Ultracapacitor Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 4.78 Billion |

| Market Size (2031) | USD 9.22 Billion |

| Growth Rate (2026 - 2031) | 14.05% CAGR |

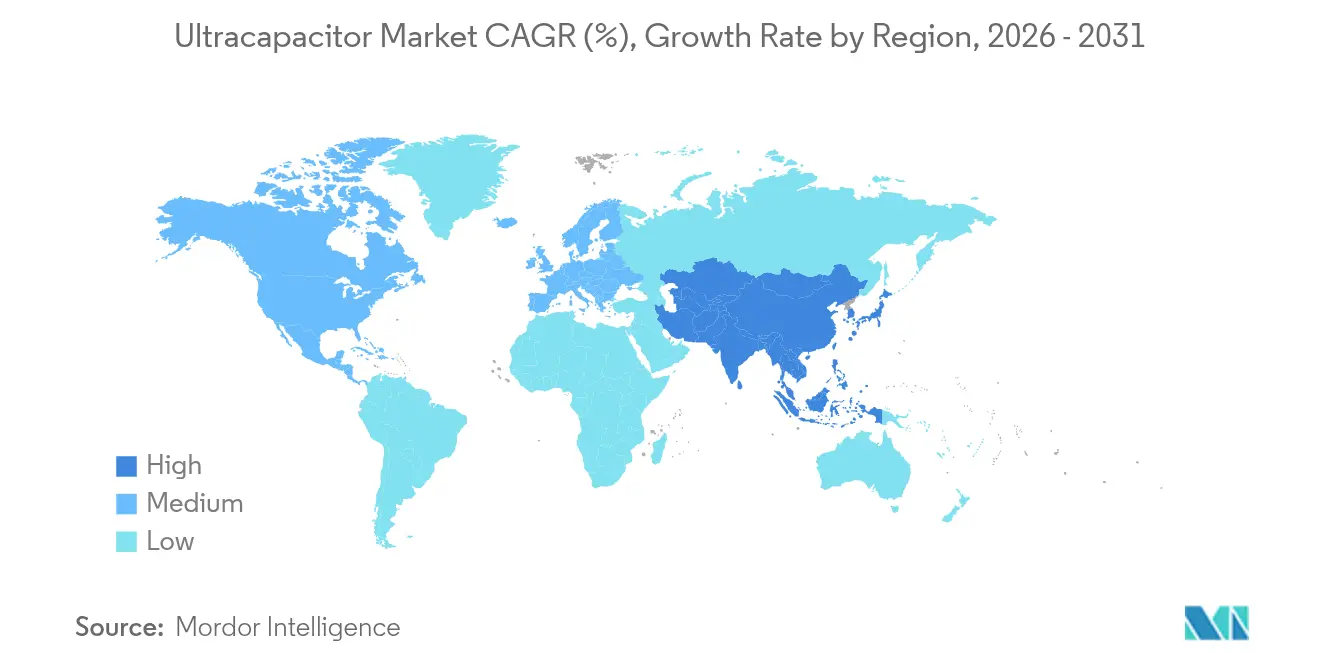

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ultracapacitor Market Analysis by Mordor Intelligence

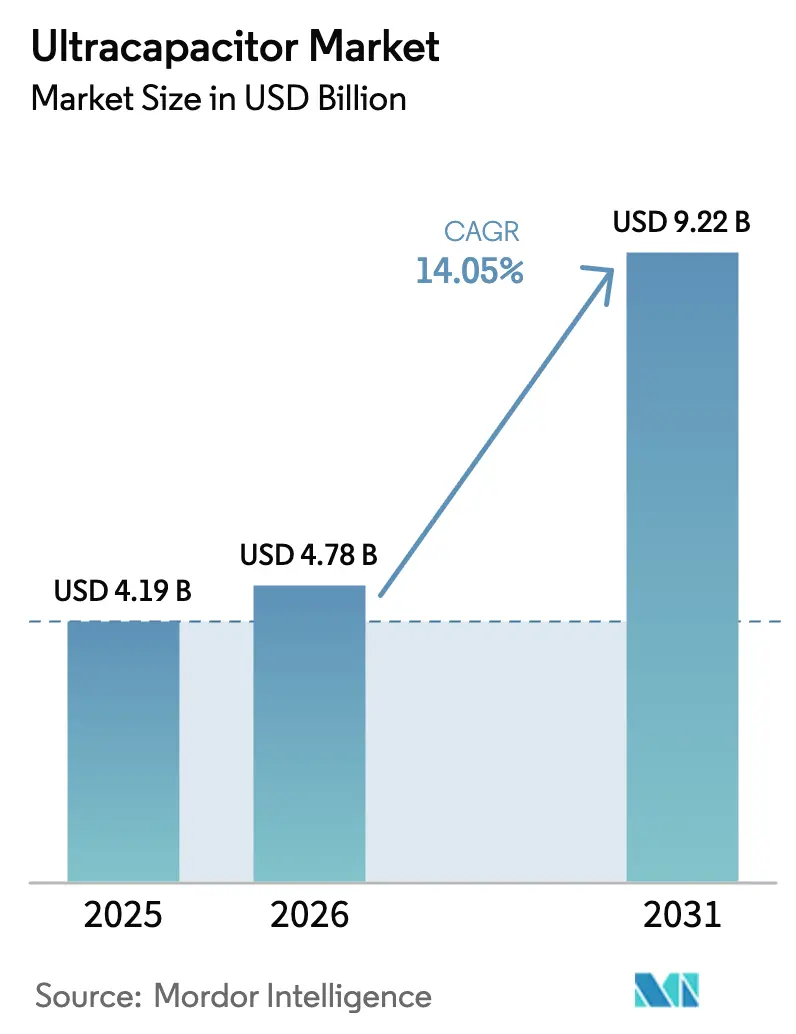

The Ultracapacitor Market size was valued at USD 4.19 billion in 2025 and estimated to grow from USD 4.78 billion in 2026 to reach USD 9.22 billion by 2031, at a CAGR of 14.05% during the forecast period (2026-2031).

This growth reflects the technology’s proven ability to deliver million-cycle durability and instantaneous power bursts that conventional batteries cannot match. Strong demand arrives from electric-vehicle regenerative braking, grid frequency regulation, and industrial automation, all of which require rapid charge–discharge performance. Manufacturers are scaling automated production lines, integrating proprietary electrode materials, and forming hybrid storage architectures that pair ultracapacitors with lithium-ion batteries. These moves shorten payback periods, reduce maintenance costs, and position the ultracapacitor market for expanded penetration across transportation, energy, and manufacturing sectors.

Key Report Takeaways

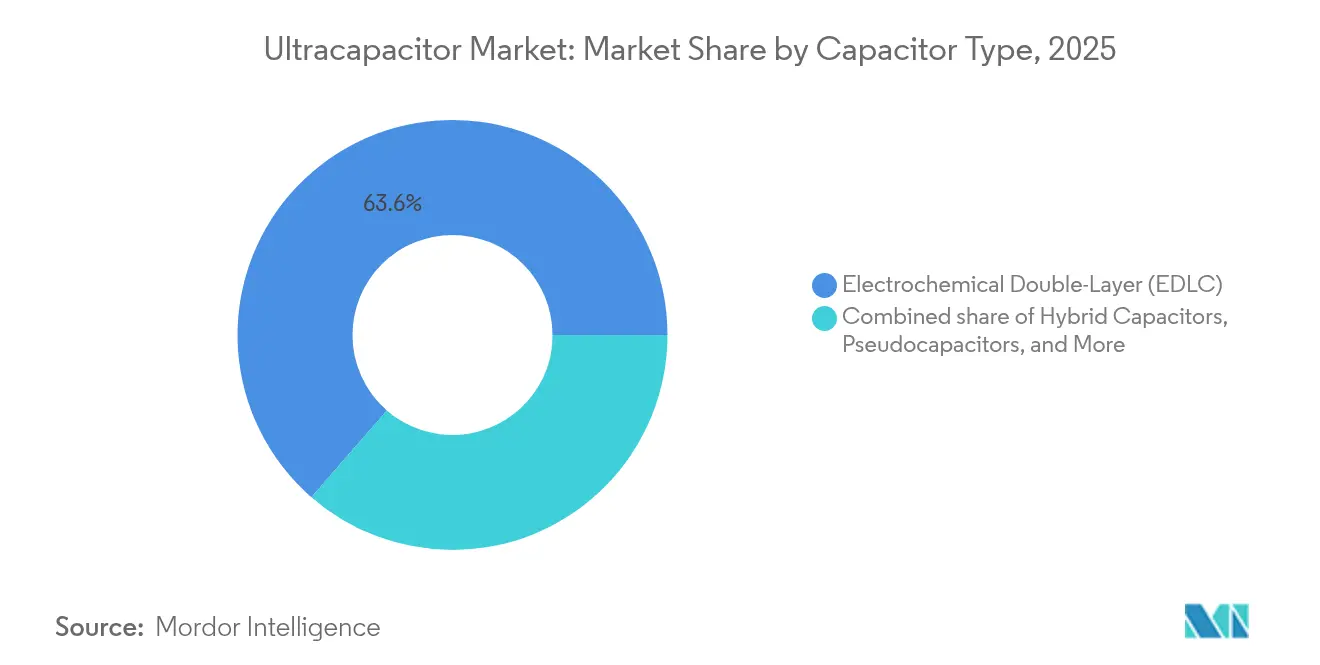

- By capacitor type, Electrochemical Double-Layer Capacitors held 63.60% of the ultracapacitor market share in 2025, while Hybrid Capacitors are projected to post a 19.50% CAGR through 2031.

- By module voltage rating, the 25-50 V segment accounted for 37.15% of the ultracapacitor market size in 2025, whereas 50-100 V modules are set to grow at a 17.35% CAGR.

- By electrode material, activated-carbon electrodes led with a 69.85% ultracapacitor market share in 2025; graphene materials are forecasted to expand at a 25.32% CAGR to 2031.

- By end-use industry, the automotive and transportation sector captured a 36.45% revenue share in 2025, while industrial equipment is on track for the highest 16.95% CAGR through 2031.

- By geography, the Asia-Pacific region commanded 44.05% of the ultracapacitor market in 2025 and is anticipated to remain the fastest-growing region, with a 15.25% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ultracapacitor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV demand surge | 3.20% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Renewable grid integration | 2.80% | Global, particularly Europe and APAC | Long term (≥ 4 years) |

| Electrode material advances | 2.10% | Global, R&D concentrated in North America and Europe | Long term (≥ 4 years) |

| Wind-turbine pitch retrofit boom | 1.90% | Europe and North America, expanding to APAC | Medium term (2-4 years) |

| Industrial-robot KERS adoption | 1.60% | APAC core, spill-over to Europe and North America | Medium term (2-4 years) |

| Rail electrification incentives | 1.40% | Europe and APAC, selective North American corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EV demand surge

Growing electric-vehicle sales generate unprecedented demand for ultracapacitor modules within regenerative braking and hybrid energy storage systems. Skeleton Technologies’ deployment in the NTT IndyCar Series demonstrated a 60-horsepower boost delivered in 4.5-second cycles, validating peak-power capability at scale. Vehicle architectures are migrating toward 800 V platforms, a voltage range that aligns well with ultracapacitors’ low internal resistance and rapid power throughput. Automakers are increasingly specifying hybrid packs that allocate transients to ultracapacitors while reserving sustained discharge for batteries, which extends battery life and enhances overall drivetrain efficiency.

Renewable grid integration

Utility operators require sub-second response to balance variable solar and wind output. China Huaneng Group’s 5 MW supercapacitor system at Luoyuan Power Plant demonstrated a 14 times faster frequency-regulation response than legacy solutions. Siemens Energy’s E-STATCOM platform achieves 75 MW cycling capability for up to two decades, offering both active and reactive power support.[1]Genkina, Dina, "Will Supercapacitors Come to AI's Rescue?," spectrum.ieee.org2671883490. European transmission operators have begun standardizing ultracapacitor components in wind farm interconnections, citing cycling lifetimes that outlast those of lithium-ion alternatives and reduce lifecycle costs.

Electrode material advances

R&D teams are closing the historical energy-density gap using new nanostructured carbons. CAP-XX and Ionic Industries are industrializing reduced graphene oxide designs that aim to approach lead-acid battery energy density without sacrificing ultracapacitor power delivery. University of Houston researchers have recorded an energy density of 75 J/cm³ with two-dimensional materials, the highest value yet achieved for polymer dielectrics. Scaling these laboratory breakthroughs into automated mass production remains the primary hurdle, but it promises to broaden ultracapacitor applicability into longer-duration roles.

Rail electrification incentives

Electrified rail corridors demand energy-buffering solutions for regenerative braking, voltage stabilization, and station powering. Policy programs in Europe and Asia allocate public funds toward energy recovery installations that include ultracapacitor banks, citing a 30% lower lifecycle cost compared to battery-only options.[2]European Railway Agency, “Energy Storage in Rail Electrification,” era.europa.eu Long-term prospects are tied to infrastructure upgrades expected through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High $/Wh vs Li-ion | -2.40% | Global, most pronounced in cost-sensitive applications | Short term (≤ 2 years) |

| Low energy density | -1.80% | Global, limiting long-duration storage applications | Medium term (2-4 years) |

| Activated-carbon supply squeeze | -1.20% | Global, with supply concentrated in Asia | Short term (≤ 2 years) |

| Absence of harmonised safety codes | -0.90% | Global, regulatory fragmentation across regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High $/Wh versus Li-ion

Although ultracapacitor modules excel in power delivery, their USD/kilowatt-hour price remains well above commodity battery packs. The U.S. Department of Energy lists cost reduction as the single biggest barrier to adoption, despite showing total-cost-of-ownership parity in high-cycle infrastructures.[3]U.S. Department of Energy, “Ultracapacitor Roadmap 2025,” energy.gov Eaton’s analysis of data-center UPS retrofits finds that eliminating battery replacement cycles offsets the higher upfront cost within five years. Suppliers, therefore, focus on automation and low-cost carbon sources to compress capital expenditures over the next two years.

Absence of harmonised safety codes

Regional certification frameworks vary, resulting in redundant testing and increased compliance costs. Industry bodies advocate for alignment with IEC 62391, but full harmonization is likely to take several years, which will weigh slightly on ultracapacitor market growth in regulated verticals.[4]IEC, “Standard 62391 Overview,” iec.ch

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacitor Type: Hybrid formats outpace entrenched EDLCs

Electrochemical Double-Layer Capacitors accounted for 63.60% of the ultracapacitor market share in 2025 and remain essential for automotive and industrial power buffering. Hybrid Capacitors, however, are projected to clock a 19.50% CAGR to 2031, an outcome driven by their ability to narrow the energy-density gap with batteries without eroding cycling durability. The ultracapacitor market size tied to hybrid formats is therefore poised to double current revenue by the decade’s end.

Pseudocapacitors and lithium-ion capacitors fulfil niche roles where unique electrochemical signatures are required, such as avionics backup and telecom rectifiers. Skeleton Technologies’ EUR 600 million SuperBattery facility highlights how hybrid architectures combine the best of lithium-ion and supercapacitor science to address both energy and power needs within a single, modular housing.

By Module Voltage Rating: Mid-range dominance meets rising 800 V demand

Modules rated 25-50 V secured 37.15% of the ultracapacitor market in 2025, serving today’s 48 V mild-hybrid vehicles and a multitude of industrial drives. Yet, modules in the 50-100 V band are forecast to grow at a 17.35% CAGR as automakers migrate to 800 V propulsion stacks and grid designers call for higher-voltage buffers. The ultracapacitor market size associated with this range will expand the fastest, reflecting system designs that lower current requirements and wiring mass.

Consumer electronics continue to specify sub-25 V parts for camera flashes and IoT power-fail bridges, whereas modules with voltages above 100 V address applications such as crane lifts, rail substations, and STATCOM platforms. Maxwell Technologies’ 3.0 V cell architecture reduces series count per pack, improving serviceability and elevating permissible ambient temperatures.

By Electrode Material: Graphene emerges from R&D into production

Activated carbon accounted for 69.85% of the ultracapacitor market share in 2025, driven by its cost efficiency and maturity. Still, graphene and curved-graphene variants are poised for a 25.32% CAGR, driven by their superior conductivity and tunable porosity, which enhance both power and energy performance. This shift will reshape future allocations of the ultracapacitor market size between legacy and next-generation materials.

Metal-oxide and conducting-polymer electrodes serve lower-volume medical devices and flexible electronics segments, where form factor outranks cost. SGL Carbon recorded a 10.4% revenue jump in specialty graphite, driven partly by energy-storage customers, signaling upstream momentum in advanced carbon supply chains.

By End-use Industry: Industrial equipment accelerates past automotive reliance

The automotive and transportation sector held 36.45% of the ultracapacitor market revenue in 2025, as regenerative braking integration became standard in hybrid powertrains. Industrial equipment, however, is expected to record the fastest 16.95% CAGR through 2031, driven by robotics, lifting machinery, and manufacturing line retrofits that harness braking energy. The ultracapacitor market size associated with industrial deployments will therefore diversify revenue streams away from cyclical vehicle volumes.

Consumer electronics maintain a stable demand for backup power, while the energy and power sector leans on ultracapacitors for grid inertia and voltage support. The aerospace, defense, and medical segments remain smaller yet vital niches that emphasize unmatched reliability and extended cycle life.

Geography Analysis

Asia-Pacific captured 44.05% of the ultracapacitor market share in 2025 and is projected to sustain a 15.25% CAGR through 2031. China’s commissioning of the 5 MW Luoyuan supercapacitor station illustrates policy-backed infrastructure scaling. Japan’s electronics leaders leverage decades of capacitor expertise, while South Korean conglomerates extend stack solutions into stationary storage. Early adoption of hybrid energy storage systems, ample manufacturing capacity, and supportive EV subsidies combine to cement regional leadership.

North America ranks second in revenue, anchored by technology innovation and grid modernization. Department of Energy programs aim to reduce costs and incentivize domestic manufacturing, projecting that ultracapacitor deployment will increase from USD 1.5 billion in 2021 to USD 15 billion by 2030. Canada leverages the cold-temperature resilience of ultracapacitors for remote microgrids, while Mexico’s expanding automotive supply chain creates new demand pockets.

Europe emphasizes sustainability and regulatory drivers. Skeleton Technologies’ turbine-pitch contracts and EU directives banning lead-acid in renewables spur ultracapacitor retrofits. Germany’s industrial automation firms are adding ultracapacitor energy-recovery modules to press lines, and Nordic utilities are embedding supercapacitors in high-renewable grids to stabilize frequency. The region’s circular economy focus favors the long service life and recyclability advantages of ultracapacitors.

Competitive Landscape

The ultracapacitor market is moderately fragmented. European pioneers, such as Skeleton Technologies, compete with Maxwell Technologies (now under Tesla), CAP-XX, and a range of cost-focused Asian producers. Competitive differentiation is based on patented electrode chemistries, automated production flows, and application-specific packaging integration.

Skeleton Technologies has invested EUR 600 million in a French SuperBattery plant, scheduled to start up in 2027, marking one of the sector’s largest capacity expansions. Tesla leverages Maxwell’s dry-electrode expertise to enhance battery lines, underscoring the strategic interplay between ultracapacitor and lithium-ion roadmaps.

Middle-tier suppliers pursue vertical integration, offering turnkey modules for wind, rail, and industrial robots. Supply-chain constraints in activated carbon and a pivot toward graphene open windows for newcomers that secure raw material diversification or license advanced carbon processes. Over the forecast horizon, intellectual-property depth, warranty cycle-life guarantees, and the ability to serve both automotive and grid accounts will define market share trajectories.

Ultracapacitor Industry Leaders

-

Skeleton Technologies

-

Maxwell Technologies

-

LS Mtron

-

Panasonic Corporation

-

Eaton Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Skeleton Technologies has opened an R&D site at LUT University in Finland to accelerate the refinement of SuperBattery chemistry.

- April 2025: CAP-XX and Ionic Industries launched a joint venture targeting graphene-oxide supercapacitors.

- November 2024: Ultralife Corporation acquired Electrochem Solutions for USD 50 million, broadening ultracapacitor capabilities.

- July 2024: Skeleton Technologies deployed supercapacitors in the NTT IndyCar Series hybrid Energy Recovery System.

Global Ultracapacitor Market Report Scope

An ultracapacitor, also known as a supercapacitor or electrochemical capacitor, is an energy storage device that drives the gap between conventional capacitors and rechargeable batteries. It stores energy through the separation of electrical charges in an electrical field, similar to a standard capacitor, but with much higher energy density. Ultracapacitors can charge and discharge rapidly, provide high power output, and have a long lifespan with minimal degradation over many cycles. Unlike batteries, which rely on chemical reactions, ultracapacitors store energy electrostatically, allowing for faster energy transfer.

The study tracks the revenue generated from the sale of ultracapacitors by various manufacturers worldwide. It also tracks the key market parameters, underlying growth influencers, and major manufacturers operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of macroeconomic factors on the market. The report’s scope encompasses market sizing and forecasts for the various market segments.

The ultracapacitor market is segmented by type (electrostatic ultracapacitors, pseudocapacitors, and hybrid capacitors), by end user vertical (automotive and transportation, consumer electronics, energy and power, industrial manufacturing, aerospace and defense, and others), and by geography (North America, Europe, Asia-pacific, Latin America, And Middle East And Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Electrochemical Double-Layer (EDLC) |

| Pseudocapacitors |

| Hybrid Capacitors |

| Lithium-ion Capacitors |

| Up to 25 V |

| 25 to 50 V |

| 50 to 100 V |

| Above 100 V |

| Activated-carbon |

| Graphene/Curved-graphene |

| Metal-oxide |

| Conducting-polymer |

| Automotive and Transportation |

| Consumer Electronics |

| Energy and Power |

| Industrial Equipment |

| Aerospace and Defense |

| Medical Devices |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia & New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Capacitor Type | Electrochemical Double-Layer (EDLC) | |

| Pseudocapacitors | ||

| Hybrid Capacitors | ||

| Lithium-ion Capacitors | ||

| By Module Voltage Rating | Up to 25 V | |

| 25 to 50 V | ||

| 50 to 100 V | ||

| Above 100 V | ||

| By Electrode Material | Activated-carbon | |

| Graphene/Curved-graphene | ||

| Metal-oxide | ||

| Conducting-polymer | ||

| By End-use Industry | Automotive and Transportation | |

| Consumer Electronics | ||

| Energy and Power | ||

| Industrial Equipment | ||

| Aerospace and Defense | ||

| Medical Devices | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia & New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected ultracapacitor market size by 2031?

The ultracapacitor market size is forecast to reach USD 9.22 billion by 2031.

Which capacitor type is growing fastest?

Hybrid Capacitors are projected to grow at a 19.50% CAGR, the fastest among all types.

Which region leads the ultracapacitor market?

Asia-Pacific leads with 44.05% market share in 2025 and is expected to maintain the highest regional CAGR.

What restraint most affects ultracapacitor adoption?

High dollar-per-watt-hour cost versus lithium-ion batteries remains the most significant short-term restraint, though total-cost-of-ownership studies show this gap narrowing.

Why are ultracapacitors used alongside batteries in electric vehicles?

Ultracapacitors handle rapid power bursts for regenerative braking, reducing battery stress and extending battery life.

How are graphene materials influencing ultracapacitor performance?

Graphene electrodes improve conductivity and energy density, enabling next-generation devices that bridge the power–energy gap while preserving cycle life.

Page last updated on: