Size and Share of Mixing Equipment Market For Battery Manufacturing

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

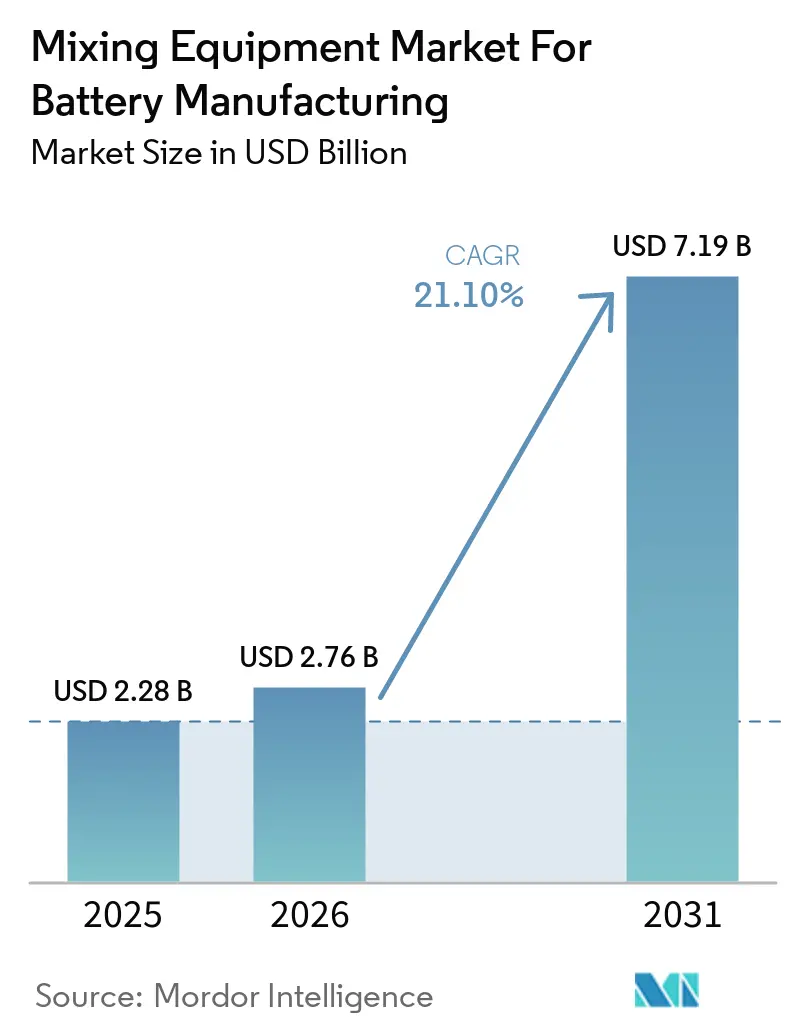

| Market Size (2026) | USD 2.76 Billion |

| Market Size (2031) | USD 7.19 Billion |

| Growth Rate (2026 - 2031) | 21.10% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Mixing Equipment Market For Battery Manufacturing by Mordor Intelligence

The battery mixing equipment market for battery manufacturing size is expected to grow from USD 2.28 billion in 2025 to USD 2.76 billion in 2026 and is forecast to reach USD 7.19 billion by 2031 at 21.1% CAGR over 2026-2031. The battery mixing equipment market is moving into a phase where slurry preparation is treated as a core yield step rather than a routine plant operation, because mixing quality has a direct effect on cell consistency and defect control in lithium-ion production.[1]Qinhuangdao Pengyi Intelligent Technology Co., Ltd., “Yushun Intelligent Double Planetary Mixer: Innovating the Preparation Technology of Lithium Battery Cathode Slurry,” Qinhuangdao Pengyi Intelligent Technology Co., Ltd., qhdpengyimc.com Producers are also reshaping capital plans around large battery plant build-outs, which is lifting demand for high-throughput systems, cleaner process control, and validated equipment performance in new facilities. The battery mixing equipment market is also seeing a clear premium for systems that can manage vacuum deaeration, inert atmosphere processing, and tighter temperature control, because newer chemistries and larger plant scales leave less room for process drift.[2]NETZSCH-Feinmahltechnik, “Improving Battery Performance and Reducing Mixing Time with NETZSCH Planetary Mixer PMH,” NETZSCH-Feinmahltechnik, grinding.netzsch.com At the same time, export controls on selected Chinese battery production equipment and the narrow supplier base in some advanced mixing formats are pushing Western buyers to qualify alternative sources and accept higher equipment pricing when supply resilience matters most. These conditions leave the battery mixing equipment market supported by strong factory investment, tighter process requirements, and a wider gap between standard mixers and high-value systems built for next-generation battery production.

Key Report Takeaways

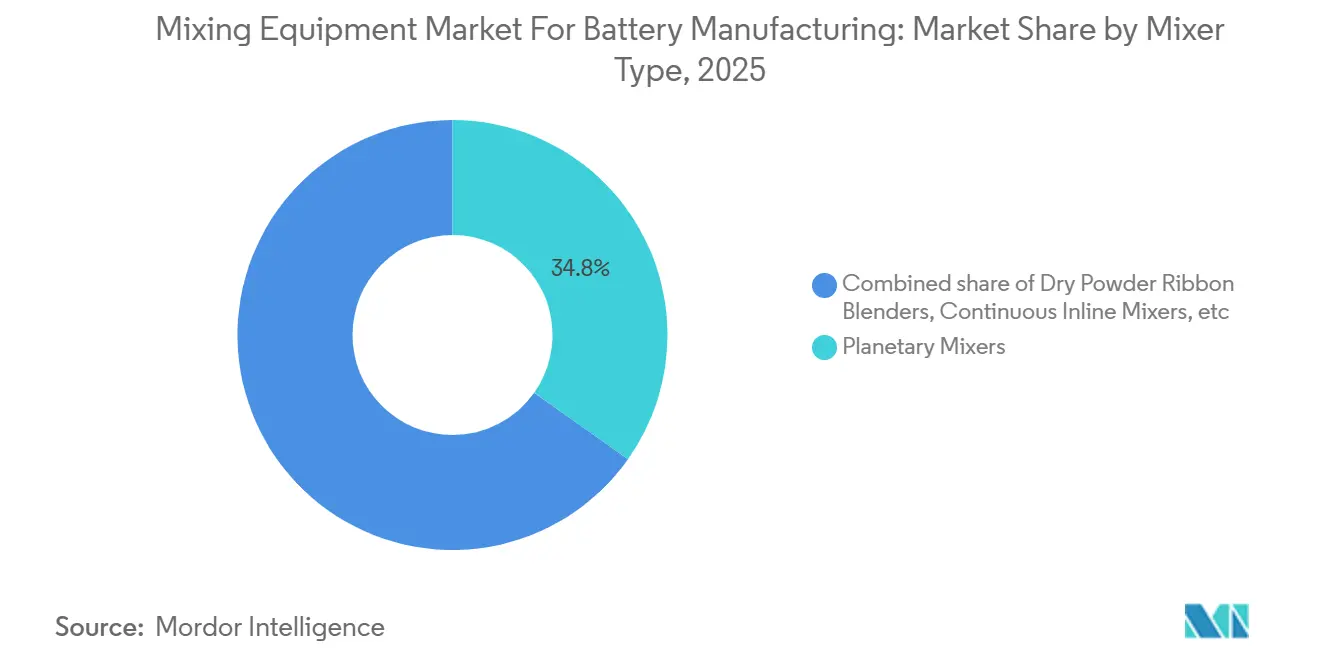

- By mixer type, planetary mixers held 34.8% of the battery mixing equipment market share in 2025, while solid-state low-shear planetary mixers are projected to expand at 24.6% CAGR through 2031.

- By capacity rating, 1,000-5,000 L systems accounted for 41.2% of the battery mixing equipment market size in 2025, while the more than 5,000 L range is forecast to grow at 25.3% CAGR through 2031.

- By battery chemistry served, LFP represented 46.5% of revenue in 2025, while solid-state and sulfide lines are expected to advance at 31.8% CAGR through 2031.

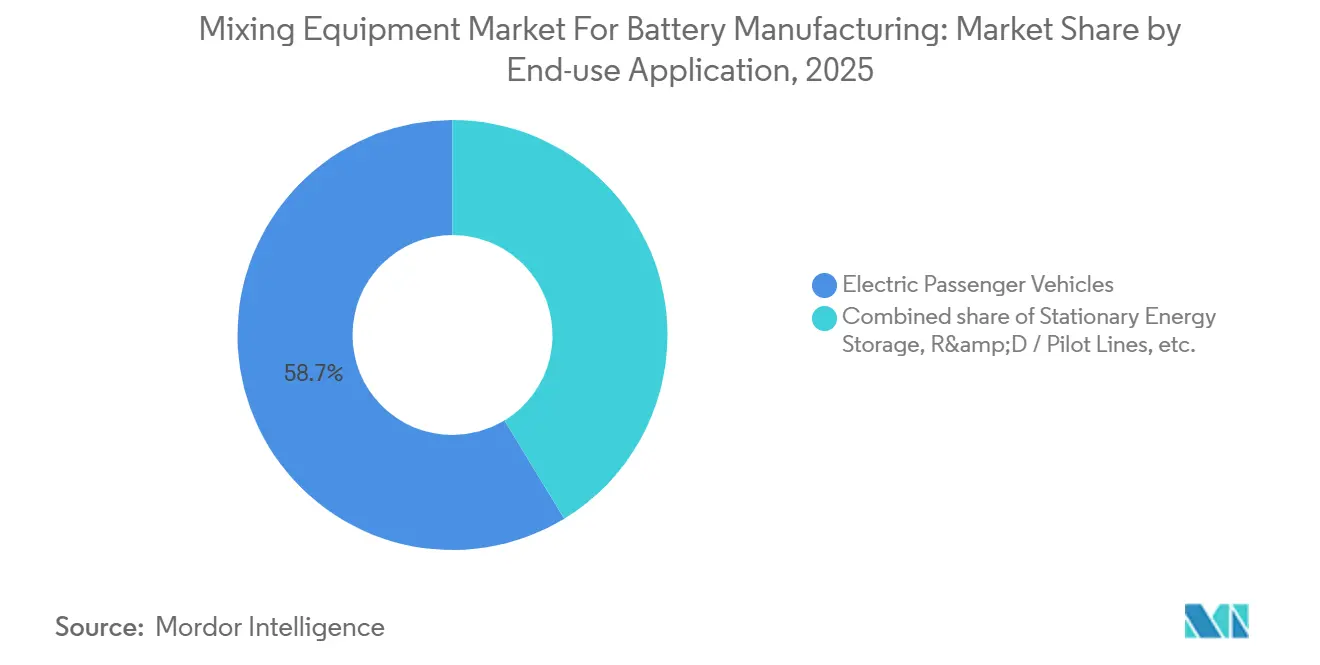

- By end-use application, electric passenger vehicles captured 58.7% of demand in 2025, while stationary energy storage is expected to record the highest CAGR at 27.1% through 2031.

- By geography, Asia-Pacific led with 63.4% revenue share in 2025, while North America is projected to grow at 26.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Insights and Trends of Mixing Equipment Market For Battery Manufacturing

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In Global Gigafactory Build-Outs Post Inflation Reduction Act | +5.2% | North America, Central and Eastern Europe | Medium term (2-4 years) |

| Rapid Capacity Additions By Tier-2 Battery Makers In Southeast Asia | +2.8% | ASEAN core (Vietnam, Indonesia, Thailand) | Short term (≤ 2 years) |

| Pressing Need For Slurry Uniformity To Enable Next-Gen High-Ni Cathodes | +3.5% | Global (APAC, Europe, North America) | Medium term (2-4 years) |

| Re-Shoring Incentives For Critical Battery Equipment In The EU | +1.8% | Europe (Germany, France, Italy, Nordic countries) | Long term (≥ 4 years) |

| Mainstream EV Penetration Lifting Demand For Large-Scale Inline Mixers | +2.5% | Global | Short term (≤ 2 years) |

| Emergence Of Solid-State R&D Lines Requiring Low-Shear Planetary Mixers | +2.2% | APAC (China, Japan, South Korea), Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

IRA-Driven Giga-Factory Build-Outs Reshape Equipment Procurement

The battery mixing equipment market is benefiting from the U.S. battery plant pipeline that followed the Inflation Reduction Act, with 23 announced cell factories tied to USD 52 billion in planned investment and 490 GWh of annual capacity. Those projects create concentrated equipment buying cycles because every new cell plant requires slurry preparation assets before coating, and downstream line qualification can move ahead. The largest pull is landing in high-capacity planetary and inline systems, especially where operators need 1,000-5,000 L units or more than 5,000 L platforms to support scaled output. This wave is also exposing a gap between U.S. battery policy and U.S. machinery capture, since Charles Ross & Son said domestic suppliers have lost some new orders to Asian turnkey competitors in U.S.-sited battery projects.[3]Charles Ross & Son Company, “How ROSS Mixers Is Advancing US Battery Manufacturing – It Starts at Home,” Charles Ross & Son Company, mixers.com That issue matters in the battery mixing equipment market because order flow may rise quickly while domestic equipment value capture grows more slowly. Envision AESC’s South Carolina project shows the scale involved, because a single plant tied to BMW was planned at USD 3 billion and 30 GWh per year, which is large enough to create a meaningful upstream mixer requirement on its own.

Slurry Uniformity For High-Ni Cathodes Creates Premium Equipment Demand

The battery mixing equipment market is also being pushed higher by the difficulty of preparing stable, high-quality slurry for nickel-rich cathodes. Research on water-based NMC811 electrodes showed that lithium leaching can drive slurry pH toward 12, which raises corrosion risk at the aluminum current collector and makes fast process control more important. That operating window favors equipment with inert handling, tighter thermal control, and reliable vacuum deaeration rather than standard mixing configurations. Pengyi’s battery slurry process guidance also highlights how modern dual planetary systems combine dry and wet charging, high-viscosity handling, and vacuum deaeration in one process sequence, which helps explain why buyers pay more for validated systems.[4]Qinhuangdao Pengyi Intelligent Technology Co., Ltd., “The Double Planetary Mixer - Critical Equipment for Consistent Lithium Battery Slurry Production,” Qinhuangdao Pengyi Intelligent Technology Co., Ltd., qhdpengyimc.com Fraunhofer IPA work reported in 2026 found that high-pressure wet jet milling of LFP cathode slurry reduced average particle size by 39%, cut process energy by 42%, and improved 1C capacity by 12.8%, which supports the case for better slurry preparation hardware even in mature chemistries. The battery mixing equipment market is likely to keep favoring premium systems from 2026 onward as aqueous processing and solvent-related compliance become more important in Europe.

Mainstream EV Penetration Accelerates Inline And Large-Format Mixer Adoption

The battery mixing equipment market is moving toward larger and more continuous systems because EV cell production at 20 GWh and above strains traditional batch mixing routines. NETZSCH reported that a conventional planetary setup at that scale would need 24 anode units and 12 cathode units, while its PMH platform could reduce that requirement to 6 and 3, with technical availability above 95% and energy use near 80 kWh per metric ton. That reduction changes not only utility consumption but also floor space, staffing, and maintenance planning, which makes mixer design a broader plant economics question. Lödige also states that its battery mixing systems are being positioned for larger cathode and anode lines as industrial battery output rises, which supports the shift toward bigger and more productive platforms. The battery mixing equipment market is therefore seeing faster acceptance of inline and large-format solutions where throughput limits are more costly than equipment price. This trend is reinforced by high EV adoption in leading battery economies, because strong vehicle output gives cell makers a clearer case for investing in equipment that removes upstream slurry bottlenecks.

Solid-State Battery Industrialization Creates A Specialized Mixer Sub-Market

The battery mixing equipment market is opening a specialized demand pool around solid-state battery production, where sealed handling and low-shear control matter more than in standard wet slurry processing. Sulfide electrolytes require very dry conditions and inert atmosphere protection, which limits the usefulness of open-vessel designs and creates room for purpose-built equipment. Lead Intelligent said its dry-process platform for solid-state production delivered more than 15% total material and manufacturing cost reduction and 35% energy savings compared with conventional wet-process lines, which gives early buyers a measurable economics argument. In March 2026, the same company presented solid-state mixing and coating equipment at InterBattery Korea and reported slurry preparation time below 2 hours with defoaming pressure at -95 kPa, showing how quickly this equipment niche is becoming more defined. SIEHE Group also moved into this space with kiloton-scale solid-state sulfide material line offerings in 2026, which shows that established wet-process suppliers are repositioning for the next procurement cycle. The battery mixing equipment market is likely to see one of its clearest high-growth pockets in these low-shear and sealed-atmosphere systems as pilot lines become industrial lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capex And Long Lead-Times For Custom High-Viscosity Mixers | -2.5% | Global, most acute in non-APAC regions | Medium term (2-4 years) |

| Volatility In Li, Ni, And Solvent Prices Squeezing OEM Cash-Flows | -1.8% | Global | Short term (≤ 2 years) |

| Scarcity Of Skilled Process Engineers For Electrode-Slurry Optimization | -1.2% | North America, Europe | Long term (≥ 4 years) |

| Complex Export-License Regimes For High-Energy-Density Battery Tech | -1.5% | Global (non-China sourcing routes most affected) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capex And Lead-Times Constrain Mid-Tier Cell Producers

The battery mixing equipment market still faces a clear adoption limit because custom high-viscosity systems are expensive and often take too long to arrive for smaller battery projects. Pengyi’s process notes show why costs rise, since advanced battery slurry mixers must handle wide viscosity ranges, vacuum deaeration, precise charging sequences, and clean internal finishes in one design. NETZSCH also positions its gigafactory-grade equipment around process performance, which supports the view that top-tier systems are engineered assets rather than standard vessels. When new entrants need specialized systems for nickel-rich or solid-state work, those extra design requirements lengthen procurement schedules and widen the cost gap with simpler alternatives. The result is a battery mixing equipment market where tier-1 producers can secure the most capable systems more easily than smaller operators. That pattern leaves many mid-tier buyers dependent on lower-cost imported equipment, even when process differentiation would favor a better machine.

Export Licensing Complexity Disrupts Global Equipment Sourcing

The battery mixing equipment market is also being held back by licensing and trade compliance risk, especially where manufacturers rely on Chinese equipment for cathode-related processes. China expanded export controls in late 2025 to cover mixers and grinding mills used in cathode material production, which means exporters must obtain licenses before shipment in controlled categories. That change forces Western gigafactory operators to qualify non-Chinese alternatives more quickly, often at higher cost and with longer delivery periods. It also reduces planning certainty for projects that were expected to have a single global sourcing strategy across China, Europe, and North America. In parallel, Europe’s policy direction is increasingly supportive of local battery manufacturing equipment, which points to a more divided procurement structure over time. The battery mixing equipment market, therefore, faces a near-term mismatch between strong demand and a more complex trade path for the most specialized systems.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mixer Type: Planetary Platforms Underpin Slurry Quality At Scale

Planetary mixers held 34.8% of the battery mixing equipment market share in 2025, which kept them in the lead across mixer types because they remain the default option for both anode and cathode slurry preparation. Their position comes from process flexibility rather than simple legacy use, since modern dual planetary designs can manage very high viscosities, support vacuum deaeration, and allow staged dry-to-wet charging in the same vessel. That ability matters in the battery mixing equipment market because manufacturers need fewer process compromises when switching between formulations, solids loading levels, and production scales. NETZSCH also reported that its PMH platform can shorten mixing time and reduce unit counts at gigafactory scale, which supports continued demand for large planetary systems where consistency and plant efficiency matter together. The category also remains well aligned with LFP and NMC production, where buyers still value a proven route to viscosity control and air removal before coating.

The fastest-growing sub-segment is solid-state low-shear planetary mixing, which is projected to advance at 24.6% CAGR through 2031 as more solid-state programs move from laboratory work into equipment ordering. That growth rate reflects a different set of process needs, because sulfide and dry-process systems require gentler handling, better sealing, and tighter environmental control than many wet-slurry lines. SIEHE Group’s 2026 move into kiloton-scale solid-state sulfide production line supply shows that even established equipment makers now view this niche as a real commercial opportunity rather than an experimental extension. The battery mixing equipment industry is also seeing more room for inline dispersion platforms where plant footprint and continuous processing matter, and Ystral’s Batt-TDS system has gained attention for improved long-term cycling performance in validated tests. Dual-shaft dispersers and continuous inline mixers still serve narrower use cases, but they are becoming more relevant where producers want a smaller footprint, faster flow, or a better fit for medium-viscosity formulations. The battery mixing equipment market is, therefore, keeping planetary systems at the center while still widening into more specialized mixer formats.

By Capacity Rating: Large-Format Systems Align With Giga-Scale Manufacturing Economics

The 1,000-5,000 L range accounted for 41.2% of revenue in 2025, which reflects the operating base of plants that sit between pilot-scale work and the largest gigafactory builds. This capacity band fits well with current commercial battery production because it can feed coating operations at a meaningful scale without forcing every plant into the most extreme equipment size. It also gives producers a practical balance between throughput, vessel utilization, maintenance access, and capital cost. In the battery mixing equipment market, this middle band has become the most common answer for facilities that need repeatable output but still want flexibility across chemistries and line configurations. That is why this segment remains the core installed base for many commissioned cell plants.

The more than 5,000 L segment is the fastest-growing part of the battery mixing equipment market size, with 25.3% CAGR projected through 2031 as larger battery plants try to remove upstream throughput bottlenecks. The case for these systems is strongest where line economics depend on high volume output, lower labor intensity, and fewer parallel mixer units across the same plant. Lödige has already pointed to the demand for larger mixer configurations as battery production targets rise, which supports the move toward higher usable vessel volume in commercial procurement. At the other end, sub-200 L systems remain important for chemistry development, process validation, and small-batch qualification before larger capital commitments are made. The BATMACHINE project and research line work in Europe show how smaller systems still carry strategic value when new formulations must be tested under realistic production conditions. The 200-1,000 L range fills the bridge role between laboratory and early production, especially for regional cell makers that are not yet operating at gigafactory scale. The battery mixing equipment industry, therefore, spans a wide capacity curve, but demand is rising fastest where plants are designed for very large annual output and tighter capital efficiency.

By Battery Chemistry Served: LFP Volume And Solid-State Demand Define Dual Growth Axes

LFP represented 46.5% of 2025 demand, which made it the broadest chemistry base in the battery mixing equipment market because EV and energy storage producers continued to rely on its cost and safety profile. Its large footprint is supported by the steady expansion of LFP across passenger EVs and utility-scale storage, which keeps upstream electrode preparation demand high even without the strictest process complexity. Fraunhofer IPA's work in 2026 showed that better LFP slurry preparation can still deliver measurable gains, including a 12.8% capacity increase at 1 °C and 42% lower process energy compared with standard dissolver mixing. That finding matters because it shows the battery mixing equipment market can still extract value from mature chemistries through process improvement rather than chemistry change alone. Water-based LFP processing also widens the usable equipment pool by reducing the role of solvent recovery and some explosion-proof requirements, which supports supplier access in parts of the value chain.

Solid-state and sulfide systems are forecast to grow at 31.8% CAGR through 2031, which makes them the fastest-rising chemistry segment in the battery mixing equipment market size. That pace reflects where the next equipment procurement wave is forming, because buyers need sealed, inert, low-residue, and low-shear systems that differ clearly from traditional wet slurry platforms. Lead Intelligent’s dry-process battery manufacturing platform and SIEHE Group’s 2026 solid-state line activity both show that suppliers are already adapting portfolios around this demand shift. NMC811 lines still command high per-unit equipment spend because pH control, contamination avoidance, and atmosphere management remain demanding in nickel-rich processing. Others, including sodium-ion and LTO, are smaller but important because they keep pilot demand active and create early commercial opportunities for specialized mixing setups. TMAX’s sodium-ion electrode preparation equipment is one example of how these smaller chemistry routes are becoming more visible in practical equipment supply. The battery mixing equipment market is thus being shaped by one large mature demand base in LFP and one faster-rising procurement frontier in solid-state systems.

By End-use Application: EV Passenger Volume Dominates As Grid Storage Accelerates

Electric passenger vehicles accounted for 58.7% of end-use demand in 2025, which kept them as the largest outlet in the battery mixing equipment market because cell volume for mainstream EV production remains unmatched. This leadership is tied to the scale of vehicle battery programs, standardization of large cell formats, and continuing pressure to raise throughput without sacrificing slurry consistency. In practical terms, every large EV battery contract feeds upstream requirements for electrode preparation equipment, vessel capacity, and validated mixing performance. The SK On and Nissan supply agreement, along with YoonSung F&C’s related mixing process order for Kentucky Plant 1, illustrates how downstream vehicle demand can translate into direct equipment procurement for slurry systems. Commercial EV and off-highway uses remain meaningful as well, especially where heavier-duty battery formats call for durable and scalable mixing lines.

Stationary energy storage is the fastest-growing end-use in the battery mixing equipment market, with 27.1% CAGR expected through 2031. That growth is being driven by large LFP-based storage projects, where battery volume expansion at the system level creates a direct need for more electrode mixing capacity upstream. EVE Energy’s Malaysia expansion for 10-15 GWh of LFP storage capacity is a useful example of how storage investment starts to look similar to EV-scale equipment demand once plant size reaches commercial scale. YIFI Laser’s delivery of a fully automated 5 GWh energy storage container assembly line to a European client in 2025 also reflects the broader industrial build-out around grid storage programs. Consumer electronics and R&D lines are much smaller in volume, yet they remain strategically useful because they support trial work, new material qualification, and fast batch reproducibility in early-stage battery programs. PRIMIX has positioned its dedicated battery solutions activity around exactly that need for repeatable small-batch process control and analytics. The battery mixing equipment market, therefore, still depends on passenger EV volume, but new storage projects are becoming the clearest source of faster incremental growth.

Geography Analysis

Asia-Pacific accounted for 63.4% of the battery mixing equipment market share in 2025, which kept the region as the clear center of global demand because it combines cell manufacturing scale, supplier depth, and faster commercial execution. China remains the core of that position, supported by its entrenched battery production base and its strong installed mix of slurry preparation systems across commercial plants. The battery mixing equipment market in the wider Asia-Pacific is also being lifted by new capacity additions in Vietnam, Indonesia, and Thailand, where battery and material projects are moving from investment plans into plant development. Indonesia’s Batang SEZ investment in LFP output and research capacity is one example of how Southeast Asia is adding practical demand for upstream battery process equipment rather than only attracting policy attention. Japan and South Korea add a different strength, because their suppliers are more active in premium, application-specific systems for advanced battery programs.

North America is the fastest-growing regional block in the battery mixing equipment market, with 26.4% CAGR projected through 2031. That momentum is tied to the post-IRA battery plant pipeline, which is large enough to support several years of equipment orders if projects continue through planned construction phases. Charles Ross & Son gives the region a domestic manufacturing base for mixers and related controls, but its comments on losing orders to Asian competitors also show that North American growth does not automatically stay within North American equipment suppliers. Canada benefits more indirectly through mineral and processing investments, while Mexico remains linked to nearshoring opportunities tied to EV assembly and regional trade rules.

Europe remains a strategically important part of the battery mixing equipment market because regulation, funding, and process standards are shaping buyer decisions as much as plant count. Germany, Italy, France, and the Nordic countries host several of the region’s most active battery manufacturing and research programs, including Fraunhofer-linked work and Italian continuous mixing installations for LFP production. The European Commission’s strategic raw materials project selection in 2025 also supports the wider midstream base that feeds battery manufacturing investment decisions. That policy backdrop favors suppliers able to prove cleanroom readiness, process quality, and local support rather than low upfront cost alone. South America, the Middle East, and Africa remain much smaller today, though pilot and early-stage projects suggest that future demand will begin with R&D and small commercial lines before moving into full-scale plant procurement.

Competitive Landscape

The battery mixing equipment market is moderately fragmented, and no supplier appears to hold more than a mid-single-digit global revenue share across all equipment types and regions. That structure reflects the way demand is spread across different chemistries, batch sizes, plant formats, and regional sourcing preferences. European suppliers such as NETZSCH, Bühler, and Ystral compete mainly through process validation, consistency, and documented cell-quality outcomes rather than simple delivery volume. NETZSCH’s work with battery manufacturing partners in the BATMACHINE project shows how suppliers are using collaborative testing to position themselves in advanced electrode preparation and gigafactory qualification. Ystral also stresses measurable performance in slurry dispersion, including long-term cell behavior and low contamination, which makes its offering relevant where qualification standards are rising.

Chinese competitors operate on a different basis inside the battery mixing equipment market, with a stronger emphasis on cost, delivery speed, and broad turnkey supply. SIEHE Group is expanding production capacity with a smart manufacturing facility in Jiaxing, and that scale-up supports faster response to buyers who want quicker supply at industrial volume. Lead Intelligent is also moving aggressively in solid-state and dry-process platforms, which gives it a foothold in one of the highest-growth equipment niches now emerging. Korean suppliers remain smaller globally, but they are becoming more visible in large customer programs, especially where continuous mixing and high-volume line integration matter.

Strategic moves in the battery mixing equipment market are increasingly focused on validation, specialization, and production readiness rather than basic catalog expansion. SIEHE Group’s April 2026 cooperation around kiloton-scale solid-state sulfide production equipment is one clear example of a supplier moving early into a future high-value sub-segment. Lead Intelligent’s dry-process battery line deliveries and InterBattery Korea recognition show a similar effort to define performance benchmarks before the solid-state field broadens further. NETZSCH is differentiating through inline analytics and viscosity monitoring, which points to more process intelligence becoming part of the equipment value proposition rather than an added option. The battery mixing equipment market is therefore competitive, but the strongest suppliers are building their position through repeatable process outcomes, new chemistry readiness, and closer alignment with plant-scale economics.

Leaders of Mixing Equipment Market For Battery Manufacturing

SIEHE GROUP

Charles Ross & Son Company

Xiamen Tmax Battery Equipments Limited

IKA-Werke GmbH

MIXACO Maschinenbau

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SIEHE Group signed a cooperation agreement with a globally leading solid-state battery material enterprise to supply core production equipment for a kiloton-scale solid-state sulfide electrolyte production line integrating mixing, reaction, and vacuum drying processes, and commenced accepting orders for thousand-ton intelligent production lines for solid-state sulfide battery material preparation the first such commercial-scale program for the company.

- March 2026: LEAD Intelligent Equipment showcased its circulating kneading disperser for all-solid-state battery slurry production at InterBattery Korea, where its dry mixing and coating system won the Best Equipment of the Year award, the platform supports slurry preparation time under 2 hours and operates at -95 kPa defoaming pressure.

- January 2026: SIEHE Group commenced construction of a 57,341 m² smart manufacturing facility in Jiaxing, Zhejiang (construction started August 2025), targeting operational status by July 2026 for an annual production of 500 intelligent equipment sets, nearly doubling the company's existing 32,000 m² combined plant footprint.

- September 2025: LEAD Intelligent delivered dry-process mixing and coating equipment for large-scale solid-state battery production to global automotive OEMs, reporting over 15% total material and manufacturing cost reduction, 35% energy savings, and mechanical production speeds of up to 100 meters per minute, meeting 5–8 GWh per line requirements.

Scope of Report on Mixing Equipment Market For Battery Manufacturing

Mixing equipment plays a crucial role in battery manufacturing processes, particularly in the production of lithium-ion batteries. The mixing of various components, such as electrode materials, binders, solvents, and additives, is essential to ensure the homogeneity and consistency of the battery materials.

The Mixing Equipment Market for Battery Manufacturing Market is segmented into mixer type, capacity, battery chemistry, end-use application, and geography. By mixer type, the market is segmented into planetary mixers, dual-shaft dispersers, solid-state low-shear planetary, high-speed wet mixers, dry powder ribbon blenders, and continuous inline mixers. By capacity, the market is segmented into below 200L, 200–1,000L, 1,000–5,000L, and above 5,000L. By battery chemistry, the market is segmented into LFP, NMC-811, solid-state/sulfide, and other battery chemistries. By end-use application, the market is segmented into EV passenger vehicles, commercial EVs, consumer electronics, stationary storage, and R&D lines. The report also covers the market size and forecasts for the mixing equipment market for battery manufacturing market across major regions, including North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Planetary Mixers |

| Dual-shaft Dispersers |

| High-speed Stirring Wet Mixers |

| Dry Powder Ribbon Blenders |

| Continuous Inline Mixers |

| Solid-state Low-shear Planetary |

| Less Than 200 L |

| 200 – 1 000 L |

| 1 000 – 5 000 L |

| Greater Than 5 000 L |

| LFP |

| NMC-811 & Higher Ni |

| Solid-State / Sulfide |

| Others (LTO, Na-ion) |

| Electric Passenger Vehicles |

| Commercial EV & Off-highway |

| Consumer Electronics |

| Stationary Energy Storage |

| R&D / Pilot Lines |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Nordic Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Nigeria | |

| Egypt | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America |

| By Mixer Type | Planetary Mixers | |

| Dual-shaft Dispersers | ||

| High-speed Stirring Wet Mixers | ||

| Dry Powder Ribbon Blenders | ||

| Continuous Inline Mixers | ||

| Solid-state Low-shear Planetary | ||

| By Capacity Rating | Less Than 200 L | |

| 200 – 1 000 L | ||

| 1 000 – 5 000 L | ||

| Greater Than 5 000 L | ||

| By Battery Chemistry Served | LFP | |

| NMC-811 & Higher Ni | ||

| Solid-State / Sulfide | ||

| Others (LTO, Na-ion) | ||

| By End-use Application | Electric Passenger Vehicles | |

| Commercial EV & Off-highway | ||

| Consumer Electronics | ||

| Stationary Energy Storage | ||

| R&D / Pilot Lines | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Nordic Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Nigeria | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the battery mixing equipment space by 2031?

It is forecast to reach USD 7.19 billion by 2031, rising from USD 2.76 billion in 2026 at a 21.1% CAGR over 2026-2031.

Which mixer type leads battery slurry preparation demand?

Planetary mixers led in 2025 with 34.8% revenue share because they remain the most established platform for anode and cathode slurry preparation across major chemistries.

Which application is growing the fastest in battery manufacturing equipment demand?

Stationary energy storage is the fastest-growing application, with a projected 27.1% CAGR through 2031 as large grid-scale battery projects expand.

Which battery chemistry creates the largest installed equipment demand today?

LFP is the largest chemistry served, with 46.5% of 2025 demand, supported by broad use in EVs and utility-scale storage.

Why are advanced slurry mixers priced above standard systems?

Higher-value systems support tighter vacuum control, better temperature management, inert processing, and more stable slurry quality, which becomes critical for high-nickel and solid-state battery lines.

Which region offers the strongest growth outlook through 2031?

North America has the fastest forecast growth at 26.4% CAGR, driven by the large post-IRA pipeline of battery cell plants and related equipment procurement.

Page last updated on: