Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

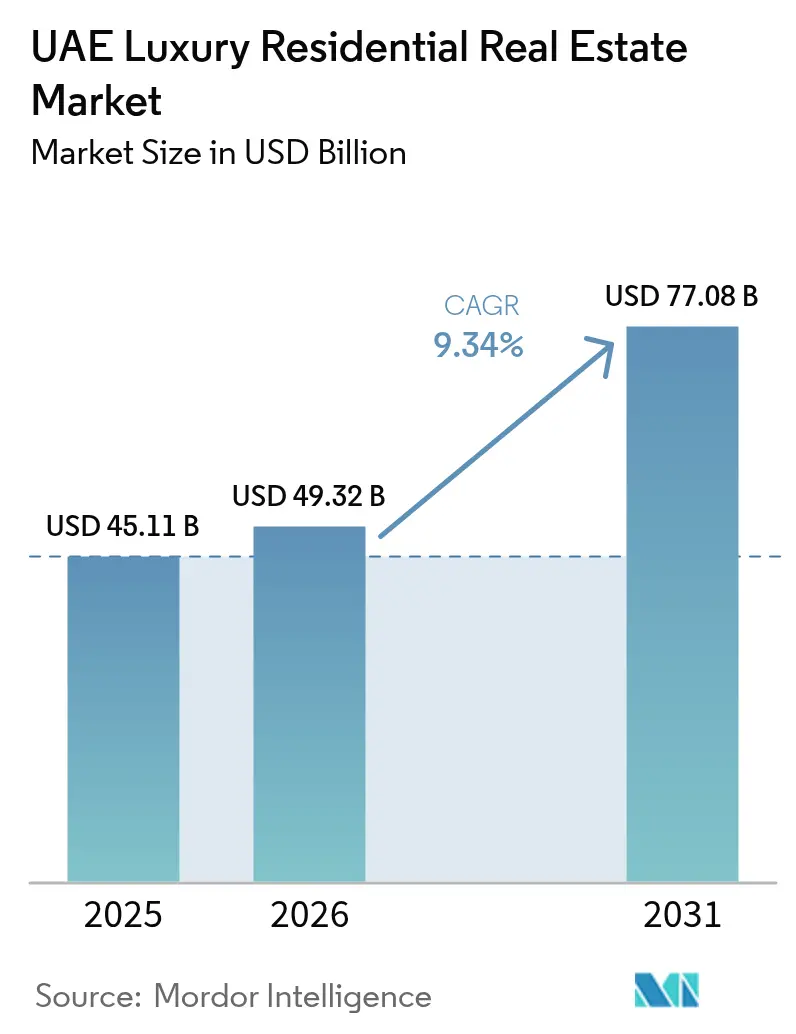

| Base Year Market Size (2025) | USD 45.11 Billion |

| Market Size (2026) | USD 49.32 Billion |

| Market Size (2031) | USD 77.08 Billion |

| Growth Rate (2026 - 2031) | 9.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Luxury Residential Real Estate Market Analysis by Mordor Intelligence

UAE luxury residential real estate market size in 2026 is estimated at USD 49.32 billion, growing from 2025 value of USD 45.11 billion with 2031 projections showing USD 77.08 billion, growing at 9.34% CAGR over 2026-2031. Demand springs from steady millionaire migration, policy‐backed foreign ownership rights, and a pipeline of mega-projects that reshape urban skylines. Luxury homes valued above USD 10 million changed hands 435 times in 2024, confirming the country’s global leadership in ultra-prime transactions. Rental yields in Dubai’s premier districts averaged 8-12%, markedly higher than traditional safe-haven cities, which draw income-oriented investors. Government plans such as the Dubai 2040 Urban Master Plan and Abu Dhabi Vision 2030 underpin infrastructure spending, anchoring long-term housing demand while supporting developers’ balance sheets.

Key Report Takeaways

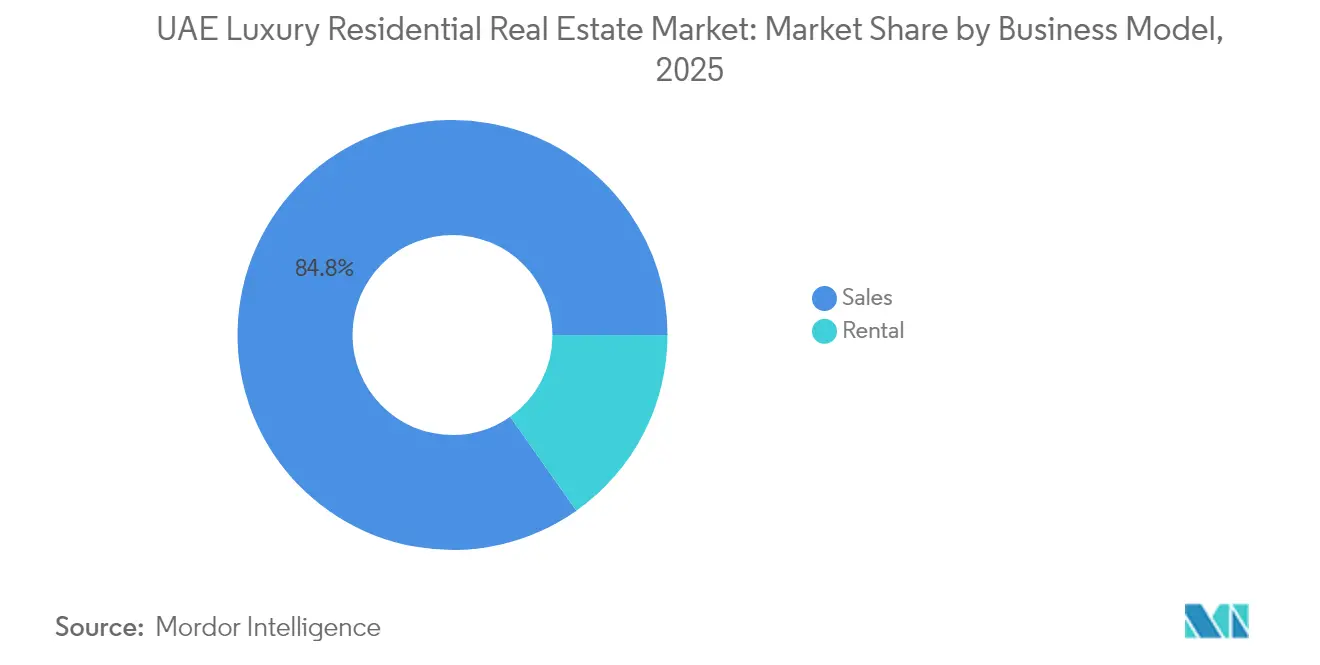

- By business model, the sales segment led with 84.78% revenue share in 2025; rentals are set to expand at a 10.06% CAGR through 2031.

- By property type, apartments and condominiums captured 52.75% of the UAE luxury residential real estate market size in 2025 and are projected to grow at a 10.22% CAGR through 2031.

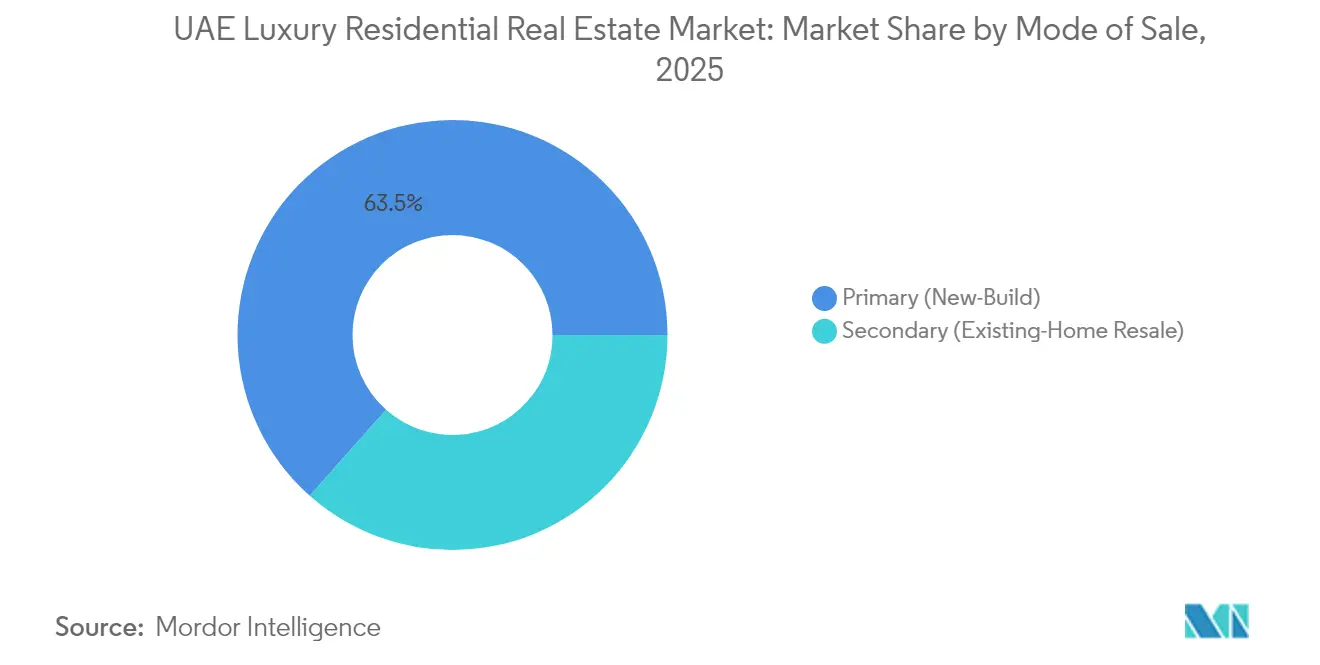

- By mode of sale, primary transactions commanded 63.45% of the UAE luxury residential real estate market size in 2025, advancing at a 9.96% CAGR over the forecast horizon.

- By city, Dubai accounted for a 64.35% UAE luxury residential real estate market share in 2025, whereas Abu Dhabi is forecast to post the fastest growth at a 10.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Luxury Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflow of high-net-worth individuals | +2.8% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Golden Visa and freehold expansion | +2.1% | Nationwide | Long term (≥ 4 years) |

| Mega-projects and branded waterfronts | +1.9% | Dubai core, Abu Dhabi spill-over | Long term (≥ 4 years) |

| Second-home and investment demand | +1.6% | Prime coastal districts | Medium term (2-4 years) |

| Smart, sustainable, wellness living | +1.3% | Premium districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong inflow of high-net-worth individuals driving luxury housing demand

Net-millionaire migration to the UAE jumped 67.5% between 2022 and 2024, bringing 6,700 new wealthy residents who promptly entered the luxury buyer pool. Their arrival fueled record sales of 435 homes priced above USD 10 million, elevating Dubai to the top spot for ultra-prime deals. Chinese buyers now represent 14% of all foreign luxury purchasers, while Russian, Indian, and European investors supply another 45% of transactions. Limited inventory in enclaves such as Emirates Hills and Palm Jumeirah tightened further as luxury villa listings fell 65% year over year. Family offices established by these new residents add persistent demand for multiple high-end residences across the Emirates.

Government initiatives expanding international buyer access

The Golden Visa now extends 10-year residency to property purchases above AED 2 million (USD 545,000), removing previous down-payment hurdles and boosting foreign participation. Dubai’s freehold zones have widened to cover 60% of prime areas versus 35% in 2020, while Abu Dhabi grants 100% foreign ownership in designated districts. Capital inflows mirrored the policy shift; Abu Dhabi recorded AED 3.28 billion (USD 895 million) in new real-estate FDI during H1 2024 alone. Regulatory clarity and the UAE’s delisting from the FATF Grey List in April 2024 strengthened institutional confidence.

Mega-projects creating branded residences and waterfront communities

Developments exceeding USD 100 billion are under construction, with roughly 40% earmarked for upscale housing. Emaar’s USD 5.72 billion (AED 21 billion) Heights Country Club and Grand Club Resort highlights the scale of integrated luxury precincts. Aldar’s USD 1.85 billion (AED 6.8 billion) Al Fahid Island will deliver 7,000 premium residences, while the firm’s broader Mubadala partnership oversees USD 8.17 billion (AED 30 billion) of coastal assets. Branded projects such as Bugatti Residences and Six Senses Marina command 15-25% price premiums, emphasizing the branding effect on buyer willingness to pay.

Preference for smart, sustainable, and wellness-integrated developments

Around 72,000 UAE buildings already meet green standards, and 35% of new luxury projects are targeting LEED certification by 2025. The Sustainable City’s zero-energy villas maintain full occupancy and spotlight the commercial viability of net-zero concepts. Wellness-centric projects enjoy price premiums of up to 15%, evidenced by a USD 34.0 million (AED 125 million) penthouse at Arada’s Akala destination. Developers routinely embed IoT, electric-vehicle charging, and biophilic design to compete for health-conscious elites[1]Yousif Al Mutawa, “Green Building Regulations & Specifications 2025 Update,” Dubai Municipality, dm.gov.ae.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High project costs and imported materials | -1.8% | Nationwide | Short term (≤ 2 years) |

| Potential oversupply in prime districts | -1.2% | Dubai, Abu Dhabi | Medium term (2-4 years) |

| Global economic and currency volatility | -0.9% | All emirates | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Risk of oversupply in prime luxury segments

Dubai could deliver 78,000 new homes by 2028, but only 368 lie in core prime areas, raising price-volatility concerns. Fitch projects up to a 15% correction between H2 2025 and 2026 following a 60% jump since 2022. Off-plan sales make up 71% of luxury deals, concentrating delivery risk in 2026-2028.

Global economic volatility is affecting foreign buyer sentiment

Currency shifts influence 60% of foreign buyers, especially Europeans and Asians holding non-USD assets. While the UAE luxury residential real estate market remains largely cash-driven, new Central Bank rules raising mortgage down payments could dampen leverage-based purchases[2]Khaled Mohamed Balama, “Mortgage Loan-to-Value Ratios—Circular No. 14/2024,” Central Bank of the U.A.E., cbuae.gov.ae. The country’s neutral diplomacy and projected 5.1% GDP growth for 2025 cushion these shocks[3]International Chamber of Commerce U.A.E., “The UAE’s Trade-Driven GDP Outlook 2025,” ICC-UAE, iccuae.ae.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Rental momentum builds under sales dominance

Sales still controlled 84.78% of all 2025 value as investors favored outright ownership for capital appreciation plays. The rental segment, however, is forecast to rise at a 10.06% CAGR as multinational corporations relocate staff and expatriate numbers swell. Luxury rents in Palm Jumeirah and Dubai Marina climbed 20.8% last year, and the Smart Rental Index introduced in 2025 improved price transparency, motivating institutional landlords. Short-term rentals achieve 85% seasonal occupancy and 7% annual yields, further widening investor options. Cash remains king; 70% of acquisitions close without financing, reflecting the affluent profile of buyers and limiting interest-rate sensitivity. Off-plan commitments within the sales channel reach 71%, locking in forward demand but creating hand-over concentration risk between 2026 and 2028.

By Property Type: Apartments retain both size and pace leadership

Apartments and condominiums held a 52.75% share of 2025 transactions and are forecast to expand at a 10.22% CAGR, keeping them the UAE luxury residential real estate market’s growth engine. Branded towers such as Six Senses Marina secure 15-25% premiums, underscoring investor fascination with hospitality affiliations. Villas, although smaller in volume, posted a 94% price surge since Q1 2020 as ultra-high-net-worth individuals prioritize space and privacy. Penthouses push record tags, with a USD 34.0 million (AED 125 million) sale ranking among Dubai’s top deals for 2025. Townhouses in master-planned estates bridge affordability gaps, serving family buyers who value community amenities yet desire prestige.

By Mode of Sale: Primary pipeline reflects developer strength

Primary sales captured 63.45% of market value in 2025 and are tracking a 9.96% CAGR toward 2031 as developers unveil ever-larger integrated communities. Off-plan buyers anticipate 20-30% capital gains before handover thanks to pre-launch pricing incentives and fee waivers. Secondary deals retain relevance where ready inventory is scarce, particularly for villas in Emirates Hills and Palm Jumeirah, where active listings fell 65% last year. RERA escrow rules and milestone-linked payment plans instill confidence, boosting absorption rates for new launches.

Geography Analysis

Dubai retained a commanding 64.35% slice of the UAE luxury residential real estate market in 2025, supported by legacy districts such as Downtown Dubai that deliver 7-8% gross yields and Palm Jumeirah, where villa prices leaped 49.4% in 2022. The Dubai 2040 Urban Master Plan projects the city’s headcount rising from 3.3 million to 5.8 million, nearly quadrupling public beachfront length and adding vast tourism zones that underpin waterfront home demand.

Abu Dhabi is the growth pacesetter at a 10.41% CAGR to 2031, buoyed by USD 8.17 billion (AED 30 billion) in Aldar-Mubadala coastal assets and a USD 1.85 billion (AED 6.8 billion) Al Fahid Island scheme for 7,000 luxury units. Rental yields average 6.5% for upmarket apartments, peaking at 6.85% on Al Reem Island. Cultural capital initiatives such as Louvre Abu Dhabi, plus the rumored Disneyland Abu Dhabi at Yas Island, amplify lifestyle appeal.

Sharjah positions itself as the cost-effective alternative, opening freehold rights that attracted buyers to the Aljada and Masaar communities. Ras Al Khaimah leverages tourism magnets; the USD 1.06 billion (AED 3.9 billion) Wynn resort anchors Al Marjan Island, driving 20.7% price appreciation in select precincts. Meanwhile, Sobha Realty’s Sobha Siniya Island project in Umm Al Quwain targets niche ultra-luxury demand for exclusive waterfront mansions.

Regulatory Landscape

The UAE luxury residential real estate market operates through emirate-level oversight, with local regulators managing registration, licensing, and investor protections. In Dubai, the Dubai Land Department (DLD) and its Real Estate Regulatory Agency (RERA) anchor the regime, with Dubai Law No. 7 of 2006 requiring that real estate dispositions be registered with DLD to be legally effective, while RERA escrow and off-plan registration rules shape primary-market confidence.

In Abu Dhabi, the Abu Dhabi Real Estate Centre (ADREC) regulates the sector under Abu Dhabi Law No. 3 of 2015, covering developers, brokers, and jointly owned property management. Across the Northern Emirates, frameworks are also tightening, including Ras Al Khaimah Law No. 12 of 2023 on regulating real estate development, which sets requirements such as developer and project registration and escrow accounts and adds institutional-style protections in newer luxury corridors.

Value Chain Analysis

The UAE luxury residential value chain begins with land origination and master planning, then moves into permitting and off-plan structuring under emirate regulators. Design, procurement, and construction execution are led by large developers (for example, Emaar, Aldar, Nakheel, and DAMAC) and tier-one contractors.

Contractor awards and program announcements in 2026 show how pipeline creation and delivery capacity sit at the center of the chain, with Nakheel awarding about AED 3.5 billion in villa contracts for Palm Jebel Ali and Aldar unveiling Yas Point (AED 6 billion) with 1,600 branded residences. These projects draw demand for high-spec materials, fit-out specialists, and hospitality-style service partners. Sales and distribution typically run through developer direct channels, broker networks, and increasingly digital enablement supported by DLD initiatives, while post-handover operations shift to property management and owners association management under jointly owned property rules. Input risks are concentrated in imported premium finishes and global logistics, and in 2026 contractors and developers managed rerouting and inventory buffering (two to six months of materials cited by Moody's for UAE construction), with some developers expanding in-house construction capabilities to manage timelines, quality, and margin amid volatile materials and labor conditions.

Competitive Landscape

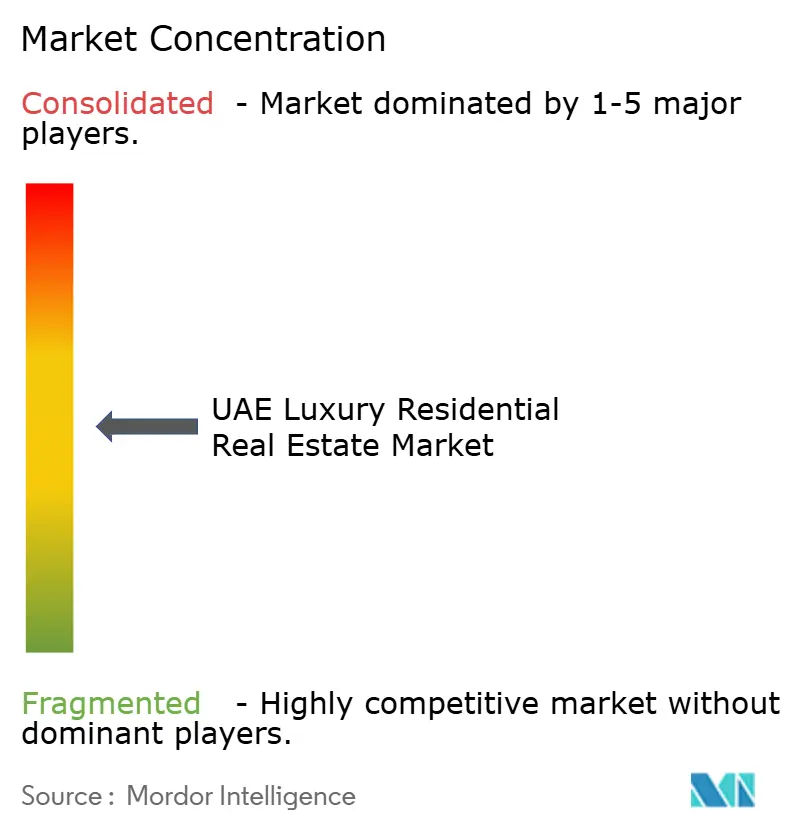

Market concentration is moderate. Emaar Properties leads after reporting USD 12.5 billion in H1 2025 sales and committing USD 5.72 billion (AED 21 billion) to fresh mega-projects. Aldar’s extended AED 30 billion partnership with Mubadala strengthens Abu Dhabi's dominance. Modon Holding collaborates with Candy Capital to chase the uber-luxury niche. Developers compete by securing hospitality brands, adopting proptech, and emphasizing ESG credentials. Dubai Land Department’s tokenization pilot envisions a USD 16 billion blockchain titling market, potentially altering transaction processes and granting tech-savvy players an edge. Compliance capabilities grew in importance after the UAE’s FATF delisting, advantaging large developers with robust governance structures.

UAE Luxury Residential Real Estate Industry Leaders

Emaar Properties

Aldar Properties

Nakheel

DAMAC

Dubai Holding

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Ultra-prime depth and liquidity in Dubai create room for additional product at the intersection of waterfront scarcity and branded living, supported by transaction momentum visible in early 2026. Dubai Land Department reported Q1 2026 real estate transactions of AED 252 billion (+31% year on year), and the luxury bracket above AED 10 million recorded 2,148 transactions in Q1 2026 (+62.6% versus Q1 2025). This supports room for more high-ticket inventory and differentiated formats, including penthouses, limited-edition villas, and hospitality-branded residences beyond traditional prime districts.

Technology-enabled transaction and asset operations also create opportunity as government-backed platforms and programs move from pilots toward commercialization. The DIFC and DLD partnership around the Dubai PropTech Hub and the PropTech 2033 roadmap targets AED 53 billion in annual productivity and supports a large local proptech base (231 UAE-based companies), giving developers, brokers, and landlords a more direct path to adopt tools for due diligence, compliance workflows, leasing automation, and tenant service. In parallel, evolving legal and regulatory scaffolding, including the federal property framework update effective 1 June 2026 and continued emirate-level escrow and registration enforcement, supports product concepts such as tokenized ownership structures and more standardized institutional participation, subject to regulator approvals and implementation timelines.

Recent Industry Developments

- July 2026: Aldar unveiled Yas Point on Yas Island, an AED 6 billion waterfront destination that includes 1,600 branded residences alongside hospitality and lifestyle components. The launch adds sizable branded supply to Abu Dhabi and reinforces the shift toward master-planned, experience-led luxury communities that compete with Dubai for global buyers.

- June 2026: Nakheel released the next phase of Palm Central Private Residences on Palm Jebel Ali, comprising 222 residences. The release advances Palm Jebel Ali from infrastructure and contracting into sellable beachfront inventory, expanding Dubai's pipeline of waterfront luxury product tied to long-dated master plan delivery.

- July 2025: Arada sold The Observatory penthouse at Akala for AED 125 million (USD 34.0 million), highlighting price premiums for wellness-integrated luxury concepts. The transaction reinforced developer focus on amenity-heavy, lifestyle-positioned residences as a lever to sustain ticket sizes amid broader supply additions.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value of luxury residential property activity in the UAE, captured through sales and rental value across high-end homes transacted in the country's prime locations.

Scope exclusions: This sizing does not include commercial real estate, land-only transactions, or pure hospitality stay revenues that are not tied to a residential unit.

Segmentation Overview

- By Business Model

- Sales

- Rental

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting picture of demand, supply, and pricing for luxury homes across the UAE. We first anchored the model using non-paywalled, official sources that show transaction direction and macro context, then layered in market materials to understand how luxury homes are positioned and sold.

Common inputs came from public sources such as the Dubai Land Department transaction statistics, Abu Dhabi Department of Municipalities and Transport reporting, Central Bank of the UAE releases (credit and mortgage direction), Federal Competitiveness and Statistics Centre datasets (population and household indicators), and UAE government open-data portals where available. We also reviewed planning and development updates from local authorities, along with annual reports, investor presentations, and press releases from listed developers and major brokerages to interpret pipelines, launch timing, and typical pricing language. In addition, paid database subscriptions for company financials and intelligence, news and financials, and global contracts and tenders were used selectively to standardize disclosures and track large project announcements. The sources listed here are illustrative, and many other public documents were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what is treated as luxury in day-to-day transactions, how pricing is typically negotiated, and how active demand shifts between new launches and resale stock. We spoke with developers, brokers, property managers, valuers, and local market advisers so secondary signals could be cross-checked across emirates.

These discussions also helped validate the split between apartments and villas, the share of waterfront and branded inventory within luxury, and the practical pace of absorption in key communities before forecasts were finalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | |

| Mid tier: 41% | Functional/Unit leaders: 40% | |

| Smaller Players: 22% | Managers: 45% |

Market-Sizing & Forecasting

The core sizing logic used a top-down and bottom-up approach, where emirate and city residential transaction values and rental value indicators were reconstructed, then filtered down to the luxury share using observed price bands, unit mix, and location concentration. We then corroborated these totals with selective bottom-up approximations, including sampled project price lists matched with unit counts, channel checks on resale deal sizes, and developer roll-ups where disclosures were clear.

Key model inputs included luxury transaction value trends in Dubai and Abu Dhabi, new launch volumes and expected handover schedules, mix shifts between apartments or condominiums versus villas and landed houses, primary versus secondary market share, and rental yield movements that influence investor appetite. Where direct luxury splits were not available, proxy rules were applied using consistent thresholds by community, followed by adjustments after interviews confirmed what was realistic for each emirate.

For forecasting, scenario analysis was used, with variables such as expected inflows of high net worth residents, mortgage rate direction and liquidity signals, supply delivery timing, and foreign buyer policy stability being stress-tested. Final year projections were produced only after the scenario outputs aligned with interview feedback on absorption pace and achievable pricing progression.

Data Validation & Update Cycle

Validation was done through cross-checks to keep the model aligned with real market signals. We compared outputs against independent indicators such as recorded transaction values, changes in average price per square foot in prime areas, and known handover schedules, then investigated any sharp variances that did not match market narratives.

A multi-step internal review followed, where assumptions were re-checked and a second analyst reviewed the math and the logic behind luxury share estimates. When a material event changed market conditions, such as a policy update or a sudden shift in financing costs, relevant experts were re-contacted to re-test the most sensitive inputs. Reports are refreshed annually, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's UAE Luxury Residential Real Estate Market Size Compared With Other Published Estimates

Published market numbers for UAE luxury homes often vary because each publisher applies the luxury definition differently, and because sales and rental value can be treated in different ways. Differences also show up when the mix of cities is handled unevenly, since Dubai's activity can dominate totals if the rest of the UAE is not sized with equal care.

Serviced apartment stay revenues and hotel-like income streams are sometimes grouped into luxury residential totals, even though those cash flows track hospitality demand more closely than home ownership or leasing. That can widen the spread between estimates. Those hospitality-linked revenues sit outside Mordor Intelligence's scope, and the market value is kept tied to residential sales and rental value by emirate and by property type, followed by checks against recorded transaction value and project delivery timing.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 45.11 B (2025) | |

| Industry Research Publisher A | USD 25.38 B (2025) | Uses a narrower property-type basket (for example, penthouses and select trophy assets) and can undercount wider luxury apartments and villas across multiple emirates, which reduces total captured value. |

| Industry Research Publisher B | USD 15.80 B (2024) | Often anchors on select prime districts and a high price-band definition, and the year reference differs, which can miss broader luxury resale and rental value captured across the UAE. |

Across the three figures, the spread mainly comes from how wide the luxury label is applied, whether rental value is fully counted, and how consistently the non-Dubai emirates are included. By keeping inputs traceable to transaction value signals, unit mix, and delivery schedules, the estimate remains easier to reconcile with what market participants see in real deals.

Key Questions Answered in the Report

How large is the UAE luxury residential real estate market in 2026?

The market reached USD 45.11 billion in 2025 and is on track to surpass USD 49.32 billion in 2026, keeping pace with a projected 9.34% CAGR.

Which city captures the biggest share of high-end property transactions?

Which city captures the biggest share of high-end property transactions?

What rental yields can investors expect from prime Dubai neighborhoods?

Gross yields in top locations such as Dubai Marina and Palm Jumeirah range from 8-12%, outpacing most global luxury hubs.

How do government visas influence foreign property demand?

The 10-year Golden Visa now ties to property investments above AED 2 million (USD 545,000), boosting long-term residency purchases.

Page last updated on: