grade and hazardous-area fixtures, a segment that requires specialized engineering and carries higher margins.

Strategic playbooks emphasize IoT integration, UL 924 compliance, and localized battery assembly. Acuity’s January 2025 acquisition of Q-SYS (USD 1.1 billion) adds audio-visual control assets that can feed mass-notification layers atop emergency egress lighting, broadening the value proposition for campus customers. Eaton doubles down on lithium battery partnerships to hedge supply volatility, while Hubbell expands wireless commissioning tools to reduce job-site labor in labor-tight regions. Mid-tier challengers court share via differentiated LiFePO4 chemistries promising 2,000-cycle life, but scale economies still favor incumbents, maintaining the United States emergency lighting market’s moderately consolidated structure.

Emerging disruptors bundle Power-over-Ethernet (PoE) drivers with cloud dashboards, pitching unified low-voltage grids that merge data, power, and control. Although the share remains small, these entrants press incumbents to quicken software rollouts, accelerating digital maturity across the United States emergency lighting market.

United States Emergency Lighting Industry Leaders

Acuity Brands Inc.

Eaton Corporation plc

ABB Ltd

Hubbell Incorporated

Signify N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Daytona Beach International Airport finished a 21-day LED runway conversion, reducing maintenance downtime and enhancing pilot visibility. Strategy: showcase rapid-deployment template adaptable to FAA-funded airport upgrades.

- April 2025: USDOT confirmed USD 279 billion of IIJA funds obligated, sustaining capex visibility for fixture makers through mid-decade. Strategy: provide predictable demand environment encouraging capacity expansion.

- February 2025: West Mifflin School District projected USD 9.9 million savings over 15 years via comprehensive emergency-lighting retrofit. Strategy: validate energy-performance contracting in the education vertical.

- January 2025: Acuity Brands acquired Q-SYS for USD 1.1 billion to embed audio, video, and control capabilities into its intelligent-spaces platform, enabling integrated emergency notification and lighting control. Strategy: expand recurring software revenue and cross-sell across enterprise campuses.

United States Emergency Lighting Market Report Scope

Scope for emergency lighting - The revenue includes emergency lamps, luminaries (LED/fluorescence), and lighting accessories, such as power packs, monitoring systems, sensing modules, and lighting test switches. Different products include escape lighting (signage lighting and anti-panic lighting) and stand-by lighting (high-risk task lighting). The study also includes coverage on key end-user domains of emergency lighting and geographies.

By System Type

| Self-sustained |

| Centrally Supplied |

By Light Source

| LED |

| Fluorescent |

| Others (Halogen, Incandescent, etc.) |

By Operating Mode

| Maintained |

| Non-maintained |

| Switched/Multi-mode |

By End User

| Commercial |

| Industrial |

| Educational Facilities |

| Healthcare Facilities |

| Public Infrastructure and Transit |

| Others (Residential, Hospitality, etc.) |

| By System Type | Self-sustained |

| Centrally Supplied | |

| By Light Source | LED |

| Fluorescent | |

| Others (Halogen, Incandescent, etc.) | |

| By Operating Mode | Maintained |

| Non-maintained | |

| Switched/Multi-mode | |

| By End User | Commercial |

| Industrial | |

| Educational Facilities | |

| Healthcare Facilities | |

| Public Infrastructure and Transit | |

| Others (Residential, Hospitality, etc.) |

Key Questions Answered in the Report

What is the current value of the United States emergency lighting market?

The market was valued at USD 2.61 billion in 2026 and is projected to reach USD 4.75 billion by 2031.

Which system type leads U.S. installations?

Self-sustained luminaires commanded 64.38% share in 2025, owing to simplified wiring and distributed battery redundancy.

How will IIJA spending influence demand?

IIJA has already obligated USD 279 billion, funding large transit and airport projects that will sustain double-digit fixture demand through 2031.

Why are LiFePO4 batteries gaining traction?

They deliver longer cycle life and lower maintenance, aligning with NFPA 90-minute backup mandates without frequent replacement.

Which end-user segment is growing fastest?

Public infrastructure and transit facilities will grow at 14.98% CAGR as they modernize lighting for safety and energy savings.

What is driving adoption of smart emergency lighting?

Wireless self-testing, centralized dashboards and compliance automation reduce labor costs and support ESG reporting goals.

Page last updated on: