Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

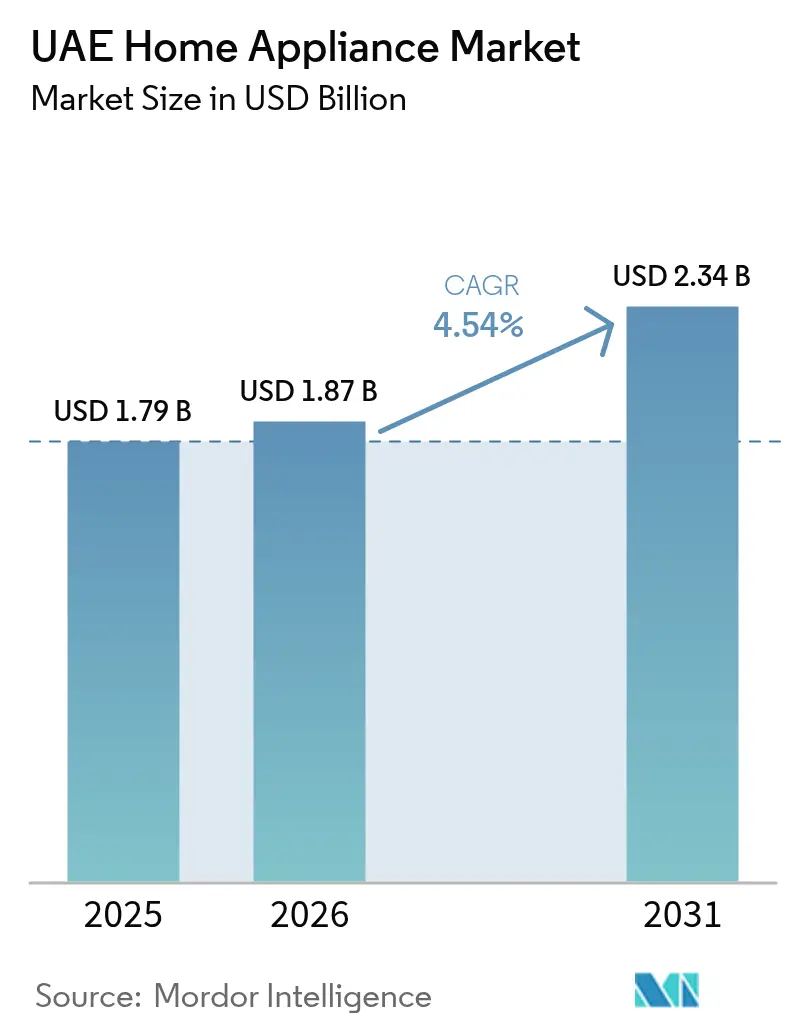

| Base Year Market Size (2025) | USD 1.79 Billion |

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.34 Billion |

| Growth Rate (2026 - 2031) | 4.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Home Appliance Market Analysis by Mordor Intelligence

The UAE home appliance market size was valued at USD 1.79 billion in 2025 and estimated to grow from USD 1.87 billion in 2026 to reach USD 2.34 billion by 2031, at a CAGR of 4.54% during the forecast period (2026-2031). Demographic expansion, especially in fast-growing mixed-use developments, continues to unlock demand, while energy-efficiency mandates accelerate replacement cycles and steer purchasing toward 5-star-rated models that reduce household electricity bills by up to 75% compared with legacy units[1]Dubai Electricity & Water Authority, “Energy Efficient Appliances,” DEWA.GOV.AE..

Infrastructure modernization linked to Dubai’s 10X strategy and Abu Dhabi’s digital transformation agenda is nurturing early adoption of connected appliances that communicate with smart-grid systems and demand-response programs. Retail channels are evolving in parallel; multi-branded stores hold scale advantages, yet rapidly maturing e-commerce networks supported by nationwide BNPL schemes and last-mile logistics upgrades are gaining share as consumers lean on AI shopping assistants for price discovery. Competitive intensity is tempered by moderate market concentration: the top five suppliers control 58.7% of sales, but smart-connectivity innovation and localization strategies are opening paths for challengers that can certify products under the Emirates Standards and Metrology Authority (ESMA) framework. Rising freight costs linked to Red Sea rerouting and classification complexity under the new 12-digit Integrated Customs Tariff system add supply-side friction, yet industry participants exhibiting agility in sourcing and inventory management continue to defend margins.

Key Report Takeaways

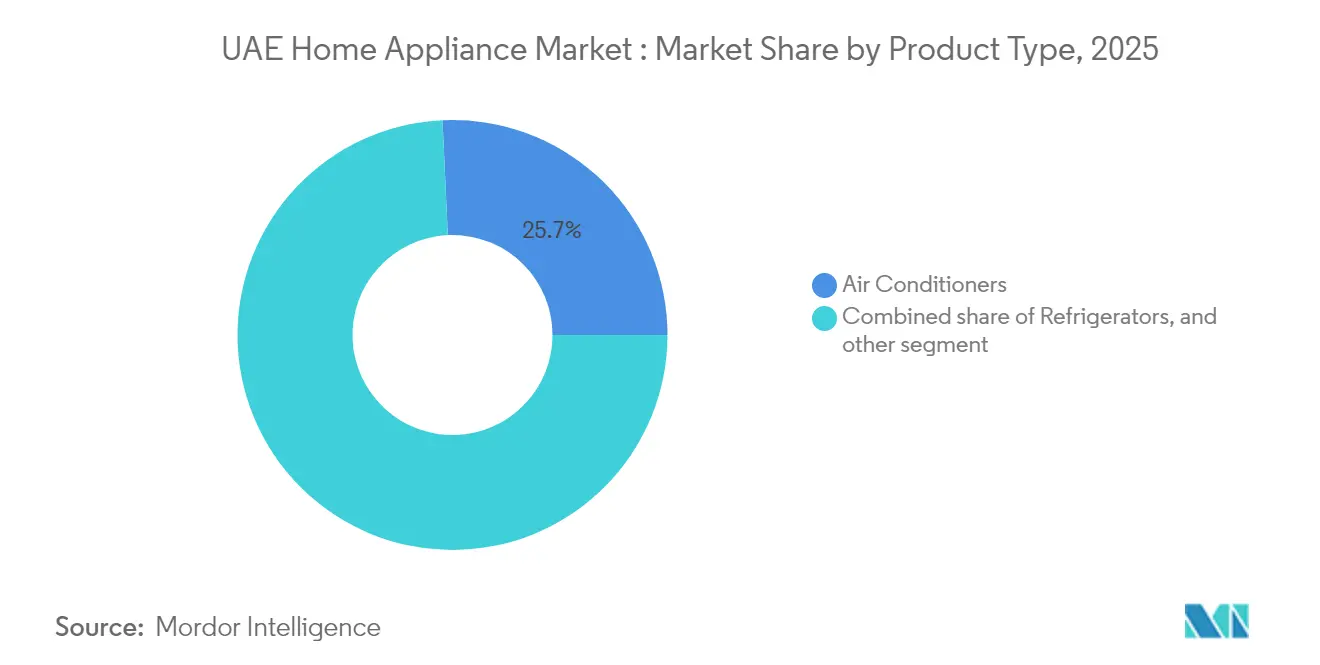

- By product type, air conditioners led with 25.74% revenue share in 2025, while smart refrigerators are projected to advance at a 13.00% CAGR to 2031.

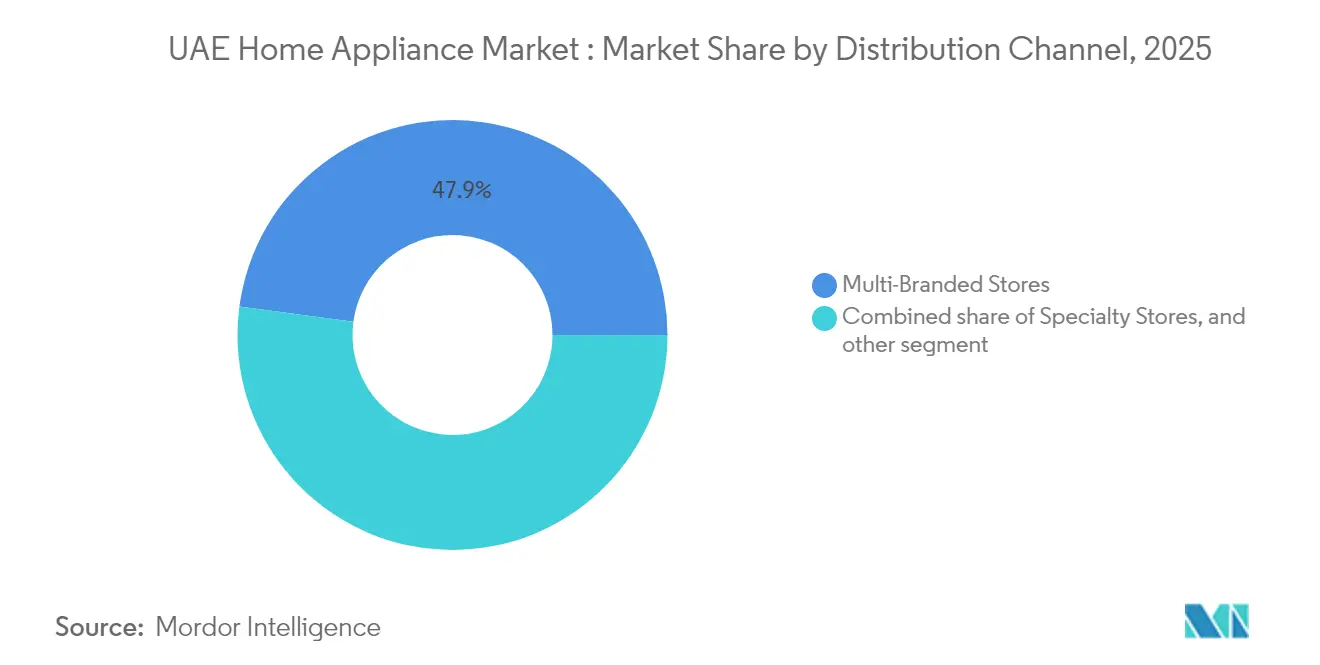

- By distribution channel, multi-branded stores held 47.88% of the UAE home appliance market share in 2025; e-commerce is poised for the fastest growth at a 15.95% CAGR through 2031.

- By technology, conventional appliances accounted for 63.95% of the UAE home appliance market size in 2025, yet smart/connected units are forecast to expand at 18.76% CAGR between 2026 and 2031.

- By geography, Dubai captured 39.85% of 2025 sales; Ras Al Khaimah and Fujairah are expected to record the highest CAGR at 10.63% over the same horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Home Appliance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in residential construction & expatriate population | +1.2% | National, concentrated in Dubai, Abu Dhabi, Sharjah | Medium term (2-4 years) |

| Energy-efficiency mandates driving replacement sales | +0.8% | National, ESMA compliance requirements | Long term (≥ 4 years) |

| E-commerce flash-sale events boosting unit volumes | +0.6% | National, Dubai and Abu Dhabi leading adoption | Short term (≤ 2 years) |

| Government smart-city initiatives spurring smart-appliance adoption | +0.7% | Dubai, Abu Dhabi, emerging in Northern Emirates | Long term (≥ 4 years) |

| Installment-based BNPL & salary-card financing widening consumer access | +0.5% | National, particularly benefiting mid-income expatriates | Medium term (2-4 years) |

| Real-estate driven demand for built-in premium cooking ranges | +0.3% | Dubai, Abu Dhabi luxury developments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Residential Construction & Expatriate Population

Abu Dhabi’s population climbed 7.5% to 4.14 million in 2024, coinciding with 29,415 new housing completions that translate directly into first-time appliance purchases [2]Statistics Centre – Abu Dhabi, “Population in 2024 Grows 7.5%,” SCAD.GOV.AE. . Developers are bundling fully-fitted kitchens and laundry spaces into lease packages to satisfy transient expatriate tenants, shifting buying power from individuals to bulk-procurement teams and amplifying volume orders for entry-level and mid-range models. Mixed-use megaprojects such as Al Dar’s Yas Bay integrate residential, commercial, and hospitality amenities, creating differentiated demand for compact dishwashers in serviced apartments and heavy-duty washers in hotel back-of-house facilities. Appliance specifications are increasingly codified at the blueprint stage to ensure compliance with ESMA’s 5-star energy benchmarks, thereby reducing post-handover retrofits and streamlining commissioning schedules. Government-backed smart-grid investments worth AED 7 billion mandate two-way data protocols, encouraging builders to pre-wire apartments for Wi-Fi–enabled cooling, cooking, and cleaning devices. This front-loaded specification approach cements pipeline visibility for suppliers and shrinks sales conversion cycles.

Energy-Efficiency Mandates Driving Replacement Sales

The ESMA labeling framework obliges retailers to phase out low-rated SKUs, funneling shoppers toward 4- and 5-star alternatives that carry higher ticket prices yet deliver a documented reduction of up to 30% in household electricity outlays [3]Dubai Electricity & Water Authority, “Smart Grid Initiative,” DEWA.GOV.AE. . Dubai Municipality’s Al Safat green-building code embeds appliance efficiency criteria into building audit checklists, compelling landlords to upgrade stock proactively to secure occupancy permits. Mortgage lenders have begun factoring projected utility savings into debt-service calculations, indirectly subsidizing premium appliance upgrades. Manufacturers now highlight “kilowatt-hour per cycle” metrics on point-of-sale materials and deploy augmented-reality apps that estimate lifetime energy expenses, reinforcing the payback narrative. The policy environment has shaved average replacement intervals for major white goods from eight years to roughly six, accelerating unit throughput for retailers.

E-Commerce Flash-Sale Events Boosting Unit Volumes

White-Friday, Ramadan-Weeks, and National-Day mega promotions compress seasonal demand into 48-hour digital windows that can equal a conventional retailer’s full-month turnover. Artificial-intelligence chatbots embedded on top-five platforms guide buyers through ESMA label interpretation and run personalized price-drop alerts, contributing to a 44% rise in AI-assisted purchases since 2024. Cross-border sellers capitalize on the UAE’s low 5% customs duty for fully-assembled appliances, but the duty-free threshold cut from AED 970 to AED 300 increased compliance costs and tilted the advantage toward domestic inventory positions. Warehousing operators in Dubai South free zone have responded by tripling last-mile capacity, enabling next-day delivery on bulky goods—a differentiator that brick-and-mortar rivals struggle to match. Flash-sale-driven spikes necessitate predictive demand-planning algorithms, prompting brands to collocate buffer stock within fulfillment centers.

Government Smart-City Initiatives Spurring Smart-Appliance Adoption

Dubai’s 10X strategy and the Mohammed bin Rashid Solar Park expansion require demand-side management that only grid-interactive devices can perform, turning connected refrigerators and HVAC systems from luxury accessories into functional infrastructure nodes. Abu Dhabi’s planned AI cognitive city, Aion Sentia, embeds appliance interoperability protocols at a district level, catalyzing OEM investment in Zigbee and Matter compliance modules. The National Policy for IoT Security, enforced since 2023, relieves cybersecurity anxiety by standardizing encryption baselines and incident-response workflows. Utilities offer time-of-use tariffs that reward smart-enabled washers capable of deferring cycles to off-peak windows, translating technology adoption into tangible bill savings. Appliance brands partner with telecom operators to bundle 24-month data plans, lowering barriers for renters to adopt smart features.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expats' high churn leading to second-hand market cannibalisation | -0.4% | National, particularly Dubai and Abu Dhabi | Medium term (2-4 years) |

| Import tariff volatility on steel & electronic components | -0.3% | National, affecting all price segments | Short term (≤ 2 years) |

| Rising logistics costs due to Red-Sea rerouting increasing retail prices | -0.2% | National, supply chain dependent | Short term (≤ 2 years) |

| Limited after-sales service network outside Dubai/Abu Dhabi | -0.3% | Northern Emirates, rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expats’ High Churn Leading to Second-Hand Market Cannibalisation

Employment contracts averaging 2-4 years prompt frequent relocations, generating a steady flow of lightly-used refrigerators, washers, and air conditioners into classifieds platforms that undercut new-product entry-level pricing. Peer-to-peer resale groups advertise appliances at 30-50% of original cost, appealing to tenants wary of long-term capital outlays. The informal secondary channel is further legitimized by third-party refurbishers offering twelve-month warranties, eroding value propositions of budget OEMs. Regulatory proposals to license refurbishment centers could formalize the segment, potentially creating trade-in programs but also deepening cannibalization.

Import Tariff Volatility on Steel & Electronic Components

The UAE's appliance market faces ongoing cost pressure from import tariff fluctuations affecting core manufacturing inputs, particularly steel and electronic components that comprise 60-70% of appliance production costs. The implementation of a new 12-digit Integrated Customs Tariff system starting August 2025, expanding from 7,800 to over 13,400 tariff codes, introduces classification complexity that could affect duty determination for appliance components. While the UAE maintains a standard 5% customs duty rate on most appliances, component-level tariffs can vary significantly, creating cost volatility for manufacturers who assemble products locally or import partially-assembled units. The reduction of Dubai's duty-free threshold from AED 970 to AED 300 in 2023 has increased compliance costs for smaller shipments, affecting spare parts and component imports that support local assembly operations. Global steel price volatility, exacerbated by geopolitical tensions and trade policy changes, creates challenges for appliance manufacturers who cannot easily pass through cost increases in the UAE's price-sensitive market segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cooling Solutions Drive Market Leadership

Air conditioners accounted for 25.74% of the UAE home appliance market in 2025, cementing their role as the backbone of household comfort in a climate where average summer temperatures exceed 42 °C. Energy Strategy 2050 goals and urban decarbonization roadmaps incentivize inverter-compressor adoption, allowing OEMs to differentiate through variable-speed efficiency gains. Hyperganic, Strata, and EOS unveiled a prototype unit targeting 10-fold efficiency improvement, signalling an impending leap rather than incremental progress. Refrigerators and washing machines sustain mid-20% combined share, benefiting from shorter replacement timelines catalyzed by ESMA’s labeling mandate. Smart refrigerators, projected to expand at 13.00% CAGR, leverage touchscreen interfaces and AI food-management apps to reduce waste, a feature that resonates with sustainability-minded millennials. Dishwashers and ovens remain niche but gain traction in premium developments where built-in aesthetics complement high-spec cabinetry. Small appliances flourish on e-commerce promotions, especially air fryers that echo healthy-eating narratives and coffee makers that ride the specialty-coffee boom among urban professionals. Commercial demand from the USD 7.63 billion domestic food-processing sector adds incremental volume for heavy-duty freezers and industrial mixers .

Convergence of product categories around connectivity is compressing innovation cycles. Air conditioners now integrate sensors to coordinate with smart blinds and thermostats, raising expectations for cross-product ecosystem harmony. Appliance makers are therefore bundling SDKs that allow third-party developers to plug devices into home-automation dashboards, boosting stickiness among tech-savvy buyers. After-sales monetization via subscription filters and cloud analytics for predictive maintenance is gaining traction, opening recurring-revenue avenues beyond one-off unit sales. This shift also drives warranty-extension uptake as consumers value manufacturer-certified firmware updates that guard cybersecurity integrity under the national IoT policy.

By Distribution Channel: Multi-Brand Dominance Faces Digital Disruption

Multi-branded showrooms maintained 47.88% share in 2025 thanks to floor-space scale, experiential displays, and bundled after-sales packages that remain persuasive for big-ticket purchases exceeding AED 2,000. In-store financing desks facilitate BNPL enrollment, capturing footfall that originates online but converts offline when buyers seek tactile reassurance on build quality. Nevertheless, e-commerce is set to outpace all other channels at 15.95% CAGR as platforms extend white-glove delivery, free installation, and hassle-free haul-away of old units. AI-powered configurators let shoppers visualize appliances inside virtual replicas of their apartment layouts, diminishing the need to visit physical outlets. Specialty boutiques that once thrived on niche Italian cooking appliances reposition as experience centers offering chef-led demonstrations to justify premium markups. Direct-to-consumer microbrands leverage social commerce to bypass retailers altogether, but logistics scale remains a barrier for bulky goods.

Institutional procurement—hotels, hospitals, and schools—forms a small yet stable slice, often serviced via project tenders where turnkey suppliers such as Whirlpool Middle East marshal broad portfolios. Stadium builds ahead of major sporting events funnel orders for industrial-grade refrigeration and laundry systems, adding counter-cyclical revenue streams that insulate distributors from household demand softness. Omnichannel integration is becoming non-negotiable: click-and-collect lockers inside hypermarkets extend pickup flexibility, and unified SKU identifiers across channels ensure real-time inventory accuracy, mitigating stock-out risk during flash sales.

By Technology: Smart Transformation Accelerates Despite Conventional Dominance

Conventional formats still represent 63.95% of the UAE home appliance market size in 2025 because resident segments prioritize reliability and user-friendly operation. However, the smart-connected subset, expanding at 18.76% CAGR, is siphoning share by coupling energy savings with lifestyle convenience. The National Policy for IoT Security alleviates hacking fears, while utility-backed demand-response rebates make the cost premium easier to justify. Over-the-air firmware updates prolong product relevance, nudging households toward a subscription mindset where appliances evolve post-purchase.

Energy-efficient appliances form a bridge between legacy and full smart capabilities. ESMA 5-star rated machines integrate advanced compressors and DC motors but may omit Wi-Fi modules, offering a mid-price steppingstone. Manufacturers employ modular design so owners can retrofit connectivity later, mitigating obsolescence anxiety. Component miniaturization unlocks slimmer form factors suited to tighter urban kitchens, a selling point in high-rise apartments where space optimization commands a premium. Marketing narratives have pivoted from horsepower and drum size to kilowatt savings and app ecosystem compatibility. In-app dashboards aggregate real-time energy metrics across devices, transforming appliances into data-generating nodes that inform household energy budgeting. This positioning reframes the purchase as an investment in utility-bill management rather than a discretionary upgrade.

Geography Analysis

Dubai’s 39.85% revenue leadership in 2025 owes much to its status as the UAE’s commercial hub, where expatriate professionals with disposable incomes gravitate toward premium, connected appliances that harmonize with smart-home ecosystems. Retail density along Sheikh Zayed Road ensures competitive pricing transparency, while free-zone incentives enable distributors to maintain hub-and-spoke logistics for regional re-exports. The emirate’s 10X smart-city blueprint mandates grid-interactive devices in new developments, fast-tracking adoption of dynamic-pricing compatible washers and HVAC systems. Tourism-driven hospitality pipelines inject incremental demand for commercial refrigeration, cooking, and laundry equipment, reinforcing Dubai’s centrality to supplier order books. Utility-administered time-of-use tariffs reward appliances capable of load-shifting, embedding a financial incentive into the upgrade narrative.

Abu Dhabi, the second-largest sub-market, leverages oil-sector wealth and public-sector employment stability to support a steady appliance revenue base. The emirate’s population uptick and 29,415 new housing deliveries in 2024 foster first-time purchase demand, while its USD 2.5 billion Aion Sentia AI-city project codifies appliance interoperability requirements at district scale. Government housing programs for Emirati nationals prefer 5-star-rated models, giving compliant brands a predictable tender pipeline. Abu Dhabi Distribution Company’s smart-meter rollout provides real-time consumption feedback to residents, reinforcing the merits of energy-efficient replacements.

Northern Emirates Sharjah, Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain—collectively trail on absolute size yet post the fastest growth, driven by rising affordability of housing and industrial diversification efforts. Ras Al Khaimah and Fujairah together are set to advance at 10.63% CAGR, buoyed by free-zone manufacturing clusters that attract a fresh expatriate labor pool requiring new living quarters and the associated appliance purchases. Logistics corridors improved by a USD 20.03 billion nationwide freight network expansion facilitate faster restocking cycles and lower last-mile costs, inching retail price parity toward Dubai levels. Limited after-sales footprints remain a bottleneck, prompting OEMs to pilot mobile-service vans equipped for on-site repairs.

Competitive Landscape

The market remains moderately concentrated, dominated by a handful of key players holding the significant share of the market. LG Electronics Gulf leads the pack, driven by its wide range of inverter air conditioners and the strength of its ThinQ app ecosystem. Samsung Gulf Electronics closely follows, leveraging its SmartThings platform to enhance user experience and appliance integration. This competitive dynamic reflects a growing focus on intelligent features and ecosystem compatibility. Regional players continue to carve out space by aligning with evolving consumer expectations for connected, energy-efficient solutions. Bosch-Siemens and Whirlpool Middle East secure mid-double-digit shares by leveraging European-quality positioning and localized after-sales centers. Haier Middle East rounds out the top tier with aggressive pricing on smart refrigerators tailored to ESMA 5-star benchmarks.

Localization initiatives have emerged as a differentiator. Rheem’s Dubai factory sources 70% of components locally, shaving lead times and buffering currency volatility. Partnerships such as Softlogic and Daikin’s joint pursuit of the USD 650 million commercial HVAC segment demonstrate the value of combining project-management expertise with tech leadership. Appliance makers are also experimenting with rental models aimed at expatriates wary of ownership friction, bundling service, upgrades, and removal into monthly fees. Solar-powered refrigerator pilots for remote worker camps indicate exploration of off-grid opportunities that align with national clean-energy ambitions. Compliance rigor remains a gatekeeper; ESMA certification costs deter opportunistic imports and encourage established players to deepen testing infrastructure, raising entry barriers.

Price wars occasionally flare during flash-sale seasons, but differentiation is increasingly anchored in software update cadence, AI-powered fault diagnostics, and interoperability with third-party platforms such as Amazon Alexa and Google Home. Brands that secure early integration within property-developer specifications tend to lock-in multiyear refresh cycles, granting a durable revenue moat.

UAE Home Appliance Industry Leaders

LG Electronics Gulf

Samsung Gulf Electronics

Bosch-Siemens Home Appliances

Whirlpool Middle East

Haier Middle East

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Siemens contracted to retrofit 60 UAE government buildings, deploying energy-efficient technologies projected to cut consumption by 27%.

- October 2024: DEWA reiterated commitment to Net-Zero 2050, highlighting solar-park expansion that strengthens the case for grid-interactive appliances.

- September 2024: Softlogic MEA and Daikin signed a strategic alliance to capture USD 650 million in commercial HVAC opportunities, focusing on turnkey solutions for real-estate megaprojects.

- July 2024: Sharp and Egypt’s Elaraby Group launched a refrigerator plant aimed at 500,000 units by 2027, reshaping MENA supply dynamics for large-capacity cold appliances.

UAE Home Appliance Market Report Scope

A complete background analysis of the United Arab Emirates Home Appliances Market, which includes an assessment of the National accounts, economy, and emerging market trends by segments, significant changes in the market dynamics, and the market overview, is covered in the report. The United Arab Emirates Home Appliances Market is segmented by Major Appliances (Refrigerators, Freezers, Dishwashing Machines, Washing Machines, Ovens, Air Conditioners, and Other Major Appliances), by Small Appliances (Coffee or Tea Makers, Food Processors, Grills & Roasters, Vacuum Cleaners, Other Small Appliances), and Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, E-Commerce and Other Distribution Channels). The report offers Market size and forecasts for the United Arab Emirates Home Appliances Market in value (USD) for all the above segments.

By Product Type

| Major Home Appliances | Refrigerators |

| Freezers | |

| Dishwashing Machines | |

| Washing Machines | |

| Ovens | |

| Air Conditioners | |

| Other Major Products (Electric Hobs, Ranges, etc.) | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Toasters | |

| Vacuum Cleaners | |

| Juicers & Blenders | |

| Other Small Appliances (Waffle Makers, Air Fryers, etc.) |

By Distribution Channel

| Multi-Branded Stores |

| Specialty Stores |

| E-Commerce |

| Other Distribution Channels |

By Technology

| Smart / Connected Appliances |

| Energy-Efficient (?5-Star, Inverter) Appliances |

| Conventional Appliances |

By Geography

| Dubai |

| Abu Dhabi |

| Sharjah & Ajman |

| Ras Al Khaimah & Fujairah |

| Umm Al Quwain |

| By Product Type | Major Home Appliances | Refrigerators |

| Freezers | ||

| Dishwashing Machines | ||

| Washing Machines | ||

| Ovens | ||

| Air Conditioners | ||

| Other Major Products (Electric Hobs, Ranges, etc.) | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Toasters | ||

| Vacuum Cleaners | ||

| Juicers & Blenders | ||

| Other Small Appliances (Waffle Makers, Air Fryers, etc.) | ||

| By Distribution Channel | Multi-Branded Stores | |

| Specialty Stores | ||

| E-Commerce | ||

| Other Distribution Channels | ||

| By Technology | Smart / Connected Appliances | |

| Energy-Efficient (?5-Star, Inverter) Appliances | ||

| Conventional Appliances | ||

| By Geography | Dubai | |

| Abu Dhabi | ||

| Sharjah & Ajman | ||

| Ras Al Khaimah & Fujairah | ||

| Umm Al Quwain | ||

Key Questions Answered in the Report

How large is the UAE home appliance market in 2025?

How large is the UAE home appliance market in 2025?

What is the expected CAGR for UAE appliance sales to 2031?

Revenue is forecast to grow at a 4.54% CAGR through 2031.

Which product type leads in UAE household appliance demand?

Air conditioners dominate with 25.74% share thanks to the country’s extreme climate.

How fast is e-commerce growing as an appliance sales channel?

Online sales are projected to expand at 15.95% CAGR between 2026 and 2031.

Why are smart appliances gaining traction in the Emirates?

Smart-city initiatives, utility rebates, and the National Policy for IoT Security are driving adoption of connected, energy-efficient devices.

Page last updated on: