Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

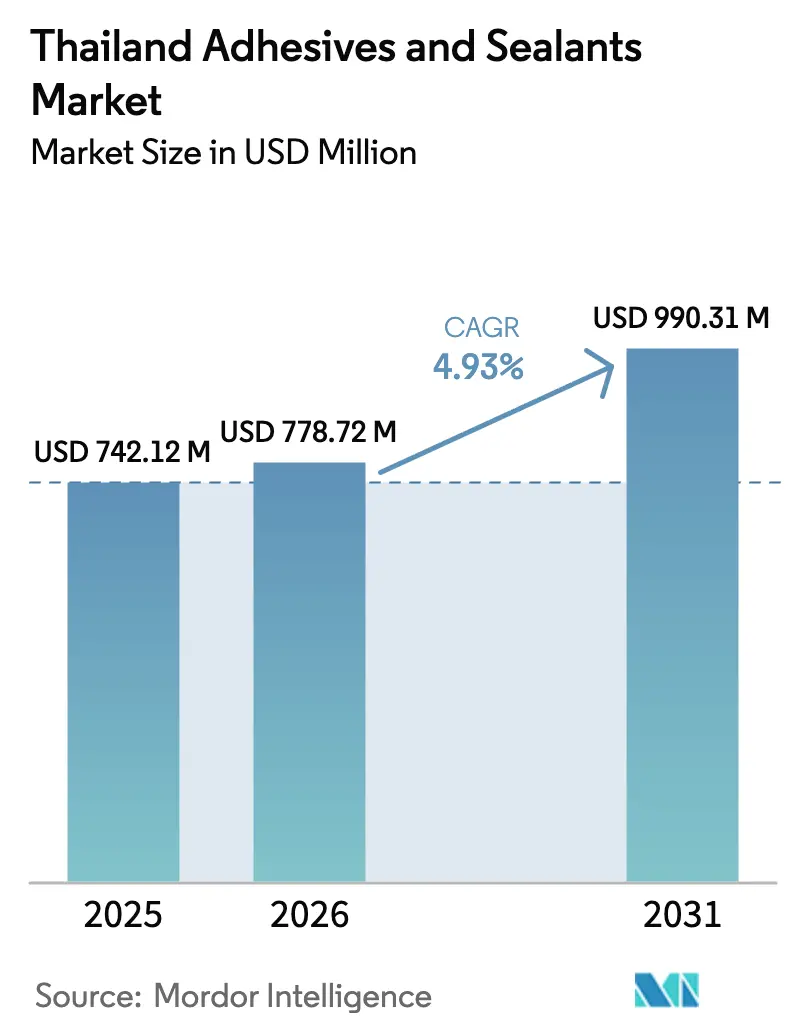

| Base Year Market Size (2025) | USD 742.12 Million |

| Market Size (2026) | USD 778.72 Million |

| Market Size (2031) | USD 990.31 Million |

| Growth Rate (2026 - 2031) | 4.93% CAGR |

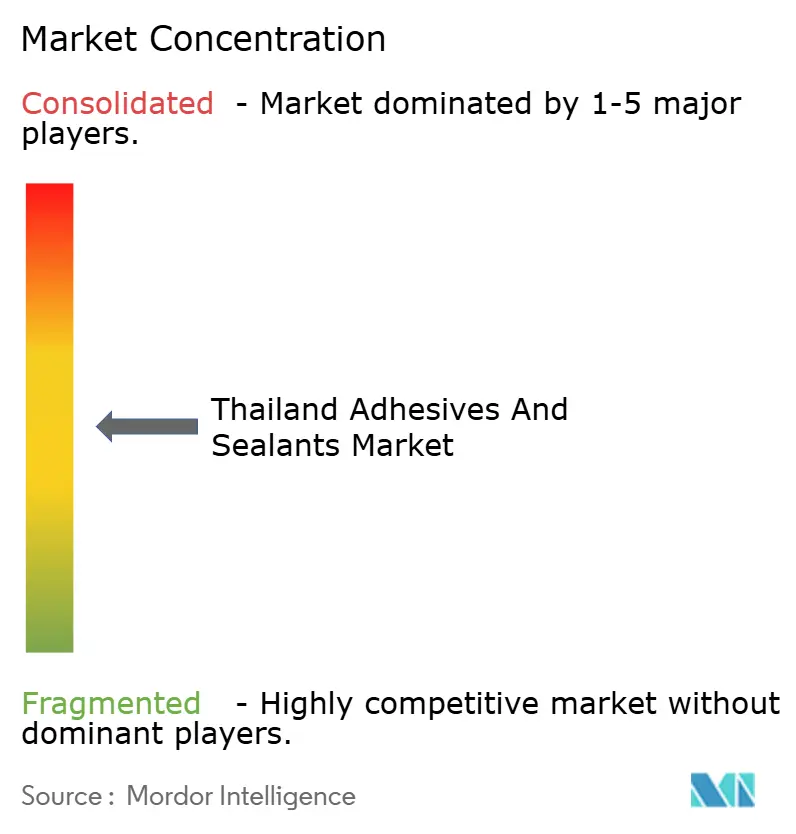

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Adhesives And Sealants Market Analysis by Mordor Intelligence

Thailand Adhesives and Sealants Market size in 2026 is estimated at USD 778.72 million, growing from 2025 value of USD 742.12 million with 2031 projections showing USD 990.31 million, growing at 4.93% CAGR over 2026-2031. Recent momentum stems from investments in electric vehicles, fast-moving consumer goods packaging upgrades, and electronics incentives, collectively shifting demand toward higher-value bonding solutions. Automotive suppliers are shifting away from spot welding toward structural epoxy and polyurethane bonds to meet lightweighting targets, while packaging converters are rapidly adopting water-borne chemistries to comply with volatile organic compound (VOC) regulations. Government tax holidays for printed-circuit-board capacity have spurred the development of UV-cured formulations that deliver sub-second cure times and zero-solvent emissions. At the same time, silicone sealants maintain a strong hold in building façades and automotive glazing due to their unrivaled weatherability. Moderate fragmentation among formulators persists, even though upstream petrochemical feedstock remains concentrated, creating input cost volatility and encouraging downstream consolidation.

Key Report Takeaways

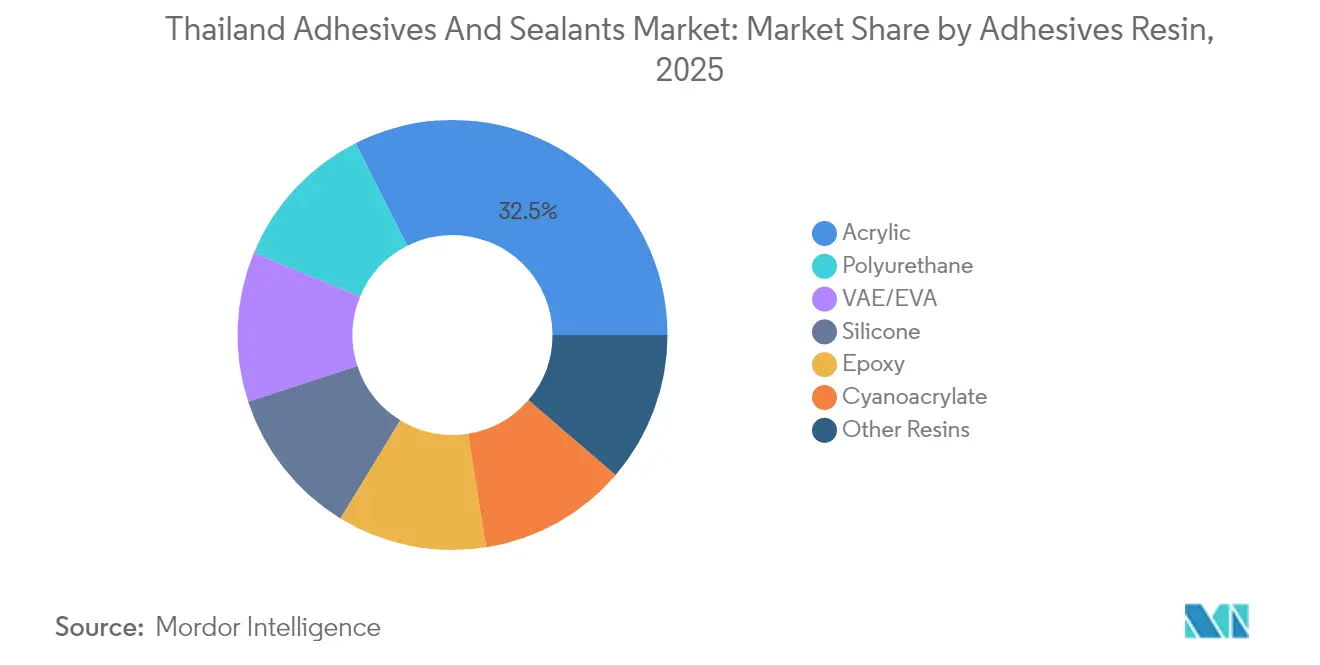

- By adhesive resin, acrylics held 32.45% of Thailand's adhesives and sealants market share in 2025, whereas polyurethane is set to expand at a 7.17% CAGR to 2031.

- By adhesive technology, water-borne adhesives captured a 44.05% share of the Thailand adhesives and sealants market in 2025, while UV-cured adhesives are advancing at a 6.62% CAGR through 2031.

- By sealant resin, silicone delivered 46.00% in 2025, while polyurethane registered the fastest 5.69% CAGR through 2031.

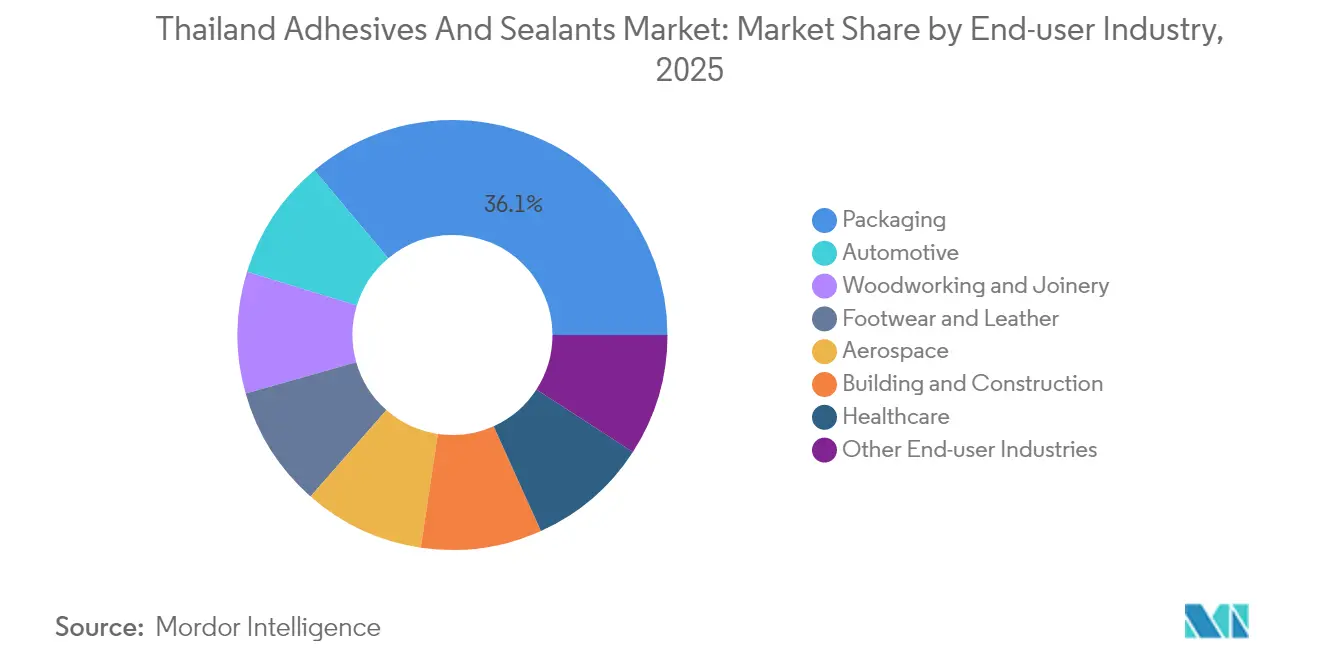

- By end user, packaging commanded 36.10% of the revenue in 2025, and the automotive sector leads the growth outlook with a 5.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand from packaging industry | +1.8% | Samut Prakan, Chonburi, Rayong industrial estates | Medium term (2–4 years) |

| Shift toward adhesive bonding for composite materials | +0.9% | Eastern Economic Corridor, Bangkok aerospace clusters | Long term (≥4 years) |

| Expansion of domestic automotive and EV production | +1.5% | Samut Prakan, Chonburi, Ayutthaya, Rayong | Medium term (2–4 years) |

| Government incentives for Electrical and Electronics clusters | +1.2% | Eastern Economic Corridor, Lamphun | Short term (≤2 years) |

| Rising preference for bio-based adhesives | +0.6% | Export-oriented packaging and furniture hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Demand from Packaging Industry

Packaging accounts for 36.42% of Thailand's adhesives and sealants market demand in 2024, anchoring converters that supply shelf-stable foods to global buyers. National programs that brand the country as the “Kitchen of the World” keep flexible pouches, aseptic cartons, and mono-material films in the spotlight. Water-borne and hot-melt chemistries are suitable for recyclable substrates, while high-molecular-weight polyester investments by adhesive makers ensure local supply continuity[1]Bostik Global Team, “Industrial, Construction & DIY Adhesives,” bostik.com. Because household debt levels dampen domestic retail sales, export momentum, and ASEAN free-trade agreements play a larger role in volume swings. Currency strength against the U.S. dollar introduces an additional variable to revenue recognition for exporters. With sustainability audits on the rise, converters are favoring low-VOC and food-contact-approved grades that expedite certification cycles for shipping into Europe and North America.

Shift Toward Adhesive Bonding for Composite Materials

Thailand’s Board of Investment strategy targets advanced manufacturing, which accelerates the uptake of composites in automotive body panels, wind-turbine blades, and smart glazing. Adhesive bonding eliminates stress concentrations created by rivets and bolts, thereby preserving fiber integrity and reducing vehicle weight. Sekisui Chemical’s investment in interlayer films in Rayong underscores this shift toward optical clarity adhesives for displays and glazing. Local automotive clusters now benchmark European crash-management designs, opening opportunities for crash-resistant polyurethane and epoxy systems. Once cost parity against stamped steel improves, tier-one suppliers are expected to migrate larger panel areas to composite substrates. The shift also strengthens demand for metering and dispensing equipment capable of mixing high-modulus epoxy pastes within tight tolerances.

Expansion of Domestic Automotive and EV Production

Under the government's 30:30 policy, which aims to achieve 30% zero-emission vehicles by 2030, new investments are flowing into battery-electric and plug-in hybrid platforms. Chang’an Automobile, with its program, mandates high local content, emphasizing the need for local sourcing of adhesives for battery enclosures, body-in-white, and interiors. Electrification removes exhaust heat limits, allowing newer chemistries with lower temperature resistance, while battery packs introduce tougher flame-retardancy and thermal-conductivity criteria. Henkel’s Bangpakong smart factory, equipped with IATF 16949 certification and zero-defect analytics, demonstrates how adhesive suppliers align with automotive quality gates[2]Henkel Press Office, “Medical,” henkel.com. Tier-two metal-stamping shops now retrain staff to dispense one-component structural adhesives, replacing spot weld cells in underbody frames. The net effect is a wider portfolio of high-strength, crash-durable bonds that directly feed into the rising Thailand adhesives and sealants market demand.

Government Incentives for Electrical and Electronics Export-Oriented Clusters

Merit-based tax exemptions of up to eight years have attracted investment in printed-circuit-board plants, imposing stringent requirements on bond strength at reflow-soldering temperatures exceeding 260 °C. UV-cured acrylics are featured prominently because LED units achieve near-instant polymerization without the need for thermal loading. Tesa’s Bangkok Customer Solution Center houses climate chambers that simulate tropical humidity cycles, enabling co-design of high-tack films for smartphone camera modules. The Competitive Enhancement Act also provides financial support for green projects, enabling mid-sized formulators to finance low-VOC reactors. Electronics assemblers insist on flux and residue-free surfaces, so suppliers are calibrating dispensing robots to control adhesive flow to micrometer precision. These shifts solidify technology upgrades inside the wider Thailand adhesives and sealants market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC regulations | -0.8% | National industrial estates under IEAT oversight | Short term (≤2 years) |

| Volatility in petrochemical feedstock prices | -1.1% | Nationwide, affecting solvent-borne and reactive grades | Medium term (2–4 years) |

| Limited cold-chain infrastructure | -0.4% | Rural provinces and secondary cities | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC Regulations

Thailand’s Hazardous Substances Act compels factories using more than 1 tonne of volatile organic compounds annually to register emissions inventories. Water-borne grades lengthen drying times, reducing line speed, while two-component epoxies increase capital expenditures for metering equipment. Small furniture and footwear workshops struggle the most with the shift, as limited access to capital and technical skills hinders rapid upgrades. Multinational converters, however, already operate enclosed lines with oxidizers and can transition faster, gaining a compliance edge. VOC stringency, therefore, widens the capability gap between larger and smaller players in the Thailand adhesives and sealants market.

Volatility in Petrochemical Feedstock Prices

Naphtha feedstock prices are projected to decline in the coming years. This decline alleviates some cost pressures, yet quarterly price swings remain unpredictable. PTT Chemical and SCG dominate the market, supplying the majority of the country's ethylene and propylene. As a result, any fluctuations in crack spreads directly impact the cost bases of acrylics, styrene-butadiene, and polyurethanes. Smaller formulators, lacking access to hedging instruments and facing heightened working-capital demands, risk margin compressions. Producers are turning to process-efficiency projects, like IRPC’s upgrade to expandable polystyrene that reduces CO₂ intensity, leveraging energy savings to counteract raw-material price volatility. Looking ahead, while bio-feedstocks present an opportunity to diversify input sources, their current scale remains limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Adhesives Resin: Polyurethane Gains as Construction and Automotive Demand Structural Bonds

Acrylic resins commanded 32.45% of the adhesive-resin market share in 2025, a legacy of their versatility in pressure-sensitive tapes, labels, and general-purpose assembly. However, polyurethane chemistries are expected to expand at a 7.17% CAGR through 2031, nearly double the growth rate of acrylic. Polyurethanes combine 300% elongation with strong adhesion to powder-coated metals, aligning with façade panels and e-mobility body parts. Covestro’s specialty isocyanate expansion inside Rayong shortens lead time and stabilizes supply for formulators. Acrylic emulsions remain a staple in pressure-sensitive labels, where cost is more important than load-bearing strength. Epoxies retain niche roles in aerospace composites and semiconductor underfill due to their thermal endurance, but two-part mixing restrains high-volume adoption. Growing bio-polyols sourced from palm or castor oil blend into polyurethanes, enhancing renewable content without degrading performance.

Silicones remain premium, finding use in electronics encapsulation and automotive glazing, where thermal and UV resistance take precedence over price. Cyanoacrylates meet the needs of small-part assembly, including catheter bonding in nascent medical lines. VAE and EVA copolymers maintain a sizable market share in woodworking due to their water-borne grades, which clean up easily and cure at ambient temperatures. Resin substitution trends thus favor reactive chemistries that balance compliance and higher bond strength inside the Thailand adhesives and sealants market.

By Adhesives Technology: UV-Cured Formulations Accelerate in Electronics Assembly

Water-borne adhesives hold a 44.05% share, while UV-cured grades advance fastest at a 6.62% CAGR, driven by the need for millisecond cures in applications such as smartphone cameras, flexible circuits, and wearable sensors. Tesa’s Bangkok lab validates UV tapes under tropical humidity, offering customers joint development and rapid prototyping. Hot-melt lines continue to be used in case-sealing jobs where instant tack outweighs heat-resistance limits. Solvent-borne options are shrinking amid stronger VOC enforcement, prompting footwear makers to trial water-borne aliphatic polyurethane dispersions that offer equivalent solvent performance on synthetic leather. Reactive two-component epoxies remain the go-to choice for structural parts requiring high modulus and chemical resistance, even though the addition of dosing gear increases cost. Grants under the Competitive Enhancement Act reduce these barriers by subsidizing automated dispensing systems. Adoption speed varies by enterprise size, with multinationals upgrading the fastest and small workshops lagging.

By Sealants Resin: Silicone Dominance Rooted in Construction and Automotive Glazing

Silicone sealants hold a 46.00% share because government infrastructure spending through 2025 continues to finance mass-transit lines, airports, and tower façades that specify silicone for its UV stability. Automotive glazing also relies on silicone to withstand temperature cycles ranging from -40 °C to +100 °C. Polyurethane sealants are projected to grow at a 5.69% CAGR, driven by applications in industrial flooring, cold storage, and precast-panel joints that benefit from their adhesion to damp concrete. Acrylic latex caulkers are suitable for interior trim where paintability is key, but they suffer outdoors in monsoon moisture. Epoxy and polysulfide maintain niche presence in chemical tanks, bridges, and insulating glass where mechanical and chemical resistance supersede cost. Sekisui Chemical’s interlayer film plant further underscores glass-bonding innovation, requiring parallel sealant performance for optical clarity.

By End-User Industry: Automotive Fastest Growth as EV Mandates Reshape Supply Chains

Packaging still tops demand at 36.10%, but the automotive sector exhibits the highest 5.46% CAGR to 2031, as local content rules for battery-electric vehicles draw adhesives deeper into the chassis, battery, and trim. The building and construction sector benefits from public and private projects, consuming tile adhesives, flooring systems, and curtain-wall sealants. Footwear volumes face wage-cost pressure, yet AICA’s stake in ADB Sealant promises scale efficiencies that may stabilize competitiveness. Woodworking remains an export-oriented industry, so formaldehyde-free and FSC-compliant adhesives are more likely to win bids. Healthcare remains small but strategic, leveraging Henkel’s medical-grade LOCTITE portfolio to support plans for a Thai medical device hub. Aerospace remains modest due to a focus on maintenance rather than full airframe builds.

Geography Analysis

Central Thailand and the Eastern Economic Corridor together account for a major portion of Thailand's adhesives and sealants market consumption. Map Ta Phut hosts integrated crackers owned by PTT Chemical and SCG, giving local formulators feedstock proximity. Henkel’s Bangpakong smart plant, certified to ISO 9001, ISO 14001, ISO 45001, and IATF 16949, underlines the corridor’s pull for advanced production. The Northern Lamphun electronics cluster absorbs UV-curable adhesives for hard disk drives and semiconductors, but has ceded some market share as global HDD output consolidates. Southern rubber plantations produce raw latex, which is used to manufacture rubber-based adhesives. However, the distance from automotive hubs has restrained earlier hopes for local compounding plants. The northeastern agricultural belt remains a modest consumer, focused on wooden furniture and general assembly.

Competitive Landscape

The Thailand adhesives and sealants market is moderately fragmented. Multinationals compete on technical service and reliability. Local names counter with price agility and distribution depth. AICA Asia Pacific’s 51% acquisition of ADB Sealant in 2024 shows growing consolidation intent. Covestro’s specialty isocyanate expansion demonstrates vertical integration moves that shorten lead times for polyurethane systems. Environmental licensing through the Industrial Estate Authority’s Green Star evaluations now ties market access to VOC metrics, favoring compliant incumbents.

Thailand Adhesives And Sealants Industry Leaders

Henkel AG & Co. KGaA

Sika (Thailand) Limited

H.B. Fuller Company

Bostik

Selic Corp PCL.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Henkel introduced Loctite Liofol LA 7837/LA 6265, a solvent-free adhesive designed for high-temperature retort packaging that combines food safety with lower CO₂ by removing energy-intensive drying.

- December 2024: Arkema completed the purchase of Dow’s flexible packaging laminating adhesive line, strengthening Bostik’s portfolio in Thailand.

Thailand Adhesives And Sealants Market Report Scope

Adhesives are substances that create a strong, permanent bond between two surfaces, and sealants are materials used to fill gaps and joints to prevent the passage of liquids, gases, or noise. The Thailand adhesives and sealants market is segmented by product type, application, and geography. By Adhesive Resin Type, the market is segmented into polyurethane, epoxy, acrylic, silicone, cyanoacrylate, VAE/EVA, and other resins. By Adhesive Technology, the market is segmented into water-borne, solvent-borne, reactive, hot-melt, and UV-cured. By Sealant Resin Type, the market is segmented into silicone, polyurethane, acrylic, epoxy, and other resins. By End-user Industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, woodworking and joinery, and other industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Adhesives Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Silicone |

| Cyanoacrylate |

| VAE/EVA |

| Other Resins |

By Adhesives Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot-Melt |

| UV Cured |

By Sealants Resin

| Silicone |

| Polyurethane |

| Acrylic |

| Epoxy |

| Other Resins |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-user Industries |

| By Adhesives Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Silicone | |

| Cyanoacrylate | |

| VAE/EVA | |

| Other Resins | |

| By Adhesives Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot-Melt | |

| UV Cured | |

| By Sealants Resin | Silicone |

| Polyurethane | |

| Acrylic | |

| Epoxy | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the size of the Thailand adhesives and sealants market in 2026?

The market is valued at USD 778.72 million in 2026 and is projected to reach USD 990.31 million by 2031.

Which segment grows fastest through 2031?

Automotive applications are expanding at a 5.46% CAGR due to electric-vehicle mandates that require structural bonding and battery-pack sealing.

Why are UV-cured adhesives gaining share?

Electronics assembly lines in the Eastern Economic Corridor require sub-second curing without thermal stress, driving demand for UV-cured volumes.

What drives polyurethane demand in Thailand?

High-rise façade construction and electric-vehicle lightweighting favor polyurethane’s elongation and adhesion to diverse substrates.

How strict are VOC regulations on adhesive makers?

Plants using over 1 tonne of VOCs annually must register emissions inventories and pass estate-level Green Star audits, pushing a shift to water-borne or reactive chemistries.

Page last updated on: