Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

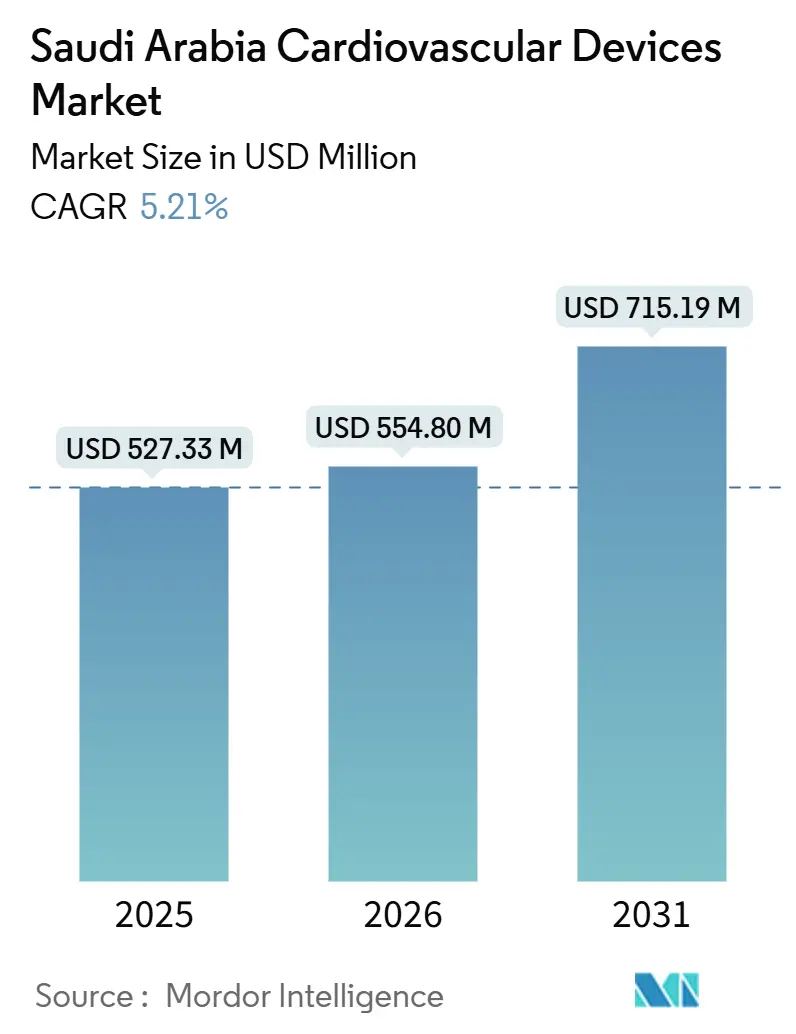

| Base Year Market Size (2025) | USD 527.33 Million |

| Market Size (2026) | USD 554.80 Million |

| Market Size (2031) | USD 715.19 Million |

| Growth Rate (2026 - 2031) | 5.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Saudi Arabia Cardiovascular Devices Market Analysis by Mordor Intelligence

The Saudi Arabia Cardiovascular Devices Market size is projected to expand from USD 527.33 million in 2025 and USD 554.80 million in 2026 to USD 715.19 million by 2031, registering a CAGR of 5.21% between 2026 to 2031.

The expansion reflects the kingdom’s pivot toward preventive cardiology, fueled by Vision 2030’s USD 65 billion health-care envelope that is modernizing catheterization laboratories, hybrid operating rooms, and virtual-care hubs. Mandatory employer-funded insurance is widening access to transcatheter therapies and home-based monitoring, while localization incentives are encouraging multinationals to assemble stents and pacemakers inside the Gulf’s largest economy. Rapid uptake of AI-enabled arrhythmia analytics is cutting 30-day readmissions, and expanding diabetes prevalence forecast to reach 9.5 million adults by 2050 is sustaining demand for drug-eluting stents tuned for calcified, insulin-resistant vessels.[1]International Diabetes Federation, “IDF Diabetes Atlas 10th Ed,” diabetesatlas.org Suppliers that pair evidence-backed hardware with cloud subscriptions are gaining an early edge as the Saudi Arabia cardiovascular devices market shifts toward value-based reimbursement structures.

Key Report Takeaways

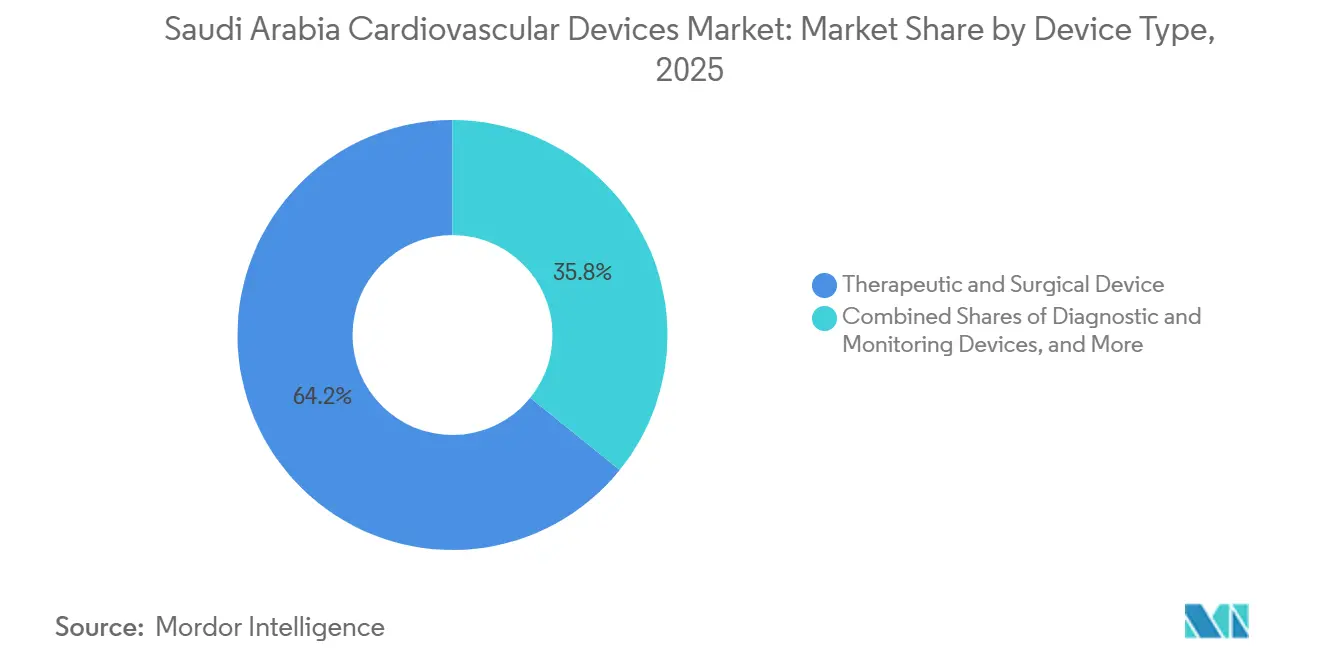

- By device type, therapeutic & surgical devices led with 64.20% of the Saudi Arabia cardiovascular devices market share in 2025, whereas diagnostic & monitoring devices are projected to post the fastest 5.93% CAGR to 2031.

- By application, coronary artery disease accounted for 48.50% of the Saudi Arabia cardiovascular devices market in 2025, while structural heart disease devices are expected to expand at a 6.45% CAGR through 2031.

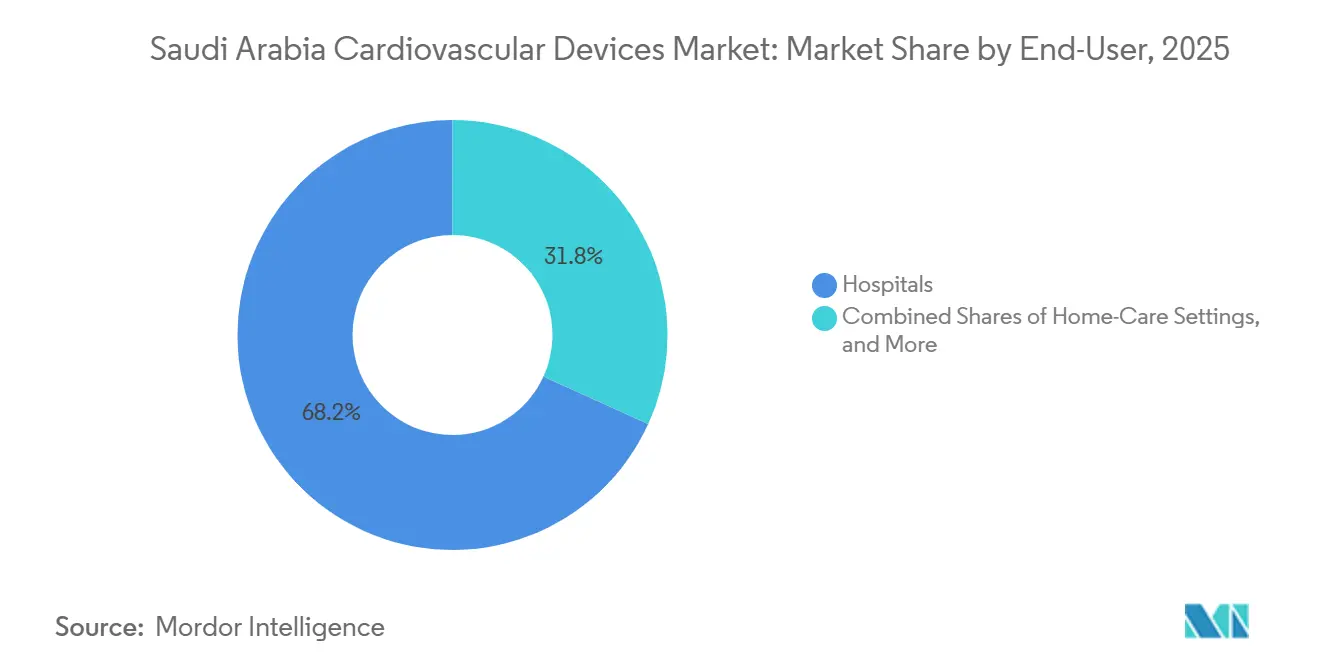

- By end user, hospitals accounted for 68.20% of revenue share in 2025; home care settings are forecast to grow at a 6.71% CAGR through 3031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Saudi Arabia Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising burden of CVD & diabetes comorbidity | +1.2% | National, focused on Riyadh, Jeddah, Dammam | Long term (≥ 4 years) |

| Large-scale vision 2030 investments in cardiac infrastructure | +1.5% | Kingdom-wide, priority in Makkah, Madinah, Eastern Province | Medium term (2-4 years) |

| Mandatory private health insurance expanding procedure access | +0.9% | Nationwide, fastest in private hospital chains | Short term (≤ 2 years) |

| Localization incentives for in-kingdom device manufacturing | +0.6% | Industrial zones around Riyadh | Long term (≥ 4 years) |

| Rapid uptake of transcatheter & hybrid cath-lab therapies | +0.8% | Tertiary centers in Riyadh and Jeddah | Medium term (2-4 years) |

| AI-enabled predictive analytics reducing readmissions | +0.3% | Major hospital clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of CVD & Diabetes Comorbidity

Cardiovascular disease accounts for more than 45% of deaths in Saudi Arabia, and diabetes prevalence stands at 23.1% among adults, creating a dual epidemic that pushes complex percutaneous interventions to the forefront.[2]International Diabetes Federation, “IDF Diabetes Atlas 10th Ed,” diabetesatlas.org

Coronary stent cases are increasingly supported by intravascular ultrasound to optimize deployment in calcified lesions common in diabetic vessels. Heart-failure clinics now rely on cardiac resynchronization devices and pulmonary pressure sensors to manage diabetic cardiomyopathy. National Transformation Program screening targets people aged 40–60. Yet, almost half of diabetics remain undiagnosed until an acute coronary event, highlighting the role for point-of-care biomarker kits and mobile echo vans in provincial areas. The sustained disease load secures long-run momentum for the Saudi Arabia cardiovascular devices market.

Large-Scale Vision 2030 Investments in Cardiac Infrastructure

The 2024 national budget reserved SAR 260 billion (USD 69.3 billion) for health and social development. Five new hospitals with 963 cardiovascular-ready beds will open by 2025, while cluster models integrate peripheral clinics via tele-cardiology networks. These physical and digital expansions accelerate placements of cath-lab imaging, portable ultrasound, and remote patient monitoring kits. Government procurement increasingly embeds local-content clauses, encouraging multinationals to establish technical transfer agreements with Saudi factories. As infrastructure matures, high-acuity centers in Riyadh and Jeddah become referral anchors for complex structural heart and electrophysiology cases.

Mandatory Private Health Insurance Expanding Procedure Access

A staged rollout of compulsory private health coverage is lifting procedure volumes across public and private hospitals. Reimbursement approvals for minimally invasive cardiovascular interventions rose 34% year-on-year in 2024. More consistent payer policies lower out-of-pocket spending, paving the way for broader adoption of premium transcatheter valves and drug-coated balloons. The insurance boom is also evident in secondary cities, where newly insured patients undergo deferred diagnostics, driving unit sales for ambulatory ECG, blood-pressure, and lipid management devices. Payers, however, are linking reimbursement to real-world evidence, spurring suppliers to bundle devices with outcome-monitoring software.

Localization Incentives for In-Kingdom Device Manufacturing

Tax holidays, subsidized land, and fast-track approvals aim to localize 30% of medical device output by 2030. Jamjoom Medical Industries is ramping PTCA balloon lines, trimming landed cost by 20% versus imports. Authorities court joint ventures with Medtronic and Boston Scientific to assemble rhythm-management devices in King Abdullah Economic City, promising Gulf-wide export reach. Local sourcing ensures supply continuity and helps suppliers comply with public procurement content rules, strengthening competitiveness in the Saudi Arabia cardiovascular devices market.

206 medical-technology plants now operate nationwide, backed by SAR 3.1 billion (USD 827 million) in capital. Balloon catheters, blood-pressure systems, and bare stents already roll off Saudi lines, shrinking lead times and insulating hospitals against global logistics shocks. 40% domestic-content rules on public tenders, effective 2025, further reinforce the shift. International OEMs are forming licensing and JV structures to maintain market access, producing low- to mid-complexity items locally while reserving high-end transcatheter platforms for direct import. The learning curve is flattening rapidly as public research grants support the development of advanced materials for implants. [3]Saudi Press Agency, “Saudi Arabia’s Healthcare Industry: A Transformative Journey Towards Self-Sufficiency,” spa.gov.sa

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented procurement & lengthy SFDA approvals | -0.8% | All clusters, sharper in secondary hospitals | Short term (≤ 2 years) |

| High price pressure in public tenders | -0.6% | Ministry of Health hospitals kingdom-wide | Medium term (2-4 years) |

| Shortage of cardiac electrophysiologists | -0.4% | Acute in Tabuk, Najran, Northern Border | Long term (≥ 4 years) |

| Cultural barriers delaying diagnosis in women | -0.3% | Conservative regions nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Procurement & Lengthy SFDA Approvals

Twenty autonomous health clusters each run distinct tenders, forcing manufacturers to navigate parallel formularies and stretching product launch timelines to 18 months on average. SFDA, limited to processing roughly 200 Class III filings a year, confronts backlogs that postpone next-generation valve and ICD introductions. Exclusive contracts in certain clusters restrict volume scale, discouraging local inventory hubs and inflating last-mile logistics. The complexity chips 0.8 percentage points from the Saudi Arabia cardiovascular devices market CAGR.

High Price Pressure in Public Tenders

Budget-capped public hospitals award contracts to the lowest bidder, often favoring bare-metal stents sold at 40% below polymer-free alternatives, despite superior outcomes in diabetic patients. Vendors endure single-digit margins and cross-subsidize with higher-priced private sales. An up-front cost focus also undercuts adoption of remote monitoring subscriptions that reduce readmissions but carry multi-year fees. Until reference-pricing models link payment to outcomes, price compression will dilute value creation inside the Saudi Arabia cardiovascular devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Therapeutic Dominance Meets Diagnostic Acceleration

Therapeutic & surgical systems captured 64.20% of 2025 revenue, underscoring the centrality of stents, valve kits, and rhythm-management implants in the Saudi Arabia cardiovascular devices market. Drug-eluting stents remain workhorses, yet bioresorbable scaffolds appeal to younger cohorts seeking vessel restoration without permanent metal. Leadless pacemakers such as Micra AV2, introduced locally in 2025, answer infection concerns and reduce pocket complications.

Diagnostic & monitoring devices, while smaller, are forecast to advance at a 5.93% CAGR through 2031, fueled by SEHA Virtual Hospital reimbursements that pay for wearable ECG patches and implantable loop recorders. GE’s rollout of 1,000 bedside monitors and 500 Portrait VSM wearables has already cut unplanned readmissions by nearly one-quarter. Non-invasive imaging modalities such as FFR-CT, cardiac MRI, and handheld ultrasound further position the Saudi Arabia cardiovascular devices market for sustained long-term growth as clinicians prioritize precision triage over indiscriminate catheterization.

By Application: Coronary Dominance Yields to Structural Complexity

Coronary artery disease accounted for 48.50% of application sales in 2025, yet its growth is moderating as lipid-lowering therapies and lifestyle campaigns gain ground. Case mix is tilting toward chronic total occlusions and left main bifurcations that demand imaging-guided atherectomy and newer 80-µm strut DES platforms. In parallel, the Saudi Arabia cardiovascular devices market for structural heart disease is projected to grow at a 6.45% CAGR as mitral clip and tricuspid repair systems clear regulatory hurdles. Edwards SAPIEN valves and Abbott Navitor kits are now routine for intermediate-risk TAVR recipients, reducing length of stay from 10 days to 2.

Arrhythmia care is another bright spot: atrial fibrillation prevalence is climbing 8–10% annually among seniors, boosting use of pulsed-field ablation catheters that shorten procedure time and spare esophageal tissue. Heart-failure pathways integrate CardioMEMS pulmonary sensors that flag pressure increases days before symptoms, enabling medication titration to curb rehospitalization. Together, these innovations diversify revenue beyond coronary workhorses and underpin the evolving Saudi Arabia cardiovascular devices market.

By End-User: Hospital Hegemony Faces Home-Care Disruption

Hospitals captured 68.20% of 2025 revenue, reflecting their role in high-acuity interventions. Government funding for five additional tertiary hospitals by 2025 will reinforce the cath-lab installed bases. Multi-disciplinary heart teams and advanced imaging suites enable comprehensive case management, reinforcing purchasing power for bundled device-and-service contracts.

Home care, though it holds little value today, will post a 6.71% CAGR. Wearable diagnostics, enabled by 4G-5G connectivity, shift routine rhythm and blood-pressure surveillance away from clinics. Insurers now reimburse cloud‐submitted vital-sign data, cutting hospital revisit rates. Suppliers compete on battery life, data encryption, and Arabic-language app interfaces. As device algorithms refine alerts, physician confidence in remote medication titration is rising. The Saudi Arabia cardiovascular devices industry consequently sees a new aftermarket for subscription-based data platforms and consumables.

Geography Analysis

Major metropolitan areas Riyadh, Jeddah, and Dammam account for almost 70% of the 2025 unit demand within the Saudi Arabia cardiovascular devices market. Large expatriate populations with employer-funded insurance drive procedural growth, particularly in PCI and rhythm management. State-backed centers of excellence in these cities benefit from early allocations of AI-ready imaging suites and robotic cath-lab systems.[4]Philips, “Philips unveils new healthtech innovations at Global Health 2024,” philips.sa

The eastern region shows outsized momentum thanks to industrial-zone employment and proximity to Bahrain and Kuwait. Cross-border referrals lift cath-lab capacity utilization, and hospitals in Al Khobar now run high-risk TAVR programs supported by remote proctorship. Device suppliers leverage bonded-warehouse status in the region’s economic zones to expedite inventory replenishment.

Western cities such as Jeddah and Mecca experience seasonal surges during Hajj and Umrah, resulting in spikes in demand for portable defibrillators and temporary cath-lab consumables. Government task forces pre-position devices to handle acute coronary syndromes among pilgrims. Vendors often employ flexible rental models to meet this predictable yet time-bound demand, thereby strengthening the aftermarket for refurbished imaging.

Northern and southern provinces, historically underserved, are now on the investment agenda. Tele-cardiology links rural clinics to central reading hubs, boosting sales of connected ECG and vital-sign devices. The Ministry of Health allocates mobile cath lab vans to these areas, thereby generating demand for compact angiography systems. Over time, equalization of service levels is expected to lift Saudi Arabia's cardiovascular devices market share in these provinces from single digits to the mid-teens.

Competitive Landscape

Global incumbents retain scale advantages, yet localization policies and joint ventures are redrawing competitive boundaries. Medtronic and Abbott co-manufacture select consumables with Saudi firms to satisfy domestic-content thresholds. Boston Scientific supplies structural heart implants while collaborating with university labs on clinician training.

Domestic producers are advancing beyond basic blood-pressure and syringe pumps into angioplasty kits and rhythm monitoring patches. WCS Global Medical Technology opened a Riyadh production line for sphygmomanometers in late 2024, targeting tender bids that require 40% local content wcs-gmedtech. Jamjoom Medical Industries secured licensing deals for compliant coronary balloons, narrowing price gaps with imports.

Digital-health entrants exploit gaps in home monitoring and data analytics. Huma Therapeutics gained Saudi FDA Class C clearance for its disease-agnostic monitoring platform that integrates rhythm and metabolic metrics huma. GE HealthCare leverages regional reference sites for its Vscan Air SL ultrasound, pairing device sales with cloud AI subscriptions medimaging. White-space opportunities remain in pediatric congenital devices and women-specific valve prostheses, segments where product portfolios are still thin.

Saudi Arabia Cardiovascular Devices Industry Leaders

Abbott Laboratories

Cardinal Health Inc.

GE Healthcare

Siemens Healthineers AG

Atlas Medical LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Acarix AB announced it had established a strategic distribution partnership with a new partner in Saudi Arabia. Under the agreement, the partner managed local regulatory approval processes for the CADScor System in Saudi Arabia at its own expense.

- June 2025: Alphaiota and PMcardio partnered to introduce the first AI-powered myocardial-infarction diagnostic platform in Saudi Arabia, marking the solution’s debut in the Middle East.

- May 2025: The American Heart Association signed an MoU with the Saudi National Heart Center to roll out evidence-based cardiac pathways and national registries.

- May 2025: Bayer and Huma Therapeutics launched the Bayer Aspirin Heart Health Risk Assessment to screen one million citizens for cardiovascular risk.

- January 2025: Abbott Laboratories completed Saudi Arabia’s first robotic HeartMate 3 LVAD implant at King Faisal Specialist Hospital & Research Centre, proving minimally invasive durability and positioning Riyadh as a regional training nucleus.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Saudi Arabia cardiovascular devices market as all FDA- and SFDA-cleared diagnostic, monitoring, therapeutic, and surgical equipment intended for human cardiovascular care across hospital, specialty clinic, and eligible home-care settings. According to Mordor Intelligence, devices covered range from non-invasive ECG systems to implantable stents, valves, pacemakers, ICDs, ventricular assist devices, and associated catheters.

Scope Exclusion: Equipment meant purely for veterinary medicine, research prototypes not yet approved for clinical use, and consumables such as contrast media are excluded.

Segmentation Overview

- By Device Type

- Diagnostic & Monitoring Devices

- ECG Systems

- Remote Cardiac Monitors & Patches

- Cardiac MRI

- Cardiac CT

- Echocardiography / Ultrasound

- Fractional Flow Reserve (FFR) Systems

- Therapeutic & Surgical Devices

- Coronary Stents

- Drug-Eluting Stents

- Bare-Metal Stents

- Bioresorbable Stents

- Catheters

- PTCA Balloon Catheters

- IVUS/OCT Catheters

- Cardiac Rhythm Management

- Pacemakers

- Implantable Cardioverter Defibrillators

- Cardiac Resynchronization Therapy Devices

- Heart Valves

- TAVR/TAVI

- Mechanical Valves

- Tissue/Bioprosthetic Valves

- Ventricular Assist Devices

- Artificial Hearts

- Grafts & Patches

- Other Cardiovascular Surgical Devices

- Coronary Stents

- Diagnostic & Monitoring Devices

- By Application

- Coronary Artery Disease

- Arrhythmia

- Heart Failure

- Structural Heart Disease

- Hypertension

- Others

- By End-User

- Hospitals

- Home-Care Settings

- Others

Detailed Research Methodology and Data Validation

Primary Research

Interviews with interventional cardiologists, biomedical engineers, purchasing heads of tier-1 hospitals, and regional distributors across Riyadh, Jeddah, Dammam, and Tabuk validated utilization rates, warranty pricing, and typical replacement cycles. Follow-up surveys with device regulators and payer executives helped us refine forecast drivers such as insurance coverage expansion and localization quotas.

Desk Research

Mordor analysts started with public sources such as the Saudi Ministry of Health statistical yearbook, the Gulf Health Council disease burden dashboards, and trade data from the General Authority of Statistics, which reveal procedure volumes and import values for stents, rhythm-management implants, and imaging consoles. Clinical incidence data were gathered from peer-reviewed journals like the Journal of Saudi Heart Association and Lancet Global Health, while reimbursement policies were tracked through the Council of Cooperative Health Insurance circulars. Company 10-Ks and SFDA post-market surveillance notices supplied average selling price (ASP) clues, and databases we subscribe to, D&B Hoovers for hospital spend, Questel for recent device patents, and Dow Jones Factiva for tender awards, completed the evidence set.

These illustrative sources are not exhaustive; many additional publications and data feeds informed baseline numbers and cross-checks.

Market-Sizing & Forecasting

A top-down construct began with SFDA import value and domestic production disclosures, which were then adjusted for channel mark-ups and service contracts to yield end-user expenditure. Select bottom-up checks, sampled ASP x annual implant volumes for coronary stents, pacemakers, and TAVR valves, balanced the totals. Key variables modeled include procedure incidence per 100,000 adults, diabetes-linked CVD prevalence shifts, catheter-lab capacity additions under Vision 2030, average device ASP erosion, and tender award cadence. Multivariate regression, anchored to these drivers and expert consensus on penetration ceilings, produced the 2025-2030 outlook. Any data gaps, for example in private-clinic volumes, were bridged through weighted extrapolation from confirmed hospital shares.

Data Validation & Update Cycle

Outputs pass three-layer review: analyst, senior domain lead, and independent QC, each flagging anomalies beyond a 5% variance band. The model refreshes annually, with unscheduled revisions triggered by major regulatory, currency, or procurement shocks before client delivery.

Why Mordor's Saudi Arabia Cardiovascular Devices Baseline Earns Trust

Published market values often diverge because firms pick differing device baskets, ASP assumptions, and update rhythms.

By aligning scope with SFDA classifications, applying fresh hospital-level interviews, and re-checking currency conversions, Mordor presents a balanced, decision-ready baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 527.33 M (2025) | Mordor Intelligence | - |

| USD 578.20 M (2024) | Regional Consultancy A | Includes veterinary and research devices; older currency rate; no local interviews |

| USD 412.60 M (2024) | Global Consultancy B | Excludes wearable monitors; relies on global ASP averages without SFDA import data |

| USD 580.00 M (2024) | Research Boutique C | Applies aggressive procedure growth from GCC average; last update 2023 |

The comparison shows that methodology choices, not simple arithmetic, drive numeric gaps. Mordor's disciplined variable selection, yearly refresh, and twin top-down/bottom-up checks give stakeholders a transparent, reproducible benchmark they can confidently use for strategy and investment planning.

Key Questions Answered in the Report

How large will Saudi Arabias cardiovascular device ecosystem be by 2031?

The Saudi Arabia cardiovascular devices market is expected to reach USD 715.19 million by 2031, growing at a 5.21% CAGR from 2026.

Which device category grows fastest in the next five years?

Diagnostic & monitoring systems are projected to advance at a 5.93% CAGR to 2031 on the back of virtual-care and wearable ECG adoption.

What role does Vision 2030 play in shaping cardiac-care demand?

Vision 2030s USD 65 billion health budget funds hybrid cath-labs, remote monitoring hubs, and hospital privatization, which together lift procedure volumes and spur local manufacturing.

Are price pressures limiting uptake of new stent technologies?

Yes, lowest-bid public tenders favor bare-metal and legacy DES models, delaying widespread use of premium polymer-free or bioresorbable platforms.

How is talent scarcity affecting rhythm-management procedures?

With fewer than 50 electrophysiologists nationwide, wait times for complex ablations and ICD implants extend beyond eight weeks outside major cities, slowing high-end device penetration.

Can patients outside Riyadh access advanced cardiac monitoring?

SEHA Virtual Hospital allows remote pacemaker checks and loop-recorder reviews, but rural areas still trail urban centers in access to AI-enabled predictive analytics.

Page last updated on: