Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 26.76 Billion |

| Market Size (2031) | USD 38.05 Billion |

| Growth Rate (2026 - 2031) | 7.29% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Defense Market Analysis by Mordor Intelligence

The United Kingdom defense market size reached USD 26.76 billion in 2026 and is forecasted to climb to USD 38.05 billion by 2031, registering a 7.29% CAGR over the period. A legislated floor of 2.6% of GDP for defense outlays by 2027, the Procurement Act 2023’s 40% cut in bid-cycle time, and fresh National Wealth Fund co-investment collectively accelerate contract flow and shorten cash-conversion cycles for suppliers. Strategic mega-programs such as Dreadnought, GCAP, and SSN-AUKUS dominate capital allocations. At the same time, a GBP 6 billion (USD 8.09 billion) munitions line and a GBP 968 million (USD 1.31 billion) space-communications package broaden the opportunity set. At the same time, a GBP 16.9 billion (USD 22.76 billion) Equipment Plan gap, binding yard and energetics capacity constraints, and a shortage of more than 20,000 cleared engineers pose execution risk. Export success, valued at USD 8.5 billion in 2023, partially offsets those structural headwinds by reducing unit costs through shared non-recurring engineering.

Key Report Takeaways

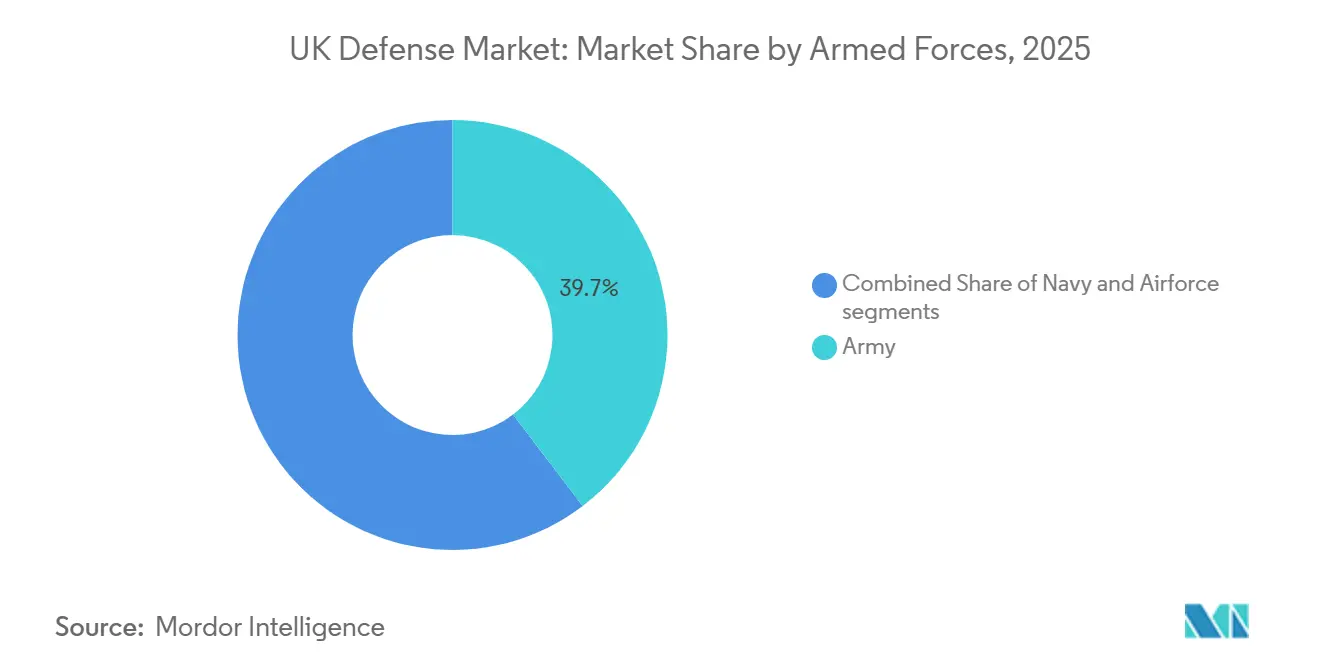

- By armed forces, the Army led with 39.65% revenue share in 2025, while the Navy is projected to grow at an 8.50% CAGR to 2031.

- By type, C4ISR and EW accounted for 29.76% of 2025 spending; unmanned systems are expected to expand at a 9.38% CAGR through 2031.

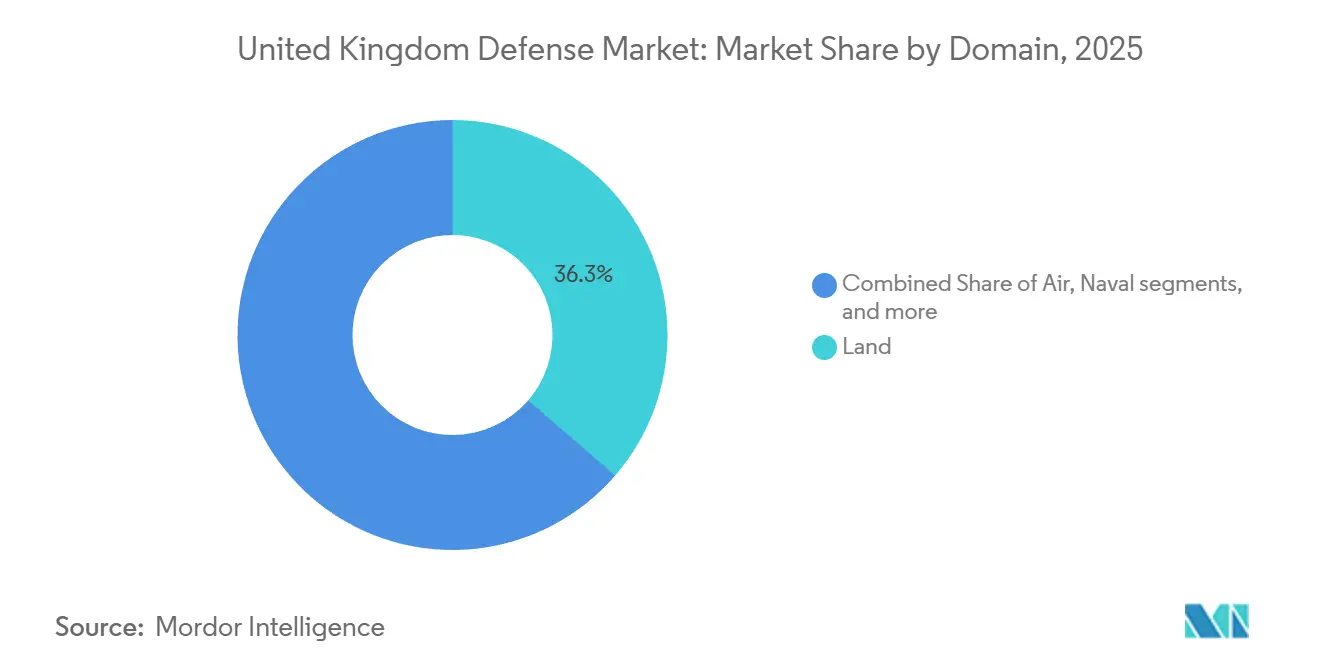

- By domain, land captured 36.34% of 2025 expenditure, whereas space is forecasted to advance at a 10.89% CAGR to 2031.

- By procurement nature, foreign procurement accounted for 56.87% of 2025 outlays; indigenous production is expected to rise at a 9.93% CAGR on the strength of the National Wealth Fund backing.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Defense Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustained budget growth to 2.6% GDP target | +1.8% | National, concentration in England | Medium term (2–4 years) |

| Strategic mega-programmes (Dreadnought, GCAP, SSN-AUKUS) | +2.1% | National with spillover to Japan, Italy, Australia | Long term (≥ 4 years) |

| Post-Ukraine munitions surge and stockpile rebuild | +1.2% | National, energetics clusters in Northwest and Scotland | Short term (≤ 2 years) |

| NATO integration and export-lead deals | +0.9% | Global, priority in Middle East and Southeast Asia | Medium term (2–4 years) |

| Procurement Act 2023 fast-track contracting | +0.6% | National | Short term (≤ 2 years) |

| National Wealth Fund co-investment in defense clusters | +0.7% | National, focus on Northwest, Scotland, Wales | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustained Budget Growth to 2.6 % GDP Target

Parliament’s binding commitment to a 2.6% of GDP defense floor delivers predictable multi-year cash flows that underpin long-lead capital programs. The Spring Budget 2025 injected an additional GBP 5 billion (USD 6.47 billion) for 2025-26 and lifted the Capital Departmental Expenditure Limits (DEL) to GBP 33.2 billion (USD 42.94 billion) by 2029-30, assuring suppliers of steady order books.[1]UK Government, “Spring Budget 2025,” GOV.UK Nevertheless, earmarking GBP 15 billion (USD 20.26 billion) for the warhead enterprise and GBP 6 billion (USD 8.14 billion) for munitions leaves less than GBP 12 billion (USD 16.29 billion) a year for all remaining capital needs, forcing trade-offs among maritime, land, and air projects. A parallel GBP 11 billion (USD 14.81 billion) “Invest” budget, managed by the National Armaments Director, accelerates urgent purchases but fragments long-range platform planning. Vendors able to toggle between conventional competitions and rapid-capability insertions stand to capture disproportionate share, while primes locked into rigid work-share models face margin pressure when inflation outpaces indexation.

Strategic Mega-Programmes (Dreadnought, GCAP, SSN-AUKUS)

The GBP 31 billion (USD 41.16 billion) Dreadnought program, along with a GBP 10 billion (USD 13.28 billion) contingency, anchors naval spending through the 2030s. SSN-AUKUS involves the addition of up to 12 attack submarines, with Australia contributing GBP 2.4 billion (USD 3.05 billion) that effectively subsidizes the upgrades at the Barrow yard, as per the Australian Department of Defence. GCAP distributes design authority across three nations, reducing the UK's work share but providing access to Japanese radar and propulsion funding that exceeds domestic reach. Combined, these programs absorb more than 40% of the equipment budget, crowding out mid-tier needs such as land-based air defense and tactical transport when overruns occur.

Post-Ukraine Munitions Surge and Stockpile Rebuild

The Strategic Defence Review 2025 allocates £6 billion to replenish stocks after the Ukraine conflict revealed higher-than-planned burn rates.[2]UK Ministry of Defence, “Strategic Defence Review 2025,” GOV.UK BAE Systems' Glascoed expansion is expected to triple the facility's energetics output by 2028; however, the facility remains below NATO's revised targets until the full rate is achieved. Interim imports from the United States and France inflate costs by roughly 25%. Semiconductor shortages at MBDA's Bolton line have stretched precision-missile lead times to 30 months, prompting the MoD to pre-fund long-lead components and shifting working-capital burdens from suppliers back to the department.

NATO Integration and Export-Lead Deals

Exports reached USD 8.5 billion in 2023, driven by the sale of Type 31 frigates and Typhoon upgrades to Gulf and Southeast Asian markets. Each additional Type 31 hull reduces domestic unit cost by around 8% owing to shared non-recurring engineering. AUKUS clauses now allow UK firms to bid for Australian and US work without prior foreign-ownership waivers, exposing suppliers to a combined AUD 368 billion (USD 240.34 billion) surface-combatant pipeline. To convert that pipeline, the Defence and Security Exports team has embedded liaison officers in Riyadh, Abu Dhabi, and Jakarta to pre-clear licenses, thereby compressing approval timelines from 18 months to less than six months.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substantial Equipment Plan funding shortfall | –1.4% | National | Long term (≥ 4 years) |

| Shipyard and energetics inflation/capacity constraints | –1.1% | National, focused on Barrow, Rosyth, Glascoed | Medium term (2–4 years) |

| Net-zero compliance costs on legacy platforms | –0.6% | National | Long term (≥ 4 years) |

| Acute digital and nuclear skills shortages | –0.9% | National, acute in Northwest England and Scotland | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Substantial Equipment Plan Funding Shortfall

The National Audit Office flags an affordability gap across 2023-33, squeezing mid-tier capabilities while flagship programs remain protected.[3]National Audit Office, “The Equipment Plan 2023-2033,” nao.org.uk The MoD now sequences major projects, delaying Type 83 design until Type 26 production stabilizes and capping Challenger 3 at 148 tanks. This sequencing reduces concurrency risk but leaves a capability “valley of death” between 2027 and 2030, during which Warrior IFVs and Puma helicopters exceed out-of-service dates with no funded replacements.

Shipyard and Energetics Inflation/Capacity Constraints

Barrow runs at full throughput on Dreadnought and Astute, leaving no slot for SSN-AUKUS until 2028. Rosyth faces 12% yearly labor-cost inflation as welders migrate to offshore wind projects, compressing Babcock’s marine margin to 4%. Interim energetics capacity trails NATO targets by 40%, forcing premium-priced imports and eroding the MoD’s purchasing power.

Segment Analysis

By Armed Forces: Naval Expansion Outpaces Land Dominance

The Navy accounts for a smaller slice today, yet its 8.50% CAGR through 2031 will narrow the gap with the Army’s 39.65% 2025 share, thanks to Dreadnought and SSN-AUKUS boats entering service. This lift places a rising floor under the United Kingdom defense market size for maritime assets. Surface-combatant momentum continues as eight Type 26 and five Type 31 frigates progress in build, while Type 83 destroyer design starts in 2028.[4]BAE Systems, “Type 26 Frigate,” baesystems.com

Sustainment reshuffles budgets. The Ajax vehicle program’s delays illustrate risk transfer to primes; only 26 units were fielded by early 2025 after vibration fixes, denting confidence in land-platform timelines. Conversely, the on-time delivery of autonomous minehunters demonstrates how modular, off-the-shelf kits can mitigate risk. Naval priorities enjoy cross-party backing, insulating them from cuts to the Equipment Plan, while land programs face recurring affordability reviews. As such, maritime growth underwrites a larger portion of the United Kingdom defense market share in the out-years.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Type: Unmanned Systems Surge as C4ISR Holds Largest Share

C4ISR and EW retained 29.76% of 2025 spending, anchoring the United Kingdom defense market size for information-dominance systems. Yet, unmanned systems will register the fastest growth rate of 9.38%, propelled by the Protector RG Mk1, autonomous mine-countermeasure (MCM) vessels, and small tactical drones. Lead times for precision munitions are widening as the semiconductor supply tightens, so integrated drone-sensor packages are gaining favor due to their cost-per-effect metrics.

Vehicles lag, constrained by Ajax uncertainty and capped Challenger 3 numbers, while GBP 6 billion (USD 8.09 billion) in munitions cash revives energetics and missile plants. Space and Cyber lines gain momentum around Skynet 6A and the 2025 Cyber Strategy, underscoring a pivot toward multi-domain, integrated fires. Simulation-based training offsets flat personal-protection budgets, reinforcing the MoD’s preference for collective over individual capability.

By Domain: Space Leads Growth While Land Retains Largest Share

Land still accounts for 36.34% of 2025 outlays, while space rises at a 10.89% CAGR as Project Minerva and Skynet 6A move forward. These gains boost the United Kingdom defense market share for orbital assets. Air spending remains significant through GCAP and F-35B orders, although it competes with submarine bills for capital allocations. Cyber, the smallest slice, grows as electronic-attack pods for Typhoon and F-35B come online, contingent on cleared talent.

As Space and naval line items grow faster than land-based ones, the overall portfolio mix shifts toward precision reach over mass. Manpower cuts in the Future Soldier plan redirect savings into cyber and intelligence, but leave brigade readiness thin as the MoD experiments with reserve cyber units, supported by GCHQ and QinetiQ, to plug skills gaps.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Procurement Nature: Indigenous Production Gains Momentum

Foreign procurement accounted for 56.87% of 2025 outlays, driven by the F-35B; however, indigenous production is forecasted to rise at a 9.93% CAGR to 2031, as the National Wealth Fund subsidizes local yards and energetics. The MoD aims to achieve 60% domestic content by value by 2030, up from 52% in 2024. This pivot broadens the national defense industry base and gradually lifts the local portion of the United Kingdom defense market size.

Domestic scaling faces talent and cost headwinds: the aerospace supply chain lost 15% of its workforce during the pandemic. The F-35's global volume continues to offer cost advantages. Hence, the MoD balances sovereignty and value by localizing long-life platforms, such as submarines and frigates, while importing shorter-cycle kits, like precision weapons.

Geography Analysis

The United Kingdom defense market clusters around distinct regional hubs. Northwest England hosts Barrow-in-Furness submarines and Glascoed energetics, accounting for roughly one-third of defense manufacturing jobs and anchoring future SSN-AUKUS work. Scotland's Rosyth and Edinburgh sites capture about 20% of the spend, but rising labor costs linked to offshore wind demand are compressing margins. Southeast England houses C4ISR and cyber specialists near the Abbey Wood procurement hub, cutting travel costs and time for negotiations.

Wales expands its role through mandated co-investment in the National Wealth Fund, which necessitates the establishment of a South Wales satellite facility, resulting in the addition of 500 jobs. Northern Ireland is being re-integrated through Leonardo's Belfast cyber center and Spirit AeroSystems' composites plant, which supplies F-35 wings. The geographic spread aligns with the "leveling-up" policy, channeling work toward regions with higher unemployment rates.

Exports influence domestic economics. Gulf buyers account for 40% of the nation's defense exports, sharing engineering costs on the Typhoon and Paveway lines. Southeast Asia orders Type 31 frigates and Protector UAVs, backed by UK Export Finance credit guarantees. AUKUS opens Australian and US markets, and Australia's yard contribution subsidizes Barrow infrastructure, benefiting UK build schedules.

Competitive Landscape

Prime contracts remain oligopolistic. BAE Systems, Babcock International, and Leonardo collectively account for around 60% of the MOD's spend. BAE's vertical integration secures a broad scope, but the Ajax delay demonstrates complexity risks. Babcock's commercial-off-the-shelf strategy on Type 31 accelerates design and attracts exports. Leonardo leverages direct-award privileges to secure helicopter upgrades.

Mid-tier firms exploit niches. QinetiQ's high-power microwave counter-drone project shows how smaller suppliers can win emerging capabilities. MBDA expands Bolton to increase missile output by 50% by 2027, despite semiconductor shortages. Meanwhile, Thales' Belfast cyber center anchors EW credentials.

AUKUS alignment allows disruptive US entrants, such as Anduril, to bid in autonomy segments, thereby raising competitive intensity. The MOD's sovereign-capability rule favors local final assembly but lifts unit costs by up to 15%. Exports continue to drive scale economies, lowering MOD unit prices on the Type 31 and Typhoon lines, thereby reinforcing the United Kingdom's defense market's global orientation.

United Kingdom Defense Industry Leaders

-

BAE Systems plc

-

Babcock International Group PLC

-

Leonardo S.p.A.

-

QinetiQ Limited

-

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: The UK MoD awarded Thales an initial contract worth GBP 10 million (approximately USD 13.49 million) to provide AI-enabled remote command centers for the Royal Navy's mine countermeasures operations.

- August 2025: Elbit Systems signed a USD 1.6 billion, five-year contract to provide a European customer with advanced defense systems. The agreement includes long-range precision artillery, rocket systems, and unmanned aerial platforms equipped with embedded AI technologies.

United Kingdom Defense Market Report Scope

The United Kingdom defense market study analyzes historical, current, and projected budget allocation and spending patterns. The market encompasses a range of activities, products, and services that support national defense and security requirements. The country's defense strategy focuses on protecting against external and internal threats while safeguarding strategic interests.

The study examines procurement and modernization plans for the UK armed forces. It also covers investments in satellite development and deployment, as well as the research and development of advanced technologies, including directed energy weapons (DEWs), hypersonic missiles, unmanned systems, advanced composites, and advanced manufacturing technologies such as 3D printing.

The United Kingdom defense market is segmented by armed forces, type, domain, and procurement nature. By armed forces, the market is segmented into the air force, the army, and the navy. By type, the market is segmented into personnel training and protection, C4ISR and electronic warfare, vehicles, weapons and ammunition, unmanned systems, and space and cyber systems. By domain, the market is segmented into land, air, naval, space, and cyber and electromagnetic spectrum. By procurement nature, the market is segmented into indigenous production and foreign procurement. The report offers the market size and forecasts in value (USD) for all the above segments.

By Armed Forces

| Air Force |

| Army |

| Navy |

By Type

| Personnel Training and Protection |

| C4ISR and Electronic Warfare (EW) |

| Vehicles |

| Weapons and Ammunition |

| Unmanned Systems |

| Space and Cyber Systems |

By Domain

| Land |

| Air |

| Naval |

| Space |

| Cyber and Electromagnetic Spectrum |

By Procurement Nature

| Indigenous Production |

| Foreign Procurement |

| By Armed Forces | Air Force |

| Army | |

| Navy | |

| By Type | Personnel Training and Protection |

| C4ISR and Electronic Warfare (EW) | |

| Vehicles | |

| Weapons and Ammunition | |

| Unmanned Systems | |

| Space and Cyber Systems | |

| By Domain | Land |

| Air | |

| Naval | |

| Space | |

| Cyber and Electromagnetic Spectrum | |

| By Procurement Nature | Indigenous Production |

| Foreign Procurement |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the United Kingdom defense market in 2026 and where is it headed by 2031?

It stands at USD 26.76 billion in 2026 and is projected to reach USD 38.05 billion by 2031 on a 7.29% CAGR.

Which segment is expanding fastest through 2031?

Naval programs, powered by Dreadnought and SSN-AUKUS, are forecast to grow at an 8.50% CAGR, the quickest among Armed Forces segments.

How does the Procurement Act 2023 affect suppliers?

The Act cuts bid-cycle time by up to 40%, favors firms with security clearances for direct awards, and imposes quarterly performance audits that shift delivery risk to contractors.

What drives the surge in unmanned systems spending?

Protector RG Mk1 drones, autonomous minehunters, and tactical reconnaissance UAVs together underpin a 9.38% CAGR for Unmanned Systems through 2031.

Which regions gain most from defense spending?

Northwest England and Scotland capture the bulk of naval and energetics work, while Southeast England leads in C4ISR and cyber activity.

Why is indigenous production rising despite higher costs?

A GBP 7 billion (USD 9.43 billion) National Wealth Fund and new sovereign-capability rules aim to raise domestic content to 60% by 2030, trading some cost efficiency for supply-chain resilience.

Page last updated on: