Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

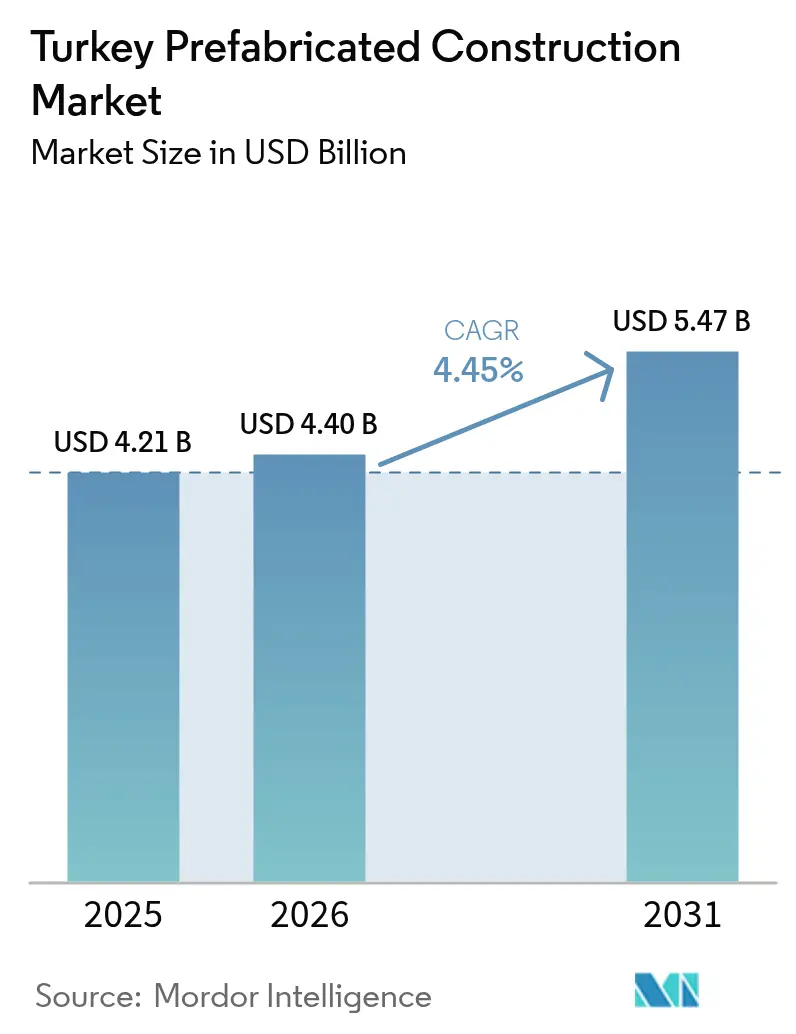

| Base Year Market Size (2025) | USD 4.21 Billion |

| Market Size (2026) | USD 4.4 Billion |

| Market Size (2031) | USD 5.47 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

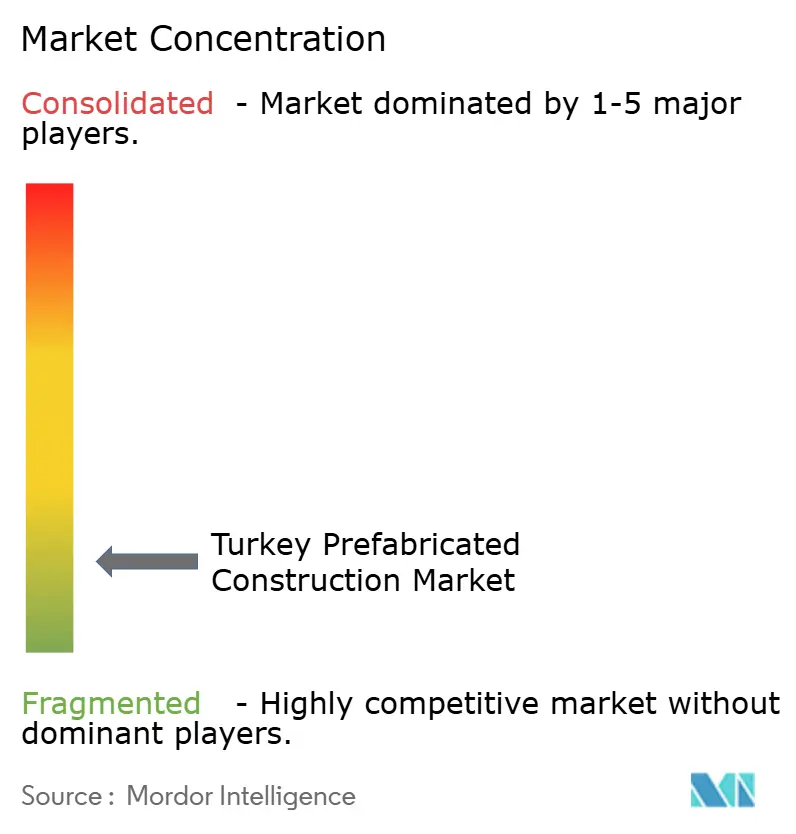

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Prefabricated Construction Market Analysis by Mordor Intelligence

The Turkey Prefabricated Construction Market size was valued at USD 4.21 billion in 2025 and estimated to grow from USD 4.4 billion in 2026 to reach USD 5.47 billion by 2031, at a CAGR of 4.45% during the forecast period (2026-2031). Post-earthquake reconstruction mandates, tighter TBEC-2018 seismic rules, and a national pledge to deliver 453,000 replacement homes within two years are anchoring near-term demand. Developers also face the April 2025 rollout of TS 825, which widens Turkey’s climate zones from four to six and raises insulation thresholds, pushing them toward factory-insulated panel systems that eliminate on-site labor bottlenecks. While concrete still dominates structural choices, new timber rules, energy-efficiency incentives, and near-EU supply-chain needs are opening space for steel-frame and modular solutions. Cost control remains pivotal amid 50% policy rates, triple-digit Lira depreciation since 2021, and a construction-cost index that quintupled in three years, steering contractors with hard-currency export books toward the domestic rebuild pipeline.

Key Report Takeaways

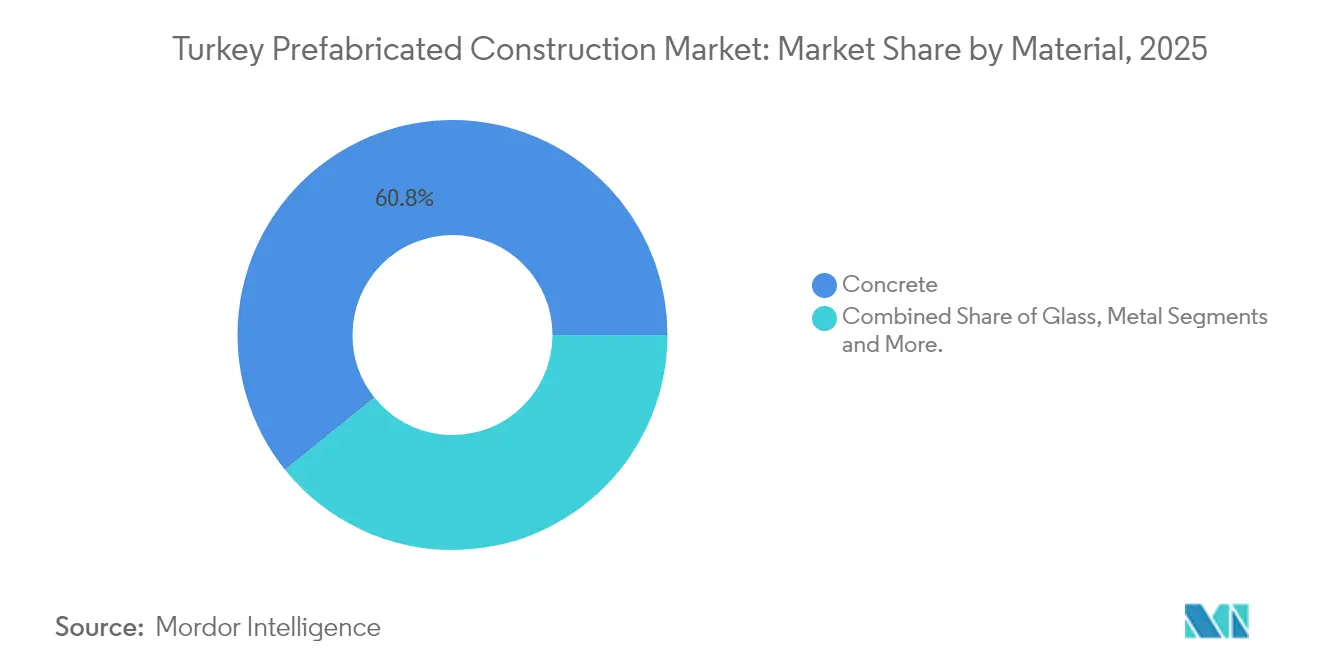

- By material, Concrete captured 60.78% of the Turkey prefabricated construction market share in 2025, while timber is set to expand at a 5.02% CAGR to 2031.

- By application, Residential applications held 44.35% of the Turkey prefabricated construction market size in 2025; the “Others” segment, led by military and disaster-relief demand, is advancing at a 5.37% CAGR through 2031.

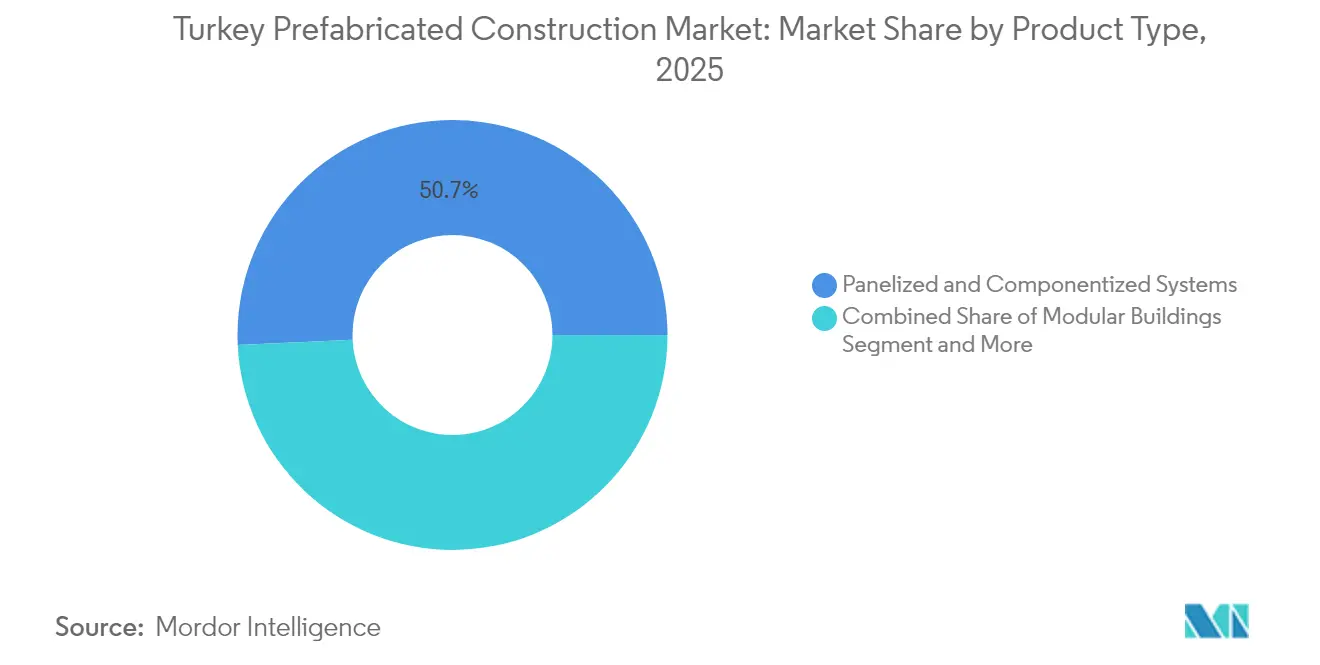

- By product type, Panelized systems commanded 50.74% of the Turkey prefabricated construction market share in 2025, whereas modular units are forecast to rise at a 5.74% CAGR to 2031.

- By geography, Istanbul generated 36.28% of total demand in 2025, yet Izmir is projected to grow fastest at 5.86% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Turkey Prefabricated Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Seismic reconstruction under TBEC-2018 | +1.2% | 11 earthquake-hit provinces | Short term (≤ 2 years) |

| Affordable-housing and urbanization push | +0.9% | Istanbul, Ankara, Izmir, nationwide urban zones | Medium term (2-4 years) |

| Near-EU manufacturing & logistics expansion | +0.7% | Marmara and Aegean regions, 18 free zones | Medium term (2-4 years) |

| Rapid-delivery public assets | +0.6% | National, focused on rural clinics, schools, military bases | Short term (≤ 2 years) |

| Energy-efficiency upgrades & export openings | +0.8% | Nationwide; EU and MENA export corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Seismic Reconstruction Under TBEC-2018

Turkey’s 2023 earthquakes damaged 680,000 dwellings, prompting a USD 44 billion reconstruction program that privileges fast, factory-built systems. TBEC-2018 legitimizes prefabricated concrete, steel, and timber by assigning ductility and R-factors distinct from cast-in-place rules. Contractors saving weeks on shell erection are winning TOKİ lots and municipal school tenders, while the World Bank’s SREEP pilot shows retrofitted prefab panels can cut retrofit timelines by half. Provincial tax breaks tied to completion by 2027 compress the project window, heightening urgency. Suppliers that lock in material hedges and scalable logistics are positioned to capture this concentrated demand pulse.

Affordable-Housing and Urbanization Push

TOKİ has delivered more than 1.06 million social units since 2003, embedding panelized and tunnel-form systems into public procurement[1]Housing Development Administration of Turkey, “TOKİ Programs,” toki.gov.tr. Istanbul’s urban-renewal grant of EUR 65,000 (USD 71,500) per flat pulls lower-income households toward standardized floorplates that suit light-steel and sandwich-panel solutions. EY projects building revenue will climb from EUR 61 billion (USD 67.1 billion) in 2024 to up to EUR 77 billion (USD 84.7 billion) by 2027, yet 41-43% mortgage rates pressure buyers to favor smaller footprints. Prefabrication’s cost and speed benefits help bridge the affordability gap. However, concrete’s premium image in mid-rise segments still tempers adoption, indicating prefab suppliers must broaden design palettes to win private developers.

Near-EU Manufacturing & Logistics Expansion

Turkey’s 2024-2028 FDI plan targets 1.5% of global inflows, prioritizing automotive, electronics, and green-energy factories that need quick-build sheds, dormitories, and offices. Karmod’s 3,388 m² Hatay camp, built in 39 days, showcases schedule compression that appeals to export-oriented industrial zones. Railway upgrades capturing 55% of the 2025 logistics budget are spawning warehouse clusters near Izmit and Tekirdağ ports. Prefabricated steel frames and insulated panels dominate these projects because they allow commissioning within one quarter, a key metric for foreign lessees. Captive power modules and PV-ready roofs bundled into volumetric units further sweeten the value proposition for climate-FDI investors.

Rapid-Delivery Public Assets

AFAD’s deployment of 10,000 container homes after the 2023 quakes set a template for off-budget emergency procurements that favor stock designs with pre-approved fire and seismic certificates. Health PPPs, such as the 1,038-bed Elâzığ Hospital carrying USD 337 million MIGA cover, increasingly insist on modular site accommodation to de-risk timelines. Defense-base modernization and NATO infrastructure refreshes add steady demand for volumetric barracks, yet tight security clearances restrict entry to incumbents like Dorce and Tepe. The “Others” application segment, growing at 5.49%, underlines a secular shift toward swift, reversible structures that minimize disruption and capital lock-in.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility & high inflation | -0.5% | Nationwide, acute for non-indexed local contracts | Short term (≤ 2 years) |

| Preference for masonry & fragmented permitting | -0.3% | More pronounced in secondary cities and rural districts | Medium term (2-4 years) |

| Uneven quality standards & limited scale players | -0.2% | Segments needing large, repeatable volumes (mass housing, industrial) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility & High Inflation

Producer-price inflation hit 57.68% year-on-year in May 2024, while the construction-cost index quintupled since 2021, eroding fixed-price prefab margins[2]Turkish Statistical Institute, “Producer Price Index,” tuik.gov.tr. Imported CNC lines, insulation cores, and adhesives are invoiced in euros, so every Lira slide pushes break-even higher. Policy rates at 50% raise working-capital costs, delaying progress-payment cycles for SMEs. Export-oriented firms such as Dorce hedge naturally with hard-currency contracts, but purely domestic shops either walk away from TOKİ bids or swallow razor-thin spreads. The squeeze explains why consolidation talks among mid-tier steel-frame makers accelerated in 2025.

Uneven Quality Standards & Limited Scale Players

Apart from a few giants, most Turkish prefab shops run sub-10,000 m² sheds with manual welding and ISO 9001-only certification. Absence of a national quality mark deters foreign developers who require traceable audits. Tepe and ENKA employ robotic lines and BIM-integrated QA, capturing mega-hospital and petrochemical jobs. Smaller firms compete on price, sometimes slipping on tolerances that lead to costly field rework, reinforcing buyer skepticism. Government-supported test labs announced for 2026 may close the gap, yet until scale catches up, reliability concerns will cap market share gains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Concrete Retains Lead While Timber Accelerates

Concrete accounted for 60.78% of the 2025 Turkey prefabricated construction market share, anchored by TOKİ’s reliance on tunnel formwork and precast hollow-core floors. Yapı Merkezi’s Panelton® system spans 2.8 million m² of delivered slabs, illustrating deep public-sector ties. Developers choose concrete for perceived fire resistance and acoustic mass, and domestic rebar supply shields costs from forex swings. However, TS 825’s insulation rules force thicker exterior cladding, slightly elongating concrete cycles versus insulated steel panels.

Timber’s regulatory breakthrough via TABY positions it as the fastest-growing material at 5.02% CAGR to 2031. Cross-laminated timber using local black pine and cedar now passes seismic and fire tests, and UNDP pilots totaling 51,800 m² will validate cost models. TeknoWood already presses 22 m long CLT panels in Antalya for export, and domestic orders are emerging for low-rise schools in Çanakkale. While insurance premiums for wood structures remain 10-15 basis points above concrete, carbon-credit monetization under Turkey’s impending ETS could narrow the gap further.

By Application: Residential Dominates, “Others” Gains Pace

Residential kept 44.35% of 2025 revenue as Istanbul’s EUR 65,000 (USD 71,500) per-flat incentive underpinned urban-renewal condos. Light-steel village houses and tunnel-form mid-rises fill the 417,000-unit quake backlog, sustaining panel fabrication lines at near capacity. Yet 41-43% mortgage rates delay first-time buyer decisions, nudging developers to pre-sell smaller units with repeatable layouts that suit the Turkey prefabricated construction market.

The “Others” segment—military, disaster relief, and site infrastructure—will rise fastest at 5.37% CAGR. AFAD’s 10,000 post-quake containers proved that volumetric units can mobilize within three weeks. Ministries now embed similar specs in barracks and rural clinic tenders, guaranteeing baseline throughput for modular yards even when housing cycles cool. Suppliers able to offer integrated water-treatment and PV kits within container footprints are differentiating on lifecycle value.

By Product Type: Panelized Holds Majority, Modular Surges

Panelized systems delivered 50.74% of the 2025 Turkey prefabricated construction market size, thanks to sandwich-panel walls and prestressed slabs tuned to TOKİ’s standardized block designs. Factories in Ankara and Sakarya push out 160,000 m² of panels monthly, shipping flat-packed to nine provinces nightly. Their dominance rests on truck-optimized logistics and local assembly skills that need only light cranes.

Modular buildings, however, are on track for a 5.74% CAGR to 2031 as healthcare PPPs and free-zone factories prize time-to-revenue. Karmod’s Hatay camp, erected in 39 days, cut civil works by 30% and reduced weather downtime to zero. Investors now factor earlier rent commencement into IRRs, offsetting 10-15% higher upfront module costs. Fire-protection rules published in December 2024 clarify insulation and sprinkler spacing, smoothing municipal approvals for taller modular stacks.

Geography Analysis

Istanbul generated 36.28% of 2025 demand, buoyed by the 14 million ft² Istanbul Financial Center and a steady pipeline of seismic-retrofit condos. The metropolis funnels three-quarters of Turkey’s office absorption, enabling large-lot fabrication yards in Gebze to run continuous shifts. While high land prices curb low-rise timber trials, volumetric bathroom pods and MEP risers shave weeks off super-tall schedules, reinforcing prefab’s urban value proposition.

Izmir posts the fastest 5.86% CAGR outlook as 5,061 TOKİ units replace Seferihisar quake losses and the port city pivots to logistics. Light-steel frames cut Bayraklı’s seven-phase rebuild from 24 to 12 months, a timeline local contractors now benchmark. Izmir’s 48,000 m² CLT and steel facility seeks Eurocode accreditation to funnel supplies to Italy and Greece, but until CE labels scale, domestic housing will anchor output.

Beyond the big three, Ankara and the 11-province “Rest of Turkey” block ride USD 44 billion earmarked for quake rebuilds through 2027. Tax holidays and fast-track permits compress bidding cycles, letting SME panel shops in Gaziantep win public dormitory work without big-city competition. Once incentives lapse, demand may normalize, yet a culture of off-site assembly is likely to persist, underpinning steady regional volumes.

Competitive Landscape

Turkey’s prefabricated construction arena remains fragmented; even Dorce’s 100,000 m² Ankara complex holds under 10% domestic revenue. Competitive dynamics pivot on export hedges, with Vefa shipping to 120 countries and Tepe leveraging Bilkent Holding’s procurement muscle. Firms adopting CNC plate lines, robot welders, and BIM-fed QA position themselves for repeat EU work where traceability and CE marks are mandatory.

Strategic moves in 2024-2025 highlight vertical integration and green credentials. Master Builders Solutions bought a 51% stake in MBT Tech, locking in local adhesives supply for panel plants. İzocam’s purchase of Terrawool expands insulation menus just as TS 825 tightens U-values. Dörce’s ISO 14064 pathway and GlobalABC ties help secure carbon-conscious tenders in Germany and the Gulf, while ENKA’s Çimtaş churns 105,000 tons of export steel modules using robotic weld cells.

Quality gaps, however, create a two-tier field. Only a handful of plants boast third-party weld and fire certificates beyond ISO 9001, steering mega projects toward the top five suppliers. Mid-tier workshops survive on price-sensitive village houses and export container offices, risking capacity loss if financing costs stay at 50%. Consolidation chatter suggests the market could tilt toward a more concentrated structure once interest rates ease.

Turkey Prefabricated Construction Industry Leaders

Prefabrik Yapı A.Ş

Karmod Prefabricated Technologies

Module-T

Tepe Prefabrik

Dorce Prefabrik

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Turkey’s Timber Building Regulation (TABY) entered force, formally approving CLT and light-frame systems and supplying a 290-page technical guide.

- December 2024: Master Builders Solutions acquired 51% of MBT Tech, adding local sealants and waterproofing to its prefab portfolio.

- October 2024: İzocam bought stone-wool producer His Yalıtım to meet TS 825-driven insulation demand.

- October 2024: TOKİ delivered 5,061 quake-replacement homes in Izmir within 12 months using light-steel frames.

Turkey Prefabricated Construction Market Report Scope

Prefabricated construction, also called "prefabs," are structures that are built off-site and then brought to the building site to be put together.It is made up of parts or units that are made in a factory and then shipped to the building site to be put together.

A complete background analysis of the Turkey prefabricated buildings market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends is covered in the report.

Turkey's prefabricated construction industry is segmented by material type (concrete, glass, metal, timber, and other material types) and application (residential, commercial, and other industrial, institutional, and infrastructure applications). The report offers market size in value terms in USD for all the above mentioned segments.

By Material

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By City

| Istanbul |

| Ankara |

| Izmir |

| Rest of Turkey |

| By Material | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By City | Istanbul |

| Ankara | |

| Izmir | |

| Rest of Turkey |

Key Questions Answered in the Report

Which material leads in Turkish prefab construction?

Concrete retains leadership with 60.78% share in 2025, mainly through precast hollow-core and tunnel-form systems.

Which application segment is expanding fastest?

The “Others” category—covering military, disaster, and site facilities—is growing at 5.37% CAGR due to emergency housing and modular clinics.

Why is Izmir expected to outpace other cities?

Post-Seferihisar quake reconstruction and port-centric logistics projects give Izmir a 5.86% CAGR outlook to 2031.

How will TS 825 influence prefab adoption?

Stricter insulation rules effective April 2025 raise traditional build costs 15–25%, steering developers toward factory-insulated panels and modules.

Which companies are dominating exports?

Dorce, Vefa/Vekon, and Tepe Prefabrik lead exports, leveraging ISO-certified plants and CE-ready modules to serve EU and MENA clients.

Page last updated on: