North America Liquid Hydrogen Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

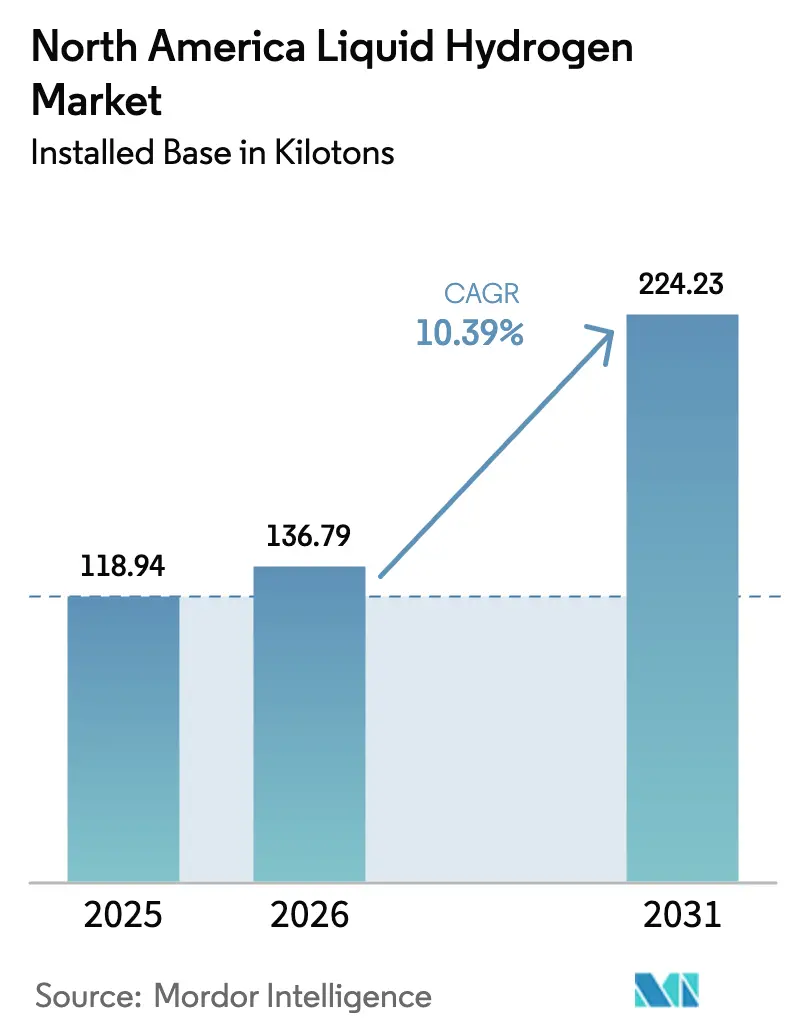

| Base Year Market Size (2025) | 118.94 kilotons |

| Market Volume (2026) | 136.79 kilotons |

| Market Volume (2031) | 224.23 kilotons |

| Growth Rate (2026 - 2031) | 10.39% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Liquid Hydrogen Market Analysis by Mordor Intelligence

The liquid hydrogen market in North America measured 136.79 kilotons in 2026 and is projected to reach 224.23 kilotons by 2031, growing at a 10.39% CAGR; this outlook underscores the market size potential as federal incentives and decarbonization targets widen use beyond aerospace into transport and industrial segments. Liquefaction economics are improving as 45V production tax credits of up to USD 3.00 per kilogram align with regional clean-energy mandates, creating stronger investment cases for both green and blue projects. Commercial fleets in California and Texas are ramping demand by substituting diesel with fuel-cell trucks that capitalize on the higher volumetric density of liquid hydrogen, while micro-bulk delivery models expand access for small and medium industrial users. Robust order books for cryogenic tankers, tube trailers, and super-insulated on-site storage point to sustained equipment sales, yet permitting delays tied to boil-off, routing restrictions, and hazmat ordinances still temper near-term momentum. Competitive dynamics are evolving as gas majors defend their installed base, equipment suppliers pursue vertical integration, and new entrants experiment with on-site liquefaction that could compress merchant margins.

Key Report Takeaways

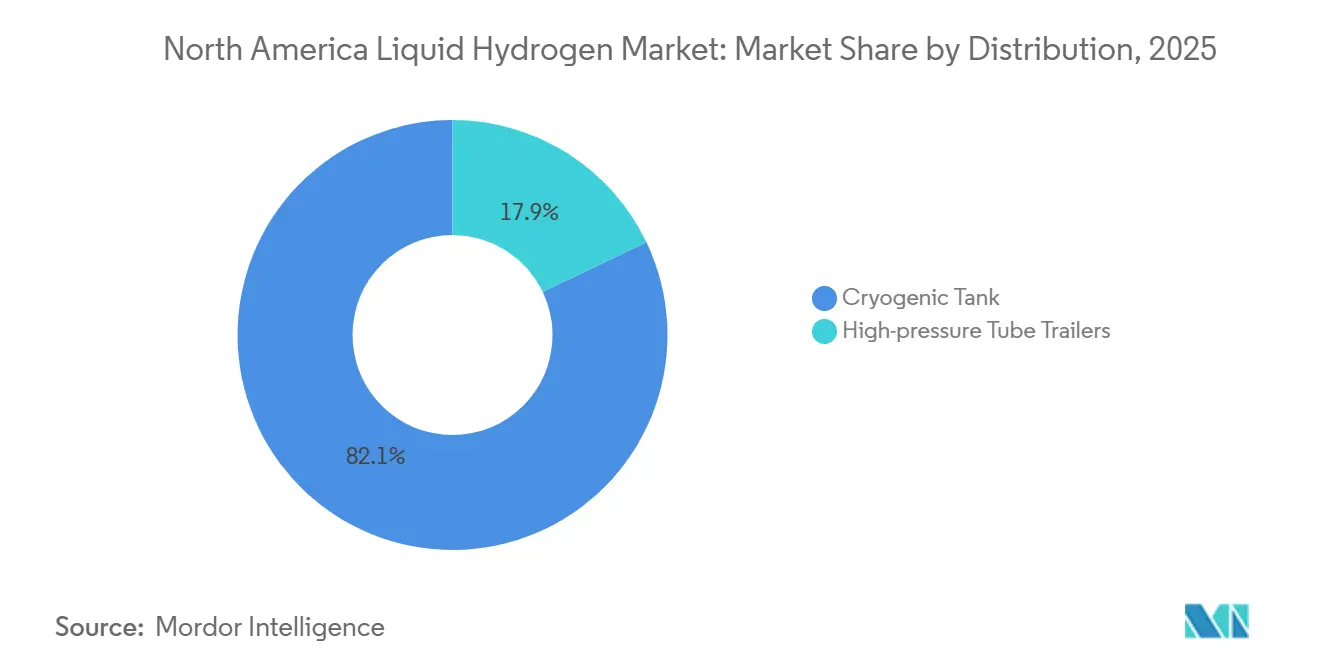

- By distribution, cryogenic tanks commanded 82.1% volume share in 2025, whereas high-pressure tube trailers are forecast to post an 11.6% CAGR to 2031 as micro-bulk models penetrate cost-sensitive users.

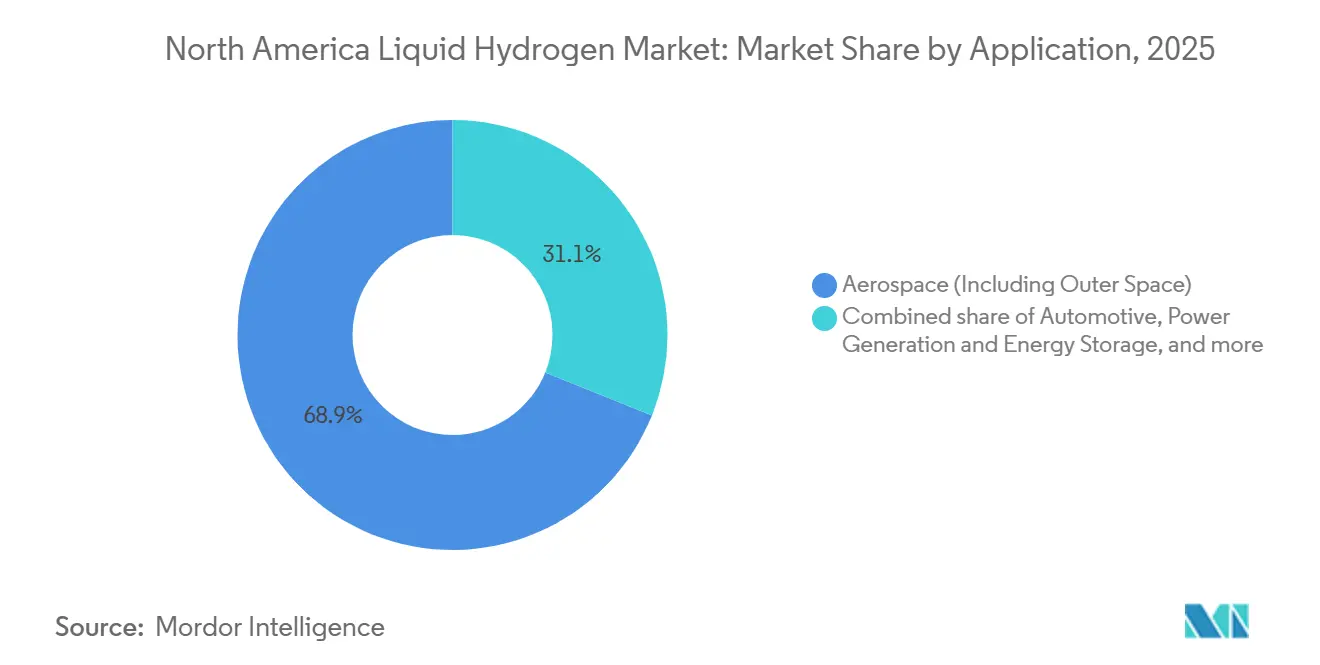

- By application, aerospace dominated with 68.9% share of the liquid hydrogen market size in 2025, but automotive end-use is advancing at an 11.9% CAGR through 2031.

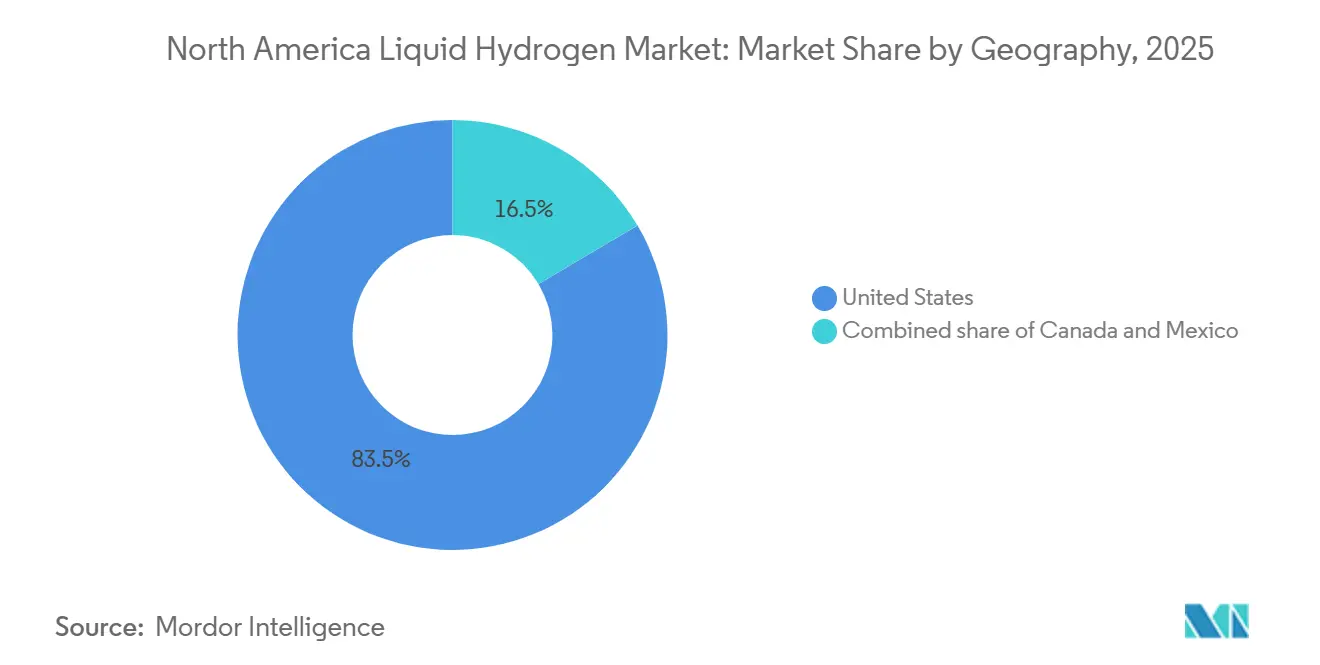

- By geography, the United States held 83.5% of the regional liquid hydrogen market share in 2025 and is expected to expand at a 10.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Liquid Hydrogen Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DOE-funded hydrogen hubs accelerate liquefaction investment | +2.8% | United States, with concentration in Gulf Coast, California, Pacific Northwest | Medium term (2-4 years) |

| Scale-up of Class-8 fuel-cell truck pilots along I-80 & I-5 corridors | +2.3% | United States, primarily California, Nevada, Oregon, Washington | Short term (≤ 2 years) |

| Federal 45V/45Q tax credits compress payback periods for CCUS-based LH₂ | +1.9% | United States, with early uptake in Texas, Louisiana, Wyoming | Medium term (2-4 years) |

| Emergence of "cold ironing" mandates at West-Coast ports | +1.4% | United States (California, Washington ports) | Long term (≥ 4 years) |

| Super-insulated micro-bulk tanks enabling LH₂ deliveries to SME sites | +0.9% | North America, with early gains in industrial clusters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

DOE-Funded Hydrogen Hubs Accelerate Liquefaction Investment

Seven regional clean hydrogen hubs awarded USD 7 billion in federal grants during 2023 are underwriting 50- to 100-ton-per-day liquefaction trains that reach sub-USD 2.50-per-kilogram unit costs and crowd-in private commitments from Air Products, Air Liquide, and other project sponsors.[1]U.S. Department of Energy, “Regional Clean Hydrogen Hubs Fact Sheet,” energy.gov Off-take contracts pooled across transport, industrial, and power customers de-risk utilization and enable developers to secure long-term debt, shortening project payback windows to well under ten years. Gulf Coast and California hubs have already broken ground on liquefaction blocks tied to port and pipeline infrastructure, while the Pacific Northwest hub combines renewable electrolysis with cryogenic storage for aerospace and cross-border exports. Regional specialization also aligns production pathways, blue projects where natural gas and sequestration are abundant, green projects where wind or solar is cheapest, optimizing capital allocation. The resulting infrastructure lattice is expected to anchor contiguous networks of production, storage, and distribution that lower delivered costs and accelerate adoption beyond early niches.

Scale-Up of Class-8 Fuel-Cell Truck Pilots Along I-80 & I-5 Corridors

California’s Advanced Clean Fleets regulation requires new drayage trucks to be zero-emission from 2024 onward, prompting fleet operators to place multi-year orders for liquid hydrogen trucks that deliver 500- to 600-mile range without payload penalties.[2]California Air Resources Board, “Advanced Clean Fleets Regulation,” carb.ca.gov Hyundai, Nikola, and Volvo have collectively deployed more than 200 heavy-duty fuel-cell tractors since 2024, supported by a growing network of refueling stations dispensing cryogenic fuel that is vaporized and compressed on site. The California Energy Commission’s USD 150 million grant program covers up to 50% of station capex, lowering retailer risk during utilization ramp-up. Fleet operators cite rapid fueling times and route flexibility as principal advantages over battery-electric trucks on long-haul lanes. As station density improves, original equipment manufacturers anticipate cost parity with diesel on a total-cost-of-ownership basis by 2028, catalyzing broader adoption across Western and Mountain states.

Federal 45V/45Q Tax Credits Compress Payback Periods for CCUS-Based LH₂

The Internal Revenue Service finalized 45V guidance in late 2023, awarding up to USD 3.00 per kilogram for hydrogen meeting sub-0.45 kg CO₂e lifecycle emissions while permitting stacked 45Q credits of USD 85 per metric ton for captured carbon, jointly reducing levelized costs of blue liquid hydrogen by roughly 35% relative to pre-credit economics.[3]Internal Revenue Service, “Section 45V Credit Guidance,” irs.gov Air Products’ Louisiana project illustrates the upside, monetizing both credits to deliver product at about USD 4.00 per kilogram, competitive with diesel parity for heavy transport. Eligibility rules favor producers who pair new renewable generation or high-capture reformers with sequestration reservoirs, steering investment to resource-rich Gulf Coast, Wyoming, and Alberta basins. The credits sunset after 10 years of production, but tilt early capital flows toward large-scale projects that can be commissioned by 2032, accelerating plant pipeline depth.

Emergence of “Cold Ironing” Mandates at West-Coast Ports

Revised at-berth regulations in California oblige container, reefer, and tanker vessels to eliminate auxiliary emissions within three hours of docking, and Washington ports are moving in lockstep, encouraging adoption of onboard fuel cells supplied by liquid hydrogen bunkering. Linde and Kawasaki have demonstrated pilot bunkering operations that deliver two tons per day using mobile liquefiers, signaling proof of concept for maritime fueling. Vessel owners view cryogenic bunkering as a compliance hedge against looming International Maritime Organization decarbonization milestones, especially for routes unsuitable for shore power connections. Port authorities are incorporating hydrogen into master-plan revisions, allocating quay space for future permanent tanks and safety perimeters. If large-scale bunkering proceeds, incremental demand could approach 20 kilotons annually by 2031, materially lifting regional throughput.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High boil-off losses for <3-t/day storage systems | -1.2% | North America, with acute impact in distributed industrial applications | Short term (≤ 2 years) |

| Limited availability of cryogenic tanker manufacturing capacity | -0.8% | North America, constrained by global supply chain for specialized components | Medium term (2-4 years) |

| County-level hazmat restrictions on LH₂ trucking routes | -0.6% | United States, concentrated in California, New York, New Jersey | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Boil-Off Losses for below 3 t/Day Storage Systems

Small storage tanks exhibit unfavorable surface-area-to-volume ratios that raise daily venting to 1.5%-3.0%, translating into USD 150-USD 300 lost product for a 1 t/day user and imposing costly mitigation requirements such as recovery compressors or active cryocoolers. NFPA 2 spacing rules further complicate installations in dense industrial parks, as vent stacks must lie at least 25 ft from ignition sources.[4]National Fire Protection Association, “NFPA 2 Hydrogen Technologies Code,” nfpa.org However, zero-boil-off pilots promise relief, their USD 0.5-1.0 million price point reserves adoption for mission-critical aerospace programs. Until costs fall, high venting erodes the business case for small-scale users, slowing penetration in fragmented industrial niches.

Limited Availability of Cryogenic Tanker Manufacturing Capacity

North America’s combined build rate for LH₂ road tankers from Chart Industries, Taylor-Wharton, and CIMC ENRIC stood near 500 units per year in 2024, but orders for liquid hydrogen market expansion already exceed planned output, pushing lead times to 18 months. Scarcity stems from specialized aluminum forgings, vacuum-insulated piping, and MC-338 compliance testing bottlenecks. Chart’s USD 50 million Minnesota expansion will raise nameplate capacity 50% by 2026, yet aggregate supply will likely remain tight through 2027, limiting how quickly new liquefaction plants can serve end-users. Equipment backlogs thus act as a physical brake on market growth even where demand signals are strong.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Distribution: Tube Trailers Gain on Micro-Bulk Economics

Tube trailers, although smaller in payload, are scaling faster than cryogenic tankers thanks to lower capital outlay and faster permitting. The segment is projected to post an 11.6% CAGR between 2026 and 2031, narrowing delivered-cost differentials with cryogenic supply to below 15% on hauls shorter than 200 miles, aided by Type 4 composite cylinders that shave trailer tare weight by 40%. Cryogenic tanks still dominate heavy-volume lanes because a single tanker carries up to 5 t, equivalent to roughly eight tube trailer loads, and achieves better utilization over long distances, making it the backbone for aerospace and refinery customers. Logistics operators are experimenting with autonomous convoys on Interstate 10 to offset driver shortages and optimize drop-and-hook cycles, a strategy expected to extend liquid hydrogen market size leadership for cryogenic fleets.

Tube trailer adoption is resonating among fleet operators that consume only 100-300 kg per day and among electronics and food processors, where on-site vaporizers inflate upfront costs. Distributors bundle trailers with mobile pumping skids, enabling customers to avoid storage tank capex entirely. This “gas-as-a-service” model reduces switching friction and diversifies demand away from cyclical aerospace volumes. Over the forecast horizon, supply chain investments in lightweight cylinders and high-capacity compressors will further improve asset turns, lifting profitability for distributors that target the mid-volume sweet spot.

By Application: Automotive Outpaces Aerospace Growth

Aerospace retained 68.9% of North American volume in 2025, anchored by NASA’s Space Launch System, Blue Origin’s New Glenn, and multiple defense programs that demand ultra-high purity liquid hydrogen. However, automotive is set to be the fastest-growing segment at an 11.9% CAGR through 2031 as Class-8 fuel-cell trucks reach commercial scale. Hyundai delivered 150 XCIENT tractors in 2024, fueling network effects that encourage station roll-outs, while Nikola and Volvo follow with deliveries and hub-and-spoke refueling models.

Industrial applications such as hydrocracking, ammonia synthesis, and float glass provide a steady baseline volume. Phillips 66’s on-site liquefiers exemplify refinery self-supply strategies that internalize venting costs and stabilize flows. Maritime demand, though nascent, could accelerate once IMO carbon-intensity rules tighten in 2027, and Kawasaki’s successful oceanic carrier trials highlight technical feasibility. Power generation remains a niche owing to round-trip efficiency penalties but holds promise for data-center backup, where resilience premiums justify higher costs.

Geography Analysis

The United States anchors the liquid hydrogen market with an 83.5% share in 2025 and a forecast 10.7% CAGR to 2031, supported by the Inflation Reduction Act, state-level zero-emission mandates, and concentrated aerospace consumption in Alabama, Florida, and California. California alone represented 35%-40% of U.S. volume in 2025, propelled by the Low Carbon Fuel Standard and USD 150 million in refueling grants that create guaranteed load for new stations. Texas and Louisiana are emerging as production hubs for blue hydrogen, with Air Products committing USD 2 billion-plus to projects that couple steam-methane reforming with 95% carbon capture.

Canada holds roughly 12% of regional demand, led by Quebec’s aerospace cluster and Alberta’s oil-sands value chain. Air Liquide’s 30 t/day Bécancour plant supplies Pratt & Whitney engine testing and merchant customers across Ontario, and an Alberta joint venture aims to bring 15 t/day online by 2026 with expansion to 50 t/day by 2028. British Columbia explores green hydrogen exports to Asia on hydroelectric power, but liquefaction remains pilot-scale for now.

Mexico accounts for near 4.5% of volume, mainly serving Pemex refineries. Linde’s planned 10 t/day Monterrey plant would localize supply for northern automotive complexes, contingent on tariff harmonization under USMCA energy provisions. Solar-rich Sonora and Baja California regions feature prominently in the 2024 National Hydrogen Strategy, though financing frameworks are still evolving. Cross-border trucking faces customs delays that add up to 15% to delivered cost, so bilateral agreements on hazmat clearances could unlock faster growth.

Competitive Landscape

The top five players, Air Liquide, Linde, Air Products, Messer, and Iwatani, control an estimated 60%-65% of North American production and distribution, giving the liquid hydrogen market a moderate concentration profile. Air Liquide operates 18 liquefiers on a hub-and-spoke model that minimizes boil-off during last-mile deliveries. Linde pushes modular Brayton-cycle designs through its Cryostar unit, filing 12 patents in 2024 that promise 30% capex savings. Air Products leverages 45Q credits and its carbon-capture know-how to dominate blue hydrogen, with facilities in Beaumont and Louisiana progressing toward a combined 1.5 million-ton annual capacity by 2028.

Plug Power integrates electrolyzers with onsite liquefiers for Amazon and Walmart, bypassing merchant logistics and trimming delivered costs by up to 30%. Chart Industries targets mobile maritime bunkering and micro-bulk solutions, winning a USD 75 million contract from the California Energy Commission in 2024 for 25 modular liquefiers along key freight corridors. Smaller firms such as Hylium and Universal Industrial Gases exploit service niches in telemetry-enabled micro-bulk delivery. Patent activity around zero-boil-off storage surged in 2024 as NASA funded Cryogenic Industries for active-cooling research that could translate to terrestrial applications.

North America Liquid Hydrogen Industry Leaders

-

Air Liquide S.A.

-

Air Products and Chemicals, Inc.

-

Iwatani Corporation

-

Linde plc

-

Chart Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Hidrogenii, a 50/50 joint venture between Plug Power and Olin Corporation, officially inaugurated its liquid hydrogen (LH₂) plant in St. Gabriel, Louisiana, boasting a capacity of 15 tons per day (TPD). The facility is set to liquefy by-product hydrogen sourced from Olin’s chlor-alkali operations.

- February 2025: Air Liquide officially opened its most significant liquid hydrogen production and logistics infrastructure facility in North Las Vegas, Nevada. The facility strives to meet the growing demand for hydrogen mobility by providing hydrogen to a wide array of industries.

- January 2025: HNO International, hailing from Texas, inked a multi-year hydrogen offtake agreement worth USD 10 million. The agreement was made with a Texas-based firm specializing in zero-emission mobility, though the firm's name remains undisclosed.

- November 2024: In collaboration with LH2 Shipping and LMG Marin, SWITCH Maritime has unveiled plans for the first U.S.-built liquid hydrogen-fueled (LH2) RoPax vehicle ferry. Drawing inspiration from Norway's MF Hydra design, the new vessel boasts a capacity for 80 cars and 300 passengers, can achieve a service speed of 14 knots, and operates with zero emissions.

North America Liquid Hydrogen Market Report Scope

Liquid hydrogen is the liquid state of the element hydrogen. Hydrogen is most commonly transported and delivered as a liquid when high-volume transport is needed in the absence of pipelines. Liquefying hydrogen must be cooled to cryogenic temperatures through a liquefaction process.

The North America liquid hydrogen market is segmented by distribution method, application, and geography. By distribution, the market is segmented into cryogenic tanks and high-pressure tube trailers. By application, the market is segmented into automotive, aerospace (including outer space), industrial, marine, power generation and energy storage, and other applications. By geography, the market is segmented into the United States, Canada, and Mexico. For each segment, the market sizing and forecasts have been done on the basis of volume (kilotons).

| Cryogenic Tank |

| High-pressure Tube Trailers |

| Automotive |

| Aerospace (Including Outer Space) |

| Industrial |

| Marine |

| Power Generation and Energy Storage |

| Other Applications |

| United States |

| Canada |

| Mexico |

| By Distribution | Cryogenic Tank |

| High-pressure Tube Trailers | |

| By Application | Automotive |

| Aerospace (Including Outer Space) | |

| Industrial | |

| Marine | |

| Power Generation and Energy Storage | |

| Other Applications | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the liquid hydrogen market in North America today?

It reached 136.79 kilotons in 2026 and is projected to hit 224.23 kilotons by 2031, reflecting a 10.39% CAGR.

Which segment is growing fastest within North American demand?

Automotive end-use is advancing at an 11.9% CAGR as Class-8 fuel-cell trucks move from pilot to fleet deployment.

What policy incentives drive new liquefaction projects?

The 45V production tax credit of up to USD 3.00 per kg and stacked 45Q carbon-capture credits significantly shorten payback periods for green and blue plants.

Where are the biggest infrastructure bottlenecks?

High boil-off in small tanks, limited cryogenic tanker manufacturing, and county-level hazmat trucking restrictions all slow last-mile delivery.

Who are the leading suppliers of liquid hydrogen in North America?

Air Liquide, Linde, Air Products, Messer, and Iwatani collectively control roughly 60%-65% of production and distribution capacity.

Page last updated on: