Energy & Power

30th JulyUnlocking Market Potential for Solid-State Transformers

3 Min Read

The United Kingdom Electric Vehicle Battery Manufacturing Market Report is Segmented by Battery Chemistry (Lithium-Ion, Emerging, Lead-Acid, and Nickel-Metal-Hydride), Cell Format (Cylindrical, Prismatic, and Pouch), Propulsion (Battery Electric Vehicle, Plug-In Hybrid Electric Vehicle, and Hybrid Electric Vehicle), and Vehicle Type (Passenger Cars, Light Commercial Vehicles, Medium and Heavy Trucks, Buses and Coaches, and More).

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

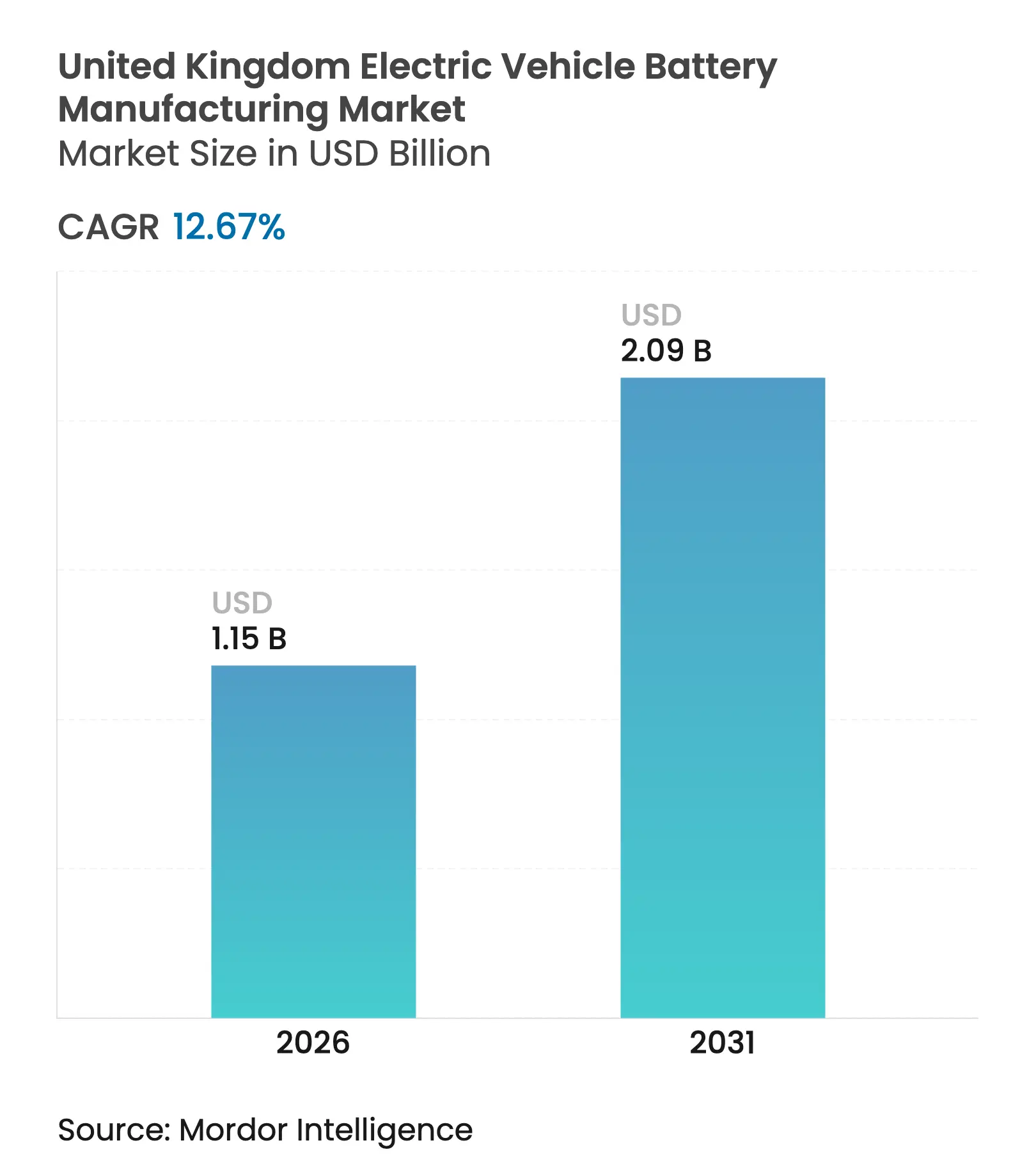

| Market Size (2026) | USD 1.15 Billion |

| Market Size (2031) | USD 2.09 Billion |

| Growth Rate (2026 - 2031) | 12.67 % CAGR |

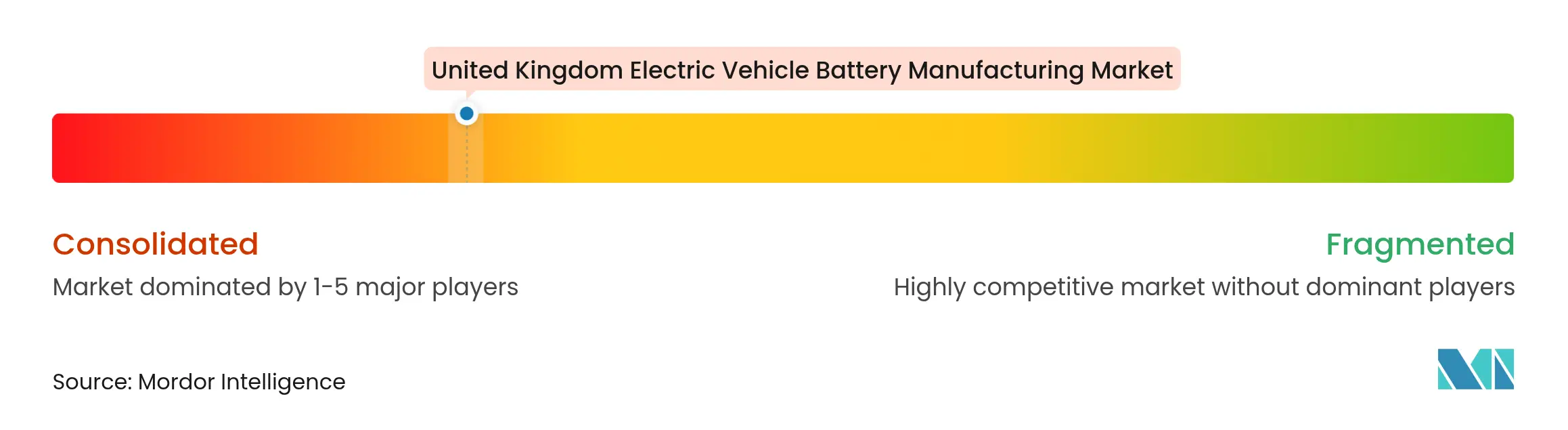

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Supply-side momentum stems from statutory zero-emission-vehicle mandates, multi-billion-pound gigafactory investments, and post-Brexit rules-of-origin thresholds that impose 10% tariffs on non-compliant vehicles from 2027. New capacity additions totaling 55.8 GWh promise to ease localisation pressures, yet electricity prices that run 50%–80% above continental peers, 5- to 7-year grid-connection queues, and an estimated 90,000-person skills gap threaten cost competitiveness and ramp-up timelines. Lithium-ion chemistries dominate but are pivoting toward cost-effective lithium-iron-phosphate cells, while light-commercial-vehicle electrification accelerates overall demand.[1]BBC Editors, “Gigafactory Race Intensifies,” BBC, bbc.com Continued policy certainty, timely infrastructure, and targeted workforce programs will determine whether the United Kingdom's electric vehicle battery manufacturing market secures its expected growth trajectory.[2]The Guardian Transport Desk, “EV Rules Tighten,” THEGUARDIAN, theguardian.com

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Government ZEV mandate fuels domestic capacity race Government ZEV mandate fuels domestic capacity race | +3.2% | National automotive clusters (West Midlands, North East, South West) | Medium term (2–4 years) | (~) % Impact on CAGR Forecast:+3.2% | Geographic Relevance:National automotive clusters (West Midlands, North East, South West) | Impact Timeline:Medium term (2–4 years) |

OEM-led gigafactory investments OEM-led gigafactory investments | +4.1% | Somerset, Sunderland, West Midlands | Long term (≥ 4 years) | |||

Automotive Transformation Fund subsidies Automotive Transformation Fund subsidies | +1.8% | Nationwide gigafactory and supply-chain sites | Medium term (2–4 years) | |||

EU-UK rules-of-origin pressure EU-UK rules-of-origin pressure | +2.7% | Entire UK, with spillover to Northern Ireland | Short term (≤ 2 years) | |||

Sodium-ion & solid-state R&D cluster Sodium-ion & solid-state R&D cluster | +0.9% | Cambridge, Oxford, Faraday Institution network | Long term (≥ 4 years) | |||

UK critical-minerals projects UK critical-minerals projects | +0.6% | Cornwall lithium belt | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Government ZEV Mandate Fuels Domestic Capacity Race

The zero-emission-vehicle mandate will rise from a 22% sales quota in 2024 to 80% for cars and 70% for vans by 2030, with financial penalties up to GBP 15,000 per non-compliant unit. Automakers therefore prioritize local batteries to avoid both fines and the 2027 tariff cliff, a dynamic estimated to expose OEMs to GBP 4.3 billion in cumulative costs if ignored. Flexibilities that allow credit borrowing dampen near-term pressure yet lapse after 2029, leaving little margin for slippage. The reinstated 2030 internal-combustion-engine ban steers all R&D toward battery-electric platforms. As a result, the United Kingdom electric vehicle battery manufacturing market gains demand pull that offsets some cost headwinds.

OEM-Led Gigafactory Investments

Tata’s Agratas began building a GBP 4 billion, 40 GWh plant in Somerset in 2024 and targets first output in 2026, BBC. Envision AESC secured GBP 1 billion in 2025 to add a 15.8 GWh line in Sunderland, leveraging extensive public guarantees. Nissan’s long-running 1.8 GWh facility may expand by 12 GWh if fresh anchor contracts materialize. Together, these staged projects create a capacity staircase that tracks OEM launch cycles and trims logistics costs by 8%–12% versus continental imports. Each venture still hinges on firm offtake agreements before full debt drawdown, underscoring execution risk.

EU-UK Rules-of-Origin Pressure to Localise Batteries

After 2026, assembled vehicles must contain 55% regional value and battery packs must reach 70%, or face 10% duties in the EU. That surcharge adds about GBP 3,500 to a mid-size EV and erodes OEM margins. Stellantis and Ford have already invested over GBP 480 million in UK battery assembly to sidestep the tariff. Any gigafactory that fails to break ground by mid-2025 risks missing the compliance window, leaving a projected 19.2 GWh capacity gap that could export production to continental Europe.

Sodium-Ion & Solid-State R&D Cluster Lowers Future CAPEX

Faradion’s sodium-ion work, now backed by Reliance, promises 20%–30% lower material costs by avoiding lithium and cobalt. Ilika advanced its solid-state Goliath P1.5 cell to OEM qualification in 2024, aiming for commercial runs by 2027. Solid-state designs could cut pack costs from GBP 80 per kWh in 2025 to GBP 50 by 2030.[3]Siemens Advanta Analysts, “UK Battery Cost Outlook 2025,” SIEMENS, siemens.com The Faraday Institution’s network accelerates lab-to-fab timelines to 5 years, enhancing the innovation pipeline. Nonetheless, the lack of a domestic sodium-ion or solid-state gigafactory means these chemistries will influence the United Kingdom electric vehicle battery manufacturing market chiefly after 2030.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Skilled-labour shortage for cell production Skilled-labour shortage for cell production | −1.4% | North East, West Midlands, South West gigafactory clusters | Medium term (2–4 years) | (~) % Impact on CAGR Forecast:−1.4% | Geographic Relevance:North East, West Midlands, South West gigafactory clusters | Impact Timeline:Medium term (2–4 years) |

UK industrial-energy prices vs. EU peers UK industrial-energy prices vs. EU peers | −2.3% | Nationwide, acute for energy-intensive coating and formation | Short term (≤ 2 years) | |||

Post-Brexit regulatory divergence Post-Brexit regulatory divergence | −0.8% | National supply-chain friction for chemical imports | Medium term (2–4 years) | |||

Grid-connection and planning delays Grid-connection and planning delays | −1.1% | Somerset, West Midlands, Sunderland | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Skilled-Labour Shortage for Cell Production

The sector needs 90,000 qualified workers by 2030, but currently produces fewer than 10,000 suitable graduates each year. Training cycles of up to 12 months extend commissioning curves and increase scrap rates during early runs. Wage competition from aerospace and semiconductor plants widens the talent gap by 10%–15% in the North East. Agratas has joined with Bridgwater & Taunton College, yet the national roll-out of similar programs would need GBP 200 million, still unfunded beyond 2026. Automation lowers headcount per GWh, but maintenance of high-precision robotics still demands mid-tier skills that remain scarce.

UK Industrial-Energy Prices vs. EU Peers

Average UK industrial power cost in 2024 was GBP 150–180 per MWh versus GBP 80–120 in France and Germany. Energy makes up 20%–30% of cell cost, so the premium adds GBP 8–12 per kWh to packs. Expiry of the Energy Bills Discount Scheme in March 2024 removed a GBP 40 per MWh buffer, exposing gigafactories to spot volatility. Renewable power purchase agreements under negotiation lock operators into 10- to 15-year fixed tariffs that risk overpayment if wholesale prices fall. Without a sector-specific tariff or expanded grid-scale storage, margins could compress by up to 300 basis points.

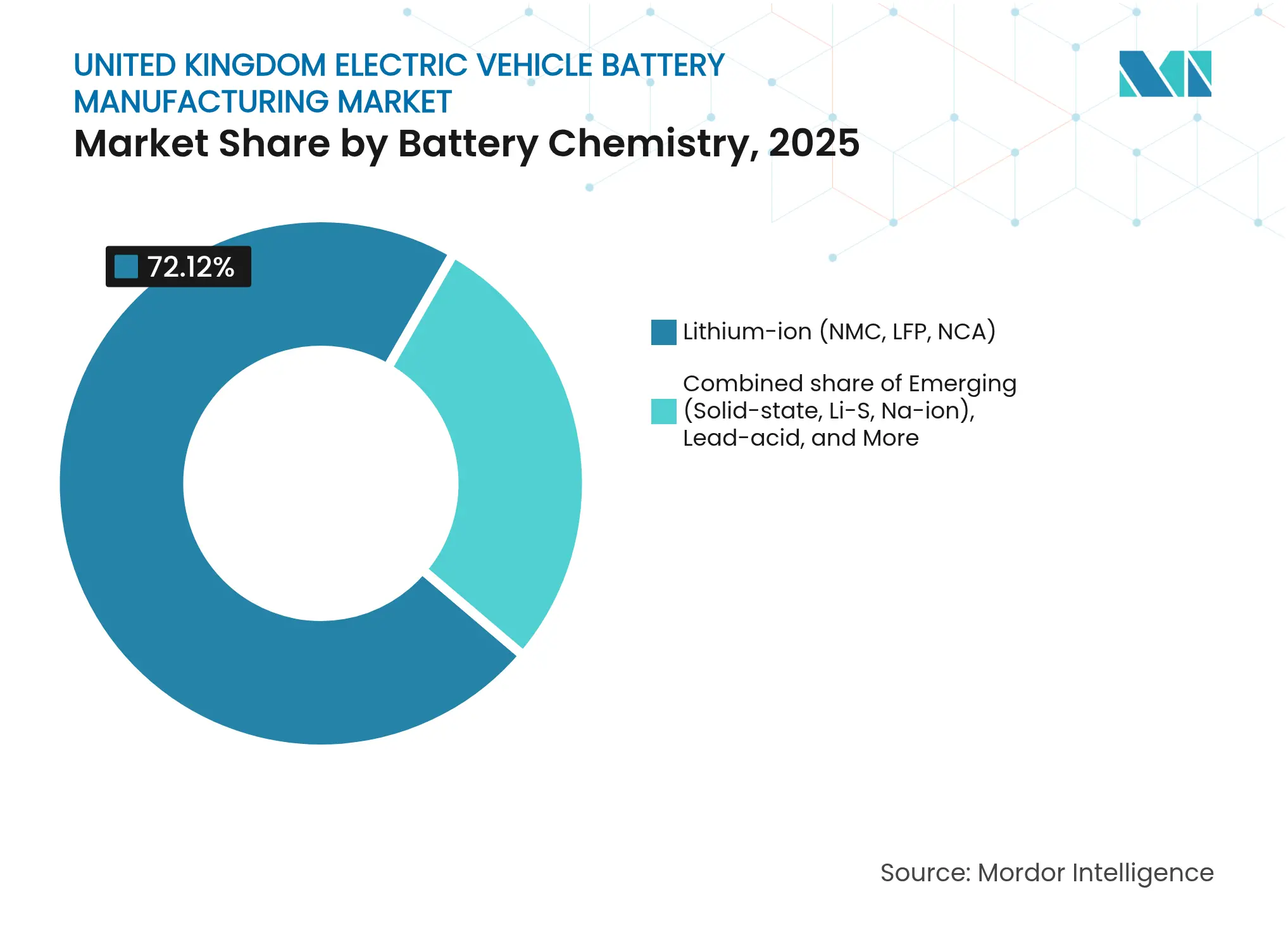

By Battery Chemistry: Lithium-Ion Maintains Dominance as LFP Scales

Lithium-ion chemistries captured 72.12% of the United Kingdom electric vehicle battery manufacturing market share in 2025, rising at a 15.08% CAGR that outpaces overall demand, BBC. The shift from nickel-manganese-cobalt to lithium-iron-phosphate cuts material costs by up to 30%, aligning with Stellantis and Ford van programs. NMC remains favored in premium passenger cars where high energy density supports ranges beyond 400 miles. Lead-acid and nickel-metal-hydride cells shrink as hybrids sunset after 2035. Emerging sodium-ion and solid-state chemistries hold under 2% share but could transform cost curves after 2030.

Through 2030, the United Kingdom electric vehicle battery manufacturing market size for lithium-ion packs is projected to increase in line with rising average pack capacities that move from 68 kWh in 2024 toward 75 kWh in 2030. Domestic lithium supply remains constrained; UK projects will meet under 30% of future needs, so feedstock diversity is essential. Johnson Matthey’s cathode exit redirects precursor sourcing to Asia, adding freight and compliance costs that local mining could partly offset. Faradion’s progress nevertheless signals longer-term optionality for lithium-free chemistry, especially in stationary storage where weight penalties matter less.

Note: Segment shares of all individual segments available upon report purchase

By Cell Format: Pouch Leads on Flexible Packaging

Pouch cells held 49.25% of the 2025 United Kingdom electric vehicle battery manufacturing market share thanks to their thin laminate construction that maximizes volumetric energy density. Envision AESC’s Sunderland line demonstrates an 8%–12% pack-mass reduction versus prismatic alternatives, supporting longer range at constant vehicle weight. Prismatic formats grow in structural packs that integrate cells into chassis, improving torsional stiffness for luxury SUVs. Cylindrical designs, popular in consumer electronics, hold under 15% share but could rise if local OEMs adopt cell-to-pack architectures.

By 2031, pouch cells are forecast to expand at a 14.62% CAGR, aligning with modular skateboard platforms under development in Europe. Cylindrical technologies such as 4680 formats remain under evaluation by Agratas for later phases, illustrating how the United Kingdom electric vehicle battery manufacturing market retains format flexibility without overcommitting capital. Nyobolt’s ultra-fast-charge prototype, based on proprietary pouch cells, shows that niche high-performance applications can command premium pricing that offsets small volumes.

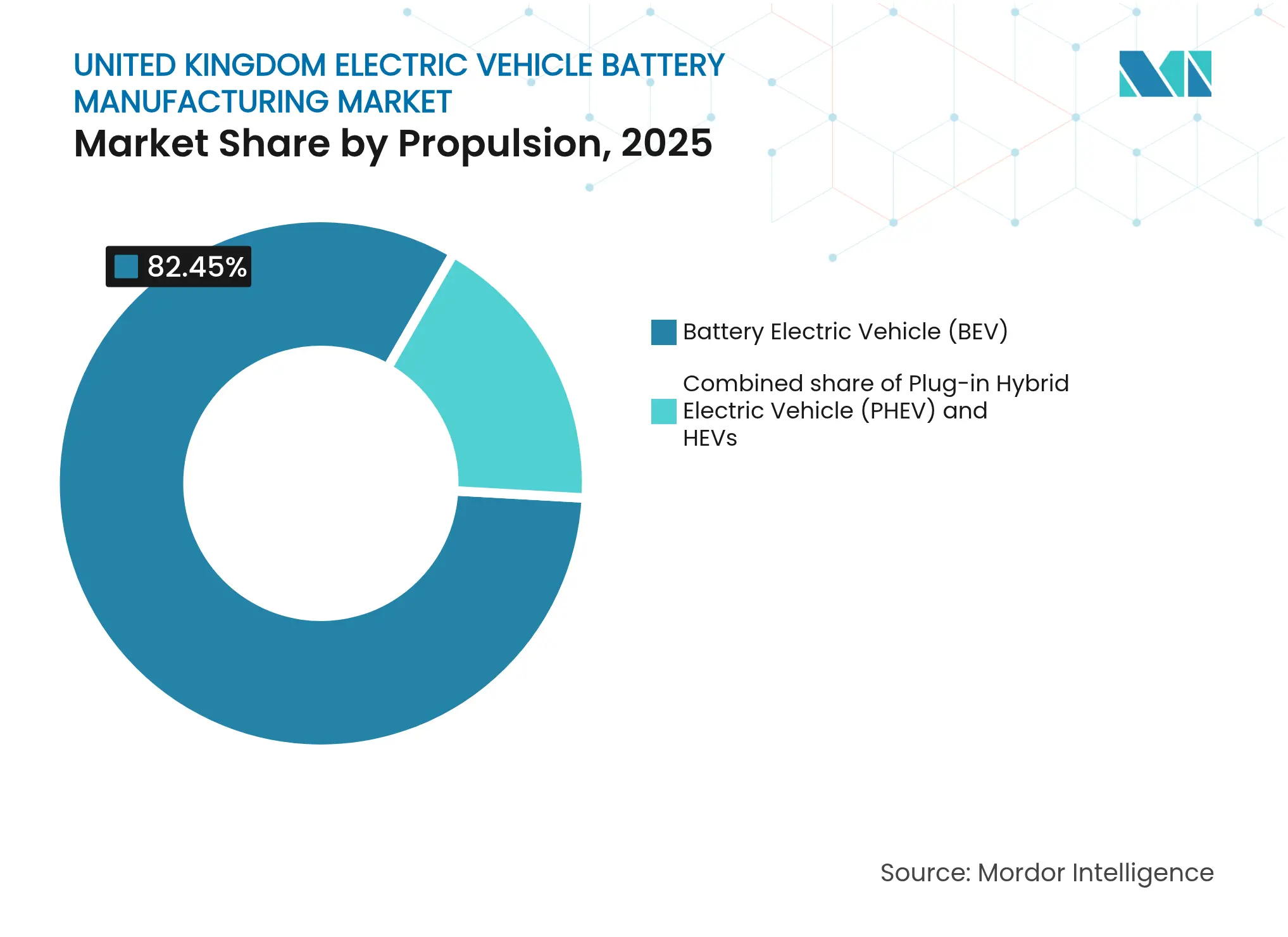

By Propulsion: BEV Share Surges Under Mandate Pressure

Battery-electric vehicles accounted for 82.45% of propulsion demand in 2025 and will grow at a 14.74% CAGR through 2031, lifted by tightening ZEV quotas and falling pack costs. Plug-in hybrids represented a 14% share but lost policy advantages after 2030 when internal-combustion bans took hold. The United Kingdom electric vehicle battery manufacturing market size associated with BEV packs, therefore, expands faster than unit sales because average capacities continue to climb.

Hybrid-electric vehicles, once critical for transition compliance, comprise less than 3% of battery demand and will fade by 2035. Pack-size inflation means every 1 percentage-point gain in BEV unit share equates to nearly 1 GWh of additional cell demand by 2030, an elastic linkage that underpins gigafactory business cases. OEMs structure offtake contracts around these forecasts, giving investors clarity on revenue visibility over 7- to 10-year horizons.

Note: Segment shares of all individual segments available upon report purchase

By Vehicle Type: LCV Electrification Outpaces Passenger Cars

Passenger cars delivered 79.35% of cell demand in 2025, yet will cede relative share as light commercial vehicles grow at a 20.95% CAGR. Clean Air Zones in major cities penalize diesel vans, and large fleets target full electrification before 2030. Stellantis and Ford assembly lines optimize 50–70 kWh LFP packs that meet high-utilization duty cycles at lower total cost of ownership.

The United Kingdom electric vehicle battery manufacturing market size attached to LCV packs will therefore compound more rapidly than the passenger-car segment, creating demand spikes in the Somerset and Ellesmere Port regions. Medium and heavy trucks plus buses represent niche demand today but may scale after 2027 as range improvements converge with depot charging infrastructure. Arrival’s 2024 collapse removed a domestic truck-battery hopeful, showing capital-intensity risks that favor incumbents with strong balance sheets.

The United Kingdom electric vehicle battery manufacturing market clusters around Sunderland in the North East, Bridgwater in the South West, and Coventry in the West Midlands. Envision AESC will lift Sunderland capacity from 1.8 GWh to 17.6 GWh by 2027, leveraging adjacent automotive assembly and Teesside chemical suppliers. Somerset’s 40 GWh Agratas plant benefits from brownfield rail links and a GBP 150 million local-infrastructure package, positioning the South West as the largest single-site contributor by the early 2030s.

The West Midlands Gigafactory proposes 60 GWh but still lacks planning approval or an anchor OEM, reflecting grid-connection queues of up to 7 years and uncertain power pricing. Sunderland’s proximity to offshore wind promises the lowest renewable-power costs, whereas Somerset faces labor competition from Hinkley Point C nuclear construction. Cornwall’s lithium projects could shorten supply chains but cover under 30% of 2035 demand, ensuring continued reliance on imported feedstock.

Scotland, Wales, and Northern Ireland remain peripheral, given limited local vehicle production and the capital requirements of greenfield sites. Northern Ireland’s Windsor Framework, however, allows tariff-free access to both UK and EU markets, offering strategic optionality for future investors. Overall, geographic concentration helps synergies but heightens exposure to local disruptions, making resilience planning vital for the United Kingdom electric vehicle battery manufacturing market.

Market Concentration

The United Kingdom electric vehicle battery manufacturing market remains highly concentrated. Envision AESC operates the longest-running plant, while Agratas races to commission the country’s largest facility by 2026. Government co-investment lowers financing costs: Agratas received GBP 500 million of support, and Envision AESC unlocked GBP 680 million in guarantees, illustrating a partnership model that de-risks capital outlays near USD 1 billion for every 10 GWh of new capacity.

White-space opportunities center on closed-loop recycling, where Recyclus Group pilot lines aim to recover lithium and cobalt from end-of-life packs. Nyobolt and Ilika occupy the innovation frontier with fast-charge and solid-state technologies, courting premium OEMs for early adoption. CATL’s 2024 plan for a new European plant keeps the competitive field fluid; if energy subsidies improve, a UK location could emerge as a contender.

Automation strategies dominate capital spending. Beckhoff control systems and ABB robotics reduce manual electrode handling, but raise CAPEX to roughly GBP 1 billion per 10 GWh. The West Midlands site demonstrates the financing challenge; without an anchor offtake contract, lenders have withheld support, leaving the proposal in limbo. Player concentration is expected to tighten as gigafactories reach scale, yet smaller niche makers such as AMTE Power may persist by serving aerospace and motorsport verticals.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Electric vehicle (EV) battery manufacturing involves designing, producing, and assembling batteries for EVs. The process starts with sourcing raw materials like lithium, cobalt, and nickel. These materials are then used to create individual battery cells, which are grouped into modules.

The United Kingdom electric vehicle battery manufacturing market is segmented by battery chemistry, cell format, propulsion, and vehicle type. By battery chemistry, the market is segmented into lithium-ion (NMC/LFP/NCA), emerging (solid-state/Li-S/Na-ion), lead-acid, and nickel-metal-hydride. By cell format, the market is segmented into cylindrical, prismatic, and pouch. By propulsion type, the market is segmented into battery electric vehicle (BEV), plug-in hybrid electric vehicle (PHEV), and hybrid electric vehicle (HEV). By vehicle type, the market is segmented into passenger cars, light commercial vehicles, medium/heavy trucks, buses, and two/three-wheelers. The report offers the market size in value terms in USD for all the abovementioned segments.

Unlocking Market Potential for Solid-State Transformers

3 Min Read

Unlocking Opportunities in Singapore's Chemical Logistics Market

5 Min Read

Deep-Dive Analysis of Feed Probiotics Across Key Regions

5 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.