Switzerland Data Center Cooling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

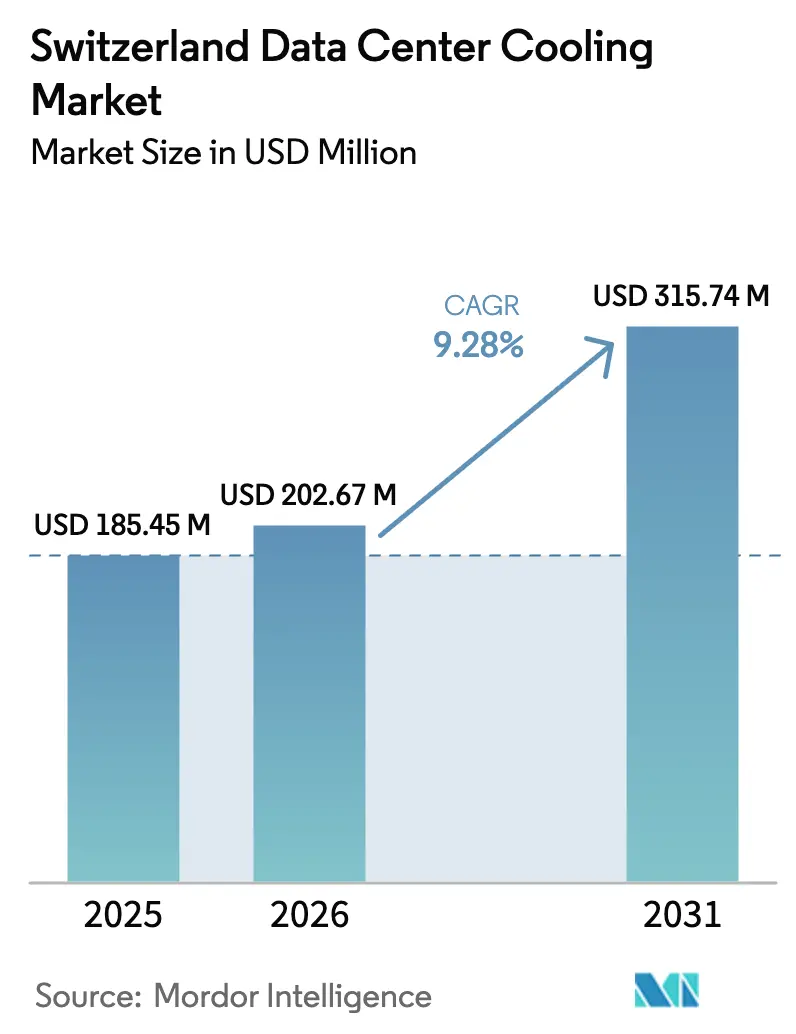

| Base Year Market Size (2025) | USD 185.45 Million |

| Market Size (2026) | USD 202.67 Million |

| Market Size (2031) | USD 315.74 Million |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

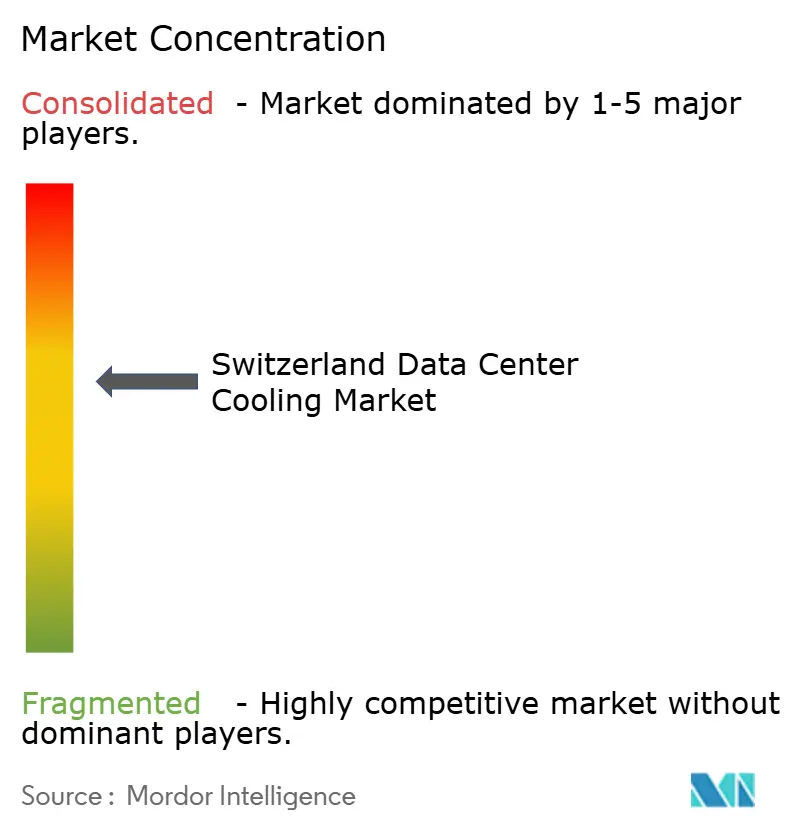

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Data Center Cooling Market Analysis by Mordor Intelligence

The Switzerland data center cooling market size is expected to grow from USD 185.45 million in 2025 to USD 202.67 million in 2026 and is forecast to reach USD 315.74 million by 2031 at 9.28% CAGR over 2026-2031. Growth is propelled by hyperscale investments linked to AI workloads, tightening Swiss energy-efficiency rules, and steady enterprise digitalisation. Rising rack densities that exceed 10 kW are hastening adoption of liquid-based solutions, while Switzerland’s 80% renewable power mix offers operators a sustainability edge that attracts global cloud providers. Carbon taxation and mandatory energy-use reporting, effective from 2025, are prompting quick payback retrofits such as waste-heat reuse and free cooling, and supply-side constraints linked to the nuclear phase-out intensify the focus on low-power designs. Competitive intensity is moderate: global vendors are consolidating niche liquid-cooling specialists and partnering with hyperscalers to launch AI-ready, prefabricated modules tailored to Swiss regulatory requirements.

Key Report Takeaways

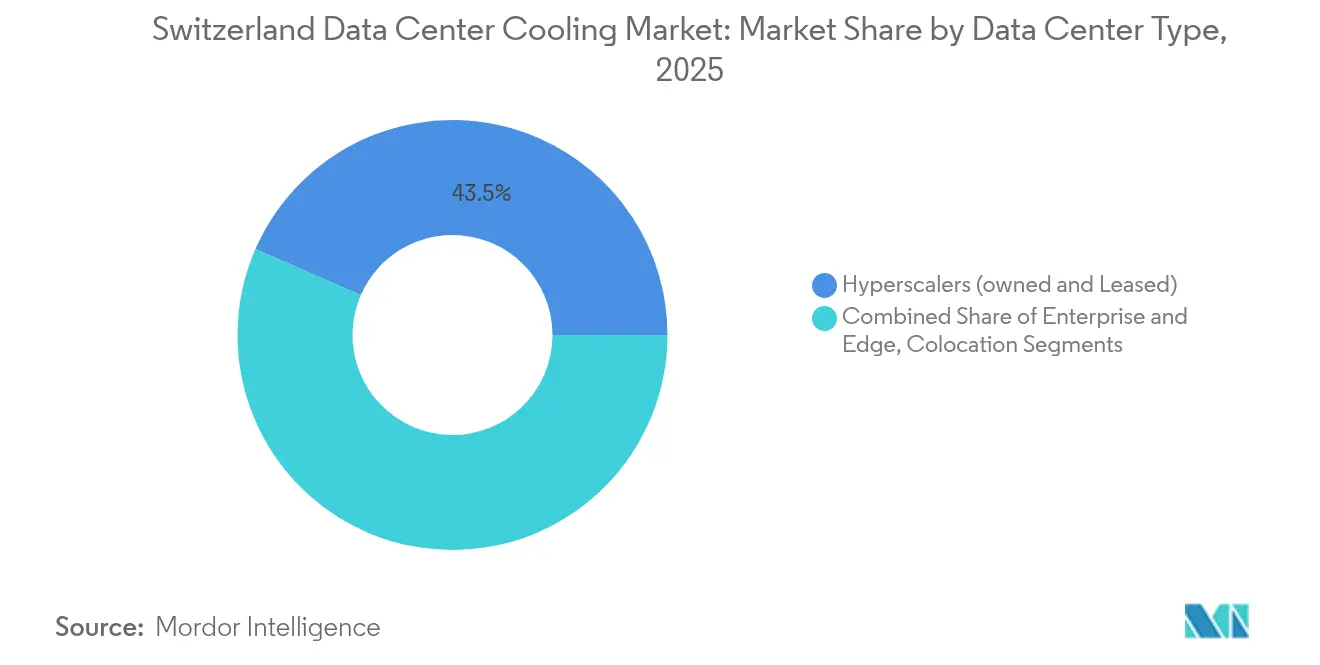

- By data center type, hyperscalers held 43.45% of the Switzerland data center cooling market share in 2025 and are advancing at a 11.65% CAGR through 2031.

- By tier, Tier 3 facilities controlled 65.80% revenue in 2025, whereas Tier 4 is the fastest-growing segment at 11.12% CAGR.

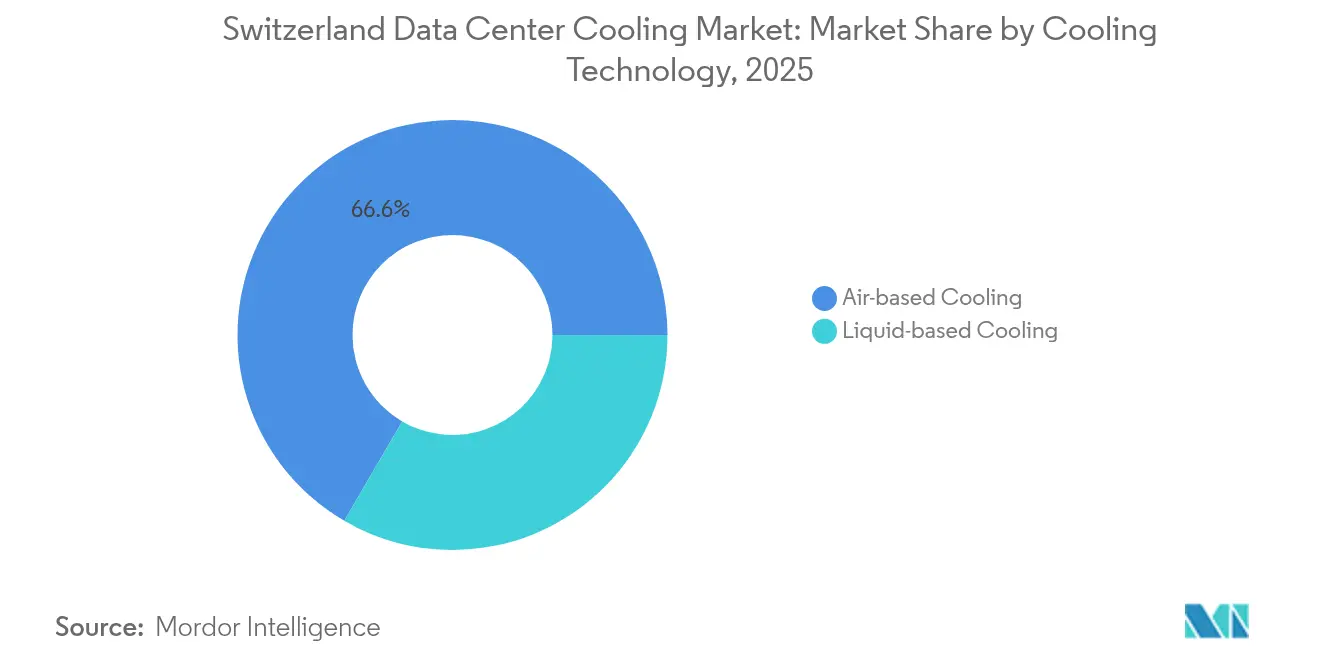

- By cooling technology, air-based systems kept 66.60% revenue share in 2025; liquid cooling is expanding at 10.02% CAGR to 2031.

- By component, equipment captured 78.05% of the Switzerland data center cooling market size in 2025 while services record the highest projected CAGR at 10.18% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland Data Center Cooling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale build-out accelerating cooling demand | +3.2% | Zurich and Geneva clusters | Medium term (2-4 years) |

| Stricter Swiss energy-efficiency and carbon-tax policies | +2.1% | National | Long term (≥4 years) |

| Liquid cooling adoption for AI/HPC workloads | +2.8% | Research hubs and hyperscale sites | Short term (≤2 years) |

| District-heating integration boosting waste-heat reuse | +1.4% | Bern, Basel, Zurich | Medium term (2-4 years) |

| Edge DC build in Alpine regions | +0.8% | Alpine cantons | Long term (≥4 years) |

| Corporate net-zero pledges | +1.6% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hyperscale build-out accelerating cooling demand

Microsoft’s USD 400 million upgrade of four Swiss facilities illustrates the scale of new thermal loads that must be handled 10-140 kW per rack. Vantage Data Centers’ CHF 370 million Zurich 2 campus employs rainwater infiltration and heat pumps to meet strict PUE targets.[1]Greater Zurich Area AG, “Vantage Zurich 2 campus sets new efficiency benchmark,” greaterzuricharea.co STACK Infrastructure’s acquisition of Safe Host adds high-density expertise, signaling continued capacity clustering in Zurich and Geneva. These projects collectively lift demand for scalable liquid and hybrid systems able to balance AI clusters and legacy racks. Vendors able to deliver turnkey, low-latency cooling gain advantage as hyperscalers increasingly dictate specification standards.

Stricter Swiss energy-efficiency and carbon-tax policies

The Climate and Innovation Act, in force since 2025, mandates net-zero by 2050 and compels annual disclosure of PUE and water usage for sites above 100 kW IT load.[2]Swiss Federal Office of Energy, “Climate and Innovation Act implementation guidelines,” admin.ch Early-adopter cantons such as Basel link tax rebates to documented waste-heat reuse, steering operators toward heat-pump-enabled chillers and free-cooling schemes. Voluntary alignment to the EU Energy Efficiency Directive raises compliance hurdles but enhances market access for Swiss operators. Cooling vendors demonstrating carbon-price resilience secure procurement preference, while service providers that optimise PUE gain annuity revenues through performance contracts. Over the long term, policy pressure is forecast to shave 10-15 bp off facility-level OPEX for compliant operators.

Liquid cooling adoption for AI/HPC workloads

ETH Zurich’s Aquasar cut energy use 40% versus air-cooled peers and re-purposed 85% of waste heat for campus heating, validating direct-to-chip solutions. The Swiss National Supercomputing Centre’s Alps system, sixth globally, relies on advanced coolant distribution to maintain stable thermals during 20× workload bursts. Vertiv’s 2024 coolant distribution units support rack densities beyond 100 kW, underscoring vendor race to standardise hardware for GPU clusters. Liquid adoption removes airflow bottlenecks, trims white-space footprint, and unlocks monetisation of exhaust heat into district grids.

District-heating integration boosting waste-heat reuse

Swisscom’s Wankdorf facility feeds Bern’s district network and sustains a PUE of 1.2 by exporting up to 15 GWh of heat yearly. IBM’s Uitikon project warms a municipal pool, saving 130 tons of CO₂ annually. Berg-Käserei cheese factory reuses data-center heat pumps to eliminate 1.5 million kWh of natural-gas demand. Growing urban heat grids in Zurich, Basel and Bern create a dual-revenue model where cooling CAPEX is offset by heat-offtake contracts.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX for advanced cooling technologies | –1.8% | National, heavier on SME operators | Short term (≤2 years) |

| Water scarcity in select cantons | –1.2% | Basel-Landschaft, Zurich, Aargau | Medium term (2-4 years) |

| Grid-capacity limits post-nuclear phase-out | –2.1% | National, acute in industrial zones | Long term (≥4 years) |

| Shortage of specialised cooling O and M talent | –0.9% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX for advanced cooling technologies

Liquid systems can exceed CHF 2 million per MW, deterring colocation players with thin margins. Schneider Electric’s AI-ready reference designs demand complete overhaul of power and piping infrastructure, pushing smaller operators to defer projects. Vertiv’s prefabricated MegaMod CoolChip cuts build time by 50% but still requires high-end CDUs and leak-detection arrays. Financing gaps curb rapid diffusion and lengthen refresh cycles, tempering near-term growth in the Switzerland data center cooling market.

Water scarcity in select cantons

The 2022 drought triggered draft ordinances to curtail industrial water withdrawals during prolonged heatwaves.[3]Swiss Broadcasting Corporation, “Switzerland prepares drought early-warning system,” swissinfo.ch Basel-Landschaft’s PFAS contamination probe tightens groundwater abstraction permits, forcing facilities to consider air-side, water-free cooling or high-efficiency adiabatic systems. Operators increasingly add rainwater harvesting and closed-loop treatment to insulate against supply disruptions, elevating project complexity and cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Data Center Type: Hyperscalers drive cooling innovation

Hyperscalers captured 43.45% of the Switzerland data center cooling market in 2025 and are on track for 11.65% CAGR through 2031, fueled by AI cluster roll-outs demanding 100 kW-plus rack densities. Enterprise and edge sites adopt smaller, modular chillers with integrated free-cooling to balance cost and uptime, while colocation operators differentiate through PUE guarantees.

Colocation campuses such as Green’s Metro Campus Zurich illustrate how shared infrastructure benefits from scale, enabling lake-water loops and rooftop PV to offset cooling load. Edge nodes in Alpine regions rely on sealed refrigerant systems and phase-change materials to cope with extreme ambient swings. Services revenue tied to hyperscale retrofits is expected to outpace equipment sales as operators seek design and commissioning expertise for high-density aisles within the Switzerland data center cooling market.

By Tier Type: Tier 4 acceleration drives premium cooling

Tier 3 maintained a 65.80% share in 2025, yet Tier 4 facilities exhibit the fastest growth at 11.12% CAGR, underpinning premium demand for 2N chillers, dual power feeds, and redundant CDUs. Swisscom’s Wankdorf site demonstrates Tier IV design, blending indirect adiabatic coolers with heat-pump redundancy to sustain operations during maintenance windows. Cost-sensitive Tier 1–2 operators focus on economiser hours and airflow containment to remain competitive. The requirement for continuous operation even during utility outages pushes Tier 4 builders toward hybrid air-liquid solutions that improve resilience and efficiency.

By Cooling Technology: Liquid systems gain AI-driven momentum

Air-based solutions held 66.60% revenue share in 2025, yet liquid technologies are growing 10.02% CAGR as GPU-rich racks exceed the thermal limits of legacy CRACs. ETH Zurich’s Aquasar and the CSCS Alps supercomputer prove that coolant loops enable high performance with 40% lower energy use, while allowing 85% heat reuse. Vendors such as Alfa Laval supply brazed plate heat exchangers tailored for dielectric fluids, and Vertiv’s coolant distribution units simplify deployment within brownfield sites. Dual-loop topologies mitigate water-quality risk, helping operators maintain regulatory compliance on effluent discharge.

By Component: Services growth reflects complexity increase

Equipment represented 78.05% revenue in 2025; however, services are advancing at 10.18% CAGR because liquid systems demand specialised design, installation and predictive maintenance. Consulting and training form a growing slice of the Switzerland data center cooling industry as operators upskill staff for hybrid environments.

Suissetec’s training campus is scaling enrolments to supply installation technicians certified on refrigerant-free liquid solutions. Managed-service contracts blending remote monitoring, leak detection and heat-recovery optimisation are becoming popular with colocation tenants who lack onsite expertise. In turn, OEMs bundle performance-based guarantees that monetise efficiency gains.

Geography Analysis

Zurich canton anchors more than one-third of installed cooling capacity, driven by hyperscale clusters and the financial sector’s stringent latency needs. Microsoft, Vantage and Green collectively lift rack counts that require megawatt-scale chiller banks and deep-lake water loops, reinforcing Zurich’s role as the epicentre of the Switzerland data center cooling market. Geneva ranks second, serving international organisations and acting as a bridge for Franco-Swiss data traffic; Infomaniak’s 2025 launch adds modular liquid-ready halls that meet dual-jurisdiction compliance.

Basel benefits from Rhine water access yet faces stricter quality controls due to PFAS investigations, uplifting demand for closed evaporative towers with zero liquid discharge. Lausanne and Bern host university HPC clusters, pushing local operators towards direct-to-chip solutions and district-heat off-take agreements to meet municipal carbon targets.

Alpine cantons such as Graubünden and Valais see rising micro-edge deployments to support tourism and IoT infrastructure. Natural low ambient temperatures support free-cooling up to 9 months annually, although grid access and fibre backhaul remain constraints. Operators mitigate by pairing modular battery systems and satellite-backed connectivity, underscoring regional nuance within the Switzerland data center cooling market.

Competitive Landscape

The Switzerland data center cooling market features a balanced mix of global leaders and regional specialists. Schneider Electric’s 2024 acquisition of Motivair augments its liquid portfolio and aligns with its AI-ready reference designs codesigned with NVIDIA. Vertiv counters with MegaMod CoolChip prefabricated halls and the CoolPhase Flex hybrid solution launched with Compass Datacenters, catering to densities beyond 100 kW per rack.

Alfa Laval and Danfoss supply European-made heat exchangers and high-lift compressors suited to Swiss refrigerant rules, while Munters, STULZ and Johnson Controls deliver indirect evaporative and adiabatic systems that maximise free-cooling hours. Regional integrators such as Rittal and Swegon provide turnkey white-space suites, leveraging local install networks to shorten lead times.

Market entry barriers include language diversity, canton-level permitting and strict labour codes, prompting foreign OEMs to partner with Swiss service firms for deployment. Waste-heat partnerships with utilities and district-energy companies emerge as a competitive differentiator, allowing operators to monetise otherwise-discarded thermal energy and to meet carbon-tax thresholds.

Switzerland Data Center Cooling Industry Leaders

Schneider Electric SE

Vertiv Group Corp.

Alfa Laval AB

Munters Group AB

Systemair AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Microsoft commits USD 400 million to upgrade four Swiss data centers, adding AI training for one million residents.

- February 2025: Vantage Data Centers allocates EUR 1.4 billion (USD 1.62 billion) to its EMEA platform, extending Swiss build-outs.

- January 2025: STACK Infrastructure acquires Safe Host, bolstering high-density cooling expertise in Switzerland.

- January 2025: Infomaniak opens a Geneva facility featuring liquid-ready cooling and renewable integration.

Switzerland Data Center Cooling Market Report Scope

Data center cooling is a set of techniques and technologies to maintain optimal operating temperatures in data center environments. Data center cooling is critical as data center facilities house many computer servers and network equipment that generate heat during operation. Efficient cooling systems are used to dissipate this heat and prevent equipment from overheating, ensuring continued reliable operation of the data center. Various methods, such as air conditioning, liquid cooling, and hot/cold aisle containment, are commonly used to control temperature and humidity in data centers.

The Switzerland Data Center cooling market study comprises by Technology (Air-based cooling (Chiller and Economizer, CRAH, Cooling Towers and Others), Liquid-based cooling (Immersion Cooling, Direct-to-chip Cooling, Rear-Door Heat Exchanger)), Type of Data Center (Hyperscaler, Enterprise and Colocation) , by End-User Industry (IT & Telecom, Retail & Consumer Goods, Healthcare, Media & Entertainment, Federal & Institutional agencies, and Other end-users). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hyperscalers (owned and Leased) |

| Enterprise and Edge |

| Colocation |

| Tier 1 and 2 |

| Tier 3 |

| Tier 4 |

| Air-based Cooling | Chiller and Economizer (DX Systems) |

| CRAH | |

| Cooling Tower (covers direct, indirect and two-stage cooling) | |

| Others | |

| Liquid-based Cooling | Immersion Cooling |

| Direct-to-Chip Cooling | |

| Rear-Door Heat Exchanger |

| By Service | Consulting and Training |

| Installation and Deployment | |

| Maintenance and Support | |

| By Equipment |

| By Data Center Type | Hyperscalers (owned and Leased) | |

| Enterprise and Edge | ||

| Colocation | ||

| By Tier Type | Tier 1 and 2 | |

| Tier 3 | ||

| Tier 4 | ||

| By Cooling Technology | Air-based Cooling | Chiller and Economizer (DX Systems) |

| CRAH | ||

| Cooling Tower (covers direct, indirect and two-stage cooling) | ||

| Others | ||

| Liquid-based Cooling | Immersion Cooling | |

| Direct-to-Chip Cooling | ||

| Rear-Door Heat Exchanger | ||

| By Component | By Service | Consulting and Training |

| Installation and Deployment | ||

| Maintenance and Support | ||

| By Equipment | ||

Key Questions Answered in the Report

What is the current size of the Switzerland data center cooling market?

The market stands at USD 202.67 million in 2026 and is forecast to grow to USD 315.74 million by 2031.

Which segment leads the Switzerland data center cooling market share?

Hyperscale facilities led with 43.45% revenue share in 2025 and are also the fastest-growing segment at 11.65% CAGR.

How fast is liquid cooling growing in Switzerland?

Liquid-based solutions are expanding at 10.02% CAGR as AI workloads push rack densities beyond the thermal limits of air systems.

Why are Swiss data centers integrating with district heating networks?

Waste-heat sales improve facility PUE, generate additional revenue and help operators comply with strict carbon-tax rules.

Page last updated on: