Thoracic Drainage Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

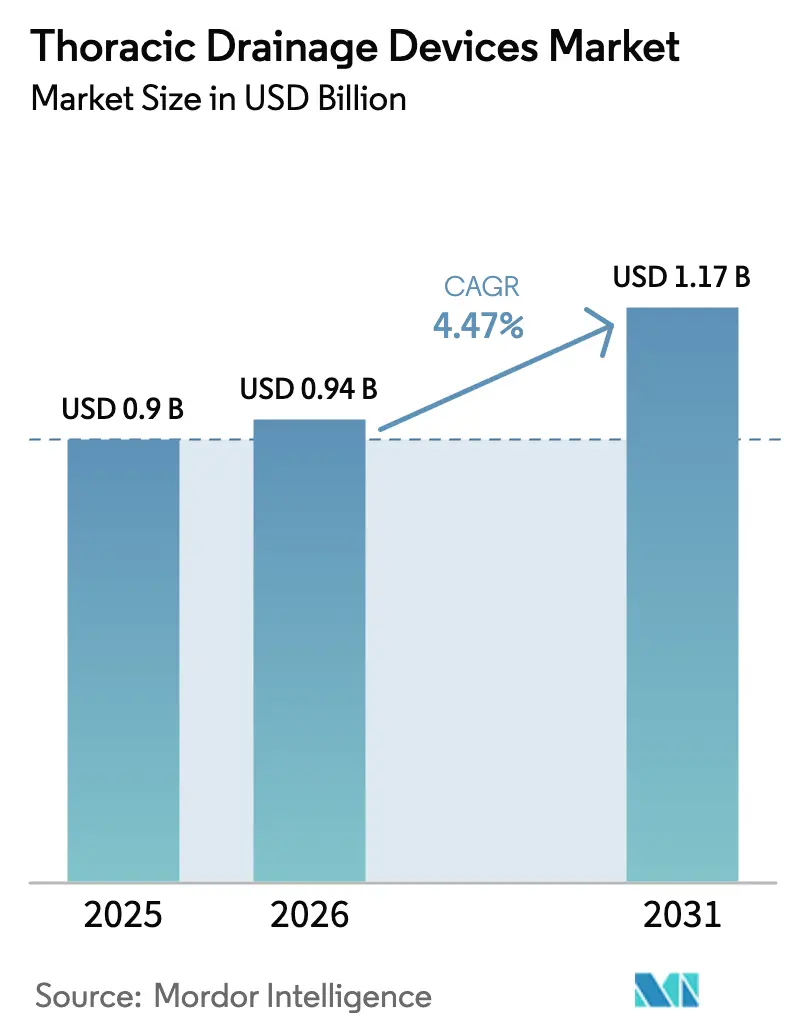

| Market Size (2026) | USD 0.94 Billion |

| Market Size (2031) | USD 1.17 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

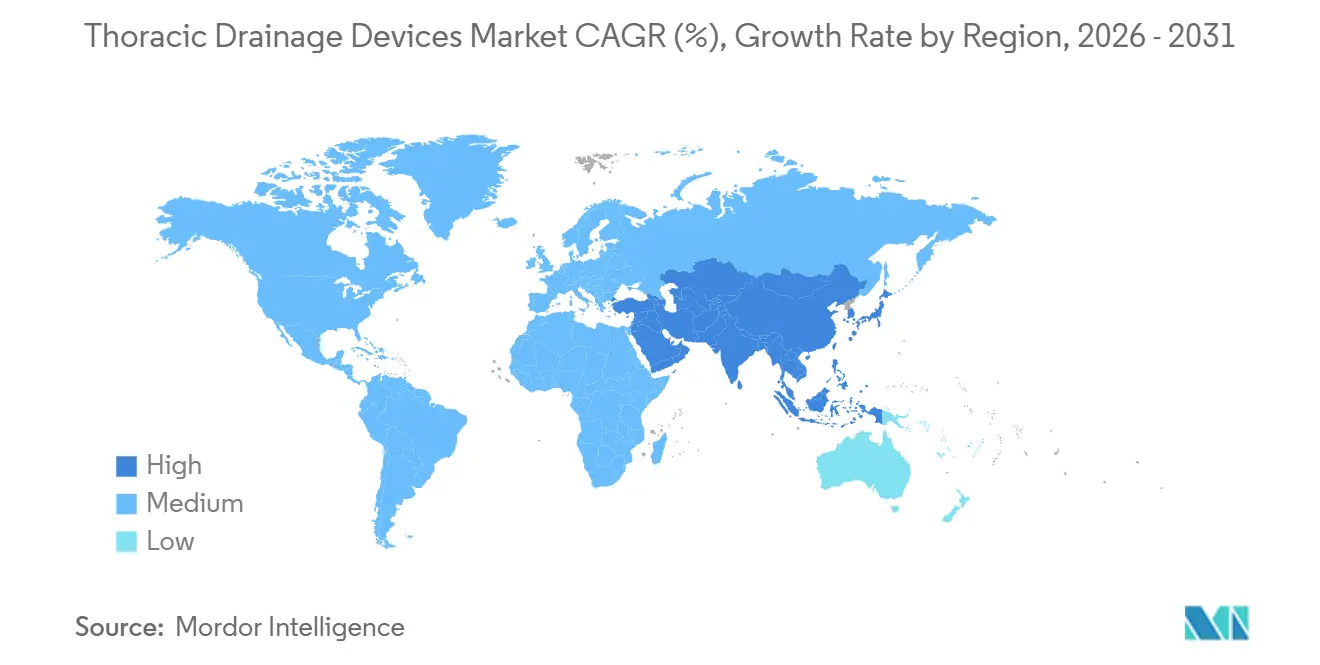

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

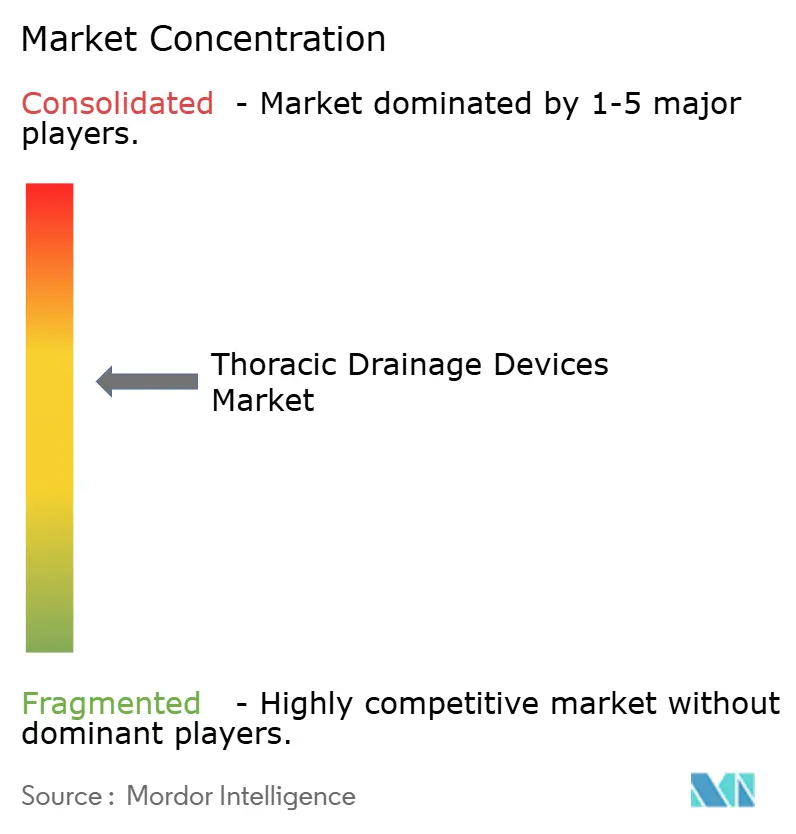

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thoracic Drainage Devices Market Analysis by Mordor Intelligence

The Thoracic Drainage Devices Market size is expected to grow from USD 0.9 billion in 2025 to USD 0.94 billion in 2026 and is forecast to reach USD 1.17 billion by 2031 at 4.47% CAGR over 2026-2031.

Remote-care reimbursement, product digitization, and material substitution collectively shape demand while moderating headline growth. Ambulatory surgical centers are expanding procedure volumes at an 8.05% annual rate, nearly 400 basis points ahead of hospitals, and digital platforms are replacing analog water-seal units in intensive care and ECMO protocols. North America remains the revenue anchor, yet the Asia-Pacific is narrowing the gap, driven by China’s Healthy China 2030 initiative and India’s Ayushman Bharat facility upgrades. However, white-space opportunities exist in home-based ECMO, AI-assisted air-leak detection, and biodegradable catheter coatings, inviting new entrants.

Key Report Takeaways

- By product type, chest drainage systems captured a 37.81% revenue share of the thoracic drainage devices market in 2025, whereas thoracic drainage kits are projected to grow at a 6.38% CAGR through 2031.

- By material composition, silicone accounted for 46.13% of the thoracic drainage devices market size in 2025, while polyurethane is expected to expand at a 6.81% annual rate through 2031.

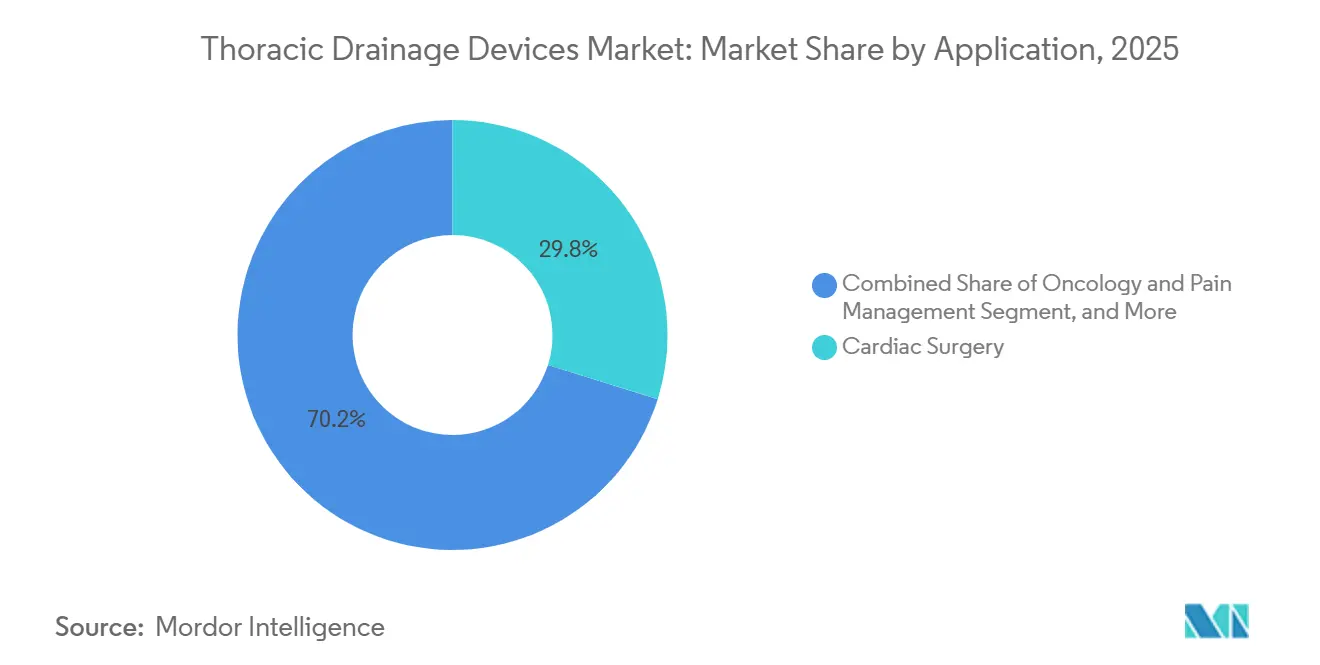

- By application, cardiac surgery led with a 29.85% market share of thoracic drainage devices in 2025, while oncology and pain management are advancing at a 5.58% CAGR through 2031.

- By end user, hospitals retained 54.06% revenue share in 2025; ambulatory surgical centers recorded the fastest CAGR at 8.05% through 2031.

- By geography, North America held a 39.64% market share of the thoracic drainage devices market in 2025; the Asia-Pacific region is projected to rise at a 7.32% annual rate through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Thoracic Drainage Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Pleural Diseases | +0.9% | North America, Europe, global burden in aging populations | Medium term (2-4 years) |

| Increasing Thoracic & Cardiac Surgery Volumes | +1.1% | North America, Europe, China, India, Japan | Short term (≤ 2 years) |

| Technological Advances in Digital Drainage Systems | +0.8% | Early adopters in North America, EU; APAC uptake post-2028 | Long term (≥ 4 years) |

| Growing Adoption of Minimally-Invasive & Robotic Procedures | +0.7% | North America, Western Europe, urban APAC hubs | Medium term (2-4 years) |

| Home-Hospital Reimbursement Models Boosting Portable Devices | +0.6% | United States, Germany, UK, Australia | Short term (≤ 2 years) |

| ECMO & Lung-Transplant Program Expansion | +0.4% | Academic centers in North America, Europe, Singapore, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Pleural Diseases

More than 1.5 million U.S. patient admissions per year require pleural drainage, and spontaneous pneumothorax is increasing 2.3% annually in adults aged ≥ 65.[1]Centers for Disease Control and Prevention, “Pleural Disease Surveillance,” cdc.gov Similar momentum in Germany, France, and the UK shows a 4.1% rise in diagnoses between 2024 and 2025. Medicare payment reforms that reward same-day discharge are increasing outpatient small-bore catheter deployment, now accounting for 40% of ambulatory cases. Low-income regions continue to have a demand for cost-effective large-bore solutions, as tuberculosis-related empyema remains a common condition. Device design pivots toward 14-Fr or smaller indwelling catheters that balance comfort with flow efficiency.

Increasing Thoracic & Cardiac Surgery Volumes

Thoracic surgery volumes rebounded to 3.2 million procedures in 2025, surpassing pre-pandemic peaks by 7%. Cardiac-surgery procedures reached 2.8 million worldwide due to aging demographics, and China’s reimbursement approval for robotic thoracic interventions triggered a 12% uptick in minimally invasive cases. The U.S. bundled-payment model incentivizes hospitals to deploy digital drainage devices that shorten stays.[2]Centers for Medicare & Medicaid Services, “Bundled Payment Arrangement 2025,” cms.gov However, Eastern Europe and Latin America lag as capital constraints and a limited surgical workforce suppress adoption.

Technological Advancements In Digital Drainage Systems

Digital platforms that integrate pressure and flow sensors reduce nursing workload by 30% per patient day. Medtronic’s Thopaz+ gained FDA clearance for ECMO support in 2024, while Getinge’s Atrium Ocean predicts removal readiness with 89% accuracy in German trials. Japan introduced an add-on reimbursement in 2025, which increased digital penetration to 18% of thoracic surgeries within six months. Upfront prices remain 3-5 times those of analog units, although rental programs at EUR 150 per episode are emerging in Germany to ease budget pressures.

Growing Adoption of Minimally-Invasive & Robotic Procedures

Robotic-assisted lobectomy accounted for 22% of U.S. cases in 2025, up from 15% in 2024. These techniques favor 12-Fr to 14-Fr tubes, enabling shorter immobilization times. Europe’s demand for auditable outcome data under its Medical Device Regulation increases the utilization of digital drainage. South Korea expanded robotic-surgery coverage to 12 thoracic indications in 2024, resulting in a 19% year-over-year increase in minimally invasive procedures.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Digital Systems | -0.7% | India, Southeast Asia, Latin America, cost-pressured EU hospitals | Short term (≤ 2 years) |

| Stringent Regulatory Approvals & Recalls | -0.4% | North America, EU under MDR | Medium term (2-4 years) |

| Sustainability Mandates Targeting Single-Use Plastics | -0.3% | EU, California, select APAC markets | Long term (≥ 4 years) |

| Shortage of Thoracic Nursing Specialists | -0.5% | Rural North America, Eastern Europe, sub-Saharan Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Digital Systems

Digital units list at USD 2,500–4,000 versus USD 600–800 for analog, restricting uptake in India where only 8% of hospitals deploy them. Brazil’s fixed reimbursement lacks differentiation, disincentivizing upgrades. The UK negotiated a 22% discount to maintain cost neutrality, taking into account nursing savings. Rental models ease barriers, yet the total cost of ownership stays 40–60% higher.

Stringent Regulatory Approvals & Recalls

Fourteen FDA Class II recalls in 2024–2025 highlighted catheter-tip separation and canister failures.[3]U.S. Food and Drug Administration, “Medical Device Recalls 2024-2025,” fda.gov Europe’s MDR re-certification costs average EUR 500,000 per product line, delaying 23 launches by early 2026. China’s unannounced factory inspections added a four-month approval lag.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Kits Gain as Efficiency Trumps Customization

Chest drainage systems accounted for 37.81% of the revenue in 2025. In contrast, thoracic drainage kits, valued for their sterilized convenience, are projected to outpace the market at a 6.38% CAGR, driven by ASC demand. Small-bore pleural catheters (≤14 Fr) predominate in the outpatient management of malignant effusions, whereas large-bore variants remain crucial for the treatment of trauma and empyema. Digital systems, though fewer in unit shipments, command 40–50% price premiums and lock in disposable revenue.

By Material Composition: Polyurethane Closes the Gap on Silicone

Silicone represented 46.13% of material revenue, favored for biocompatibility. Polyurethane is closing the gap with a 6.81% annual growth rate, aided by thin-wall extrusion technologies. PVC’s share of the thoracic drainage devices market size is expected to drop below 10% by 2031 as regulatory curbs escalate. Advanced polymers such as antimicrobial-coated polyurethane reduce infections by 38%, supporting a 30% price premium.

By Application: Oncology Rises as Cardiac Surgery Plateaus

Cardiac surgery held 29.85% of the thoracic drainage devices market share in 2025, but this is expected to slow as transcatheter interventions reduce chest-tube dwell time. Oncology and pain management advance at a rate of 5.58% annually, reflecting the prevalence of malignant pleural effusion in approximately 150,000 U.S. patients each year. Trauma and infectious disease segments remain steady in emerging economies.

By End User: Ambulatory Centers Disrupt Hospital Dominance

Hospitals retained 54.06% revenue in 2025. However, ASC volumes climb at 8.05% as Medicare adds 18 thoracic procedures to its approved list. Home healthcare, though smallest, is expanding rapidly as portable devices enable remote management and 31% global placement growth of PleurX catheters in 2025.

Geography Analysis

North America’s thoracic drainage devices market share was 39.64% in 2025, as digital platforms gained penetration in academic centers above 22%. Medicare’s Hospital-at-Home expansion accelerated demand for portable catheters, while Canada piloted digital devices to cut ICU stays. Germany’s DRG system favors analog systems, whereas the UK negotiated national contracts that bundle device cost with reduced nursing time. France and Italy expanded surgical capacity via public-private partnerships, although expenditure caps limit digital conversion.

The Asia-Pacific market is expected to grow at a 7.32% annual rate through 2031. China is establishing 120 thoracic centers under the Healthy China 2030 initiative, which is funded by the government. India’s procedure volumes increased by 19% after the inclusion of Ayushman Bharat reimbursement. Japan and South Korea’s expansion of robotic-surgery coverage further boosts demand for small-bore catheters.

Competitive Landscape

The top five vendors, Medtronic, Teleflex, Becton Dickinson, Getinge, and Cardinal Health, control a significant market share of the thoracic drainage devices market through group-purchasing agreements. Their strategies converge on AI-enabled digital platforms, Asia-Pacific sales expansion, and vertical integration of disposable components. Patent issuance reached 47 in 2024-2025, underscoring the intensity of innovation. New entrants such as Centese and Sinapi Biomedical leverage ISO 13485 contract manufacturing in Southeast Asia to undercut prices by up to 30% while meeting FDA 510(k) and CE standards.

Home-based ECMO support remains a frontier opportunity; an estimated 10,000 U.S. candidates annually lack access to ICU beds, creating a demand for portable oxygenation and drainage systems. Regulatory stringency under the MDR and China’s surveillance program is forcing consolidation, giving well-capitalized incumbents a compliance advantage.

Thoracic Drainage Devices Industry Leaders

Becton Dickinson and Company

Getinge AB

Smith Medical

Cook Medical

Teleflex Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Coaxial silicone drains demonstrated significant postoperative pain reduction after VATS lobectomy.

- October 2024: The FDA disclosed review timelines for the Gore Tag Thoracic Branch Endoprosthesis, highlighting evidence barriers for complex devices.

- June 2024: Pleural Dynamics treated the first patient with its fully implantable automatic effusion shunt in a clinical trial.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the thoracic drainage devices market as all single-use or reusable catheters, kits, trocar drains, and digital or analog chest drainage systems designed to clear air, blood, or fluid from the pleural or mediastinal space after trauma or surgery. Values represent factory-gate revenue from new units and their proprietary disposables, expressed in USD.

Scope Exclusions: simple wound drains, abdominal or neurosurgical drainage systems, and rental-only service contracts are not counted.

Segmentation Overview

- By Product Type

- Chest Drainage Systems

- Water-Seal Systems

- Dry-Seal Systems

- Digital / Automated Systems

- Pleural Drainage Catheters

- Small-Bore

- Large-Bore

- Thoracic Drainage Kits

- Trocar Drains

- Secured Needles

- Unsecured Needles

- Accessories

- Chest Drainage Systems

- By Material Composition

- Silicone

- Polyurethane

- Polyvinyl Chloride (PVC)

- Latex

- Other Advanced Polymers

- By Application

- Thoracic Surgery & Pulmonology

- Cardiac Surgery

- Trauma & Emergency Medicine

- Oncology & Pain Management

- Infectious Diseases

- Intensive Care & ECMO

- Others

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Thoracic & Cardiac Centers

- Home Healthcare Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed thoracic surgeons, trauma physicians, ICU nurses, and supply managers in the United States, Germany, India, and Brazil. Their feedback on digital-drain uptake, kit replacement cycles, and reimbursement nuances sharpened model inputs and confirmed price corridors.

Desk Research

We map procedure volumes and installed base using open datasets such as the WHO Global Health Observatory, OECD hospital-discharge files, Eurostat surgical registers, the US FDA MAUDE alerts, and leading thoracic journals. Company 10-Ks, procurement portals, and public price lists refine average selling prices, while D&B Hoovers and Dow Jones Factiva validate manufacturer revenue splits. This list is illustrative; many additional public records supported data collection and clarification.

Market-Sizing & Forecasting

A top-down rebuild of cardiac, thoracic, and trauma surgeries links procedure counts to device utilization ratios, then cross-checks bottom-up with sampled supplier shipments. Key variables modeled include pneumothorax incidence, average length of stay, digital system share, inflation-adjusted ASP, and hospital bed growth. Multivariate regression supported by scenario analysis projects demand through 2030; gaps in supplier data are bridged with channel checks and weighted averages.

Data Validation & Update Cycle

Outputs pass anomaly scans, senior analyst review, and management sign-off. We refresh annually and issue interim updates for recalls, guideline changes, or currency swings.

Why Our Thoracic Drainage Devices Baseline Commands Reliability

Published estimates vary because firms choose different product baskets, price decks, and refresh cadences. Mordor's clear scope, dual-path validation, and yearly update narrow those gaps.

Key gap drivers include some studies that fold wound drains, others that ignore digital systems, and several that rely on aging procedure datasets that miss ambulatory centers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.83 B (2025) | Mordor Intelligence | |

| USD 0.89 B (2024) | Global Consultancy A | excludes smart systems; older ASP bench |

| USD 1.20 B (2024) | Trade Journal B | bundles vacuum wound drains; broad kit overlap |

Mordor's disciplined scope and frequent refresh therefore give clients a transparent, dependable baseline for planning.

Key Questions Answered in the Report

How large will the thoracic drainage devices market be by 2031?

It is projected to reach USD 1.17 billion, reflecting a 4.47% CAGR from 2026 to 2031.

Which product segment grows fastest?

Thoracic drainage kits are forecast at a 6.38% CAGR because ASCs prefer turnkey sterile bundles.

Why is polyurethane gaining material share?

Thin-wall extrusion enables smaller-bore catheters and helps comply with PVC phase-out mandates in the EU.

What drives Asia-Pacific growth?

China’s infrastructure spending and India’s Ayushman Bharat reimbursement add surgical capacity, lifting procedure volumes.

Do digital drainage systems justify their premium?

Academic studies show 1–2 day shorter hospital stays and 30% lower nursing workload, offsetting higher device cost in high-acuity centers.

Page last updated on: