Multi-Parameter Patient Monitoring Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

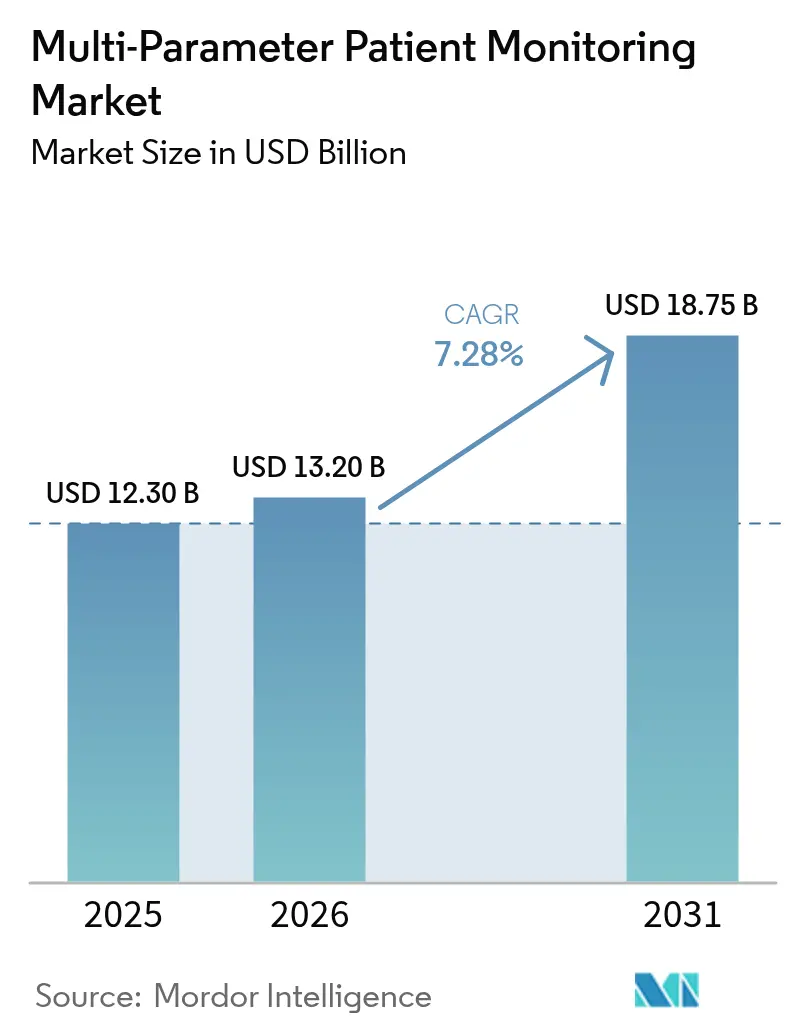

| Market Size (2026) | USD 13.2 Billion |

| Market Size (2031) | USD 18.75 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

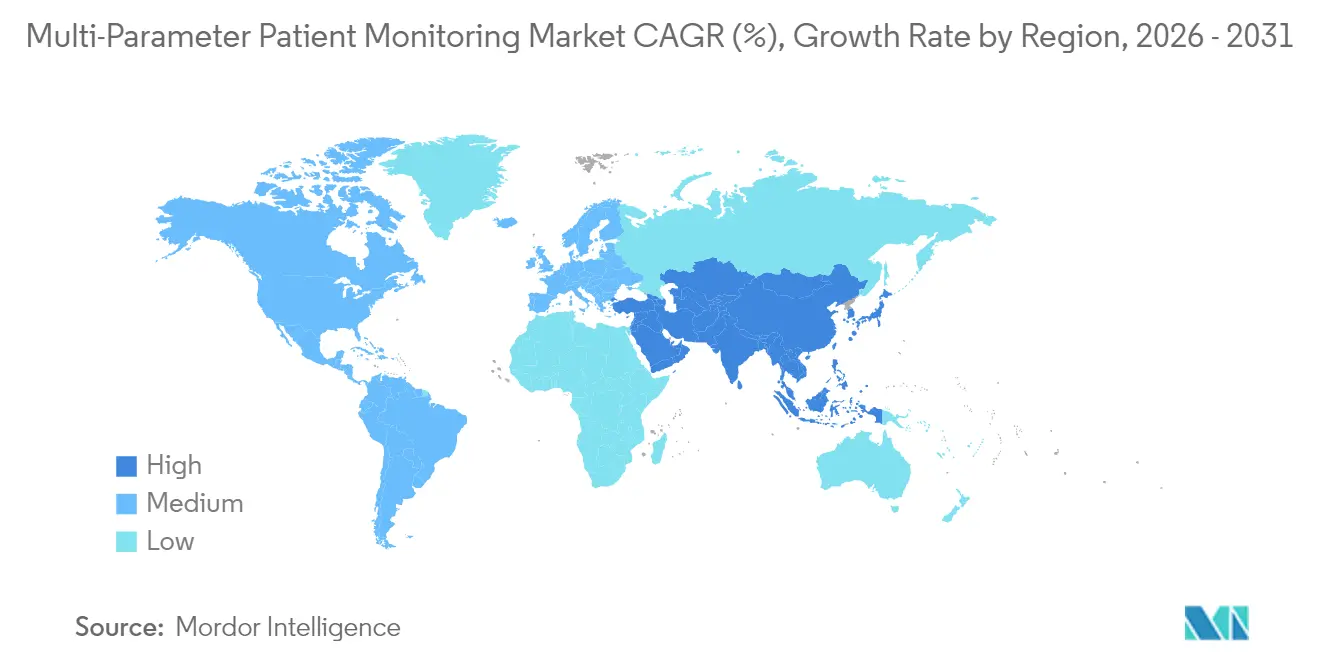

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi-Parameter Patient Monitoring Market Analysis by Mordor Intelligence

The multi-parameter patient monitoring market size is expected to grow from USD 12.30 billion in 2025 to USD 13.2 billion in 2026 and is forecast to reach USD 18.75 billion by 2031 at 7.28% CAGR over 2026-2031. Within this growth arc, clinical priorities have shifted toward mobility, interoperability and data-driven decision support, accelerating the transition from fixed bedside units to portable, wearable and AI-enabled platforms. Hospital staffing shortages, higher patient acuity and chronic-disease prevalence continue to elevate demand for continuous surveillance, while reimbursement expansion in the United States and Europe sustains investment in remote care. Semiconductor supply tightness has pushed manufacturers to redesign hardware around power-efficient architectures, and energy-harvesting wearables are beginning to remove battery-related limitations. Strategic alliances—such as GE HealthCare’s multi-year imaging and monitoring partnership with Sutter Health—illustrate how large providers are standardizing on platform ecosystems that embed predictive analytics into routine workflows.

Key Report Takeaways

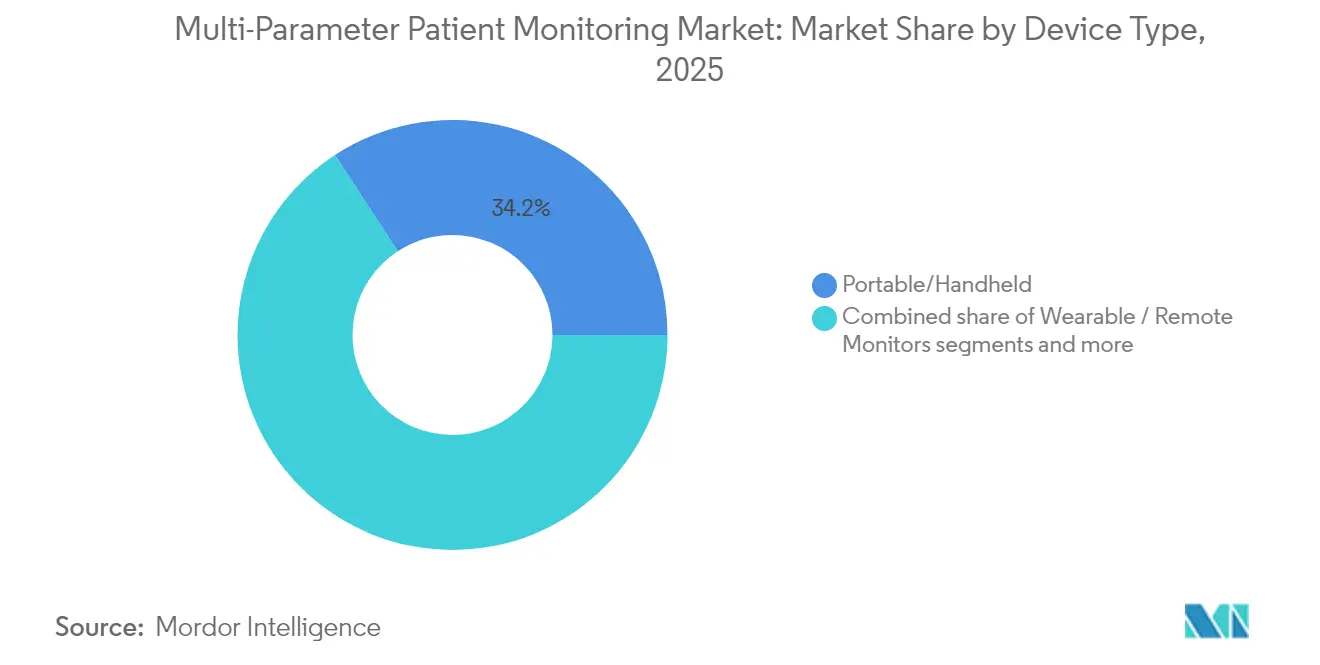

- By device type, portable/handheld monitors led with 34.21% of the multi-parameter patient monitoring market share in 2025. Wearable/remote monitors are projected to expand at an 8.23% CAGR through 2031.

- By patient age group, adults accounted for 52.78% share of the multi-parameter patient monitoring market size in 2025, while the geriatric cohort is forecast to grow at 9.29% CAGR to 2031.

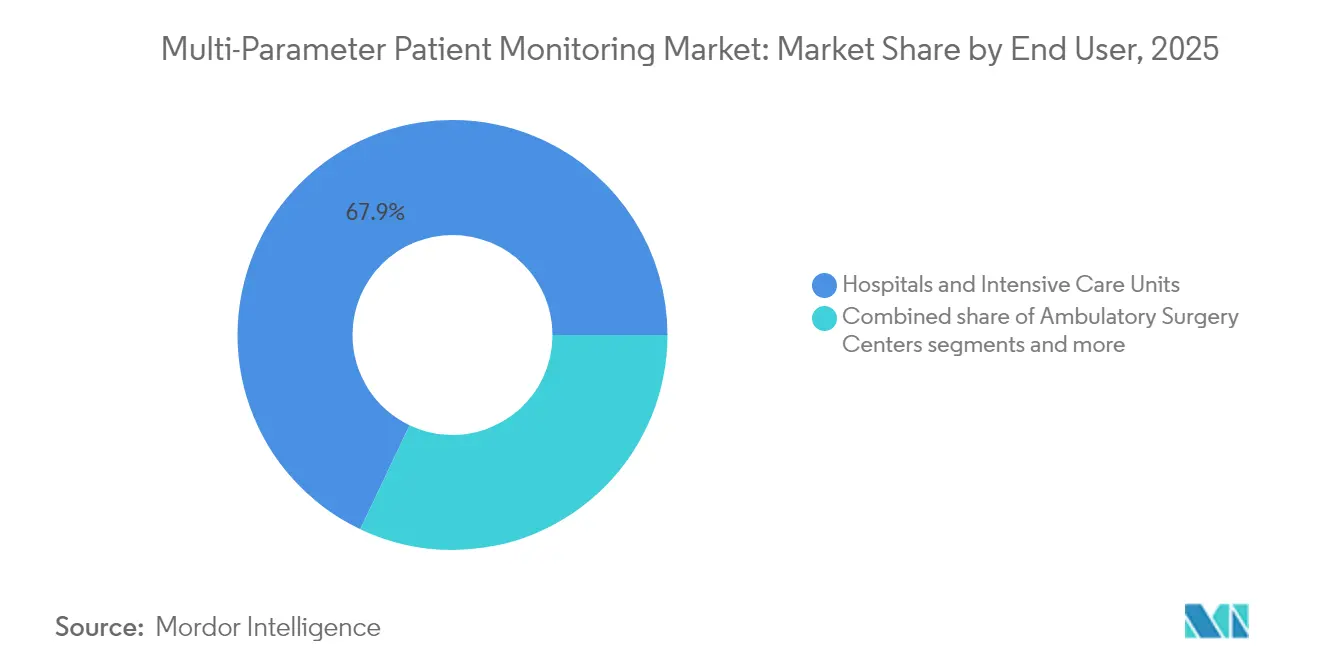

- By end user, hospitals and intensive care units held 67.94% share of the multi-parameter patient monitoring market size in 2025; homecare settings record the fastest growth at 9.85% CAGR through 2031.

- By application, cardiology captured 37.22% of the multi-parameter patient monitoring market share in 2025, and respiratory monitoring is advancing at a 8.72% CAGR to 2031.

- By geography, North America commanded 41.85% share of the multi-parameter patient monitoring market size in 2025, whereas Asia-Pacific is expanding at 10.44% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Multi-Parameter Patient Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic diseases requiring continuous vital-sign surveillance | +2.1% | Global, with highest impact in North America & EU | Long term (≥ 4 years) |

| Accelerated adoption of remote patient monitoring post-COVID-19 | +1.8% | Global, spill-over from developed to emerging markets | Medium term (2-4 years) |

| Hospital capacity constraints driving demand for portable multi-parameter monitors | +1.5% | North America & EU core, expanding to APAC | Short term (≤ 2 years) |

| Reimbursement expansion for home telemetry in the U.S. & EU | +1.2% | North America & EU, early adoption in select APAC markets | Medium term (2-4 years) |

| AI-enabled predictive analytics embedded in next-gen monitors | +0.9% | Global, with early gains in US, Germany, Japan | Long term (≥ 4 years) |

| Battery-less energy-harvesting wearables lowering TCO | +0.4% | Global, initial deployment in premium markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic Diseases Requiring Continuous Vital-Sign Surveillance

More than 537 million adults live with diabetes and cardiovascular diseases remain the leading global cause of death. Continuous glucose monitors, such as Dexcom G7 cleared by FDA in 2024, deliver 8% mean absolute relative difference accuracy over an extended 15-day sensor life. Integrated solutions linking Abbott glucose sensors with Medtronic insulin pumps are lowering hypoglycemic events by 40%. Multimorbidity among older adults intensifies demand for multi-parameter platforms capable of flagging subtle deterioration far earlier than spot-check routines.

Accelerated Adoption of Remote Patient Monitoring Post-COVID-19

Clinician uptake of remote patient monitoring climbed above 80% in 2024 as telehealth reimbursement parity removed geographic barriers in the United States. India’s eSanjeevani network has delivered more than 340 million consultations since launch, confirming scalability in resource-constrained settings. RPM programs have reduced readmissions for chronic conditions and supported home-based transition pathways such as Masimo’s donation of Stork Smart Home Baby Monitors to 50,000 families.

Hospital Capacity Constraints Driving Demand for Portable Multi-Parameter Monitors

A 10% rise in patient acuity has collided with nurse shortages, forcing providers to decentralize surveillance. GE HealthCare’s FDA-cleared Portrait VSM brings ICU-grade accuracy into a handheld form factor, cutting manual vitals collection time by 30%. In the surgical theater, Terumo’s CDI OneView displays 22 vital parameters on a single compact unit, minimizing equipment footprint without sacrificing fidelity.

Reimbursement Expansion for Home Telemetry in the U.S. & EU

The 2025 Medicare Physician Fee Schedule maintains CPT 99453-99458, paying up to USD 47.87 per 20-minute interactive RPM session when FDA-cleared devices transmit at least 16 readings every 30 days. Germany’s Digital Healthcare Act similarly supports digital therapeutics, accelerating commercial adoption of connected monitors. Private payers such as Cigna now deem RPM medically necessary for COPD, diabetes and heart-failure management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost for high-acuity bedside systems | -1.3% | Global, particularly acute in LMIC regions | Medium term (2-4 years) |

| Cyber-security & interoperability concerns in networked monitors | -0.8% | Global, heightened in regulated markets (US, EU) | Short term (≤ 2 years) |

| Shortage of trained biomedical engineers in LMIC hospitals | -0.6% | LMIC regions, particularly Sub-Saharan Africa, Southeast Asia | Long term (≥ 4 years) |

| Supply-chain fragility for critical semiconductors | -0.5% | Global, with acute impact on high-tech monitoring systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost for High-Acuity Bedside Systems

Fully featured ICU monitors can cost USD 15,000–50,000 per bed and lifetime ownership expenses often double that figure. Nihon Kohden addressed affordability by introducing subscription plans that bundle training and maintenance, lowering upfront hurdles for resource-constrained providers. Infrastructure gaps—such as unreliable power and limited clinical engineering capacity—continue to hamper installations in many low-income regions, extending payback periods and deterring capital projects.

Cyber-Security & Interoperability Concerns in Networked Monitors

Medical device vulnerabilities totaled 993 in 2024, prompting the FDA to require manufacturers to patch products throughout their lifecycle. Integrating multi-vendor fleets with electronic records raises compatibility issues that can expose protected health information, leading hospitals to demand encryption, device authentication and network segmentation—requirements that raise development cost and lengthen approval timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Wearables Drive Next-Generation Monitoring

Portable/handheld systems accounted for 34.21% of 2025 demand, favored for their compact footprint in emergency, perioperative and step-down settings where floor space is constrained. Wearable and remote devices, boosted by organic-photovoltaic harvesters that reach 16.18% energy-conversion efficiency, are projected to post the fastest 8.23% CAGR to 2031. Pandemic-era care models validated the clinical safety of untethered vitals capture, prompting providers to place portability ahead of feature depth when refreshing fleets. Hardware redesigns also mitigate semiconductor shortages by using lower-power chipsets, extending service life and easing maintenance schedules.

SurePulse Medical’s wireless newborn monitor demonstrates how NICU-grade accuracy is now delivered without traditional cables, reducing caregiver workload and improving skin integrity in fragile infants. Fixed bedside consoles still dominate intensive and perioperative care because they aggregate multi-parameter streams and integrate with hospital alarm middleware. Yet vendors are embedding Bluetooth Low Energy radios into those consoles so data can mirror to clinician tablets, smoothing migration toward fully wireless ecosystems. Hospitals that standardize on a single operating system for both portable and fixed units also gain cybersecurity uniformity, an increasingly important buying criterion. As a result, product roadmaps across leading brands show converging design languages that prioritize modular sensor ports, cloud compatibility and subscription-based analytics.

By Patient Age Group: Geriatric Surge Reshapes Care Models

Adults held 52.78% share in 2025, reflecting the broad need for routine vitals collection in medical, surgical and telemetry wards. The geriatric cohort is expanding at a 9.29% CAGR as populations age and multimorbidity heightens surveillance requirements across cardiac, metabolic and respiratory domains. Frailty scores used by hospitalists reinforce the business case for continuous monitors that detect subtle deterioration earlier than nurse rounding. Remote monitoring also allows long-term-care facilities to escalate patients before crises, reducing avoidable transfers to overcrowded emergency departments.

At the opposite end of the spectrum, neonatology has become a high-value niche where touchless optical systems monitor movement and heart rate without adhesives that can damage preterm skin. Pediatric centers deploy stretchable, skin-interfacing biosensors that flex with growth and activity to capture cardiac and respiratory data painlessly. Adolescents benefit from cloud-linked asthma and diabetes wearables that feed clinician dashboards as well as parental smartphone apps, fostering adherence. Together, these age-tailored innovations extend the multi-parameter patient monitoring market beyond traditional acute-care silos into schools, homes and rehabilitation venues.

By End User: Homecare Settings Accelerate Market Expansion

Hospitals and ICUs commanded 67.94% of the multi-parameter patient monitoring market size in 2025, underlining their role as anchor purchasers that demand interoperability with electronic medical records and clinical-decision platforms. Unit economics still favor bulk renewal contracts every five-to-seven years, with cross-department standardization lowering training load and spare-parts complexity. Homecare, however, is set to grow at a 9.85% CAGR through 2031 as CPT 99453-99458 reimbursement guarantees revenue for remote physiological monitoring, making hospital-at-home programs financially sustainable. Device vendors now package cellular hubs, pre-configured tablets and logistics services into starter kits that clinicians can mail directly to patients.

Ambulatory surgery centers require slim, rechargeable monitors that meet post-anesthesia care guidelines while enabling same-day discharge. Specialty clinics leverage disease-specific telemetry—for example, cardiology offices integrate arrhythmia patches that auto-populate structured data into electronic records. Emergency medical services have begun deploying ruggedized handheld units that stream vitals en route, allowing trauma teams to prepare resources before ambulance arrival. Long-term-care facilities adopt fall-detection wearables linked to nurse call systems, closing gaps during staffing shortages. Collectively, these diverse end-user needs encourage manufacturers to offer modular platforms that scale from single-patient kits to enterprise command centers.

By Application: Respiratory Monitoring Gains Clinical Priority

Cardiology dominated with 37.22% share in 2025, supported by AI hemodynamic engines such as BD’s HemoSphere Alta that predict hypotension minutes in advance and suggest fluid or vasopressor interventions. ECG patches capable of seven-lead output and cloud-based arrhythmia analytics now replace Holter recorders, shortening diagnosis cycles for atrial fibrillation. Post-PCI patients receive home telemetry kits that push ischemia alerts to cardiologists, reducing readmissions.

Respiratory monitoring will log the highest 8.72% CAGR after COVID-19 spotlighted silent hypoxia and non-invasive ventilation management. Continuous capnography and pulse-oximetry bundles help wards detect deterioration hours earlier than spot-checks, prompting earlier oxygen titration. Neurologic applications use computer-vision algorithms to flag seizure-like events in NICU babies from live video streams. Fetal and neonatal segments adopt heart-rate variability tools like the NIPE monitor that quantify pain and autonomic tone, informing anesthetic dosing. Temperature, metabolic and multi-parameter fitness tracking round out smaller but growing niches as consumer-grade sensors cross regulatory thresholds into clinical practice.

Geography Analysis

North America retained 41.85% share in 2025, underpinned by Medicare RPM coverage and enterprise-wide rollouts such as Sutter Health’s seven-year partnership with GE HealthCare across 300 facilities.

Asia-Pacific is forecast to register a 10.44% CAGR, buoyed by India’s Ayushman Bharat Digital Mission issuing 568 million health IDs and by China’s commitment to WHO-aligned digital-health standards. Regional suppliers are tailoring cost-efficient monitors for fast-growing mid-tier hospitals.

Europe continues steady adoption as the Medical Device Regulation enforces post-market surveillance, while Germany’s DiGA fast-track reimburses connected therapies. Southern and Eastern Europe leverage EU structural funds to modernize monitoring infrastructure.

South America shows potential with Brazilian firms such as BR HomMed expanding tele-ICU models that bridge rural access gaps. In the Middle East and Africa, Gulf states are investing aggressively in e-ICU hubs that centralize surveillance for satellite hospitals.

Regulatory Landscape

Multi-parameter patient monitors are regulated as medical devices across major markets, with the United States primarily using the FDA 510(k) pathway where manufacturers demonstrate substantial equivalence to a predicate (commonly mapped to 21 CFR device classifications used for patient monitoring functions). FDA-recognized consensus standards shape design and verification expectations for multifunction monitors, including IEC 80601-2-49:2018+AMD1:2024 for multifunction patient monitor safety and essential performance, alongside ECG monitoring standards such as IEC 60601-2-27 referenced across multiple national adoptions.

In Europe, devices marketed under the Medical Device Regulation (EU MDR 2017/745) face risk-based classification (commonly Class IIa or higher under Rule 10 for active diagnostic devices) and heightened post-market obligations compared with earlier regimes. The European Commission Medical Device Coordination Group (MDCG) issued guidance such as MDCG 2025-10 to reinforce structured Post-Market Surveillance (PMS) as a standing Quality Management System requirement, increasing the day-to-day workload for manufacturers that support networked monitor fleets across multiple sites and geographies.

Value Chain Analysis

The value chain starts with critical inputs (physiological sensors such as ECG, SpO2, and NIBP modules; compute; batteries and power-management; and connectivity components) provided by specialized electronics and semiconductor vendors. It then moves to device OEMs that integrate hardware, embedded software, cybersecurity controls, and user interfaces into bedside, portable, and wearable multi-parameter platforms. Given the market emphasis on interoperability and remote monitoring, the software layer (device operating systems, alarm management, and integration middleware) and connectivity layer (Wi-Fi/cellular gateways and enterprise integration) are increasingly central to differentiation, alongside compliance testing against recognized safety and performance standards for multifunction monitors.

Downstream, distribution and commercialization cover direct hospital tenders and group purchasing for ICU and ward fleets, channel partners for mid-tier and emerging-market hospitals, and kit-based logistics models supporting homecare deployment (shipping, onboarding, and returns). Providers and health systems influence specifications through enterprise standardization and integration requirements, while component availability and quality documentation can constrain supply. This, in turn, prompts OEM efforts to strengthen traceability and regulated documentation across manufacturing and logistics networks, and to design around power-efficient architectures when electronics tightness affects lead times.

Competitive Landscape

Market concentration is moderate: diversified leaders—GE HealthCare, Philips, Medtronic, Masimo, BD and Nihon Kohden—bundle hardware, cloud analytics and managed services. GE HealthCare partners with NVIDIA to embed autonomous imaging into monitoring ecosystems. Masimo extends beyond oximetry with W1 health watches and Sleep Halo, supported by a tele-monitoring alliance with UCHealth. Philips and Medtronic integrate Nellcor pulse oximetry and Microstream capnography to streamline alarm workflows. Start-ups focusing on non-contact vital signs and cuffless blood-pressure algorithms pressure incumbents to accelerate R&D.

Multi-Parameter Patient Monitoring Industry Leaders

Abbott Laboratories

Medtronic PLC

Koninklijke Philips NV

Becton, Dickinson and Company

General Electric Company (GE Healthcare)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Home-based and decentralized monitoring programs are opening white space for enterprise-grade offerings that combine multi-parameter capture with operational tooling (device logistics, onboarding, and workflow integration), rather than standalone hardware. One clear demand signal is the May 2026 Philips announcement of an eight-year hospital-at-home agreement with Region Stockholm (Sweden) supporting care for up to 15,000 patients annually, which reinforces purchasing pathways for connected monitors, services, and integration that can scale beyond single-hospital deployments.

Technology and regulatory progress are also expanding the set of clinically acceptable form factors and measurement modalities, especially for wearable and contactless monitoring that fits mobility and staffing constraints. In early 2026, FDA clearance activity in this area for Philips IntelliVue modules/monitors and software-based vital sign estimation (for example, PanopticAI Vital Signs cleared in May 2026) underscores an opportunity for vendors to pair validated measurement performance with interoperability and cybersecurity-by-design. That direction supports mixed fleets across bedside, wearable/remote, and command-center views without forcing fragmented clinical workflows.

Recent Industry Developments

- June 2026: Sibel Health received an EU MDR Class IIb CE Mark for its ANNE One wireless wearable patient monitoring platform. The milestone pushes wearable multi-parameter monitoring deeper into regulated acute and sub-acute settings, supporting procurement in Europe where MDR compliance and post-market expectations influence vendor selection.

- May 2026: Philips announced an eight-year agreement to deliver vital technology supporting a hospital-at-home program for Region Stockholm in Sweden, covering care for up to 15,000 patients annually. The deal formalizes scaled remote monitoring operations and indicates provider willingness to contract for long-duration, service-enabled monitoring ecosystems rather than one-off device purchases.

- September 2024: BD completed its acquisition of the Critical Care business from Edwards Lifesciences and rebranded it as BD Advanced Patient Monitoring. The transaction broadened BD's monitoring portfolio depth in hemodynamics and supports more integrated offerings across monitoring, consumables, and hospital workflows.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from multi-parameter patient monitors that measure and display more than one vital sign at the same time, used for continuous or spot monitoring across care settings such as hospitals, ambulatory sites, and homecare.

Scope exclusions: We do not count disposable consumables and hospital IT services that sit outside the sale of the monitoring device and its core accessories.

Segmentation Overview

- By Device Type (Value)

- Portable / Handheld Monitors

- Wearable / Remote Monitors

- Fixed

- Wireless Integrated Monitors

- By Patient Age Group (Value)

- Neonatal

- Pediatric

- Adult

- Geriatric

- By End User (Value)

- Hospitals & Intensive Care Units

- Ambulatory Surgery Centers

- Specialty Clinics

- Homecare Settings

- Emergency Medical Services

- By Application (Value)

- Cardiology

- Neurology

- Respiratory

- Fetal & Neonatal

- Temperature Monitoring

- Other Applications

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to set the basic structure of the market and to anchor assumptions that can be checked in public data. We rely on official healthcare statistics and regulatory information to understand care volumes, device adoption direction, and safety requirements that shape buying decisions.

Illustrative sources include government health and statistics agencies such as the US CDC and OECD health datasets, regulator databases such as the US FDA and the European Commission MDR resources, and international bodies such as the WHO. We also refer to clinical guidelines and peer reviewed journals to confirm how vital sign monitoring is used across ICU, operating room, and emergency settings. Company annual reports, investor decks, earnings call transcripts, and credible press releases help validate product mix changes and regional demand signals, and we also use paid subscriptions for company financials and news screening, plus patent databases to track platform refresh cycles. These sources are not exhaustive, and many other public documents were reviewed to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work is used to pressure test what desk research cannot fully show, especially pricing ranges, replacement timing, and the split between portable, wearable, and fixed bedside systems. We speak with a mix of device manufacturers, distributors, hospital biomedical teams, and clinicians, and we also include feedback from homecare providers and emergency medical services so the final assumptions reflect different buying pathways across regions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 14% | APAC: 49% |

| Mid tier: 50% | Functional/Unit leaders: 37% | EMEA: 31% |

| Smaller Players: 18% | Managers: 49% | Americas: 20% |

Market-Sizing & Forecasting

For sizing, the core model starts from a demand pool view where hospital and outpatient procedure volumes, critical care bed footprint, and monitored patient days help reconstruct the likely install base and annual purchase needs by region. Once that top-down estimate is formed, it is corroborated with selective bottom-up checks such as sampled average selling prices by device class, channel markups, and supplier and distributor revenue splits, which are then used to adjust totals where the first pass looks stretched.

Key inputs used in the model include ICU and operating room utilization trends, chronic disease burden that increases monitoring intensity, the shift toward remote and wearable monitoring in step-down and home settings, replacement cycles for bedside monitors, and ASP movement linked to connectivity and software enabled features. Forecasts are built using scenario analysis around hospital capex budgets, staffing constraints that favor automation, and region level adoption speed for connected monitoring, followed by a sanity check against historical growth patterns. Where bottom-up inputs are missing for smaller countries, proxy pricing and penetration rates are applied from comparable markets and then validated through interviews.

Data Validation & Update Cycle

Outputs are cross checked against independent signals like device shipment commentary in public filings, regulatory approval cadence, and hospital procurement direction discussed by interviewees. Variances are reviewed in more than one step, and outliers trigger rechecks of the underlying drivers such as ASP, replacement timing, and end user mix before the model is finalized.

Reports are refreshed annually, and interim updates are made when major events materially change demand or pricing. Before delivery, we run a final review pass so the numbers and assumptions reflect the latest available information.

Mordor Intelligence's Multi Parameter Patient Monitoring Market Size Compared With Other Published Estimates

Published market values for multi-parameter patient monitoring can differ because each study draws the line around products and settings in its own way, and then uses different price and adoption assumptions to extend the forecast. Differences also show up when base years change, when currency conversions use different timing, and when some updates lag behind recent product refresh cycles.

Disposable sensor probes and other single use monitoring consumables sit outside Mordor Intelligence's scope, which commonly reduces the total versus estimates that bundle device revenue together with recurring consumable spend. In addition, some published totals lean on an aggressive remote monitoring ramp without checking it against hospital replacement cycles and realistic ASP movement for portable versus fixed systems, which can lift near term values.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.20 B (2026) | |

| Global Consultancy A | USD 12.90 B (2024) | Uses an earlier base year and often blends broader patient monitoring system revenue into the total, which can dilute multi-parameter specific device pricing and mix shifts. |

| Industry Publisher B | USD 13.54 B (2025) | May include adjacent recurring spend tied to monitoring episodes and applies generalized ASP progression, which can overstate revenue where price erosion offsets feature driven upgrades. |

The spread in the table largely comes from what is counted as device revenue versus adjacent recurring items, and from the chosen starting year for the model. By keeping the inputs traceable to install base logic, care setting mix, and realistic ASP ranges, the final number stays repeatable and easier to reconcile when new information arrives.

Key Questions Answered in the Report

How large is the multi-parameter patient monitoring market today and how fast is it growing?

The multi-parameter patient monitoring market size reached USD 13.2 billion in 2026 and is projected to hit USD 18.75 billion by 2031, translating into a 7.28% CAGR.

Which device category is expanding the quickest?

Wearable and remote monitors are forecast to grow at an 8.23% CAGR, outpacing all other device types as sensor miniaturization and reimbursement incentives favor continuous home surveillance.

What drives the surge in Asia-Pacific demand?

Large-scale digital-health programs such as India's Ayushman Bharat Digital Mission and China's adherence to WHO interoperability frameworks underpin a 10.44% CAGR across Asia-Pacific.

Why are hospitals investing in portable monitors?

Higher patient acuity, staffing shortages and the need to minimize intrahospital transfers prompt hospitals to adopt portable multi-parameter units that maintain ICU-grade accuracy at the bedside.

How does reimbursement influence remote monitoring uptake?

U.S. Medicare CPT 99453-99458 payments and similar European schemes compensate providers for device setup, data transmission and clinician review, making remote physiological monitoring financially sustainable.

Which clinical application shows the highest growth potential?

Respiratory monitoring leads with a projected 8.72% CAGR as post-COVID care models stress early detection of ventilation deterioration and continuous oxygen saturation tracking.

Page last updated on: