Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

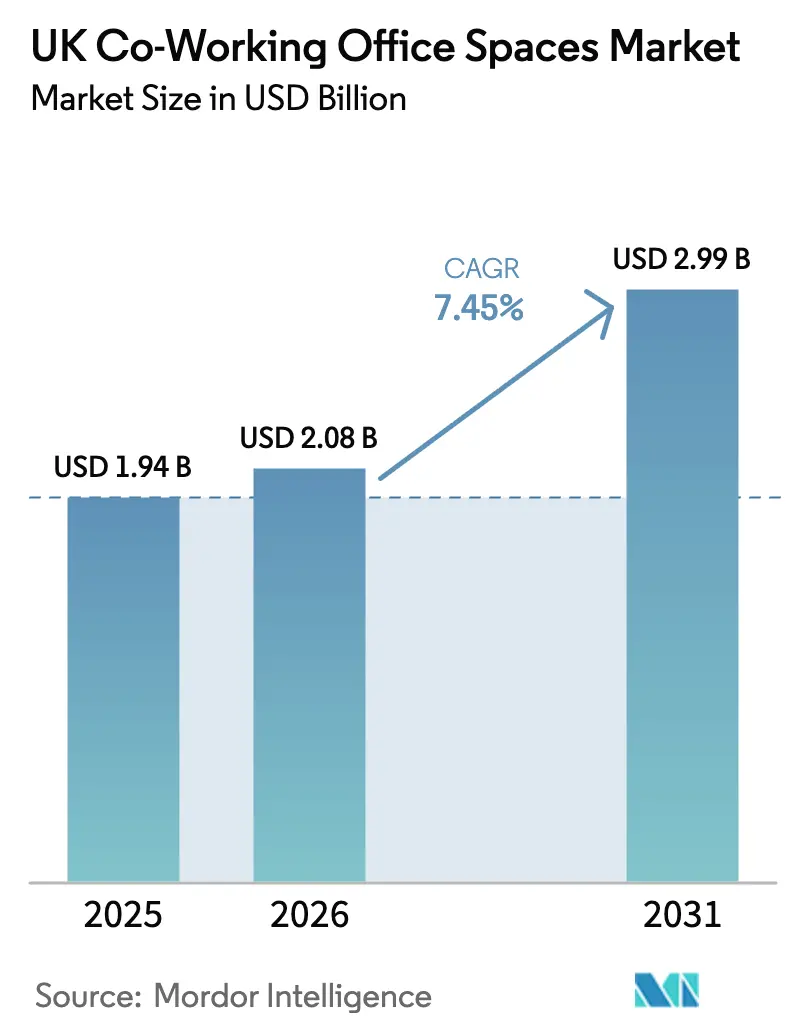

| Base Year Market Size (2025) | USD 1.94 Billion |

| Market Size (2026) | USD 2.08 Billion |

| Market Size (2031) | USD 2.99 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

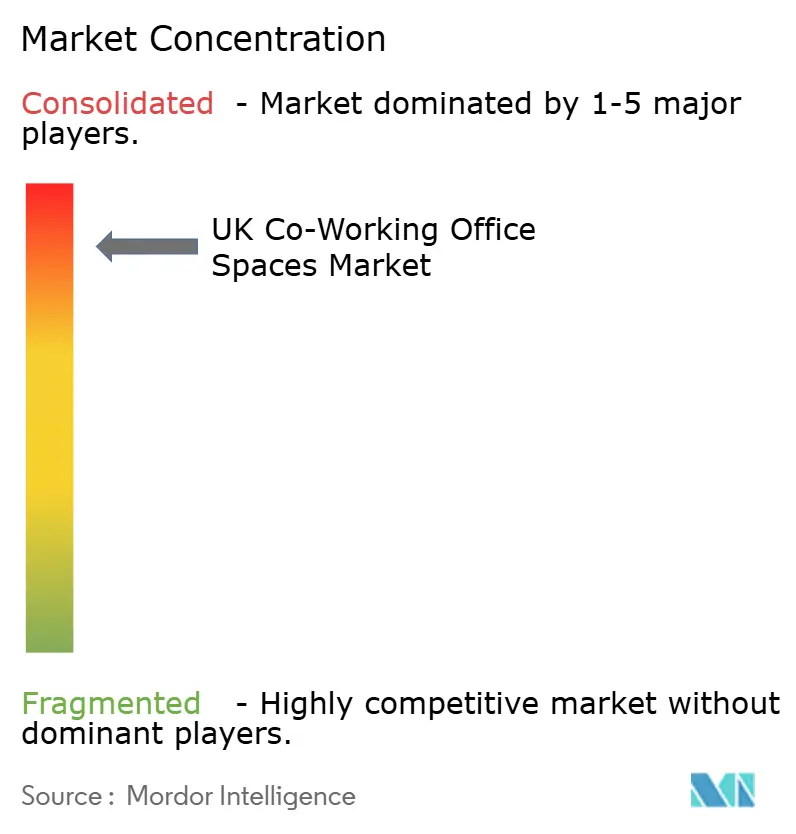

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UK Coworking Office Spaces Market Analysis by Mordor Intelligence

The UK co-working spaces market size was valued at USD 1.94 billion in 2025 and estimated to grow from USD 2.08 billion in 2026 to reach USD 2.99 billion by 2031, at a CAGR of 7.45% during the forecast period (2026-2031)[1]Chartered Institute of Personnel and Development, “Flexible and Hybrid Working Practices in 2024,” cipd.org. Demand is being propelled by employers formalizing hybrid policies, which has shifted flexible workspace from a cyclical perk to a core component of real-estate strategy. Enterprises are renegotiating headquarters footprints while adding regional satellites, a move that enlarges the addressable pool for the UK co-working spaces market. ESG mandates are simultaneously pushing landlords to retrofit or develop BREEAM- and LEED-certified buildings, encouraging operators to prioritize certified assets where rent premiums reach 15-20%. Capital is abundant: family offices, infrastructure funds, and REITs are allocating dry powder to revenue-share agreements that shield operators from heavy fit-out costs and give landlords upside participation. Meanwhile, regional hubs such as Manchester and Belfast are closing the gap with London, signaling a durable geographic rebalancing that diversifies portfolio risk for providers active in the UK co-working spaces market.

Key Report Takeaways

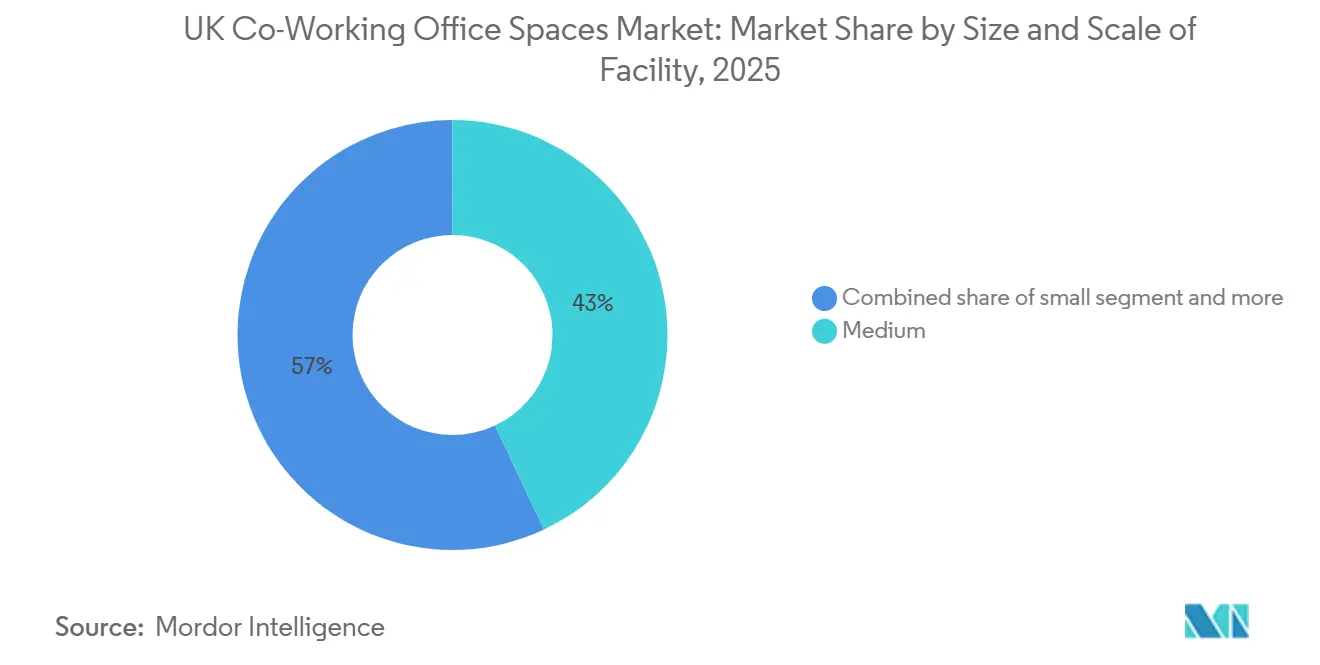

- By size & scale of facility, medium-scale centers commanded 43% of the UK co-working spaces market share in 2025, while large campuses are forecast to accelerate at a 9.11% CAGR through 2031, buoyed by life-sciences and technology tenants.

- By sector, IT & ITES dominated with 36.50% revenue share in 2025; life-sciences is projected to climb at a 10.20% CAGR between 2026-2031 as demand for CL2-ready lab modules intensifies.

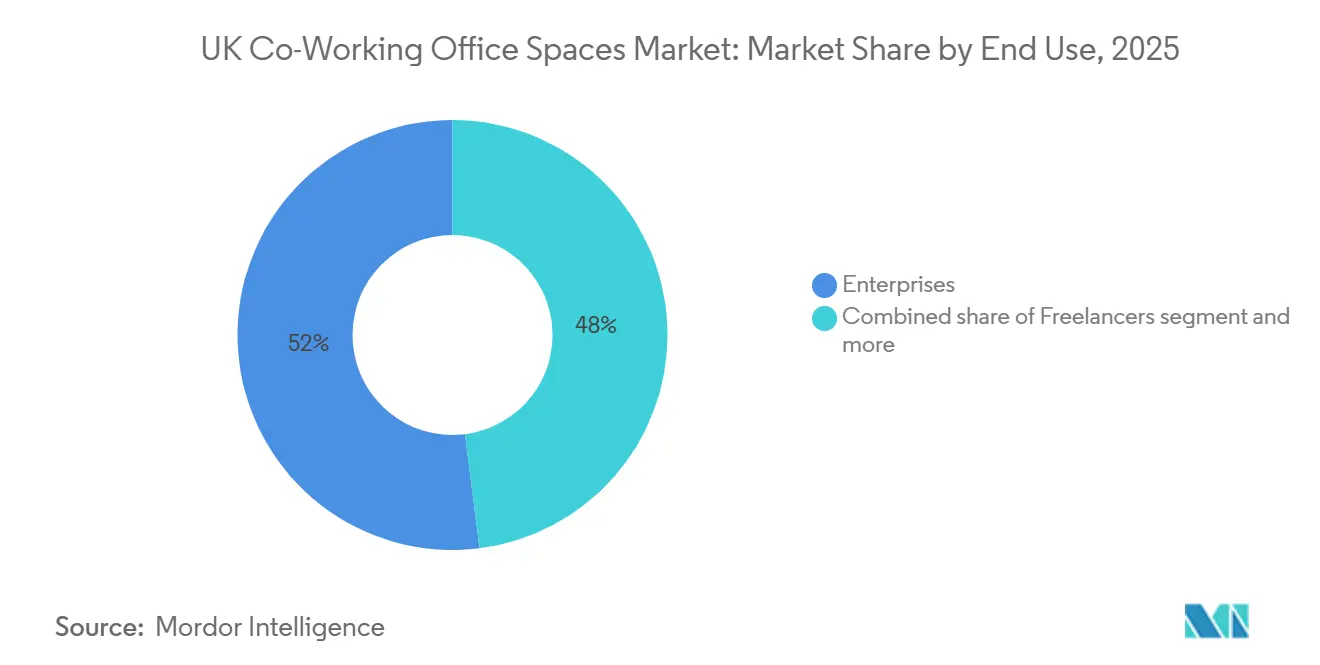

- By end use, enterprises held 52% of the UK co-working spaces market size in 2025, but start-ups and freelancers are poised to expand at an 8.78% CAGR thanks to steadier venture-capital inflows.

- Geographically, England accounted for 86% of the value in 2025, whereas Northern Ireland is the fastest-growing territory with an 8.93% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UK Coworking Office Spaces Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid-work penetration sustaining double-digit flexible-space absorption | +2.1% | England, Scotland | Medium term (2-4 years) |

| Technology, creative & professional-services tenants extending multi-city footprints | +1.8% | England, Scotland | Long term (≥ 4 years) |

| Regional-hub demand spike narrowing London dependence | +1.5% | England, Northern Ireland | Medium term (2-4 years) |

| Shift toward BREEAM/LEED-certified spaces to meet occupiers’ ESG mandates | +0.9% | England, Scotland | Long term (≥ 4 years) |

| Family-office & infrastructure-fund capital earmarked for income-resilient portfolios | +1.3% | England, Scotland | Short term (≤ 2 years) |

| Landlord-operator revenue-share models lowering entry barriers for new sites | +1.2% | England, Wales, Northern Ireland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hybrid-Work Penetration Sustaining Double-Digit Flexible-Space Absorption

Two-thirds of UK employers now require employees in the office at least part of the week, up sharply since 2023, and average office utilization hit 66% in 2025. Companies are therefore shifting from fixed leases toward variable-cost desks that can expand or contract with headcount. Technology giants have mainstreamed occupancy-sensor ecosystems that feed real-time data into scheduling tools, and operators able to plug into this stack are winning enterprise contracts[2]Microsoft, “Introducing Microsoft Places,” microsoft.com. This uptake underpins stable, double-digit absorption across the UK co-working spaces market.

Technology, Creative & Professional-Services Tenants Extending Multi-City Footprints

Government grants for gaming, film, and digital media—totaling USD 480 million since 2024—are driving tenants to Manchester, Birmingham, and Leeds, where new innovation districts bundle studio space with co-working floors[3]UK Department for Culture, Media & Sport, “Creative Industries Sector Vision,” gov.uk. Professional-services firms mirror this pattern, piloting nearshore delivery teams outside London to control salary costs, which enlarges the UK co-working spaces market beyond the capital.

Regional-Hub Demand Spike Narrowing London Dependence

Regional absorption exceeded 450,000 square feet in 2024, with Manchester alone taking 280,598 square feet—up 34.5% year on year. Occupiers are chasing talent pools, affordable rents, and upgraded transport links, pushing operators to deploy capital across England’s core cities and in Belfast, thereby diversifying revenue streams inside the UK co-working spaces market.

Shift Toward BREEAM/LEED-Certified Spaces to Meet Occupiers’ ESG Mandates

The looming EPC-B requirement for non-domestic buildings by 2030 is making certification a must-have. New centers like Huckletree’s 8 Bishopsgate achieved BREEAM Excellent with smart HVAC and LED lighting, allowing operators to charge 15-20% rent premiums over non-certified stock. Investors favor portfolios that are alignment-ready, reinforcing ESG as a durable growth lever for the UK co-working spaces market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Localized oversupply in Central-London sub-markets depressing desk rates | -1.4% | England (Central London) | Short term (≤ 2 years) |

| Elevated energy, FM and labor costs squeezing operator EBITDA margins | -1.9% | England, Scotland | Medium term (2-4 years) |

| SME demand volatility amid UK inflation/recession fears | -1.1% | England, Wales, Northern Ireland | Short term (≤ 2 years) |

| Upcoming non-traditional competition eroding pricing power | -0.8% | England, Scotland | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Localized Oversupply in Central-London Sub-Markets Depressing Desk Rates

Inventory in the City and Westminster grew by more than 1 million sq ft between 2022-2024, yet utilization lingers below 70%. Average monthly desk rates reached USD 994 in early 2024, but landlords in fringe zones now offer rent-free periods and fit-out subsidies to fill space, straining margins for incumbent operators.

Elevated Energy, FM and Labor Costs Squeezing Operator EBITDA Margins

Electricity prices climbed 54% from 2021-2024, while the national living wage rose nearly 10% in 2024, collectively knocking 3-5 percentage points off EBITDA for space providers. Only operators that deploy sensor-based HVAC and AI scheduling platforms have offset these pressures within the UK co-working spaces market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Size & Scale of Facility: Large Campuses Capture Life-Sciences Surge

Large campuses accounted for the fastest expansion path, registering a 9.11% CAGR outlook as of 2026-2031. Operators like Bruntwood SciTech and British Land are building 200,000 sq ft CL2-ready developments that compress fit-out timelines to eight weeks, making them magnets for biotech and AI drug-discovery ventures. Medium-scale hubs still hold the greatest slice at 43% of the UK co-working spaces market share, favored by enterprises distributing 5,000-20,000 sq ft footprints across multiple cities. Small neighborhood locations under 5,000 sq ft flourish in suburban London, absorbing work-from-near-home demand with minimal commute friction. Collectively, the trio of formats gives providers a diversified revenue mix that insulates them from cycle swings.

Demand heterogeneity requires operators to balance portfolio mix. Campuses can anchor multi-year agreements with anchor tenants, while medium hubs function as satellite nodes, and small sites satisfy freelancers. Groups that over-index on one scale risk occupancy shocks as tenant requirements evolve. Consequently, expansion blueprints in the UK co-working spaces market now bundle at least one asset in each scale tier to hedge against structural shifts.

By Sector: Life-Sciences Acceleration Reshapes Facility Design

IT & ITES led with 36.50% of 2025 revenue, yet life sciences is the fastest riser, forecast to post a 10.20% CAGR to 2031. The sector’s appetite for plug-and-play lab benches is evident at The EpiCentre in Haverhill, which filled initial capacity within three months of its 2024 launch. BFSI tenants follow close behind, opting for regional hubs where regulatory-compliant meeting rooms can be secured at a 30% discount to London rents. Professional-services consultancies leverage co-working for sprint teams in client geographies, sustaining baseline occupancy across centers.

Operators are retrofitting additional power, cooling, and air-change capabilities to lure biotech tenants while upgrading cybersecurity layers for BFSI occupiers. Sector diversification thus converts into rent resilience, broadening the UK co-working spaces market’s customer matrix and reducing correlation with single-industry cycles.

By End Use: Start-Ups Rebound as Venture Funding Stabilizes

Enterprises occupied 52% of the value in 2025, but momentum is tilting toward start-ups and freelancers, projected to advance at an 8.78% CAGR through 2031. Huckletree’s Oxford Circus site, which curated Web3 demo days and VC pitch weeks, hit 80% desk utilization within 90 days of opening, illustrating how programming lifts occupancy among early-stage firms. Freelancers gravitate to residential hubs that minimize commute times; IWG’s HomeWork tie-up added three south-London branches in 2024 that target this micro-segment.

Operators now tier membership products: corporates sign master service agreements covering multiple regions, start-ups receive rolling 12-month leases linked to funding milestones, and freelancers pay day rates. Precision in product-market fit keeps churn contained, helping stabilize revenues across the UK co-working spaces market.

Geography Analysis

England monopolized 86% of 2025 revenue, though regional cities are diluting London’s grip. Manchester absorbed 280,598 sq ft of flexible space in 2024, aided by USD 307 million in Bruntwood SciTech projects such as No. 3 Circle Square. Birmingham’s CreaTech Frontiers is adding 130,000 sq ft, financed partly by USD 8.5 million in public funds targeting gaming studios. Leeds benefits from the Northern Creative Corridor, channeling cultural grants into designer-friendly environments that sustain double-digit annual demand. London remains the primary headquarters node, but its share of the UK co-working spaces market declined from 92% in 2019 to 86% in 2025 as firms redistribute talent and cost bases.

Northern Ireland is on course for the quickest climb, with an 8.93% CAGR through 2031. Belfast is luring fintech and cybersecurity firms seeking a post-Brexit regulatory bridge and 40-50% rent arbitrage over Dublin. Scotland adds steady mid-single-digit growth; Edinburgh’s asset-management cluster values LEED Gold buildings that align with stewardship codes, while Glasgow’s renewable-energy ecosystem needs project suites for engineering teams. Wales lags, capped by softer venture inflows, yet Cardiff’s public-sector contractors are gradually embracing revenue-share sites that eliminate upfront capex. Across the islands, government grants and university anchors shape micro-pockets of outsized potential inside the UK co-working spaces market.

Competitive Landscape

IWG remains the scale outlier, operating 245,000 rooms worldwide and pledging 2,000 new UK sites over five years via management contracts that limit balance-sheet exposure. Bruntwood SciTech focuses on sector-specific assets, reporting USD 23.5 million operating profit and 900,000 sq ft of 2025 lettings across Manchester, Leeds, and Birmingham, underscoring the appetite for lab-enabled stock. Huckletree differentiates through curated communities and secured BREEAM Excellent ratings to capture ESG-centric corporates. Together, these players shape an ecosystem where scale and specialization co-exist in the UK co-working spaces market.

Investment activity signals growing institutional conviction. The Office Group’s USD 1.5 billion sales process drew pension and sovereign bidders, while revenue-share deals proliferate, 95% of IWG’s H1 2024 launches used this structure. Technology is a competitive wedge; Smart Spaces won PropTech Company of the Year 2025 for AI-driven occupancy and climate control that cuts energy by 20-30%. Operators lacking comparable platforms are becoming acquisition targets.

Non-traditional contenders such as hotel chains and retail landlords broaden choice but compress entry-level margins. This forces incumbents to create moats via sector-specific buildouts, wet labs, production studios, fintech-grade meeting suites, that justify premium desk rates. Consolidation is inevitable as elevated energy and labor costs outstrip the resources of providers with fewer than 10 sites, gradually lifting the floor of professionalism within the UK co-working spaces market.

UK Coworking Office Spaces Industry Leaders

International Workplace Group plc

WeWork

The Office Group

Landmark

Huckletree

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Bruntwood SciTech committed USD 21.5 million to expand Manchester One, adding four floors and raising total space to 160,000 sq ft, completion slated for 2028.

- February 2026: Bruntwood SciTech posted USD 23.5 million operating profit on USD 2.4 billion assets under management, signing 455 new customers and leasing 900,000 sq ft in FY 2025.

- January 2026: IWG opened 60,000 sq ft across Bolton, London, Croydon, Leeds, and Lisburn via capex-light management contracts.

- July 2025: Bruntwood SciTech completed a USD 16.4 million retrofit of the 38,000 sq ft King’s House, configuring it for CL2-compliant labs and co-working.

UK Coworking Office Spaces Market Report Scope

By Size & Scale of Facility

| Small |

| Medium |

| Large |

By Sector

| IT & ITES |

| BFSI |

| Business Consulting & Professional Services |

| Other Services (Retail, Lifesciences, Energy, Legal) |

By End Use

| Freelancers |

| Enterprises |

| Start-ups & Others |

By Country

| England | London |

| Rest of England | |

| Scotland | |

| Wales | |

| Northern Ireland |

| By Size & Scale of Facility | Small | |

| Medium | ||

| Large | ||

| By Sector | IT & ITES | |

| BFSI | ||

| Business Consulting & Professional Services | ||

| Other Services (Retail, Lifesciences, Energy, Legal) | ||

| By End Use | Freelancers | |

| Enterprises | ||

| Start-ups & Others | ||

| By Country | England | London |

| Rest of England | ||

| Scotland | ||

| Wales | ||

| Northern Ireland | ||

Key Questions Answered in the Report

What is the current value of the UK Coworking Office Spaces Market?

The sector generated USD 2.08 billion in 2026 and is projected to reach USD 2.99 billion by 2031.

How quickly is Northern Ireland region growing?

Northern Ireland is forecast to post a 8.93% CAGR between 2026 and 2031, the fastest rate among U.K. regions.

Which facility size is expanding the most?

Large-scale facilities locations lead with an 9.11% CAGR thanks to demand for proximity and convenience.

Which tenant sectors dominate demand?

Information technology holds the largest share, while professional services show the highest growth momentum.

Page last updated on: