Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 766.08 Million |

| Market Size (2031) | USD 904.20 Million |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Israel Home Appliances Market Analysis by Mordor Intelligence

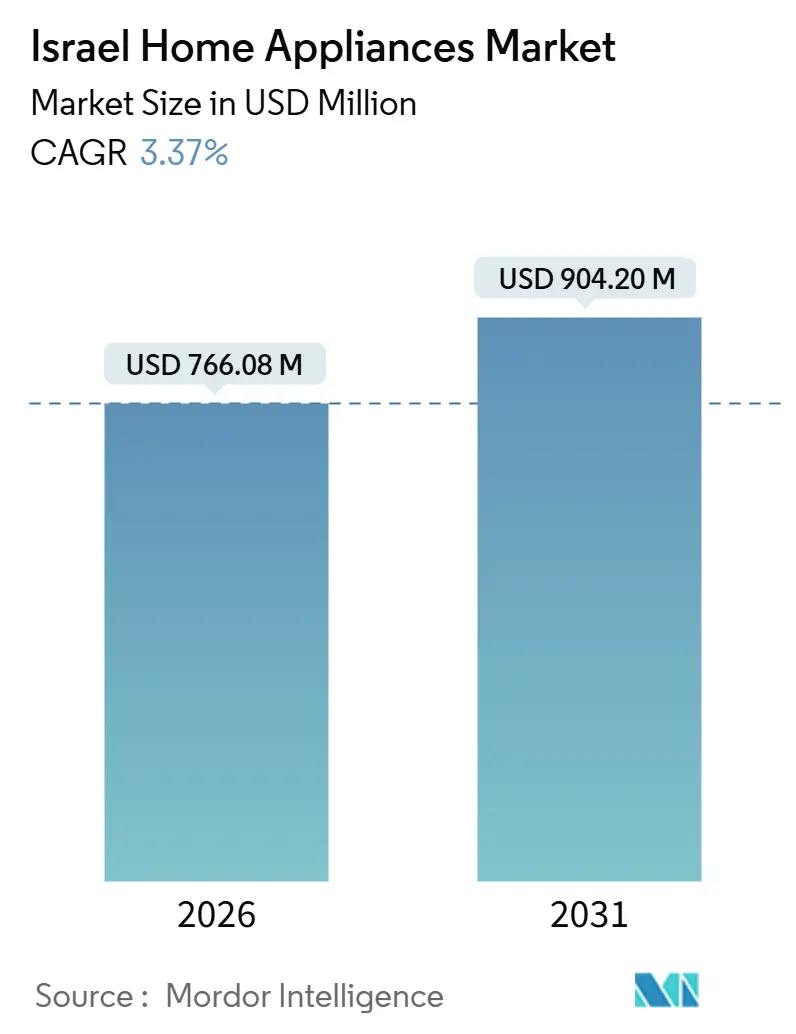

The Israel Home Appliances Market size is estimated at USD 766.08 million in 2026, and is expected to reach USD 904.20 million by 2031, at a CAGR of 3.37% during the forecast period (2026-2031).

Streamlined import procedures that align with European Ecodesign and Energy Labelling rules are expanding the range of compliant products and reducing time to shelf, which supports both premium and mid-market offerings[1]Ministry of Energy and Infrastructure, “The Ministry of Energy’s Import Reform,” Government of Israel, gov.il. Maritime rerouting around the Cape of Good Hope after Red Sea disruptions keeps freight and insurance premiums elevated, so distributors continue to manage higher landed costs that affect retail pricing and promotional calendars. E-commerce adoption for durable goods has broadened, aided by omnichannel investments from national chains and reliable last-mile fulfilment, which shortens decision cycles for small appliances and accelerates price discovery for big-ticket categories. Consumer purchasing power recovered in 2025 and is projected to strengthen in 2026, which sustains upgrade intent and supports replacement cycles across major categories. Within categories, refrigerators remain the volume anchor while coffee makers are projected to post the sharpest growth as households balance utility with attainable premium features.

Key Report Takeaways

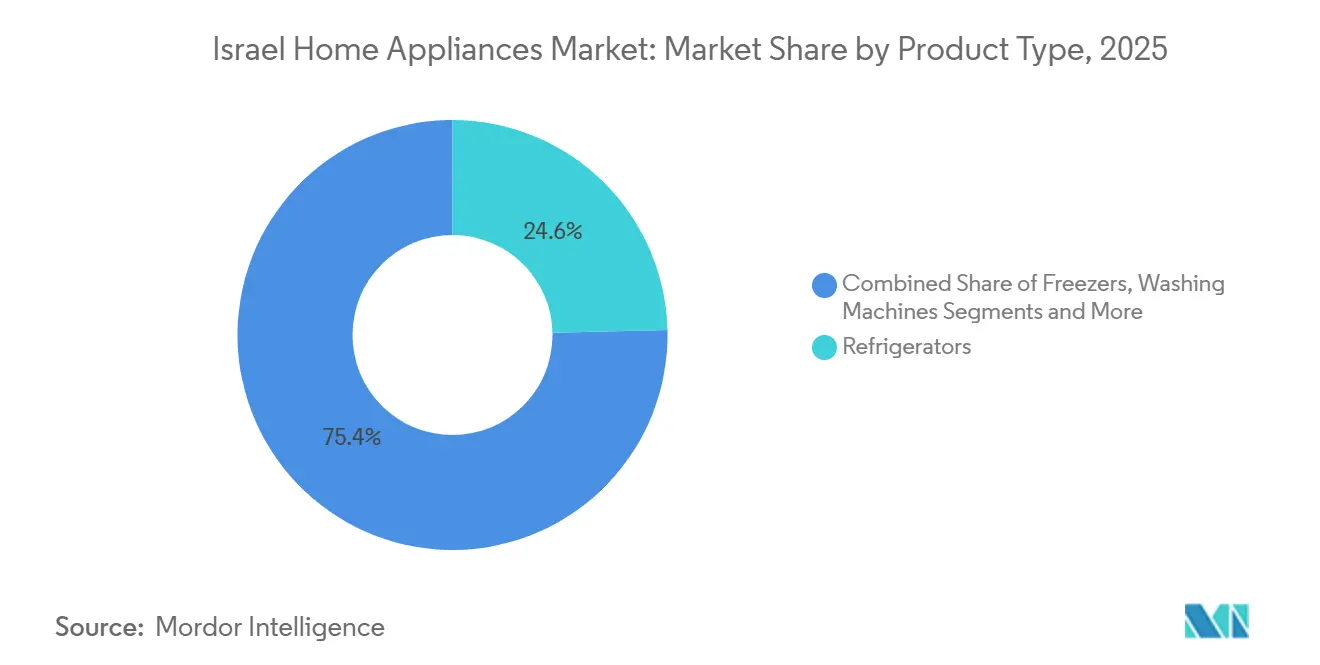

- By product category, refrigerators led with 24.63% of the Israel home appliances market share in 2025, and coffee makers are forecast to expand at a 3.92% CAGR through 2031.

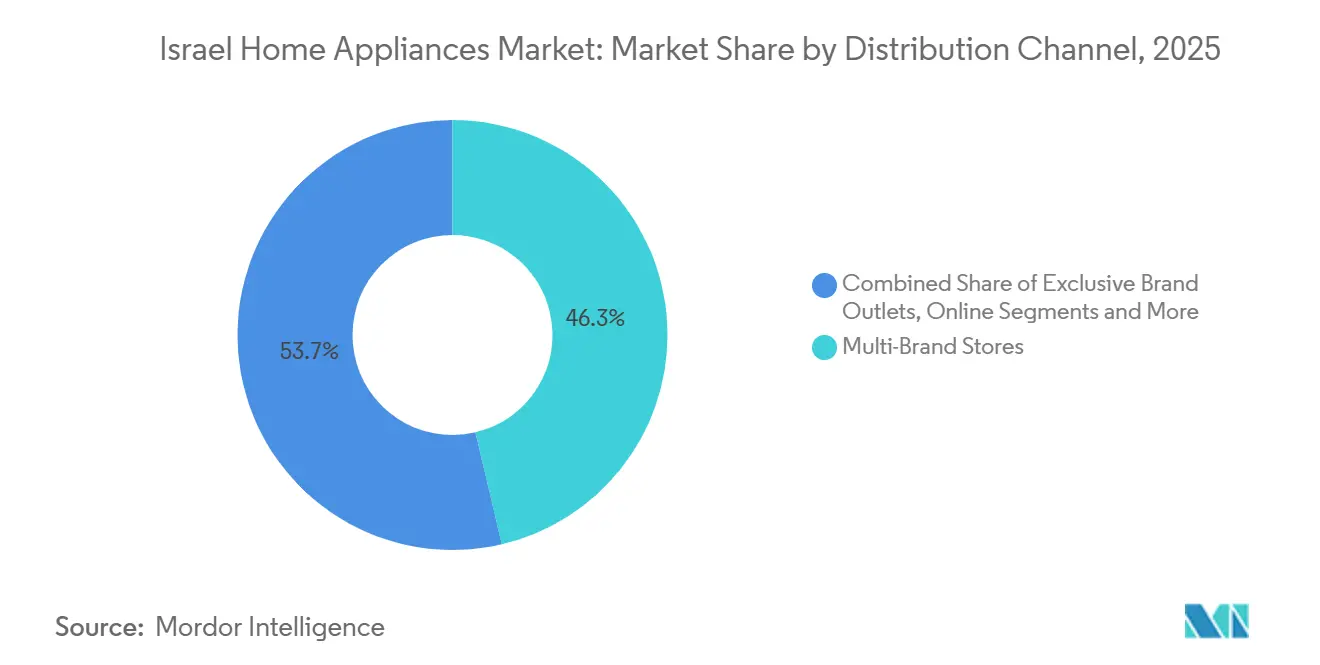

- By distribution channel, multi-brand stores held 46.32% of the Israel home appliances market share in 2025, while online retail is forecast to grow at a 4.16% CAGR to 2031.

- By geography, the Central District accounted for 41.93% of the Israel home appliances market share in 2025, and the Tel-Aviv District is projected to advance at a 3.75% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Israel Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising household disposable income & new-build completions | +1.2% | National, strongest in Central & Tel-Aviv Districts | Medium term (2-4 years) |

| Energy-efficiency mandates triggering replacement demand | +0.9% | Global, with accelerated uptake in Tel-Aviv & Central urban cores | Long term (≥ 4 years) |

| E-commerce penetration of durable goods | +0.6% | National, the highest in the Tel-Aviv District metro | Short term (≤ 2 years) |

| Intensifying cooling needs due to hotter summers | +0.5% | National, most acute in the southern peripheral districts | Medium term (2-4 years) |

| Lower water tariffs from desalination are encouraging dishwashers | +0.2% | National, with early gains in coastal municipalities | Long term (≥ 4 years) |

| Tech-savvy aliyah inflow boosting smart-appliance uptake | +0.1% | Concentrated in the Tel-Aviv District, with moderate spill-over to the Central District | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Household Disposable Income & New-Build Completions Fuelling Replacement Cycles

Household purchasing power strengthened in 2025 and is projected to remain firm in 2026, with the OECD estimating private consumption growth of 5.6% in 2025 and 6.0% in 2026, which supports higher value upgrades and steadier replacement cycles for large and small appliances[2]OECD, “OECD Economic Surveys, Israel 2025,” OECD Publishing, doi.org. The Bank of Israel reported that durable goods demand rebounded in 2024 after a weak 2023, restoring momentum for essential categories such as refrigerators, washing machines, and air conditioners, and improving the base for subsequent growth. Retailers with broad store networks and integrated delivery capabilities aligned inventory with household move-in timelines, which helped convert dwelling handovers into coordinated bulk orders for core appliances and follow-on purchases of small kitchen products. Urban renewal and completions in core districts concentrate installations in established neighbourhoods, and that pattern favours energy-efficient replacements where labels and lifetime cost narratives are familiar to shoppers under Israel’s EU-aligned policy framework. Together, these factors underpin a steady cycle in which each completed unit generates an anchor set of major appliances followed by discretionary additions as budgets allow, creating recurring demand that retailers and service providers can plan for with technician capacity and bundled installation offers.

Energy-Efficiency Mandates Triggering Replacement Demand Through EU-Aligned Standards

Israel’s import reform aligns appliance approvals with European Ecodesign and Energy Labelling regulations, which reduces duplicate testing, accepts ILAC-accredited reports, and widens the flow of EU-compliant models across refrigerators, washing machines, dryers, dishwashers, air conditioners, and ovens. The transition included a structured period with guidance that addressed differences between legacy local requirements and EU rules, including topics such as flammable refrigerants and performance in warmer climate zones, which helped importers adapt documentation and product mix without prolonged delays. Harmonization supports competitive pricing by allowing manufacturers to leverage one conformity file across markets, and it increases shelf-ready choice for consumers, which is visible in broader model assortments and more consistent energy labels across brands. The National Energy Efficiency Action Plan targets an improvement in energy intensity by 2030 versus a 2015 baseline, with projected savings from appliance regulations that strengthen the case for retiring older equipment ahead of end-of-life and for adopting inverter compressors, variable-speed motors, and heat-pump drying. As higher efficiency becomes the baseline in mid-range tiers, retailers can anchor merchandising around total cost of ownership and reliable label comparisons, which encourages upgrades and supports replacement-led volume over the medium term.

E-Commerce Penetration of Durable Goods Accelerating Direct-to-Consumer Channels

Omnichannel strategies widened the shopping funnel for large and small appliances, as national chains expanded stores while integrating reservation, delivery booking, and installation scheduling in one interface to drive higher conversion on bulky products. Retail disclosures show that online sales contributed to growth and that hybrid models are gaining traction, which suggests that shoppers are increasingly comfortable completing high consideration purchases digitally when service and installation are bundled. Local e-commerce specialists reinforce adoption by offering localized content, compliant power standards, and Hebrew documentation, which reduces purchase friction for new immigrants and time-pressed urban professionals while protecting post-purchase satisfaction with clear support channels. As assortment depth improves and delivery reliability stabilizes despite maritime detours, digital discovery is influencing final purchase location across categories and moving more transactions into online checkout for even large appliances. Providers that show clear delivery windows, damage protection, and compliant installation workflows are converting higher-priced baskets online, which shifts channel mix and supports faster uptake of energy-labelled models with detailed feature content on product pages.

Intensifying Cooling Needs Due to Hotter Summers Driving Air-Conditioner Demand

Heat risk indicators point to more frequent hot days and warm nights in Israel, and these conditions increase residential cooling loads and make efficient split systems and inverter technologies more salient in purchase decisions[3]World Bank Group, “Israel, Compounded Heat Risks,” Climate Change Knowledge Portal, climateknowledgeportal.worldbank.org. Retailers reported steady demand for climate systems in 2025 and highlighted the role of service networks in managing installation and maintenance during peak seasons, which stabilized sell-through even as shipping schedules fluctuated. As households run cooling for longer hours in summer months, the price premium for A-class efficiency and inverter control is easier to justify on power bills, which nudges the mix toward models that moderate electricity use while maintaining comfort. EU-aligned approvals also make it easier for distributors to bring in higher-efficiency AC models already validated for comparable climate conditions, which broadens choice and shortens time to shelf under the import reform. These dynamics reinforce the structural role of climate in category demand and support lifecycle-oriented merchandising that highlights running cost and service reliability alongside upfront pricing in stores and online.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High import duties & shipping costs | −0.8% | National, with acute pressure on import-reliant retailers | Short term (≤ 2 years) |

| Supply-chain disruptions & NIS volatility | −0.6% | National, affecting all importers and exporters | Medium term (2-4 years) |

| Shrinking kitchen footprints in rental units | −0.3% | Concentrated in Tel-Aviv & Central rental markets | Long term (≥ 4 years) |

| Producer cost from stricter e-waste regulation | −0.4% | National, compliance burden on manufacturers & importers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Import Duties & Shipping Costs Compressing Distributor Margins and Delaying Purchases

Prolonged maritime detours around the Cape of Good Hope continue to lift fuel consumption and insurance, and shippers have redeployed capacity in an effort to maintain service frequency, which has kept container rates elevated relative to 2023 levels. Freight volatility increases the landed cost of goods and narrows room for discounting, so retailers rebalance assortments toward models with strong value narratives and reliable after-sales economics. Importers must also navigate regulatory costs tied to packaging and recycling compliance requirements in Israel, which adds handling and documentation overhead during clearance and delivery. As these cost layers stack, consumer sensitivity to big-ticket prices intensifies, and replacement cycles may lengthen in price-conscious segments of the Israeli Home Appliances Market. Operators that lock in volume contracts and optimize shipment timing are better positioned to preserve gross margins while maintaining promotional activity.

Supply-Chain Disruptions & NIS Volatility Extending Lead Times and Introducing Currency Risk

Attacks in the Red Sea region caused a sharp drop in Suez Canal transits and pushed carriers to route around Africa, extending voyage times by 10 to 14 days and disrupting schedule reliability for Asia–Europe lanes. The World Bank expects the security premium on maritime transit and insurance to persist, which is consistent with carriers’ capacity redeployment and the congestion ripple effects observed across major transshipment hubs. Maersk analysis points to a reduction in effective container capacity and continued port bottlenecks, pressuring import calendars for seasonal launches and limiting the flexibility of just-in-time replenishment[4]Maersk, “The ongoing ripple effects of Red Sea shipping disruptions,” A.P. Moller–Maersk, maersk.com. During unpredictable transit windows, distributors carry higher buffer inventory or extend lead times to avoid stockouts, which ties up working capital and complicates pricing for currency-denominated purchases. Hedging programs cushion swings but carry costs that can compress margins in the Israel home appliances market when exchange rates move between purchase order and shelf date.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dual-Speed Growth with Refrigerators Anchoring Volume and Coffee Makers Capturing Aspirational Spending

Refrigerators held 24.63% of the Israeli home appliances market share in 2025, which reflects mandatory fit-out in new units and a steady replacement cadence for existing households. Coffee makers are forecast to expand at a 3.92% CAGR through 2031, as compact capsule systems and semi-automatic espresso machines gain traction among urban professionals and students who value convenience without sacrificing perceived quality. Energy-labelled appliances with inverter compressors and improved insulation are converting shoppers who compare lifetime running costs, and those efficiency narratives align with EU harmonization in Israel that smooths approval for advanced models. The Israel home appliances market also benefits from growing awareness of water and power savings, which reinforces the case for heat pump dryers and A-class refrigerator options that reduce consumption footprints across the home. Retailers support this shift by highlighting energy labels online and in-store and by bundling installation and service plans that protect premium purchases through the first years of use.

Laundry is trending toward front-load washers with inverter motors and condenser or heat pump dryers that better manage utility costs in compact apartments, which strengthens mid-tier demand. Small appliances post a diverse growth pattern as robotic vacuums with auto-empty docks and cordless sticks with multi-surface attachments consolidate floor care into fewer SKUs that command category shelf space. Built-in ovens and cooktops increasingly promote low-maintenance cleaning cycles and preset cooking functions, while Sabbath mode support in ovens and refrigerators broadens addressability across observant households, a feature often highlighted in local product merchandising. Air conditioners remain core to comfort and climate resilience, and distributors with strong service networks are positioned to capture multi-room installations and recurring maintenance revenues. The Israel home appliances market continues to balance essential white goods with discretionary coffee and floor care upgrades, creating a layered demand profile that supports both value and premium tiers.

By Distribution Channel: Multi-Brand Stores Retain Incumbency While Online Scales Omnichannel Convenience

Multi-brand chains lead the channel mix with 46.32% of the Israel home appliances market and provide showroom experiences that matter for refrigerators, ovens, and built-in dishwashers, including professional installation and extended service options. National operators expanded store networks in 2025, invested in digital experiences, and kept delivery capacity resilient during shipping disruption cycles, which protected category availability and customer satisfaction. Exclusive brand outlets support product education for connected features and energy labels, and these locations serve as visibility hubs for new model families that then cascade to broader retail. Supermarkets and home centres carry a selection of small appliances, but their fast-turn merchandising and limited floor space keep the focus on kettles, toasters, and handheld cleaning devices rather than large white goods. The Israel home appliances market continues to rely on the scale and services of multi-brand stores to introduce premium features and manage the lifecycle of big-ticket sales. Across the network, retailers highlight integrated installation and after-sales care to lower friction for consumers moving between dwellings and upgrading key kitchen and laundry equipment.

The Israel home appliances market size for online retail is forecast to grow at a 4.16% CAGR through 2031, supported by user-friendly storefronts, comparison tools, and reliable delivery options that extend to bulky items. Domestic e-commerce specialists offer installment payments, certified business transparency, and localized support with Israeli power standards and Hebrew documentation, while cross-border platforms broaden choice when delivery windows are reliable. National chains have adopted hybrid models that let shoppers reserve inventory online for store pickup or schedule home installation within one interface, closing the gap between digital research and in-home service. This approach preserves the tactile reassurance of showrooms for high consideration purchases while capturing the convenience and price transparency of online shopping.

Geography Analysis

The Central District accounted for 41.93% of Israel home appliances market share in 2025, reflecting its dense mix of family households and steady new completions. National retailers maintain strong showroom footprints across the district and report healthy revenue in their electrical retail segments, which underscores consistent demand in the district for essential white goods and seasonal cooling systems. Housing turnover supports scheduled appliance replacements and fit-outs, and stable employment in the district helps sustain mid-range and premium purchases. Energy efficiency labelling is salient in family-oriented buying decisions, and the EU-aligned permit pathway has broadened the assortment available for households looking to lower running costs. Seasonal heat underscores the need for reliable split systems and window units, which keep service capacity valuable and support recurring maintenance revenues for retailers with technician networks. The Israel home appliances market in the Central District, therefore, balances necessity spend with selective upgrades as families trade up to refrigerators and laundry systems that fit efficiency and space needs.

Tel Aviv District is projected to grow at a 3.75% CAGR through 2031, with purchasing power and household formation among young professionals supporting small kitchen appliances and compact major appliances that optimize space. Cross-border and domestic e-commerce play a pronounced role in discovery, and price comparison for Tel Aviv households, and omnichannel pickup or delivery options increase conversion for time-sensitive purchases. International migration inflows enhance demand for familiar brands and connected features, and early adopters in this district lean into app-enabled devices when the feature premium is justified by convenience. Price transparency and reliable last-mile service help narrow the online-to-offline gap for major appliances and improve willingness to purchase larger items online when installation is bundled. The Israel home appliances market in Tel Aviv District, therefore, shows a faster tilt toward compact, efficient, and connected products that fit smaller kitchens and flexible living arrangements. Retailers emphasize narrow-depth refrigerators, slim dishwashers, and combination washer-dryer towers to meet these constraints while maintaining useful capacity.

The Rest of Israel combines Northern, Haifa, Southern, and Jerusalem districts, with growth patterns shaped by regional demographics, reconstruction dynamics, and retail access. Southern and Jerusalem areas demonstrate active housing pipelines and urban renewal projects that support essential white goods, while the product mix adjusts to household size, budget, and climate needs. Retailers target these districts with assortments that favour value models, reliable warranties, and practical features rather than premium connectivity at higher price points. The Israel home appliances market across these regions benefits from government energy efficiency policy consistency that brings more EU-compliant options to showrooms and online stores. As maritime and currency conditions normalize, service levels and availability are expected to improve in regional cities and towns, which strengthens the foundation for steady category replacement.

Competitive Landscape

The Israel home appliances market shows moderate fragmentation, where global brands compete alongside national distributors with deep retail and service footprints. Leading chains reported sustained revenue in 2025, reflecting expanded stores and omnichannel investments that raised visibility for white goods and small appliances across core districts. A renewed distribution agreement strengthened one of the leading retailers’ positions in large kitchen appliances and televisions from a top global OEM starting in 2025, which consolidated import flows and broadened the assortment. Domestic manufacturers are investing in climate system capabilities and adjacent energy technologies while managing export exposure and logistics headwinds into Europe and other markets. Stability in category demand gives room for premium innovation, yet price sensitivity remains elevated for large-ticket purchases, which keeps promotional depth and financing options central to conversion. The Israel home appliances market, therefore, rewards operators that align value narratives with efficient service models and strong brand partnerships.

Strategic partnerships and portfolio moves have reshaped channel access for several brands. A leading retailer’s direct import arrangement for large appliances from a top-tier consumer electronics maker improved SKU breadth and supply visibility, which also supported national promotions coordinated across online and store networks. Appliance manufacturers with local assembly continue to refine product roadmaps for heat-efficient solutions and refrigerants aligned with evolving regulations, and they stated revenue goals that reflect prudent assumptions on logistics normalization and demand pacing toward 2026. European OEMs also maintain in-country subsidiaries and equity links to the local industry, which sustain technology transfer and service quality in the Israeli market. Category-level innovation continues in connected appliances, although adoption remains selective and tied to clear use cases and credible warranty support. Competitive differentiation is concentrated in energy performance, space efficiency, and service reliability.

Red Sea rerouting and port congestion required distributors to adjust procurement calendars, which favoured players with diversified sourcing and the ability to book forward capacity. Carriers reported persistent ripple effects across Europe and key transshipment hubs, so top retailers emphasized inventory visibility and multi-supplier strategies to mitigate delays. At the same time, policy alignment with EU standards keeps the flow of higher efficiency models increasing, which lifts the baseline for major categories and enables retailers to tell stronger total-cost-of-ownership stories at the point of sale. National chains that integrate installation, recycling take back, and extended warranties have an advantage in conversion and retention because these services address consumer concerns around delivery, fit, and end of life. The Israel home appliances market thus remains a contest of breadth, logistics execution, and after-sales excellence as brands and retailers compete for household spending.

Israel Home Appliances Industry Leaders

Electra Consumer Products

Tadiran Holdings

BSH Home Appliances

Whirlpool Corporation

LG Electronics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Haier Israel hosted a high-profile product launch in Tel Aviv, attracting over 250 partners and media representatives. Haier Smart Home, achieving over 20% annual growth in Israel's home appliance market, unveiled premium products, including the 825 series refrigerator with 681L capacity, MSA smart preservation technology, and adjustable temperature zones for diverse storage needs.

- August 2025: AEG introduced AI-powered ovens in Israel, enabling automated recipe-to-cooking program conversion. Imported by Miniline, the German-made ABE75722T from AEG’s 7000 series features a 71-liter capacity, 30-300°C range, A++ energy rating, MAXIKLASSE XXL chamber, and a 4.3-inch touch screen for preset programs, OTA updates, language options, and manual or automated cooking control.

- June 2025: TCL announced that it is expanding its presence in Israel by diversifying its product offerings and establishing new distribution agreements. C-Data will distribute TCL’s TVs and monitors, while Electra Consumer Products will market white goods. Electronics Pro, Retphone, and Flerom will provide installation and service support, enhancing TCL’s local market positioning.

- January 2025: AEG, imported by Miniline, launched the Comfort Lift series of dishwashers in Israel with a globally patented feature allowing the lower basket to lift to a comfortable working height, priced starting at NIS 4,390, targeting premium consumers willing to pay 50 to 60 percent above entry-level models for ergonomic convenience and advanced features including automatic program selection and AirDry technology.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of home appliances sold for household use in Israel, across major and small appliances, counted at the point of sale through offline and online channels.

Scope exclusions: It does not count second-hand sales, informal peer-to-peer resales, or repair and maintenance services that do not include a new appliance unit.

Segmentation Overview

- By Product

- Major Home Appliances

- Refrigerators

- Freezers

- Washing Machines

- Dishwashers

- Ovens (Incl. Combi & Microwave)

- Air Conditioners

- Other Major Home Appliances

- Small Home Appliances

- Coffee Makers

- Food Processors

- Grills & Roasters

- Electric Kettles

- Juicers & Blenders

- Air Fryers

- Vacuum Cleaners

- Electric Rice Cookers

- Toasters

- Counter-top Ovens

- Other Small Home Appliances

- Major Home Appliances

- By Distribution Channel

- Multi-Brand Stores

- Exclusive Brand Outlets

- Online

- Other Distribution Channels

- By Geography

- Central District

- Tel-Aviv District

- Rest of Israel

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the base context and the guardrails for sizing, including household formation, housing activity, and retail trade conditions that shape appliance replacement cycles. We reviewed public statistics and releases such as those from the Israel Central Bureau of Statistics, the Bank of Israel, Israel Tax Authority import and customs publications, and the Israel Standards Institute (for labeling and compliance signals that can impact category mix). Broader comparisons were also taken from sources such as UN Comtrade, World Bank indicators, and relevant peer reviewed consumer durables and energy efficiency studies.

Company annual reports, public financial statements, investor decks, and retailer announcements were then used to cross-check category momentum and channel mix, especially for online penetration and promotion intensity. For structured fact finding, paid subscriptions were used selectively for company financial intelligence, shipment-level import and export records, and patent look-ups to sanity check product refresh trends. This list is not exhaustive, and many other public and paid sources were referenced as needed to collect data, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work focused on interviewing and surveying Israel-based stakeholders across the value chain, including distributors, multi-brand retailers, brand-led outlets, and service ecosystem participants who understand sell-through and replacement demand. We also spoke with product and category managers to confirm pricing ladders, seasonal peaks around holidays, and how energy labels and installation constraints influence what is actually purchased across districts.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 15% | APAC: 44% |

| Mid tier: 51% | Functional/Unit leaders: 34% | EMEA: 30% |

| Smaller Players: 15% | Managers: 51% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs Israel demand using household counts and new housing completion signals, and then applies replacement and first-time purchase rates by appliance group before it is converted to value using observed price bands. Because the final number should still look realistic versus what suppliers and channels see, we corroborate the total with selective bottom-up approximations such as sampled unit volumes by category times average selling prices, along with channel checks on offline versus online splits.

Key inputs used in the model include appliance penetration and replacement cycles, new home additions and renovation activity, import dependence by category, retail price movements by major versus small appliances, and the share shift toward online and multi-brand stores. Where direct unit indicators are patchy for a subcategory, we bridge gaps using proxy series like import value trends, stock-keeping unit turnover discussions from fieldwork, and consistency checks against household spending patterns. Forecasting uses scenario analysis supported by short time-series smoothing on core drivers, and the forward view is then adjusted after discussing the likely path of promotions, energy-efficient upgrades, and consumer confidence with industry participants.

Data Validation & Update Cycle

Outputs are validated through several checks so totals do not drift away from real market signals. We compare results against independent indicators such as import trends, category price ladders, and channel mix shifts, and then investigate outliers that appear when a single assumption changes the total too sharply.

Before sign-off, the model and narrative go through multi-step analyst reviews, and respondents are re-contacted when a variance cannot be explained through public data or earlier notes. The report is refreshed annually, and interim updates are triggered for material events such as policy changes affecting imports, major pricing resets, or sudden demand shocks. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Israel Home Appliances Market Size Compared Against Other Published Estimates

Published market sizes for Israel home appliances can look far apart, even when they are talking about similar products, because the study periods, value points in the chain, and what gets counted as an appliance sale are not aligned. Differences also come from how each publisher treats online pricing dispersion, exchange rate timing, and the split between major and small appliances.

One common source reports a broader consumer electronics style total, and another presents an annual snapshot that appears to mix Israel into a wider regional framing. In Mordor Intelligence, the count is limited to major and small home appliances sold in Israel across identified retail channels, and services and informal second-hand flows are kept out so the value tracks unit sales and practical ASPs.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 766.08 M (2026) | |

| Market Analytics Publisher A | USD 2.50 B (2025) | Uses an approximate annual value and presents Israel inside a broader regional structure, which can lead to wider scope capture and looser checks on what portion is strictly domestic appliance sell-through. |

| Market Dataset Publisher B | USD 462.50 M (2023) | Anchors on an earlier base year and applies a higher growth curve, and the method summary does not clearly separate new-unit revenues from adjacent spend items, which can shift the implied CAGR and total. |

The spread in the table is mainly explained by how tightly the study defines what qualifies as a counted appliance sale, and by the base year and growth path selected. Our approach stays traceable to household and housing demand signals, observed price bands, and channel reality checks, which makes the final number easier to reproduce and update with new evidence.

Key Questions Answered in the Report

What is the current size and growth outlook for the Israel home appliances space?

The Israel Home Appliances market size is USD 766.08 million in 2026 and is forecast to reach USD 904.20 million by 2031 at a 3.37% CAGR.

Which channels are expected to grow fastest in Israel for home appliances by 2031?

Online retail is forecast to grow at a 4.16% CAGR through 2031 as omnichannel models and reliable last-mile delivery expand consumer comfort with large-item purchases.

Which products are leading and which are growing quickest in Israel?

Refrigerators are the largest with 24.63% share in 2025, while coffee makers are projected to grow fastest at 3.92% CAGR through 2031.

Which Israeli regions show the strongest opportunity through 2031?

The Central District remains the largest at 41.93% share in 2025, and the Tel‑Aviv District shows the fastest growth at a projected 3.75% CAGR.

How are regulations shaping appliance offerings in Israel?

EU-aligned import reform streamlines approvals and expands high-efficiency offerings, and Extended Producer Responsibility adds take-back and recycling requirements that shape reverse logistics and product design.

What are the main supply risks that sellers in Israel should plan for?

Red Sea transit disruption, elevated freight costs, and currency management needs can extend lead times and raise working capital, making diversified sourcing and hedging policies important to preserve margins.

Page last updated on: