Taiwan Defense Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

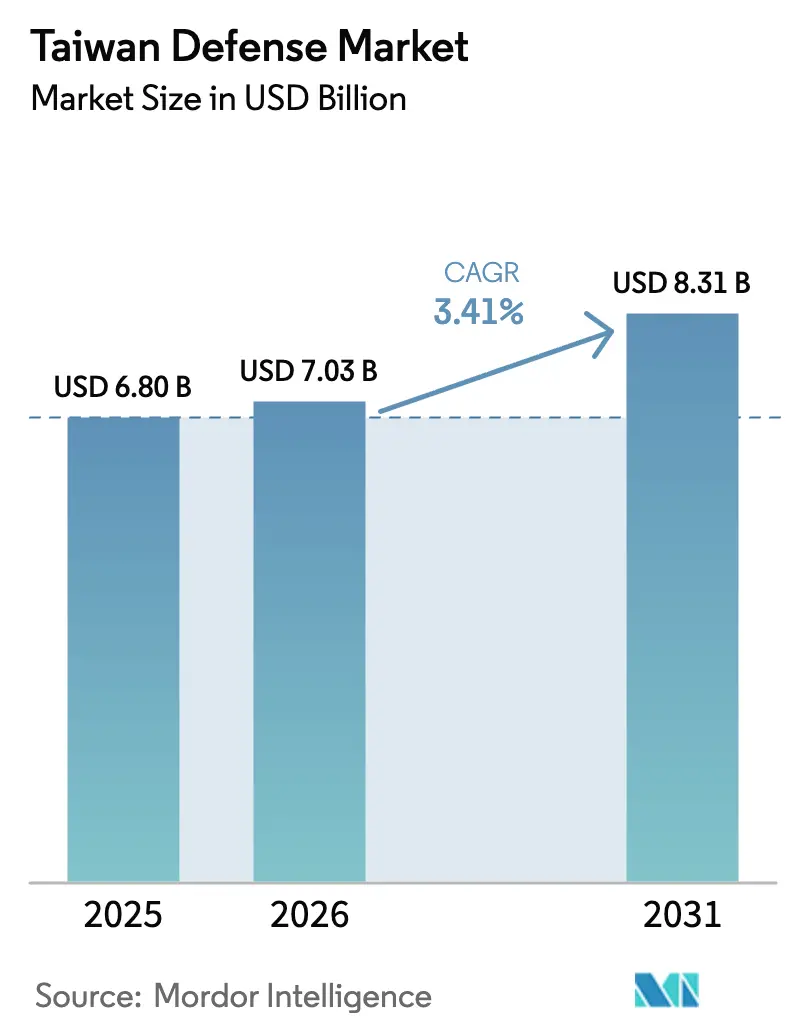

| Base Year Market Size (2025) | USD 6.80 Billion |

| Market Size (2026) | USD 7.03 Billion |

| Market Size (2031) | USD 8.31 Billion |

| Growth Rate (2026 - 2031) | 3.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Taiwan Defense Market Analysis by Mordor Intelligence

The Taiwan defense market size in 2026 is estimated at USD 7.03 billion, growing from 2025 value of USD 6.80 billion with 2031 projections showing USD 8.31 billion, growing at 3.41% CAGR over 2026-2031. Spending growth is paced yet persistent, driven by cross-strait threat escalation, a record TWD 647 billion (USD 20.2 billion) defense budget allocation equal to 2.45% of GDP, and the legislature’s continued commitment—despite periodic cuts—to modernizing forces.[1]Source: Nikkei Asia desk, “Taiwan allots record defense budget to meet China threat,” asia.nikkei.com Platform demand centers on fighter upgrades, intelligence networks, and asymmetric assets such as long-range precision fires and underwater systems. Foreign equipment remains dominant, but rising local production, especially in missiles and submarines, gradually reduces single-source dependence. Technology-transfer frameworks, industrial co-production, and cooperative research on unmanned platforms are emerging as core opportunity areas for suppliers that can align with export-control rules and Taiwan’s “porcupine strategy.”

Key Report Takeaways

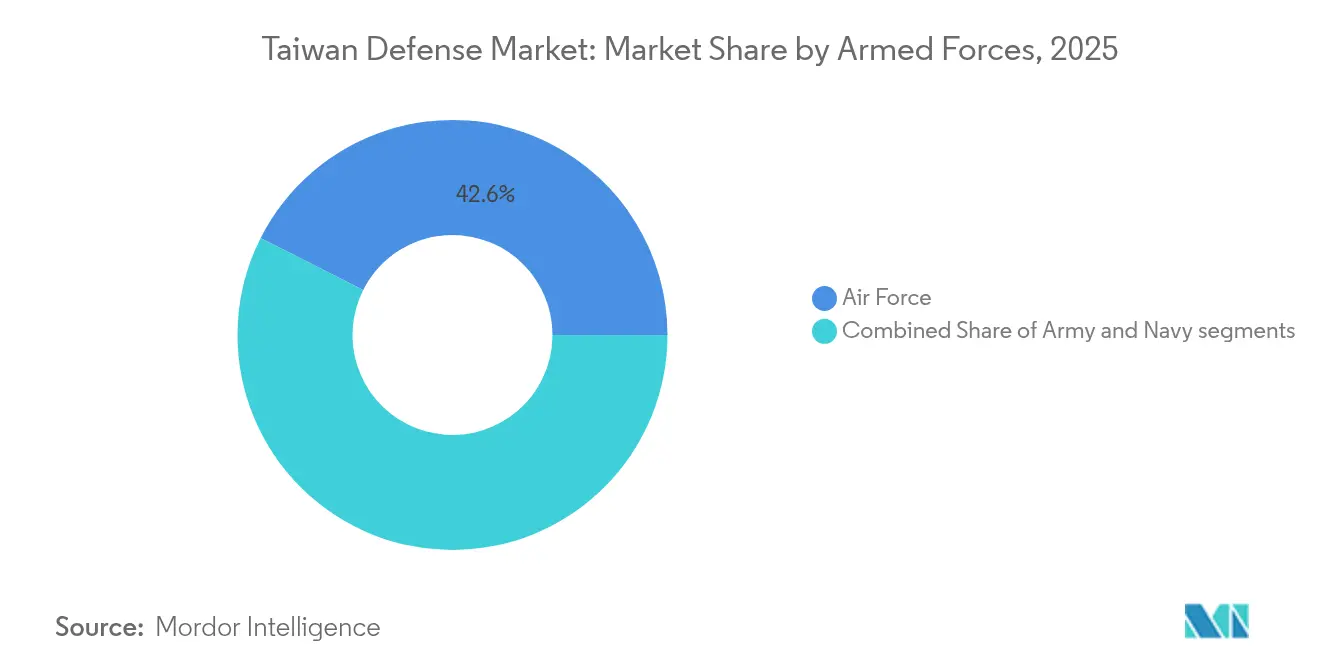

- By armed forces, the air force led with 42.55% of the Taiwanese defense market share in 2025, while the navy is projected to grow at a 4.12% CAGR to 2031.

- By type, C4ISR and electronic warfare systems accounted for a 23.44% share of the Taiwanese defense market in 2025; unmanned systems are forecasted to expand at a 6.42% CAGR.

- By procurement nature, foreign purchases represented 64.98% share of the Taiwanese defense market size in 2025, whereas indigenous production is rising at a 4.57% CAGR.

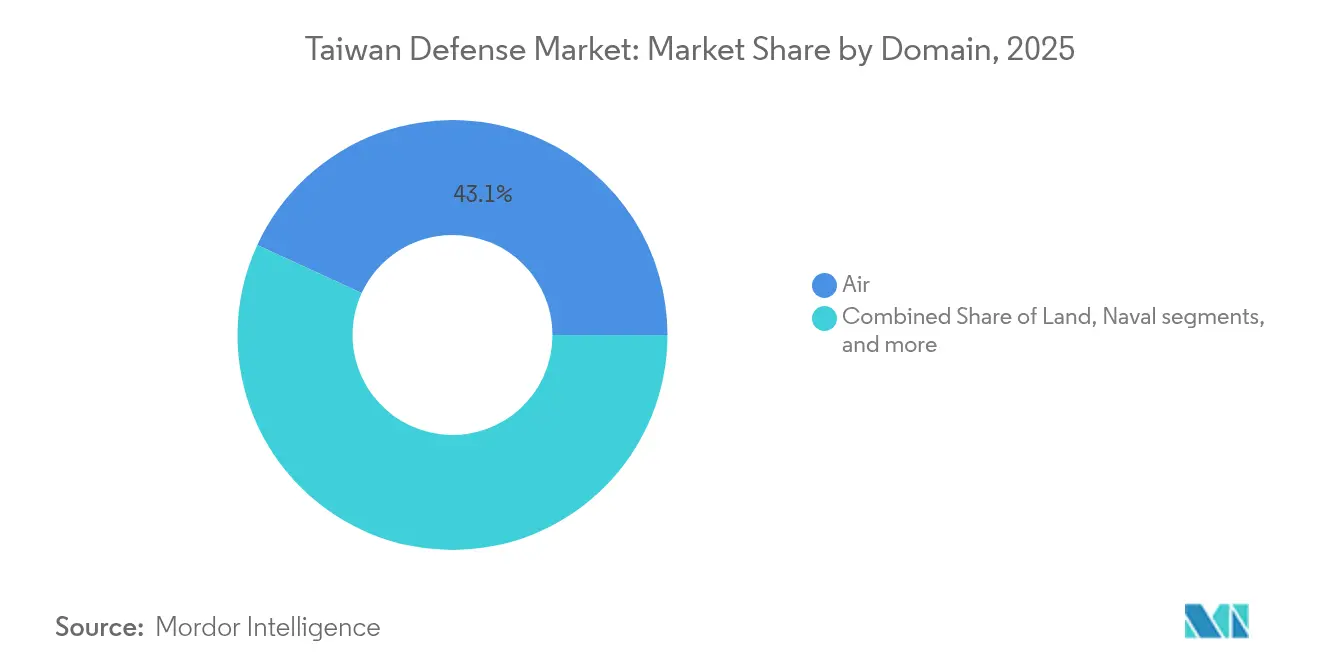

- By domain, the air segment held 43.12% of Taiwanese defense market share in 2025; space assets are advancing at a 6.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Taiwan Defense Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating PLA incursions over Taiwan Strait | +1.2% | Taiwan; spillover to Japan and the Philippines | Short term (≤ 2 years) |

| US-Taiwan Foreign Military Sales (FMS) pipeline expansion | +0.8% | Taiwan; US defense industrial base | Medium term (2-4 years) |

| Indigenous Defense Submarine (IDS) program milestones | +0.4% | Taiwan; partners in the UK and Australia | Long term (≥ 4 years) |

| Whole-of-society “Porcupine Strategy” implementation | +0.6% | Taiwan | Medium term (2-4 years) |

| Dual-use semiconductor R&D spin-offs for C4ISR | +0.3% | Taiwan; global chip supply chain | Long term (≥ 4 years) |

| Private UAV start-ups filling tactical ISR gaps | +0.2% | Taiwan; regional drone markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating PLA incursions over the Taiwan Strait

Chinese aircraft and vessels now appear in the Taiwan Strait on an almost daily basis, compressing warning times for Taipei’s joint-force commands and compelling planners to adopt a permanent high-alert posture. To keep pace, the Ministry of National Defense moved Army Tactical Missile Systems, High-Mobility Artillery Rocket System (HMARS) batteries, and man-portable air-defense launchers to forward positions that can respond within minutes. The operational surge also drove a revision of compulsory service from four months to one year, lifting the 2025 conscript intake to 9,839-41% higher than the 2024 cohort.[2]Source: Taipei Times reporters, “Military tracks record PLA incursions,” taipeitimes.com Budget reallocations favor quick-reaction coastal interceptors, point-defense radars, and personal protection equipment that supports small, dispersed units able to survive the opening hours of a cross-strait contingency. Procurement officials shortened contracting cycles by granting emergency authority to the Armaments Bureau, which can now place rapid-award orders for expendable drones, loitering munitions, and battlefield communications sets without the lengthy public-tender process. These structural changes signal an institutional shift toward asymmetric resilience rather than platform mass, anchoring the near-term expansion of the Taiwan defense market and accelerating demand for technologies that confer tactical agility.

US-Taiwan Foreign Military Sales pipeline expansion

The United States remains Taiwan’s principal security partner, and combined FMS plus direct commercial transactions reached USD 1.75 billion in 2024. Authorizations for a further USD 300 million in Altius-600M unmanned systems and technical talks on Link-22 network roll-out through 2026 confirm sustained pipeline momentum. Each platform purchase automatically spawns follow-on contracts for depot support, spare parts, training simulators, and software upgrades, lifting total program value well beyond the headline figure. American primes have responded by stationing resident technical teams in Taichung and Kaohsiung, streamlining field-level troubleshooting and shortening downtime for critical assets such as F-16V fighters and AN/TPY-2 radars. Taiwan’s firms benefit in parallel: co-production clauses written into recent letters of offer and acceptance allow local suppliers to machine structural components, assemble sub-modules, and certify software to US cyber-security standards. As the backlog grows, the Taiwan defense market witnesses a gradual shift from a straightforward buyer-seller relationship toward a hybrid model that blends the import of advanced subsystems with indigenous final-assembly and sustainment, sharpening domestic engineering skills, and anchoring a robust supply ecosystem.

Indigenous Defense Submarine program milestones

Completing harbor trials for the prototype Hai Kun submarine marked the most tangible proof that Taiwan can master complex undersea technologies without relying on hull imports. The vessel is scheduled for handover in November 2025 and sits at the center of an NT 284 billion blueprint for seven follow-on boats delivered over 15 years. The program has multiplied CSBC Corporation’s monthly revenue by eight and created a steady order book for more than 100 small-and medium-sized enterprises that machine pressure hull rings, fabricate lithium-ion battery casings, and integrate combat-management software. Domestic sonar laboratories have moved from prototype arrays to low-rate production, laying the foundation for a national maritime-electronic cluster. In parallel, the navy committed to indigenously produced heavyweight torpedoes, ensuring that weapons, sensors, and hulls mature as a coherent family. Every one-percent rise in the submarine program’s local-content target displaces millions of dollars that would otherwise flow abroad, underscoring why policymakers view the project as a bellwether for Taiwan’s broader push toward defense autonomy and why it exerts an outsized pull on the Taiwan defense market.

Whole-of-society “porcupine strategy” implementation

Taipei’s asymmetric doctrine envisages a dense web of cost-effective, mobile, and easily hidden assets that complicates any invasion plan. In 2025, the Executive Yuan approved USD 1.35 billion to ramp monthly drone capacity to 15,000 units by 2028 and sanctioned the Thunder Tiger SeaShark 800 unmanned surface vessel, which can carry a 1,200 kg explosive package over 500 km. Funds cover palletized air-defense missiles transportable on commercial trucks, lightweight anti-armor rounds issued at squad level, and encrypted mesh radios that link reservists to active formations. Civic organizations receive grants to convert underground parking lots into emergency ammunition caches, while universities embed cyber-resilience training in engineering curricula. The outcome is a distributed network of lethal and non-lethal capabilities that magnifies the defender’s cost-imposition potential, directly influencing procurement patterns by channeling demand toward compact launch tubes, commercial-off-the-shelf sensors, and software-defined radios. Suppliers able to harden commercial technology for military environments find immediate openings, further enlarging the Taiwan defense market as civilian sectors merge with territorial-defense requirements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legislative Yuan budget-cap debates | -0.7% | Taiwan domestic politics | Short term (≤ 2 years) |

| ITAR and export-licence restrictions on critical tech | -0.4% | US-Taiwan defense trade | Medium term (2-4 years) |

| Conscript force downsizing amid ageing population | -0.3% | Taiwan, Regional demographic trends | Long term (≥ 4 years) |

| Industrial talent drain to commercial chip sector | -0.2% | Taiwan, Global semiconductor competition | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Legislative Yuan budget-cap debates

Although central government defense outlays have climbed for seven straight years, opposing blocs in the Legislative Yuan imposed a 6.6% haircut on the 2025 appropriation, holding back NT 63.6 billion and freezing half of the NT 2 billion earmarked for submarine follow-on construction. Procurement officers must now juggle milestone payments, delaying long-lead material orders, and stretching suppliers’ cash-flow forecasts. The freeze coincided with proposals to lift basic military pay to NT 30,000 per month; if enacted, personnel costs will consume a larger slice of available funds, potentially squeezing modernization accounts. Project managers respond by breaking large contracts into annual tranches that fit within narrower ceilings, but that tactic inflates administrative overhead and can deter foreign vendors wary of funding gaps. The recurrent debate injects uncertainty into the Taiwan defense market, reducing the predictability that complex programs must lock in multiyear pricing.

ITAR and export-license restrictions on critical technology

Washington’s proposed amendments to the International Traffic in Arms Regulations expand the “military end user” definition and oblige contractors to pursue fresh approval for subsystem-level changes, lengthening an already protracted compliance cycle. Therefore, Taiwan’s USD 19 billion order backlog is exposed to schedule creep as US primes queue for commodity-jurisdiction rulings and commodity classification requests.[3]Source: Bradley Bowman, “US delivery delays hamper Taiwan,” warontherocks.com Delays bite hardest in C4ISR programs that depend on commercial microelectronics, which are no longer classified as purely dual-use once integrated into secure radios. To mitigate, Taiwan holds larger buffer stocks of spares and pursues parallel domestic development where feasible, though the latter sometimes lacks the performance envelope of US originals. This regulatory drag tempers the 3.46% compound growth forecast, shaving an estimated 0.4 percentage points off the Taiwan defense market CAGR during the 2025–2030 window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Armed Forces: Air Force dominance amid naval acceleration

The Air Force’s 42.55% slice of Taiwan's defense market share in 2025 is anchored by the ongoing delivery of 66 F-16V Block 70 fighters and negotiations for E-2D early-warning aircraft that promise enhanced detection of stealth threats. Yet the Navy’s 4.12% CAGR signals a relative tilt toward undersea and littoral capabilities, led by submarine construction and compact frigates optimized for strait patrols.

The Army maintains robust funding for 108 M1A2T tanks and a fully operational HIMARS regiment capable of cross-strait precision strikes. Integration exercises conducted in 2025 illustrate a joint doctrine where air assets furnish targeting data, naval units deny chokepoints, and ground forces deliver saturation fires. This paints a composite demand profile that sustains both traditional platforms and nimble missile batteries across the Taiwan defense market.

By Type: C4ISR leadership challenged by unmanned-systems surge

C4ISR and electronic warfare assets captured 23.44% of Taiwan defense market size in 2025, propelled by the TWD 7.81 billion Field Information Communications System and network-gateway upgrades to Link-16 and planned Link-22 interoperability. Nevertheless, unmanned systems expanded at a 6.42% CAGR as government financing and relaxed procurement rules unlock scale production of air, surface, and subsurface drones.

Missile-manufacturing throughput topped 1,000 rounds in 2024, while Clouded Leopard II armor achieved 89% domestic content, underscoring a maturing industrial base. Growth potential persists for electronic-warfare pods, multispectral sensors, and secure datalinks that tie unmanned nodes into the broader kill chain.

By Domain: Air supremacy gives way to space innovation

Air assets retained 43.12% of % Taiwan defense market share in 2025 through F-16V induction and NASAMS rollout. Yet, investments in orbital assets drive a 6.64% CAGR for space systems as sovereign satellite networks become indispensable for beyond-line-of-sight coordination.

Naval developments like the Hai Kun submarine supply strategic depth, while land forces focus on mobile launchers that leverage satellite cueing. Counter-UAS projects ready for Q3 2025 fielding fuse radar, electro-optical, and cyber effects into a layered defense, illustrating how boundaries between air, land, and space are blurring inside the Taiwan defense market.

By Procurement Nature: Foreign dependence gradually yields to indigenous growth

Foreign platforms still account for 64.98% of Taiwan's defense market size in 2025, exemplified by the USD 987 million F-16 sustainment deal and continued HIMARS deliveries. However, Indigenous programs now log a 4.57% CAGR after missile production tripled and submarine construction proved viable at scale.

Local content in Clouded Leopard II armored vehicles has reached 89%, while the Chien Hsiang loitering munition moves toward low-rate initial production. Bilateral pacts with Japan's drone sector add propulsion and precision-machining know-how, reinforcing a procurement balance that shifts from outright imports to blended co-manufacture, anchoring sustainable growth in the Taiwan defense market.

Geography Analysis

Taiwan’s insular geography and 180 km separation from mainland China dictate a defense posture reliant on rapid-response fires, mobile sensors, and survivable basing. Harpoon anti-ship launchers enter service in mid-2025 to police the Taiwan Strait’s narrow sea lanes. NASAMS batteries shield northern population centers closest to Chinese air bases, while the island’s mountainous east hosts submarine pens and mobile missile depots that exploit natural cover.

Strategic depth is enhanced through US-Japan-Australia coordination under Indo-Pacific frameworks; a memorandum with Japan’s UAS industry anchors supply-chain cooperation in semiconductors and precision mechanics. Regional integration shapes platform interoperability choices and amplifies demand for link-compatible data networks.

Infrastructure upgrades concentrate on resilient command nodes designed to survive first-strike scenarios. Satellite communications link dispersed units, while fiber-optic redundancy spans urban regions. The geography-driven focus on compact launchers, sea-denial drones, and hard-to-detect missile trucks fosters continued local innovation.

Competitive Landscape

The Taiwan defense market is moderately concentrated, with US primes dominating high-value systems and Taiwanese entities scaling up subsystems and indigenous platforms. Lockheed Martin leads fighter sustainment and upgrades, RTX supplies missile inventory, and Leidos supports F-16 fleets. The National Chung-Shan Institute of Science and Technology (CSIST) tripled missile output in 2024, reflecting rising domestic capability.

Emerging private players such as Thunder Tiger and Geosat Aerospace compete in the expanding drone space, while CSBC Corporation anchors naval programs through the Hai Kun submarine line. Co-production clauses embedded in recent US contracts and the Taiwan-US Defense Industry Forum accelerate technology migration to local firms. Competitive advantage favors suppliers offering modular designs compatible with Taiwan’s dispersed basing and joint data standards.

Market entrants face stringent export-control vetting and must contend with cyclic budget reviews. Yet, opportunities abound in sustainment, cybersecurity, training, and obsolescence upgrades as Taiwan shifts from platform acquisition to readiness optimization.

Taiwan Defense Industry Leaders

National Chung-Shan Institute of Science and Technology

Aerospace Industrial Development Corporation

Lockheed Martin Corporation

RTX Corporation

General Dynamics Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: The cabinet cleared a TWD 410 billion (USD 12.6 billion) special budget that carves out TWD 150 billion (USD 4.6 billion) for UAV infrastructure, coast-guard upgrades, and IT enhancements, pending legislative sign-off

- February 2025: A military source confirmed on Monday that the United States finalized a deal to sell Taiwan three National Advanced Surface-to-Air Missile Systems (NASAMS) for approximately TWD 24.98 billion (USD 761.94 million). This agreement underscores the strengthening defense collaboration between the two nations amidst rising regional security concerns.

Taiwan Defense Market Report Scope

The Taiwan defense market report covers a detailed analysis of the country’s defense sector, encompassing various aspects such as military budgets, equipment procurement, indigenous defense production, defense OEMs, and security policies. The report focuses on Taiwan’s defense market and analyzes different aerial, naval, and land platforms.

The Taiwan defense market is segmented by equipment type (personal training and protection, communication, armament, and transport) and platform (terrestrial, aerial, and naval). The report offers the market size in value terms in USD for all the abovementioned segments.

| Air Force |

| Army |

| Navy |

| Personnel Training and Protection |

| C4ISR and Electronic Warfare |

| Vehicles |

| Weapons and Ammunition |

| Unmanned Systems |

| Space and Cyber Systems |

| Land |

| Air |

| Naval |

| Space |

| Cyber and Electromagnetic Spectrum |

| Indigenous Production |

| Foreign Procurement |

| By Armed Forces | Air Force |

| Army | |

| Navy | |

| By Type | Personnel Training and Protection |

| C4ISR and Electronic Warfare | |

| Vehicles | |

| Weapons and Ammunition | |

| Unmanned Systems | |

| Space and Cyber Systems | |

| By Domain | Land |

| Air | |

| Naval | |

| Space | |

| Cyber and Electromagnetic Spectrum | |

| By Procurement Nature | Indigenous Production |

| Foreign Procurement |

Key Questions Answered in the Report

What is the value of the Taiwan defense market today and in 2031?

The market stands at USD 7.03 billion in 2026 and is projected to reach USD 8.31 billion by 2031, growing at a 3.41% CAGR.

Which armed service holds the largest share and which is expanding the quickest?

The Air Force commands 42.55% of 2025 spending, while the Navy shows the fastest growth with a 4.12% CAGR through 2031.

Why are unmanned systems central to Taiwan’s modernization plans?

Government funding of USD 1.35 billion targets monthly production of 15,000 drones by 2028, supporting a porcupine strategy built on distributed, low-cost platforms.

How does the Indigenous Defense Submarine program benefit the domestic industry?

The TWD 284 billion (~USD 9.18 billion) program has multiplied CSBC Corporation’s revenue eight-fold and opened long-term orders for local sonar, combat-system, and torpedo suppliers.

What major obstacles slow Taiwan’s defense procurement cycles?

Legislative budget freezes reduced the 2025 allocation by 6.6%, and tightened US export-license rules add delays to a USD 19 billion arms backlog.

How important is the US-Taiwan Foreign Military Sales pipeline for market growth?

Combined FMS and direct commercial deals totaled USD 1.75 billion in 2024, with an extra USD 300 million approved for Altius-600M UAVs, generating follow-on demand for sustainment, training, and infrastructure.

Page last updated on: