Tungsten Carbide Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

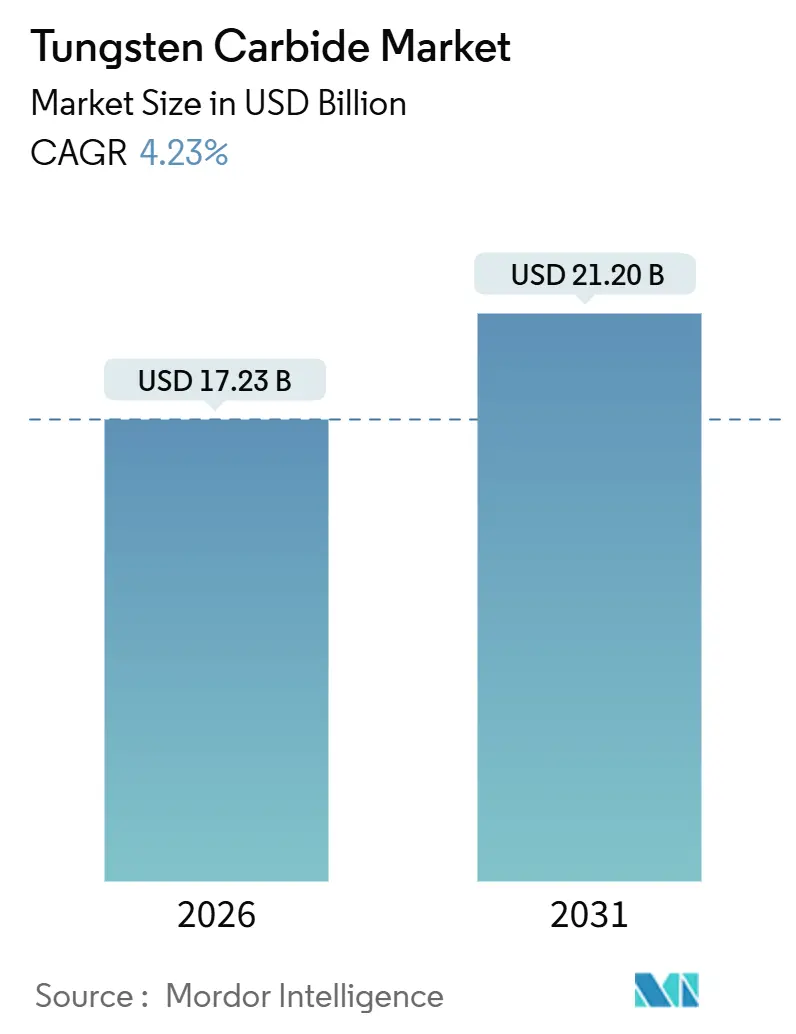

| Market Size (2026) | USD 17.23 Billion |

| Market Size (2031) | USD 21.20 Billion |

| Growth Rate (2026 - 2031) | 4.23% CAGR |

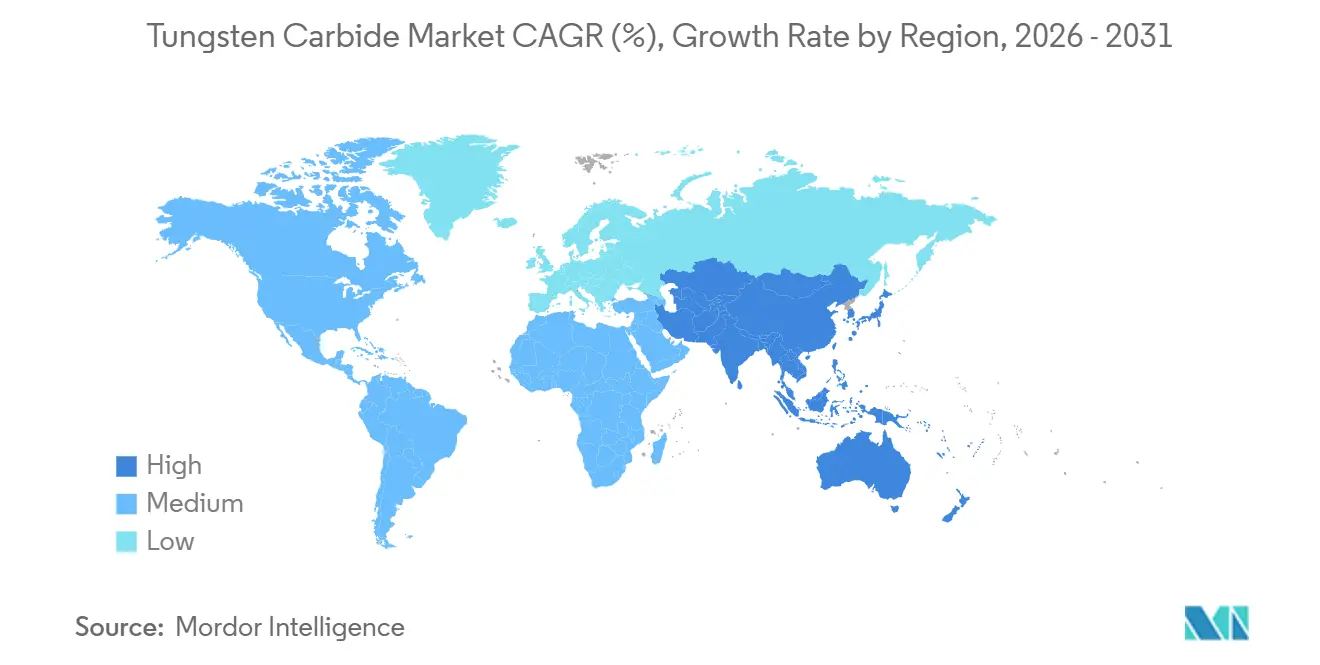

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tungsten Carbide Market Analysis by Mordor Intelligence

The Tungsten Carbide Market size is estimated at USD 17.23 billion in 2026, and is expected to reach USD 21.20 billion by 2031, at a CAGR of 4.23% during the forecast period (2026-2031). Diversification away from Chinese concentrate is prompting Western buyers to accept higher costs in exchange for assured access. Parallel ecosystems are forming: one continues to favor price-first Chinese powder metallurgy, while the other prioritizes regulated, tariff-insulated routes anchored in South Korea, the United States, and the European Union. Cemented carbide remains indispensable in mining, automotive, and general machining, yet the fastest growth is shifting toward coatings as multilayer PVD and CVD stacks double or even triple insert life. Mining and construction capex, defense rearmament, and aggressive recycling targets further support tool turnover, keeping the market in steady, mid-single-digit expansion.

Key Report Takeaways

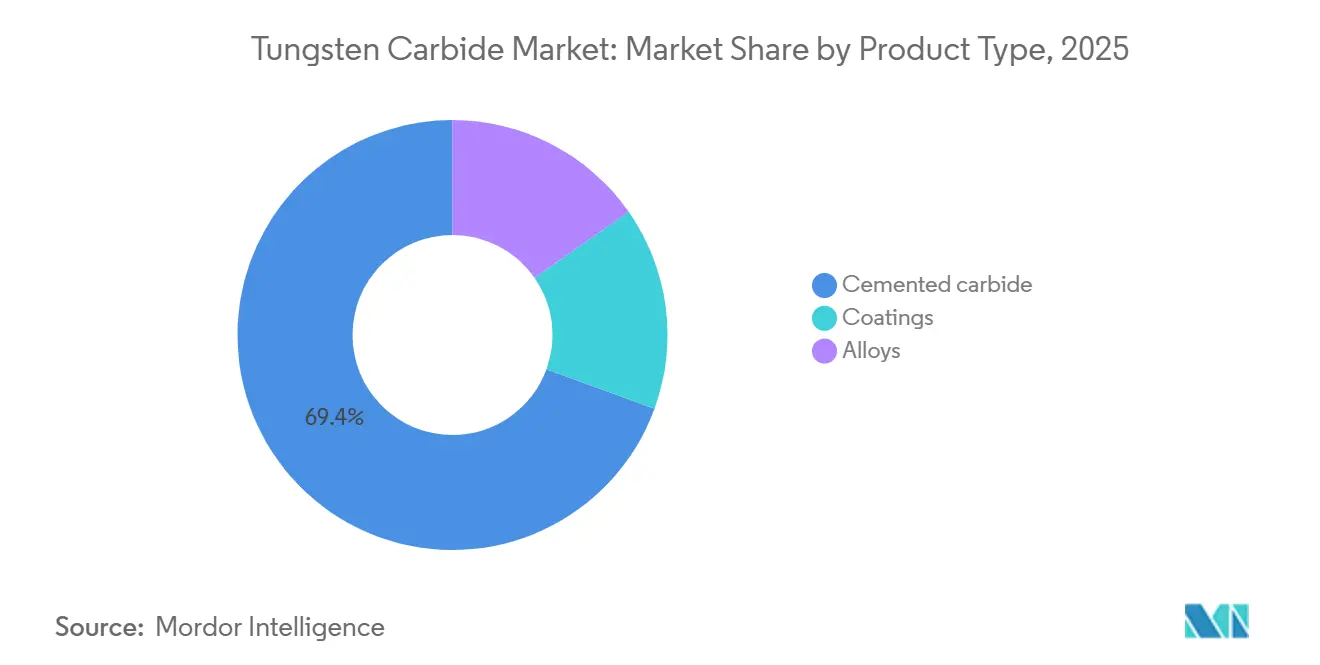

- By product type, cemented carbide held 69.42% of the tungsten carbide market share in 2025, while coatings are forecast to post the fastest 5.28% CAGR through 2031.

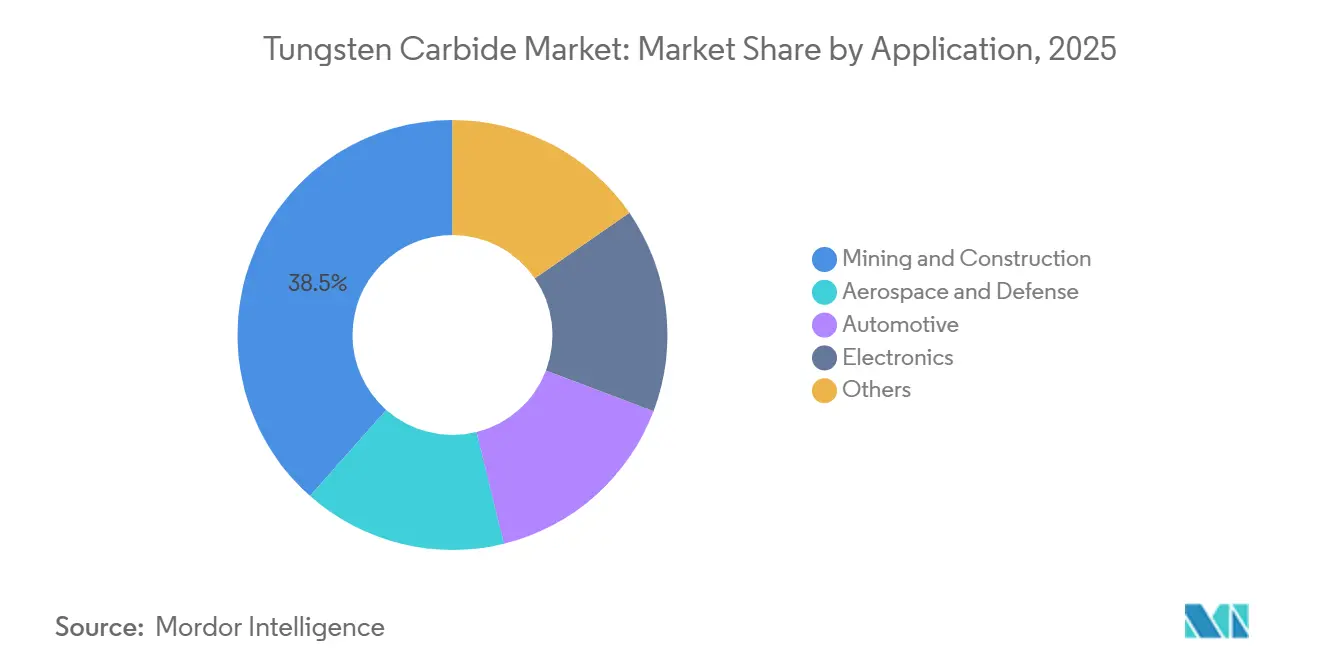

- By application, mining and construction led with 38.47% of the tungsten carbide market size in 2025; aerospace and defense are advancing at a 5.14% CAGR to 2031.

- By geography, Asia-Pacific commanded 51.36% of the market in 2025 and is projected to expand at a 4.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Tungsten Carbide Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for wear-resistant cutting tools in automotive and mining | +1.2% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| Rapid industrialization across APAC manufacturing hubs | +1.0% | APAC core (China, India, Vietnam, Indonesia) | Long term (≥ 4 years) |

| Accelerating infrastructure and construction investments worldwide | +0.9% | Global, with emphasis on India, Middle East, Southeast Asia | Medium term (2-4 years) |

| Recycling programmes recovering tungsten from spent inserts | +0.6% | Europe, North America, Japan | Long term (≥ 4 years) |

| Adoption of 3-D-printed cemented-carbide components | +0.4% | North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Wear-Resistant Cutting Tools in Automotive and Mining

In 2024, automotive output hit significant levels, with a growing shift towards electric vehicles leading to increased wear on tools, as manufacturers now machine harder aluminum alloys at elevated speeds. Mining operators, facing dwindling ore grades, are rapidly transitioning from steel bits to carbide-tipped tools. This trend is echoed in the mining equipment sector, which is expanding steadily. Caterpillar and Komatsu's budget hikes for carbide purchases in 2025 and 2026 underscore OEMs' belief in the correlation between tool longevity and total cost-of-ownership management[1]Caterpillar Inc., “Annual Report 2024,” caterpillar.com. As a result, demand from both the automotive and mining sectors remains counter-cyclical, ensuring consistent growth even during economic slumps. The combined forces of electrification and the pursuit of deeper ore deposits bolster the tungsten carbide market's resilience.

Rapid Industrialization Across APAC Manufacturing Hubs

India’s Production-Linked Incentives have accelerated capital flows into electronics, automotive, and machinery plants, each new CNC cell raising annual carbide insert demand. Vietnam and Indonesia are on similar trajectories as multinational firms move capacity out of China, strengthening the regional tungsten carbide market. In 2024, China alone accounted for a consumption of tungsten carbide, surpassing the combined total of the entire Asia-Pacific region. Any disruption in Chinese power, environmental enforcement, or export policy ripples through global carbide availability within weeks. Over the long term, however, the upward climb in precision manufacturing across APAC underpins continuous latent demand for higher-grade tooling.

Accelerating Infrastructure and Construction Investments Worldwide

Multi-year public-works budgets in the Middle East, India, and Southeast Asia reach into the hundreds of billions, driving orders for carbide-tipped road-milling cutters, tunnel-boring discs, and demolition tool inserts, thereby supporting growth in the tungsten carbide market. India's National Infrastructure Pipeline pledges a hefty investment through 2025, signaling a consistent demand for cutting tool replacements in concrete and asphalt[2]Government of India, “Production-Linked Incentive Schemes,” india.gov.in. With the construction equipment market projected to grow steadily, the demand for wear parts remains robust. Heat and abrasive sand in the Middle East build elevate performance thresholds, so contractors willingly pay premiums for high-cobalt or fine-grain carbides. Continuous mega-project rollouts therefore prolong a robust order book for insert producers.

Recycling Programs Recovering Tungsten from Spent Inserts

CERATIZIT’s zinc-process recovers more than 99% of tungsten from end-of-life inserts, enabling near-zero virgin content grades now gaining traction among automotive OEMs pursuing Scope 3 targets. Sandvik’s Bergla powder, made entirely from recycled metal, emits 90% less CO₂ than virgin powder routes. Epiroc’s take-back scheme for worn drill bits launched in 2024, offering mine operators credit toward new tools. Mitsubishi Materials aims to reach 80% recycled content by FY 2031, a hedge against concentrate price swings. As carbon border adjustments advance in Europe and North America, low-emission recycled powder will carry tangible cost advantages, accelerating sustainability-driven innovation across the tungsten carbide market and speeding adoption beyond early movers.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility due to Chinese supply dominance | -0.8% | Global, with acute exposure in spot-market buyers | Short term (≤ 2 years) |

| Toxicity and occupational-health regulations on WC-Co dust | -0.5% | North America, Europe, Japan | Medium term (2-4 years) |

| High sintering energy intensity and looming carbon pricing | -0.4% | Europe, with spillover to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility Due to Chinese Supply Dominance

In 2025, APT spot prices surged significantly within just six months, following the announcement of export controls. This move highlighted Beijing's significant influence on pricing. In response, Western producers swiftly secured multi-quarter contracts to shield themselves from potential losses. In contrast, smaller fabricators, lacking hedges, grappled with margin compression. While the restart of the Sangdong Mine provides some respite, its ramp-up hasn't kept pace with demand. As the market awaits alternative concentrates to scale, sudden policy changes threaten to negate an entire year's growth in the tungsten carbide market. Suppliers who are vertically integrated, boasting their own mines or strong recycling capabilities, are better equipped to handle price surges than those reliant on the spot market.

Toxicity and Occupational-Health Regulations on WC-Co Dust

OSHA sets the cobalt dust limit, while NIOSH advocates for a stricter threshold. In Europe, discussions are underway for a tighter REACH classification, especially after the National Toxicology Program flagged cobalt-tungsten carbide as "reasonably anticipated to cause cancer." Upgrading dust-collection systems increases grinding and finishing costs, with small shops feeling the pinch the most. While cobalt-free binders offer a safer alternative, they remain a niche choice, lacking the toughness essential for high-impact drilling. With stricter limits on the horizon, regulatory compliance costs could weigh on profitability across the tungsten carbide market unless safer binder chemistries can be commercialized swiftly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cemented Carbide Anchors the Market, Coatings Drive Innovation

Cemented carbide claimed a dominant 69.42% tungsten carbide market share in 2025, attributed to its hardness and unmatched fracture toughness compared to ceramics. While the mature segment tracks an overall demand growth, it consistently provides stable cash flow for vertically integrated producers. Coatings, however, deliver the fastest 5.28% CAGR as multilayer AlCrN or TiAlN films extend insert life two to five times, cutting tool inventories for users, and raising value capture for coaters. As cutting speeds rise and dry machining becomes more prevalent in the automotive and aerospace sectors, the market share for coatings in the tungsten carbide arena is set to expand. Meanwhile, alloyed carbides, infused with titanium or tantalum, are carving out niche roles in drilling and energy sectors, albeit at a premium of price surcharges and limited volume.

Additive manufacturing is redefining product boundaries by integrating substrate and architecture. Sandvik’s coolant-channel mills have successfully reduced titanium cycle times, underscoring a shift in future value creation towards hybrid designs. CERATIZIT’s CT-GS20Y grade, crafted from recycled tungsten, bridges the gap between circularity and high performance, making it particularly appealing to OEMs mindful of Scope 3 emissions. ISO 4499-2 guarantees grain-size uniformity across suppliers, a crucial assurance given the complexities of coatings that can obscure substrate microstructures. Looking ahead, while coatings and hybrid AM parts are poised to capture a larger share, cemented carbide is set to continue leading in volume demand.

By Application: Mining and Construction Lead, Aerospace Accelerates

Mining and construction accounted for 38.47% of the tungsten carbide market size in 2025, anchored by abrasive rock drilling, road milling, and wear-plate replacement. The mining equipment sector is a significant driver for insert reloads. As deeper deposits are tapped, there's a shift towards tougher, cobalt-rich grades, enhancing bit life. However, adhering to dust-toxicity regulations has led to increased processing costs.

Aerospace and defense posts the quickest 5.14% CAGR. The industry's pivot towards next-generation turbine blades, made from titanium aluminides and ceramic-matrix composites, demands ultra-fine grain tools with grain sizes under 0.8 µm, complemented by heat-stable coatings. Meanwhile, the automotive sector's transition to aluminum battery enclosures lightens vehicle mass but heightens precision demands. This shift has resulted in increased tool expenditure per part, even as the number of units remains stable. In the electronics realm, PCB micro-drilling requires carbide diameters below 0.1 mm, with Taiwan and South Korea leading as primary end-users. Kennametal's revenue distribution underscores how diversified suppliers can mitigate mining's cyclical nature, capitalizing on the steady growth in aerospace within the tungsten carbide market.

Geography Analysis

Asia-Pacific controlled 51.36% of the tungsten carbide market share in 2025 and is forecast to grow at a 4.92% pace through 2031, reflecting robust machine-tool installations in China, India, and Southeast Asian electronics corridors. In 2024, China consumed significant volumes, but 2025's export quotas prompted a swift pivot towards Western sourcing. Meanwhile, India, harnessing Production-Linked Incentives, is witnessing a surge in domestic precision machining, boasting double-digit growth from its nascent base.

North America accounted for a notable share of the global market in 2025. Starting January 2025, the US Tungsten Carbide Market was influenced by the United States tariff on tungsten-related imports from China, spurring reshoring and alternative sourcing. Both Canada and Mexico act as manufacturing hubs for the aerospace and automotive industries, linking their tool demand closely to the United States' industrial activities. The Sangdong Mine's revival in South Korea presents a strategic feedstock option, though its gradual ramp-up tempers immediate repercussions.

Europe, with a significant market share in 2025, reintroduced anti-dumping duties on Chinese tungsten carbide in 2023 to bolster supply security. Additionally, the bloc greenlit two extraction initiatives under Decision 2025/840 to bolster local feedstock. Germany, with its dense clusters in machine-tool and automotive industries, leads the region in consumption, valuing proximity in supply. Both South America and the Middle East-Africa regions collectively account for a smaller portion of the market, with demand fluctuating based on infrastructure projects and mining expansions. Brazil's automotive and oil-and-gas sectors drive sporadic surges, while Saudi Arabia's NEOM project boosts demand for cutters resilient to high sand abrasion. South Africa's mining industry, albeit facing power constraints, remains a consistent consumer.

Competitive Landscape

The global tungsten carbide market is moderately fragmented. The primary competitive advantage lies in vertical integration, spanning from mining or scrap intake to powder production, pressing, sintering, grinding, and coating. Governments are backing strategic projects like Sangdong and Spain’s El Moto, highlighting white-space opportunities in non-Chinese concentrate lines. Specialty suppliers are carving niches in medical and defense tooling by experimenting with cobalt-free variants and ultra-fine grain grades (<0.5 µm). Quality assertions across this varied supplier landscape are anchored by ISO 6508-2’s Rockwell calibration standard.

Tungsten Carbide Industry Leaders

Sandvik AB

Kennametal Inc.

CERATIZIT S.A.

Xiamen Tungsten Co., Ltd.

Guangdong Xianglu Tungsten Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Ceratizit USA agreed to pay USD 54.4 million to settle allegations of evading customs duties by misclassifying Chinese tungsten carbide as Taiwanese origin, resolving a False Claims Act probe by the U.S. Department of Justice.

- January 2024: Sandvik expanded North American tungsten powder capacity by tapping hydropower-based production at Buffalo Tungsten’s New York facility to serve regional customers with lower-emission material.

- February 2022: CERATIZIT S.A. announced the takeover of the remaining 50% of the shares of Stadler Mettale and thus became the sole owner of the company. The company is one of the most important sources of secondary raw materials for making tungsten and tungsten carbide powders. Because of this, CERATIZIT S.A. depends on the company a lot.

Global Tungsten Carbide Market Report Scope

Tungsten carbide is a chemical compound containing almost equal proportions of tungsten and carbon. In its most basic form, it is a fine gray powder, but smelting can shape it into a variety of shapes for use in various industries.

The tungsten carbide market is segmented by product type, application, and geography. By product type, the market is segmented into cemented carbide, coatings, and alloys. By application, the market is segmented into aerospace and defense, automotive, mining and construction, electronics, and others. The report also covers the market size and forecasts for the tungsten carbide market in 17 countries across major regions. For each segment, market sizing and forecasts have been done based on revenue (USD).

| Cemented carbide |

| Coatings |

| Alloys |

| Aerospace and Defense |

| Automotive |

| Mining and Construction |

| Electronics |

| Others (Medical, Sports, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Cemented carbide | |

| Coatings | ||

| Alloys | ||

| By Application | Aerospace and Defense | |

| Automotive | ||

| Mining and Construction | ||

| Electronics | ||

| Others (Medical, Sports, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the tungsten carbide market in 2026?

The tungsten carbide market size is USD 17.23 billion in 2026 and is expected to reach USD 21.20 billion by 2031.

What is the expected CAGR for tungsten carbide to 2031?

The market is forecast to grow at a 4.23% CAGR through 2031.

Which product type leads demand?

Cemented carbide holds 69.42% market share and remains the largest volume segment.

Which application is growing fastest?

Aerospace and defense tooling posts the highest 5.14% CAGR to 2031 due to advanced-material machining needs.

Which region dominates consumption?

Asia-Pacific commands 51.36% of global demand and is expanding at a 4.92% CAGR.

How are suppliers mitigating raw-material risk?

Leaders invest in recycling loops and new non-Chinese concentrate projects to shield against price and export volatility.

Page last updated on: