Terminal Tractor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 1.78 Billion |

| Growth Rate (2026 - 2031) | 4.70% CAGR |

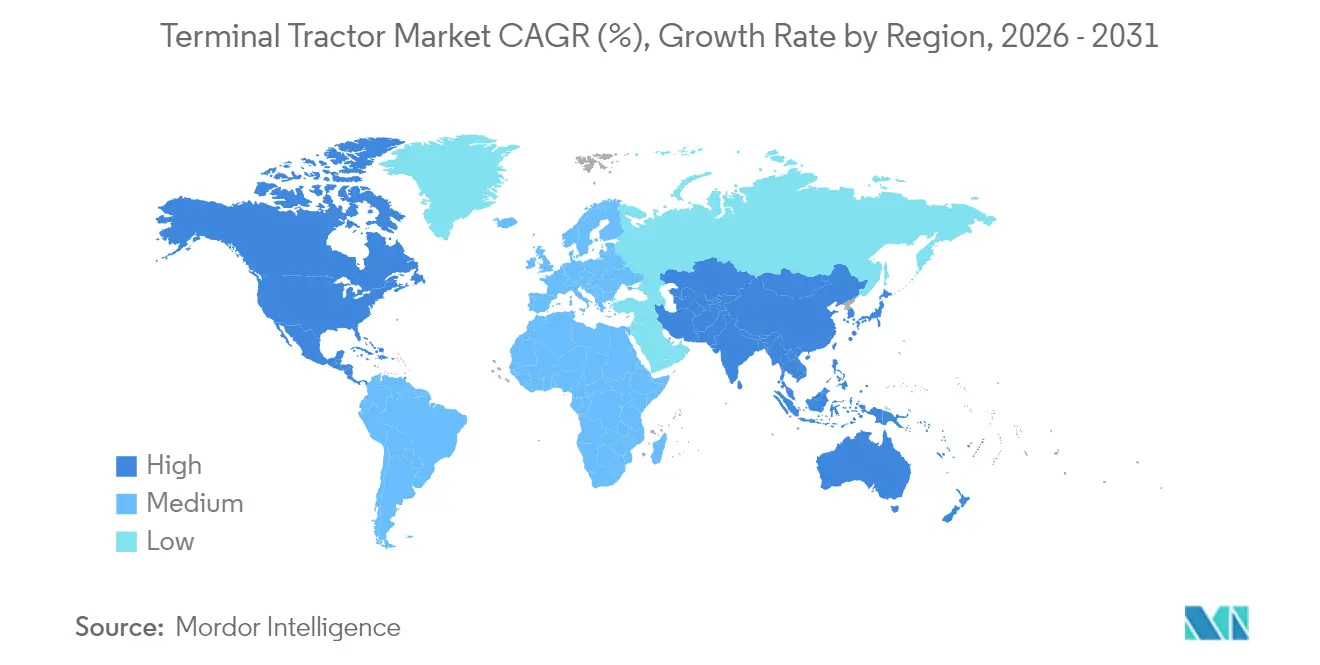

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Terminal Tractor Market Analysis by Mordor Intelligence

Terminal tractor market size in 2026 is estimated at USD 1.41 billion, growing from 2025 value of USD 1.35 billion with 2031 projections showing USD 1.78 billion, growing at 4.7% CAGR over 2026-2031. Growth is paced by accelerating electrification, tightening emissions regulation, and the steady rise of cooperative autonomy between software firms and established OEMs. Diesel units still anchor 63.20% of global demand, yet battery-electric alternatives record the highest expansion rate as ports and distribution hubs move to curb operating emissions and maintenance costs. North America retains the lead in revenue thanks to stringent California Air Resources Board rules, while Asia-Pacific posts the quickest up-trend on the back of Chinese port automation and Indian logistics investment. Rental and short-term leasing add another structural tailwind because operators want flexibility when propulsion and digital technologies change faster than a typical 7-year depreciation window. Across the terminal tractor market, fully autonomous models, premium 6x4 and 4x4 drivetrains, and higher-capacity (above 100 ton) variants command climbing order books as mega-vessels and e-commerce fulfillment centers sharpen performance requirements.

Key Report Takeaways

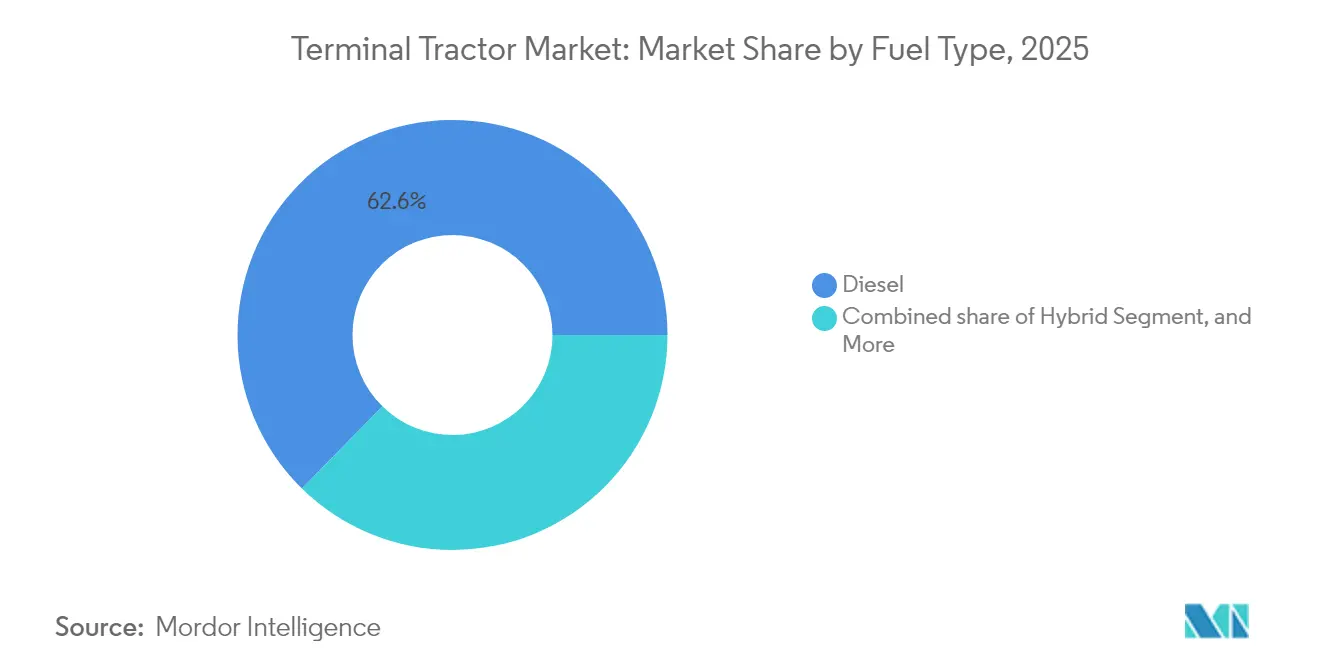

- By fuel type, diesel led with 62.65% of terminal tractor market share in 2025; battery-electric is projected to climb at an 17.6% CAGR to 2031.

- By vehicle type, manual operation held 74.55% of the terminal tractor market share in 2025, while fully autonomous units represent the fastest growth at a 21.2% CAGR through 2031.

- By drive configuration, 4x2 captured 64.10% of the terminal tractor market share in 2025; 6x4 is expected to expand at a 9.7% CAGR between 2026-2031.

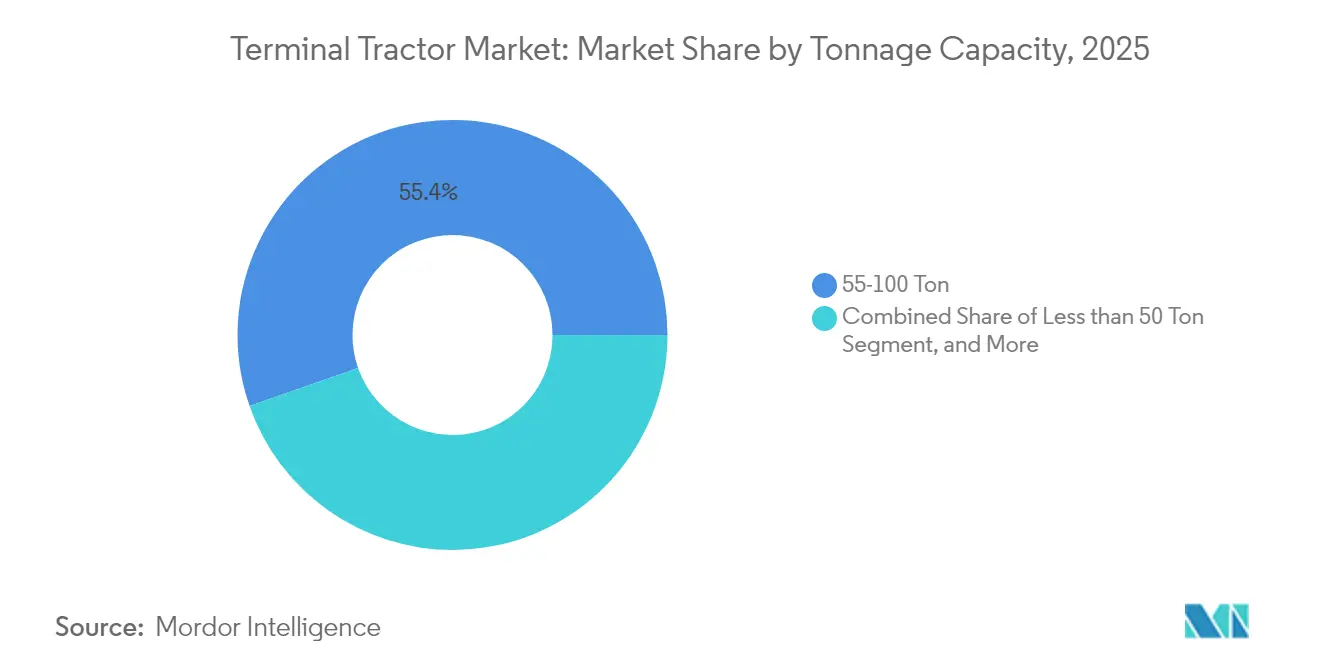

- By tonnage capacity, 50-100 ton models accounted for 55.35% of the terminal tractor market size in 2025; units rated above 100 ton forecast a 7.3% CAGR.

- By end-use industry, retail & e-commerce 3PLs commanded a 31.95% of the terminal tractor market share in 2025, whereas automotive OEM yards logged the top growth at an 8.5% CAGR.

- By geography, North America delivered 36.30% of the terminal tractor market revenue in 2025; Asia-Pacific is poised for a 6.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Terminal Tractor Market Trends and Insights

Drivers Impact Analysis*

| Driver | Percentage Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent IMO & CARB Emission Mandates Catalyzing Electric Yard Truck Adoption | +1.5% | North America, Europe | Short term (≤ 2 years) |

| E-Commerce-Driven Trailer Turnover Escalating Terminal Tractor Cycles | +1.2% | North America, Europe | Medium term (2-4 years) |

| Green Hydrogen Pilots In EU Ports Enabling Fuel-Cell Terminal Tractors | +0.7% | Europe, spillover to North America | Long term (≥ 4 years) |

| Rise Of Rental-Model Warehousing In India Accelerating Short-Tenure Tractor Leasing | +0.6% | Asia-Pacific, particularly India | Medium term (2-4 years) |

| 4x4 Drive Demand From Intermodal Rail Yards In Nordics Boosting Premium Tractor Sales | +0.4% | Nordics, North America | Medium term (2-4 years) |

| AI-Enabled Fleet Optimization Software Increasing Utilization Rates & Replacement Cycles | +0.3% | Global, with early adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce-Driven Trailer Turnover Escalating Terminal Tractor Cycles

Surging online retail volumes push North American mega-fulfillment centers to process trailer moves at 2.77 times the pace seen in legacy retail hubs, a shift that elevates duty cycles and hastens fleet replacement. Electric models gain favor because their maintenance expense runs 60-75% lower than diesel equivalents [1] "Top OEM Manufacturing Electric Yard Trucks in the US", YMX Logistics, ymxlogistics.com, letting operators sustain round-the-clock shifts without lengthy service breaks. Fleet managers now specify high-durability frames, reinforced driveline components, and smart yard management software to handle 24/7 traffic peaks. The resulting jump in utilization makes premium-priced units financially viable, thereby reinforcing the ongoing migration toward alternative propulsion in the terminal tractor market. Comparable patterns emerge in European postal distribution hubs, signaling a broadening geographic ripple.

Stringent IMO & CARB Emission Mandates Catalyzing Electric Yard Truck Adoption

California’s 2025 Mobile Source Strategy enforces a 90% cut in NOx and an 80% cut in diesel particulate matter from cargo-handling equipment by 2026. Similar targets appear in the IMO 2023 decarbonization strategy, pressuring global ports to overhaul diesel fleets. With compliance deadlines looming, electric terminal tractors offer a near-term pathway because they require less infrastructural overhaul than quay cranes or shore-power retrofits. The Port of Long Beach integrates zero-emission yard trucks while still processing record container volumes, demonstrating feasibility under high-throughput conditions [2] "State of Ports & Ocean Carriers", Food Logistics, foodlogistics.com. These regulations compress decision windows, pushing procurement teams to lock in battery-electric models despite higher purchase prices, driving measurable expansion across the terminal tractor market.

Green Hydrogen Pilots In EU Ports Enabling Fuel-Cell Terminal Tractors

Northern European ports trial hydrogen fuel-cell yard trucks to overcome battery range limitations in cold climates where temperatures sink below freezing. Fast H₂ top-off, under 10 minutes, suits high-utilization shuttles that cannot spare 90-minute fast-charge downtimes. As the production capacity of hydrogen within the European Union continues to expand, terminal operators are increasingly adopting mixed-fleet strategies. These strategies combine the use of batteries for standard daytime operations with fuel cells designed for prolonged, heavy-duty cycles. This approach serves as a prudent hedge against potential infrastructure risks and the fluctuations associated with battery commodity markets, ensuring a more resilient and adaptable operational framework.

Rise Of Rental-Model Warehousing In India Accelerating Short-Tenure Tractor Leasing

India's warehousing sector is transitioning to a rental-model approach, fueled by increasing demand for efficient logistics and storage solutions across retail, e-commerce, and agriculture. This model emphasizes flexibility and cost efficiency, with short-term tractor leasing gaining traction among farmers seeking productivity without long-term obligations.

By offering access to modern machinery during peak seasons or for specific projects, this approach minimizes capital expenditure and boosts adaptability. The synergy between rental warehousing and tractor leasing enhances logistics, streamlining supply chain management and enabling businesses to adapt swiftly to market dynamics. This shift in India's rental-model warehousing is transforming short-term tractor leasing, empowering businesses with greater flexibility and operational efficiency in a competitive market.

Restraints Impact Analysis*

| Restraint | Percentage Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front CAPEX Of BEV/FC Terminal Tractors Vs. Diesel Equivalents | -0.9% | Global, pronounced in price-sensitive markets | Short term (≤ 2 years) |

| Fragmented Power Infrastructure At Brownfield Ports Delaying Fast-Charge Roll-Out | -0.6% | Global, acute in Asia-Pacific | Medium term (2-4 years) |

| Volatile Battery-Grade Nickel & Lithium Prices Inflating TCO Forecasts | -0.5% | Global, with the highest impact in regions without domestic battery production | Short term (≤ 2 years) |

| Limited Skilled Technicians For Autonomous Tractor Maintenance In Emerging Markets | -0.4% | Asia-Pacific, Africa, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High up-front CAPEX of BEV/FC terminal tractors vs. diesel equivalents

Battery-electric yard trucks list between USD 275,000-350,000, nearly triple a diesel unit’s USD 100,000-125,000 cost, which stretches payback beyond five years in moderate-utilization fleets lacking incentives. Hydrogen fuel-cell models face an even steeper hurdle as bespoke components keep sticker prices 250-300% higher. Smaller logistics providers struggle to secure financing that matches 3-5 year replacement cycles [3] "Terminal Tractor Report", North American Council for Freight Efficiency, nacfe.org, especially in countries without subsidy schemes. Although total cost of ownership trends now tilt in favor of electric when annual hours exceed 5,000, upfront sticker shock continues to trim addressable demand, tempering overall progress in the terminal tractor market.

Fragmented power infrastructure at brownfield ports delaying fast-charge roll-out

Legacy ports often feature electrical systems sized only for lighting and reefer plugs, falling short of the multi-megawatt supply needed for dozens of simultaneous 175 kW chargers. Ownership fragmentation complicates upgrades because utilities, port authorities, and private terminal operators each control separate feeders. The Cleveland-Cuyahoga County Port Authority’s net-zero plan illustrates that reinforcing feeders can triple project budgets and add two-year lead times. Until infrastructure gaps close, fleets must oversize equipment pools to compensate for charge dwell, which raises capital costs and slows adoption of battery-electric models, particularly at Asia-Pacific brownfield sites where throughput expansion already strains grids.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Electrification Accelerates Despite Diesel Dominance

Diesel technology accounted for a 62.65% terminal tractor market share in 2025, anchored by its extensive installed base and lower acquisition cost. Electric models, however, are projected to post an 17.6% CAGR from 2026-2031 as regulatory pressure stiffens and battery pricing eases. Early adopters in California, British Columbia, and Guangdong report maintenance savings that counterbalance higher purchase prices within four operating years. Hybrid and CNG/LNG variants fill specific compliance windows where fuel availability or duty cycle characteristics favor flexible propulsion. Hydrogen fuel-cell prototypes, though representing low single-digit volumes today, attract EU funding as range and cold-weather resilience gain strategic weight. Across the terminal tractor market, propulsion choice is increasingly bound to port-specific carbon targets, electricity tariffs, and incentive stacks, reinforcing a regionally divergent adoption curve.

Electric penetration also influences parts supply and resale dynamics. OEMs bundle battery warranties, telematics, and preventive maintenance contracts to de-risk lifetime costs for buyers. As diesel emission systems grow more complex, downtime linked to after-treatment adds operating risk that further tips preference toward battery-electric. The coming half-decade therefore signals a progressive shift where diesel’s share declines but remains material in emerging economies without robust grid capacity, keeping the global fleet in a dual-propulsion state through at least 2030.

By Vehicle Type: Autonomous Technology Disrupts Traditional Operations

Manual tractors retained 74.55% of the terminal tractor market share in 2025 because many yards still demand human judgment in mixed-traffic scenarios. Yet autonomous units, rising at a 21.2% CAGR, re-shape operational economics by cutting labor costs and extending duty hours. Controlled environments, container stack shuttles, automotive marshalling yards, and high-security air cargo aprons offer ideal testbeds where geo-fencing ensures predictable routes. The terminal tractor market now hosts new entrants from robotics and AI, including Forterra and FERNRIDE, who supply drive-by-wire kits and remote-teleoperation platforms that retrofit OEM chassis. Traditional manufacturers answer with factory-ready autonomy interfaces, shortening integration cycles.

Roll-out speed links tightly to labor availability and local regulatory clarity. European Machinery Directive certification, achieved by FERNRIDE in 2025, provides a harmonized framework likely to accelerate deployments across EU member states. North American OEMs focus on modular upgrades, allowing fleets to shift between supervised and unsupervised modes. As AI perception stacks mature, cost curves bend downward, enabling smaller terminals to adopt autonomy sooner than previously expected. That trajectory cements self-driving functionality as a mainstream spec line-item by the late 2020s.

By Drive Configuration: Application-Specific Requirements Drive Diversification

The 4x2 layout held 64.10% of the terminal tractor market share in 2025, favored for its lower cost and adequate traction on paved yards. Growth momentum, however, tilts toward 6x4 variants posting a 9.7% CAGR because ultra-large container vessels push container weights upward, necessitating higher axle loads. In ice-prone Nordic rail yards, 4x4 all-wheel-drive units fill a reliability niche where downtime carries severe penalty fees. OEMs such as Autocar and Dana refine driveline torque management and corrosion resistance for these extreme environments, converting a once-minor configuration into a lucrative premium segment within the terminal tractor market.

Drive-train choice increasingly maps to specific throughput and terrain profiles rather than operator size. Ports facing land-side gradients or loose gravel adopt 6x4 to safeguard tire wear and maintain cycle time. Meanwhile, emerging inland logistics parks in India and Brazil opt for standard 4x2 to minimize capital outlay. The net outcome is a broader catalog of chassis SKUs, empowering fleets to optimize asset utilization rather than over-specifying a single universal model.

By Tonnage Capacity: Mega-Ships Drive Demand for Higher Capacity

Units rated 50-100 tons represented 55.35% of the terminal tractor market in 2025, balancing versatility and fuel economy for most shipping containers. Vessels exceeding 20,000 TEU push some yards toward >100 ton tractors, driving a 7.3% CAGR for that class through 2031. Greater lift capability allows dual-container shuttle moves, trimming round-trip intervals when berth windows narrow. Manufacturers must contend with longer wheelbases and heightened structural stress, particularly when integrating heavy battery packs in electric variants. Conversely, sub-50-ton models serve airports and parcel hubs where tight turning radii matter more than brute strength.

Up-rating capacity has design ramifications beyond metallurgy. Higher-ton tractors increasingly adopt advanced braking systems, regenerative energy capture, and active stability control. These features become new differentiation levers as the terminal tractor market evolves from basic mechanical workhorses to digitally managed assets.

By End-Use Industry: Retail & E-commerce Lead Transformation

Retail and e-commerce 3PLs command 31.95% of the terminal tractor market share in 2025 because their fulfillment models rely on dense trailer marshalling. The automotive sector, forecast to grow 8.5% CAGR, now modernizes yard logistics to orchestrate just-in-time sequencing for component deliveries. Food & beverage producers hold a stable share due to frequent dock rotation in temperature-controlled networks. Heavy industrial parcels, from steel coils to chemical totes, demand high-ton tractors equipped with explosion-proof lighting or extended-reach fifth wheels.

Digital integration distinguishes industry verticals. E-commerce operators equip tractors with RFID readers and slot-level GPS to sync gate activity with order management systems. Auto OEMs, in contrast, specify tugger robots and quasi-autonomous convoy modes to match assembly takt times. Such divergent specifications compel OEMs to modularize wiring harnesses, control architectures, and safety certifications, reinforcing customization as a core competency in the terminal tractor market.

Geography Analysis

North America represented 36.30% of the terminal tractor market revenue in 2025, anchored by extensive Gulf and West Coast port capacity and aggressive zero-emission rules. California drives early adoption, but Canada scales procurement as Prince Rupert and Vancouver deepen terminals to absorb Pacific trade diversions. The region demonstrates rapid software uptake as Aurora Innovation’s highway platooning algorithms cross-pollinate into yard automation platforms, foreshadowing a broader autonomy wave. Electricity pricing variability nonetheless affects rollout speed; utilities in Texas and Georgia deploy preferential industrial tariffs to lure battery-electric conversions.

Asia-Pacific logs the fastest regional expansion at a 6.9% CAGR through 2031, buoyed by Chinese smart-port funding and India’s GatiShakti infrastructure drive. Guangzhou Port recently expanded its intelligent guided vehicle fleet to 158 units, illustrating state-backed scale on automation. Japan and South Korea mature toward hybrid electrification models to offset high electricity tariffs, while Southeast Asian corridors—Thailand’s Eastern Economic Corridor and Vietnam’s Cai Mep cluster—order tractors primarily for new-build terminals rather than retrofit programs, giving OEMs greenfield specification flexibility.

Europe sustains high adoption of low-carbon propulsion through harmonized EU Green Deal incentives, making it a launchpad for fuel-cell pilots at Wilhelmshaven and Rotterdam. Nordic countries pave the road for all-weather 4x4 electric fleets, leveraging hydropower-sourced electricity to claim lifecycle emission savings. Central and Eastern European hubs, led by Poland’s Gdansk, invest in redundancy to capture Baltic trans-shipment traffic, expanding addressable demand. Elsewhere, the Middle East and Africa witness stepped-up investment in Saudi Arabia’s Jeddah port and South Africa’s Durban expansion, revealing fresh opportunities as these hubs chase trans-shipment share from capacity-constrained Suez routes across the terminal tractor market.

Competitive Landscape

The terminal tractor market is dominated by several key players such as Kalmar (Cargotec), Terberg Group, Konecranes, TICO, and Sany. Market leaders leverage international service networks and complementary handling equipment lines to lock in bundled contracts. Kalmar capitalizes on its third-generation electric platform launched in 2025, integrating modular battery architecture that scales from 100 kWh to 266 kWh, thereby accommodating duty cycles spanning heavy container yards to parcel depots. Terberg extends reach through regional assemblers and a burgeoning retrofit parts business that converts legacy diesels to battery-electric.

Partnerships reshape competitive geography. Konecranes’ distribution pact with Terberg Tractors Belgium opens cross-selling of lift trucks and yard tractors, while Forterra and Kalmar fuse autonomy software with OEM chassis. FERNRIDE’s human-assisted autonomy, already certified to the European Machinery Directive, positions it as the interface between manual fleets and full self-driving regimes. Chinese challengers XCMG and Geely’s commercial vehicle arm pursue aggressive overseas expansion, buoyed by domestic economies of scale that compress battery costs. In response, Western incumbents accelerate subscription-based telematics and predictive maintenance, crafting service annuities that buffer hardware margin erosion.

Disruptive white spaces focus on data. OEMs embed sensor suites that feed cloud dashboards, enabling benchmark comparisons of brake wear, battery degradation, and idle ratio against anonymized fleet cohorts. Operators monetize insights by reducing spare-part inventories and optimizing charging schedules, locking in brand loyalty even as chassis commoditization looms. Consequently, sustainable competitive advantage migrates from mechanical differentiation to integrated hardware-software ecosystems, mirroring broader trends within the terminal tractor market.

Terminal Tractor Industry Leaders

-

Terberg Group BV

-

Kalmar (Cargotec Corp.)

-

Hyster-Yale Group Inc.

-

Konecranes Inc.

-

TICO Tractors

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Electrification programs at large ports and terminals are creating whitespace for OEMs and integrators that can deliver vehicles alongside infrastructure-ready packages. APM Terminals Maasvlakte II expanded its automated electric terminal tractor fleet with additional units in April 2026, moving toward a planned total of 30 through cooperation with Embotech and Terberg. This points to demand for automation-ready, zero-emission yard operations that can be deployed in live terminal environments.

In Europe, 2026 product activity is also broadening the standardized electric platforms available to ports, rail yards, and large distribution hubs. Kalmar brought the fully electric TT7 to European markets, while Terberg unveiled next-generation YT201EV and upgraded YT203EV models. Over the near term, the clearest adoption opportunity is reducing friction to take-up, since high upfront purchase prices and fragmented brownfield power capacity keep many fleets in a dual-propulsion operating pattern. That opens room for bundled charging solutions, staged fleet conversion plans, and retrofit pathways for existing diesel tractors where terminal duty cycles and asset age support mid-life upgrades. Tender demand is also shifting toward higher-utilization use cases and premium configurations, such as 6x4 and above 100-ton requirements, where electrified drivetrains, telematics, and predictive maintenance contracts help monetize uptime. OEMs with service networks and software partners are in a better position to win as autonomous and supervised-autonomy deployments move beyond pilots.

Recent Industry Developments

- May 2026: Terberg Special Vehicles launched next-generation YT201EV and enhanced YT203EV electric terminal tractor models for global markets. The updates broaden the OEM electric portfolio for multi-shift terminal and yard applications and support fleet standardization as buyers move from pilots to repeatable procurement.

- May 2026: Terberg Special Vehicles received an order to supply 106 electric terminal tractors to Marsa Maroc for the Nador West Med terminal. The contract indicates scaling demand for zero-emission terminal equipment in Africa-linked gateway infrastructure and strengthens Terberg's position in large fleet conversions.

- March 2024: Forterra and Kalmar partnered to co-develop a terminal tractor designed for automation-ready operation using Forterra's AutoDrive system. The collaboration reinforces the shift toward OEM-chassis platforms built to integrate autonomy stacks, which can shorten deployment cycles for terminals pursuing higher yard productivity.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers terminal tractors used for short-distance movement of semi-trailers inside yards, ports, intermodal terminals, and logistics hubs, where the main task is trailer spotting and yard shuttling.

Scope exclusions: We exclude on-road tractor trucks, standard heavy-duty trucks, and general forklifts or reach stackers that are not designed as yard spotters.

Segmentation Overview

-

By Propulsion Type

- Diesel

- Hybrid

- Electric (BEV)

- CNG / LNG

- Hydrogen Fuel-Cell

-

By Vehicle Type

- Manual

- Semi-Automated

- Fully Autonomous

-

By Drive Configuration

- 4x2

- 4x4

- 6x4

-

By Tonnage Capacity

- Less than 50 Ton

- 50-100 Ton

- Greater than 100 Ton

-

By End-Use Industry

- Retail & E-commerce 3PL

- Food & Beverages

- Heavy Industry & Manufacturing

- Automotive OEM Yards

- Marine Ports Industry

- Oil and Gas Industry

- Logistics Industry

- Others (Rail Logistics Yards, etc.)

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- India

- Japan

- South Korea

- Indonesia

- Vietnam

- Philippines

- Australia

- New Zealand

- Rest of Asia-Pacific

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Nigeria

- Egypt

- Rest of Middle East and Africa

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us set the boundary of what gets counted and establish base demand signals for yards and terminals. We relied on public, non-paywalled sources such as port authority throughput releases and annual reports, UNCTAD port and trade publications, U.S. Bureau of Transportation Statistics datasets, Eurostat freight transport series, and International Energy Agency notes on transport electrification trends. These sources were used to understand how cargo flows, intermodal activity, and yard operations are changing over time.

We also reviewed company filings, product catalogs, investor presentations, and reputable press coverage to map typical configurations and buying patterns across diesel, hybrid, and electric units. Where available, paid subscriptions for company financials and news, patent databases, and shipment-level import and export data were used to cross-check supplier footprints and equipment movement signals without depending on any single disclosure. The desk sources listed here are illustrative, and many other references were used to clarify, validate, and complete the data trail.

Primary Interviews and Surveys

Primary work was used to confirm what desk signals cannot fully explain, especially real-world replacement cycles, electric adoption pace, and typical pricing by duty class. We spoke with a mix of OEM-side roles, terminal and yard operations leaders, dealer and service stakeholders, and fleet procurement teams across APAC, EMEA, and the Americas, so assumptions could be checked against practical buying and usage behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 16% | APAC: 43% |

| Mid tier: 46% | Functional/Unit leaders: 34% | EMEA: 33% |

| Smaller Players: 21% | Managers: 50% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs the addressable demand pool from terminal activity and fleet renewal behavior, then converts that pool into unit demand and value. In practice, throughput growth, intermodal expansion, and yard automation programs shape how many tractors are required, followed by replacement timing and utilization assumptions that are refined through interviews.

To keep the model grounded, we use a small set of inputs that typically move the total most, such as terminal and inland depot throughput trends, electrification share by yard duty cycle, average service life and refresh cadence, mix by capacity bands (for example, 50 to 100 ton and above 100 ton), and the shift toward semi-automated or autonomous yard moves. Pricing is handled through a working ASP range by powertrain and configuration, then translated into USD with consistent currency timing for the year being measured. Results are corroborated with selective bottom-up approximations, including sampled ASP times estimated unit demand by region and channel checks on order flow. Where direct disclosures are thin, gaps are handled by proxying from comparable terminal equipment intensity.

For forecasting, scenario analysis is used so the outlook can reflect differences in port capex cycles, emission rules that push electric adoption, and charging or hydrogen infrastructure readiness. Assumptions are then adjusted after expert feedback, so the final curve stays aligned with what buyers and suppliers expect in near-term bids and fleet plans.

Data Validation & Update Cycle

Validation is done through several checks before sign-off, with the goal of ensuring the market total matches reality-based signals. Analysts compare outputs against independent indicators such as port and intermodal activity trends, observed fleet replacement behavior, and pricing ranges heard in interviews, then investigate outliers that do not fit the operating logic. When a variance is found, the assumptions are traced back to the driver, and follow-up calls are triggered to re-check the point with additional respondents.

A multi-step internal review is used so totals, growth rates, and regional splits remain consistent with the evidence trail and with related equipment markets. Reports are refreshed annually, with interim updates when material events occur, and a final pre-delivery pass is completed so clients receive the latest updated view.

Mordor Intelligence's Terminal Tractor Market Sizing Compared With Other Published Estimates

Published market sizes for terminal tractors often do not match because the counting rules are not the same, even when the topic name looks identical. Differences usually come from what equipment types are included, which end-use yards are counted, and how pricing is treated for electric and higher-capacity units.

Order activity signals from ports and intermodal yards, together with interview-validated replacement cycles and observed ASP ranges, are the checks that keep Mordor Intelligence tied to terminal-tractor-only demand, instead of blending in adjacent yard equipment or on-road tractors. Other estimates can move up if they include RoRo tractors or broader terminal equipment, or they can move down if they only cover seaports and skip inland depots, rail yards, and warehouse terminals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.41 B (2026) | |

| Trade Journal A | USD 1.40 B (2024) | Uses an earlier base year and relies heavily on high-level trade and logistics growth assumptions, with limited adjustment for electric ASP differences and capacity-mix shifts. |

| Industry Publication B | USD 4.30 B (2024) | Combines terminal tractors with RoRo tractors and related yard-use tractors, which expands the scope beyond trailer-spotting units used in ports and intermodal yards. |

The comparison shows that scope boundaries and year selection explain most of the spread, followed by how pricing and electrification are modeled. By keeping the demand pool anchored to yard-spotter use cases and then checking totals against practical fleet and price signals, the resulting number stays traceable to clear steps that can be repeated each update cycle.

Key Questions Answered in the Report

What is the current value of the terminal tractor market?

The terminal tractor market size is USD 1.41 billion in 2026.

How fast will the market grow over the next five years?

Global revenue is projected to expand at a 4.7% CAGR, reaching USD 1.78 billion by 2031.

Which propulsion type is growing the fastest?

Battery-electric models record the highest growth, advancing at an 17.6% CAGR due to regulatory mandates and lower maintenance costs.

Which region offers the strongest growth outlook?

Asia-Pacific leads with a 6.9% CAGR through 2031, propelled by Chinese port automation and Indian infrastructure programs.

Page last updated on: