Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.53 Billion |

| Market Size (2026) | USD 1.61 Billion |

| Market Size (2031) | USD 2.05 Billion |

| Growth Rate (2026 - 2031) | 4.99% CAGR |

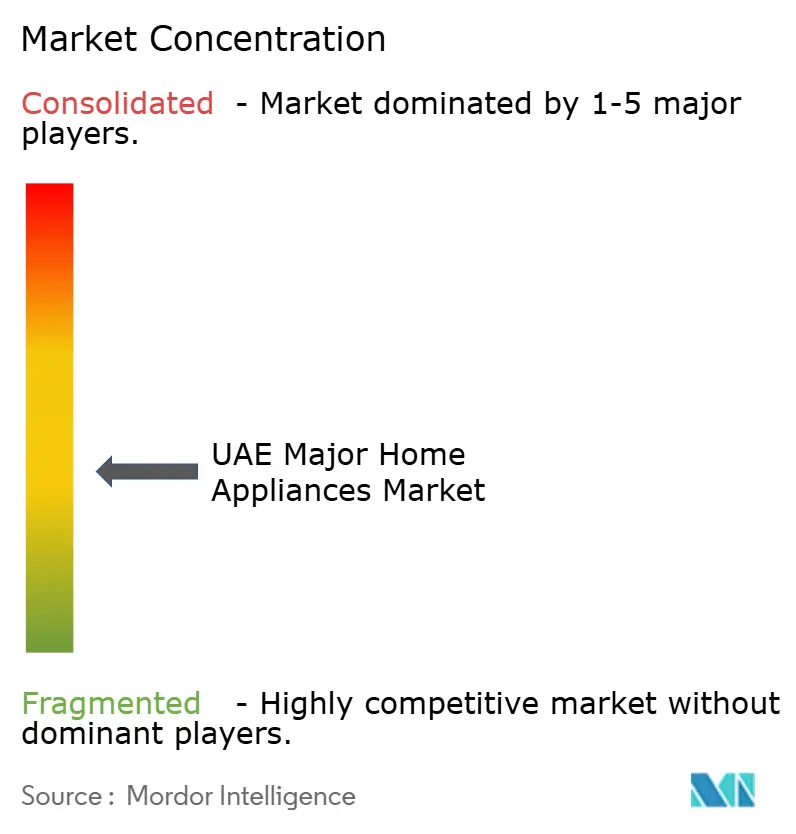

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Major Home Appliances Market Analysis by Mordor Intelligence

The UAE major home appliances market size is expected to increase from USD 1.53 billion in 2025 to USD 1.61 billion in 2026 and reach USD 2.05 billion by 2031, growing at a CAGR of 4.99% over 2026-2031. This solid trajectory reflects continuous household formation among the Emirates’ predominantly expatriate population, rising regulatory pressure for energy-efficient products, and a steady rebound in consumer purchasing power[1]Dubai Statistics Center, “Households and Residential Combines by Selected Characteristics,” dsc.gov.ae. Refrigerators continue to anchor demand, yet fast-growing categories such as dishwashers and smart laundry systems reveal a visible shift toward premium, convenience-driven living. Digital retail is extending assortment depth beyond the flagship malls of Dubai and Abu Dhabi, while government clean-energy mandates accelerate the replacement of legacy appliances with high-efficiency models[2]Mohamed Ibrahim Al Hammadi, “The UAE’s Net Zero Advantage,” abudhabisustainabilityweek.com. Competitive intensity remains moderate as global brands deepen regional footprints through acquisitions and local manufacturing partnerships that sharpen price and service propositions[3]Arçelik, “Second Quarter 2024 Financial Results Conference Call Transcript,” arcelikglobal.com .

Key Report Takeaways

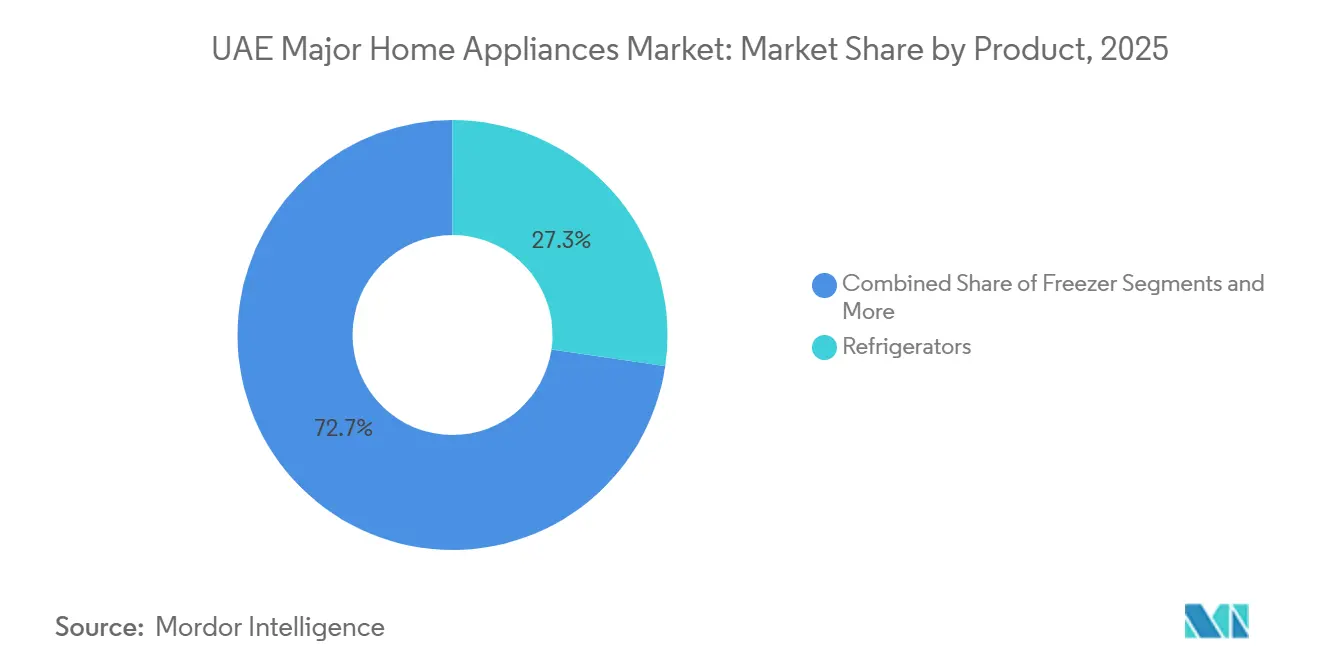

- By product, refrigerators led the UAE's major home appliances market with 27.31% share in 2025; dishwashers are forecast to expand at a 6.22% CAGR through 2031.

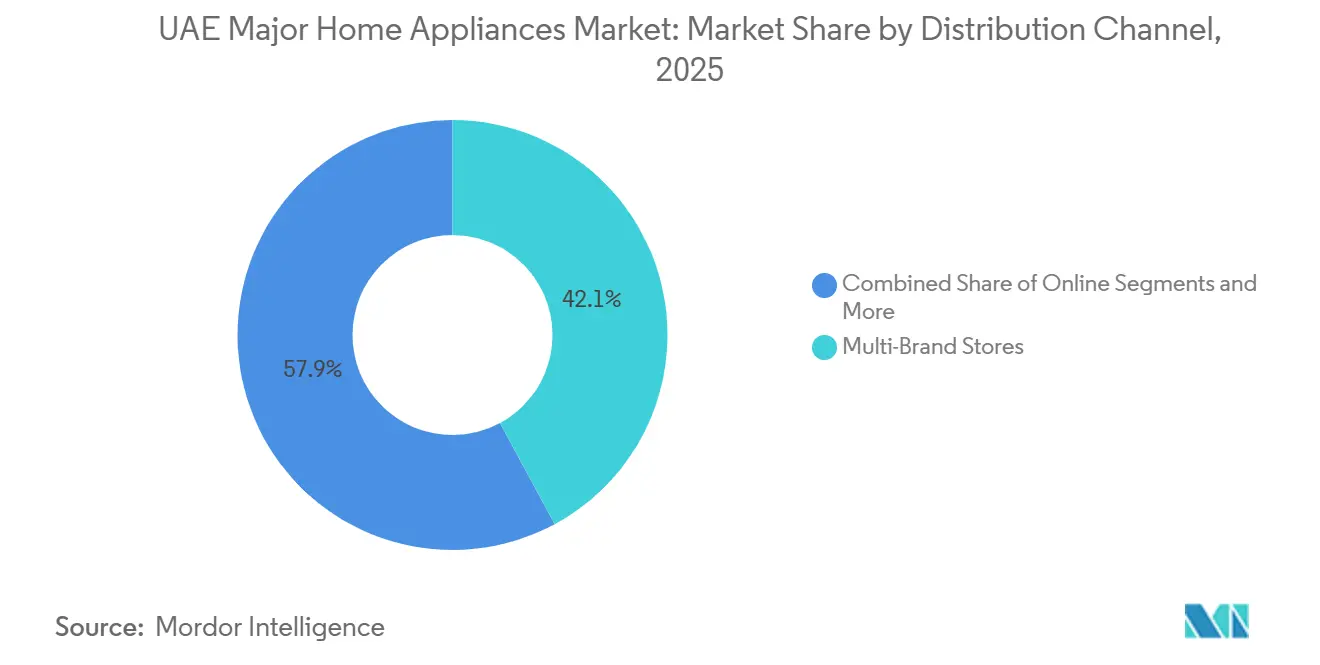

- By distribution channel, multi-brand stores commanded 42.12% of the UAE major home appliances market share in 2025; online channels are anticipated to advance at a 6.78% CAGR during 2026–2031.

- By geography, Dubai captured 37.12% of the UAE's major home appliances market's geographic share in 2025; Abu Dhabi is anticipated to be the fastest-growing emirate, registering a 6.91% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

UAE Major Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising expatriate population | +1.2% | Dubai and Abu Dhabi core, and spill over to the Northern Emirates | Medium term (2-4 years) |

| Stricter energy-efficiency standards | +0.9% | National, early gains in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Expanding e-commerce reach | +0.7% | National, strongest in Dubai and Sharjah | Medium term (2-4 years) |

| Restored consumer purchasing power | +0.6% | National, strongest in Dubai and Abu Dhabi | Short term (≤ 2 years) |

| Direct-to-consumer rental models | +0.4% | Dubai and Abu Dhabi urban centers | Long term (≥ 4 years) |

| Net-Zero 2050 smart-building push | +0.5% | National, focused on new developments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Expatriate Population Fuels Household Formation

Expatriates represent more than 80% of UAE residents, creating a structural demand base that purchases full appliance suites when new households are formed rather than when units fail. Dubai counted 624,195 households in 2021, averaging 4.3 persons, which underscores the scale of middle-to-upper income groups with dependable spending capacity. Steady off-plan sales, which comprised 60% of residential transactions in H1 2025, confirm a persistent pipeline of new homes that require refrigerators, washing machines, and increasingly premium dishwashers. Government incentives for affordable housing targeted at the skilled expatriate workforce further enlarge the addressable customer pool. Collectively, these factors lengthen the growth runway for the UAE's major home appliances market.

Stricter Energy-Efficiency Standards Accelerate Replacement Sales

The Emirates Authority for Standardisation and Metrology has widened mandatory labeling from air conditioners to refrigerators and washing machines, prompting consumers to upgrade sooner to avoid higher utility bills. Dubai’s Supreme Council of Energy is pursuing a 30% electricity-demand cut by 2030, making high-efficiency appliances central to compliance. Barakah Nuclear Energy Plant already supplies 25% of national power needs, showing the government’s commitment to a cleaner grid that supports smart, connected appliances. Appliance brands that align portfolios with five-star ESMA ratings are well-positioned to benefit from the ensuing replacement wave.

Expanding E-commerce Reach Widens Product Access

National broadband coverage, secure payment systems, and efficient last-mile logistics have converted once occasional online buyers into habitual shoppers of large appliances. The consumer goods segment booked USD 1.07 billion of online sales in 2023, demonstrating comfortable digital spend thresholds that readily stretch to refrigerators and ovens. Retailers such as Eros Group now integrate in-store consultation with web-based checkout and deferred-payment plans, ensuring the same service assurance found in malls. As smartphone penetration tops 98%, e-commerce will deepen geographical coverage into the Northern Emirates, lowering entry barriers for niche brands and subscription models.

Restored Consumer Purchasing Power Post-COVID

The UAE economy is tracking 4% GDP growth in 2025, fuelled by resilient oil prices and diversification successes that stabilize employment. Dubai’s mortgage activity surpassed 20,000 new loans in 2024, hinting at rejuvenated household balance sheets. The improved economic climate encourages postponed upgrades to energy-saving refrigerators, advanced washers, and smart cooking ranges. Government inflation allowances to Emirati families strengthen local purchasing capacity, cushioning price-sensitive segments from VAT-related cost escalation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Market saturation and longer replacement cycles | -0.8% | Dubai and Abu Dhabi are mature districts | Long term (≥ 4 years) |

| VAT and customs duties inflate prices | -0.6% | National, acute in budget segments | Medium term (2-4 years) |

| Water-scarcity rules limit high-consumption washers | -0.3% | National, more stringent in arid zones | Medium term (2-4 years) |

| Proliferation of micro-apartments reduces space | -0.4% | Dubai and Sharjah urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Market Saturation and Lengthening Replacement Cycles

Penetration for refrigerators, air conditioners, and fully automatic washers now exceeds 90% in high-income districts of Dubai and Abu Dhabi, signaling that most households already own core appliances. Higher build quality from premium brands such as Miele and Bosch extends usable lifespans to 12–14 years, stretching past the 7–10-year benchmark that once governed replacement planning. Subscription and rental operators maximize uptime through preventive maintenance programs, which further postpones the need for new unit purchases and keeps working products in circulation longer. As a result, unit demand becomes increasingly tied to incremental technological upgrades like Wi-Fi connectivity or AI-driven diagnostics rather than outright functional failure. Brands that cannot present compelling smart-feature narratives face margin pressure as value-oriented competitors thrive on price-sensitive repeat buyers. Over time, the saturation dynamic is expected to suppress volume growth even as it nudges the average selling price upward within the UAE major home appliances market.

VAT and Customs Duties Inflate Retail Prices

A combined 5% VAT and 5% customs duty imposes a 10% baseline tax on imported appliances, immediately pushing up shelf prices across entry-level and mid-tier segments. Dubai trimmed its duty-free threshold for personal imports from AED 970 (USD 264) to AED 300 (USD 81.67) in 2023, which shifted even small countertop items and spare parts into the taxable bracket and raised the total cost of ownership for consumers. From August 2025, the 12-digit Integrated Customs Tariff expanded code listings from 7,800 to more than 13,400 classifications, some carrying duty bands of 10%, 50%, or 100%, adding compliance complexity and potential rate hikes for specific appliance sub-types. Importers must now budget for additional brokerage fees, longer clearance times, and expensive reclassification audits when errors occur. The incremental costs often cascade to end-users, prompting shoppers to delay discretionary upgrades or switch to locally assembled alternatives that can bypass some duties. Consequently, fiscal policy acts as a structural drag on volume expansion and compresses retailer margins in the UAE's major home appliances market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Refrigerators Retain Scale While Dishwashers Accelerate

Refrigerators held 27.31% of the UAE major home appliances market share in 2025, anchored by year-round cooling requirements that push ordinary households to favor frost-free models rated at ESMA four or five ticks. The segment accounted for the largest slice of the UAE's major home appliances market, reflecting heavy utility consumption and the pivotal role of fresh food storage in a hot desert climate. Enhanced inverter compressors and embedded IoT sensors entice consumers to replace older units ahead of technical expiry, thereby sustaining baseline demand.

Dishwashers, though coming from a smaller base, are projected to expand at a 6.22% CAGR, driven by dual-income expatriate households that prioritize convenience, hygienic cleaning, and water savings relative to manual washing. New-build villas in Abu Dhabi include dedicated dishwasher space in fitted kitchens, reinforcing category adoption. In parallel, freezers serve hospitality and large-family niches, while washer-dryers gain traction under water-rating schemes encouraging resource-efficient cycles. Oven-microwave hybrids appeal to compact apartments seeking multipurpose cooking solutions. This evolving mix underlines a premiumization trend, keeping the UAE major home appliances market on an upward, value-rich path.

By Distribution Channel: Multi-Brand Stores Lead but Digital Gains Momentum

Multi-brand retailers controlled 42.12% of the UAE major home appliances market size in 2025 through extensive mall footprints, immediate stock availability, and on-site service desks. Their showrooms display entire product suites, allowing shoppers to compare energy ratings and negotiate bundled installation, which remains a decisive factor for heavy items such as refrigerators and washers.

Online channels, however, are set to post a 6.78% CAGR to 2031. Click-and-collect models and next-day delivery for refrigerators illustrate logistic improvements that remove one-time barriers. Flash-sale events timed around Ramadan and White Friday boost web traffic and widen the customer funnel into Sharjah and the Northern Emirates. Exclusive brand stores remain vital for flagship demonstrations of connected appliances and chef-led cooking sessions that elevate perceived value. Corporate B2B tender sales complement the mix, supplying large residential projects and hotels that specify ESMA five-tick equipment packages as part of green-building certification.

Geography Analysis

Dubai generated the largest revenue share at 37.12% in 2025 because it houses the majority of expatriate professionals and commercial enterprises. Continuous off-plan property launches, coupled with 8.4% growth in residential prices during H1 2025, underscore robust household formation that directly feeds appliance sales. Dubai’s Green Building Regulations drive upgrades to ESMA five-tick refrigerators and inverter air conditioners, reducing energy bills and shortening replacement cycles.

Abu Dhabi follows as the fastest-growing emirate with a forecast 6.91% CAGR through 2031. Massive infrastructure outlays and Barakah’s nuclear capacity, supplying one-quarter of national electricity, boost grid stability, enabling smart appliance adoption at scale. Government housing plans for Emirati citizens, along with international talent attraction into energy and technology sectors, widen the consumer base for premium dishwasher and washer-dryer combos.

Sharjah and the Northern Emirates collectively post moderate yet steady growth, supported by spill-over employment from Dubai and improved transport corridors that facilitate multi-brand store expansion. Lower average incomes preserve demand for value-oriented refrigerators and top-load washers, yet rising e-commerce penetration equalizes product availability. Fujairah, Umm Al Quwain, Ras Al Khaimah, and Ajman trail on an absolute scale but present greenfield prospects for installers of ESMA five-tick units backed by micro-financing schemes.

Competitive Landscape

The UAE major home appliances market is moderately fragmented but moving toward consolidation. Arçelik’s EUR 20 million (USD 23.35 million) acquisition of Whirlpool’s MENA operations in April 2024 delivered control of USD 121 million in regional revenue and is forecast to generate EUR 300 million (USD 350.26 million) in annual synergies. The deal strengthens Arçelik’s brand roster in refrigerators and dishwashers and expands after-sales service capacity across the Emirates.

Global giants are sharpening technology differentiation. Samsung integrates its SmartThings platform into UAE-sold washers and fridges, preparing for AI-based energy optimization as nuclear-supported supply makes time-of-use tariffs plausible. LG and Samsung are jointly evaluating the purchase of Hitachi’s appliance division, signaling additional scale plays to counter aggressive Chinese brands seeking Gulf footholds.

Local and regional assemblers respond by situating production nearer to demand. Sharp’s joint venture with Egypt’s Elaraby Group will ship 400,000 refrigerators annually from March 2026, promising lower landed costs in the UAE. LG’s air-conditioner line in Egypt aims to sidestep tariff complexity and shorten lead times for project deliveries. Meanwhile, D2C specialists develop subscription packages that bundle installation, filter replacement, and software updates, attracting mobile expatriate tenants and expanding aftermarket data streams.

UAE Major Home Appliances Industry Leaders

LG Electronics

Samsung Electronics

Whirlpool Corporation

Haier Smart Home (incl. GE Appliances)

Arçelik A.Ş. (Beko, Grundig)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Samsung Electronics and LG Electronics entered talks to acquire Hitachi’s home appliance division in a deal worth KRW 1–2 trillion (USD 720 -1440 million), seeking scale synergies against Chinese competitors.

- August 2025: Dubai and Abu Dhabi adopted a 12-digit Integrated Customs Tariff, raising the number of codes to 13,400 and introducing duty bands up to 100%, altering appliance pricing structures.

- March 2025: Miele released W2 and T2 Nova Edition laundry units featuring InfinityCare drums and FlexLoad AI resource optimization, targeting premium households.

- July 2024: Sharp and Egypt’s Elaraby Group agreed to build a refrigerator plant with 400,000-unit annual capacity for Africa and the Middle East.

UAE Major Home Appliances Market Report Scope

"Major Home Appliances means clothes washers, clothes dryers, dishwashers, ranges, ovens, cooktops, micro-hood combinations, refrigerators and freezers, and other home appliances considered as major home appliances. A complete background analysis of the UAE's Major Home Appliances Market, which includes an assessment of the economy, market overview, market size estimation for key segments, emerging trends in the market, market dynamics, and key company profiles, are covered in the report.

UAE's major home appliances market is segmented by product type and distribution channel. By product type, the market is segmented into refrigerators, freezers, dishwashing machines, washing machines, ovens, air conditioners, and other major appliances, and by distribution channel the market is segmented into hypermarkets/supermarkets, specialty stores, online, and other distribution channels. The report offers market size and forecasts for the UAE major home appliances market in value (USD) for all the above segments."

By Product

| Refrigerators |

| Freezers |

| Washing Machines |

| Dishwashers |

| Ovens (Incl. Combi & Microwave) |

| Air Conditioners |

| Other Major Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| Abu Dhabi & Al Ain |

| Dubai |

| Sharjah & Northern Emirates |

| Others (Fujairah, Umm Al Quwain, Ras Al Khaimah, Ajman) |

| By Product | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| By Distribution Channel | Multi-Brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| By Geography | Abu Dhabi & Al Ain |

| Dubai | |

| Sharjah & Northern Emirates | |

| Others (Fujairah, Umm Al Quwain, Ras Al Khaimah, Ajman) |

Key Questions Answered in the Report

How large is the UAE major home appliances market in 2025?

The UAE major home appliances market size reached USD 1.53 billion in 2025 and is forecast to hit USD 2.05 billion by 2031.

Which product category leads sales?

Refrigerators retained the largest share at 27.31% of 2025 revenue, reflecting essential food-storage needs in the desert climate.

Which emirate is growing the fastest?

Abu Dhabi is projected to record a 6.91% CAGR through 2031 on the back of infrastructure investment and high-income household inflows.

What drives replacement demand in coming years?

Stricter ESMA efficiency labels and the Net-Zero 2050 agenda are accelerating replacement of older, power-hungry appliances.

How will the new 12-digit customs tariff affect prices?

The expanded tariff system introduces higher duty bands that are expected to raise landed costs, especially for budget models imported fully built.

Are online channels gaining share?

Yes, e-commerce sales of large appliances are forecast to grow at a 6.78% CAGR as national logistics and payment ecosystems mature.

Page last updated on: