Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

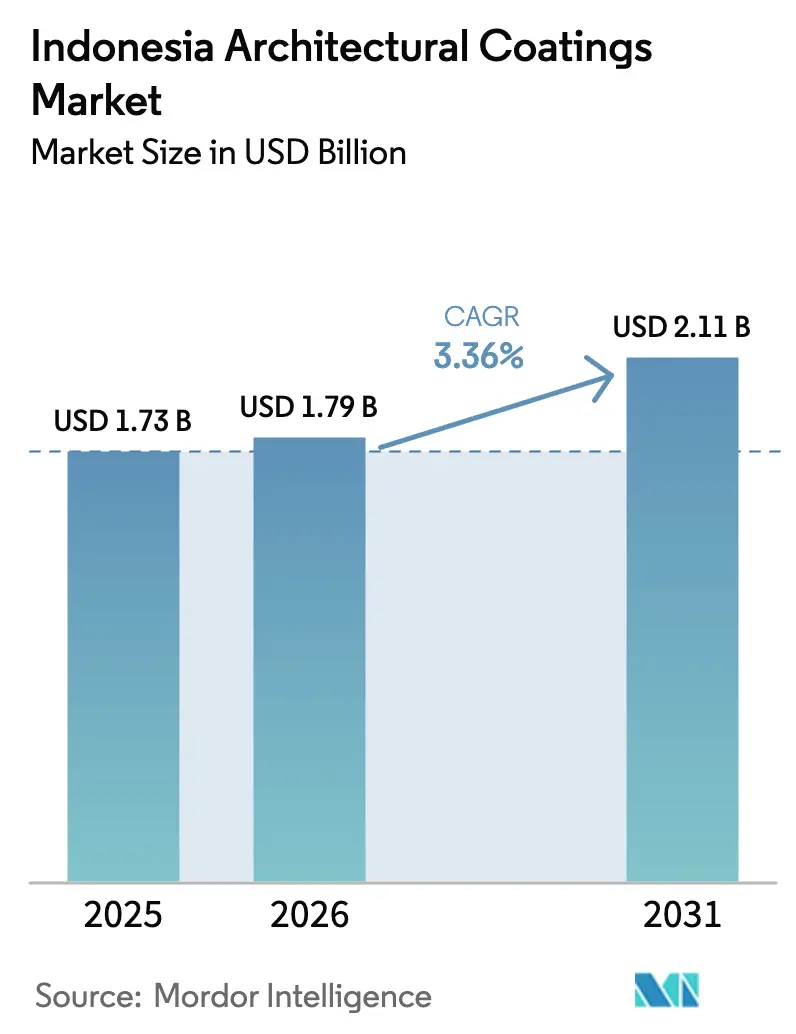

| Base Year Market Size (2025) | USD 1.73 Billion |

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.11 Billion |

| Growth Rate (2026 - 2031) | 3.36% CAGR |

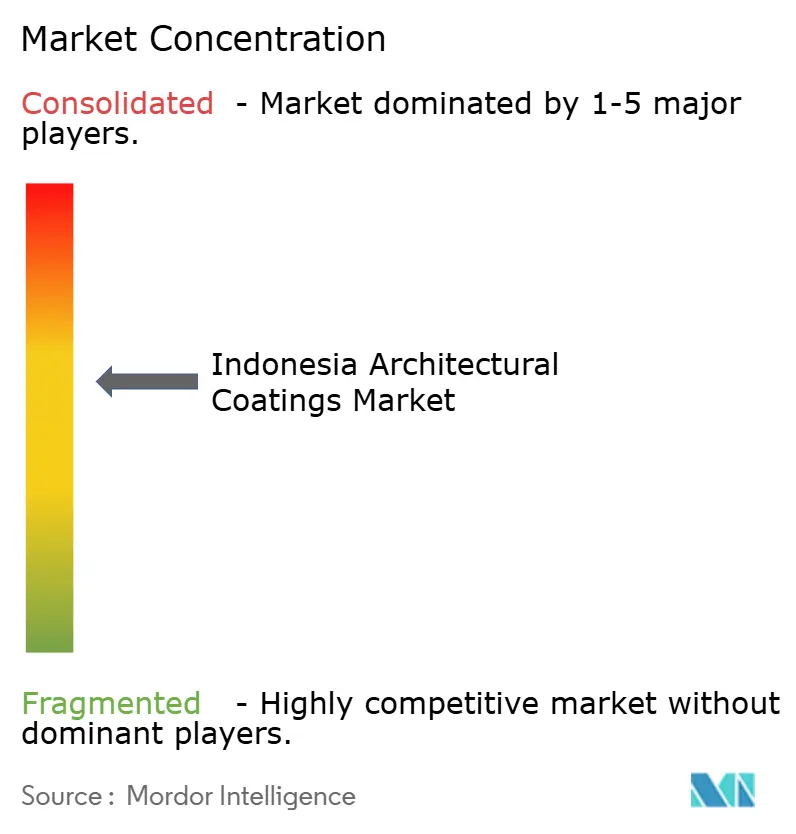

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Architectural Coatings Market Analysis by Mordor Intelligence

The Indonesia Architectural Coatings Market size is expected to grow from USD 1.73 billion in 2025 to USD 1.79 billion in 2026 and is forecast to reach USD 2.11 billion by 2031 at 3.36% CAGR over 2026-2031. The steady expansion mirrors Indonesia’s robust construction pipeline, abundant government infrastructure spending, and growing consumer preference for sustainable, low-odor water-borne products. Policy-driven social housing schemes, rising middle-class purchasing power in secondary cities, and booming e-commerce channels create new avenues for value-added sales. Meanwhile, the logistics complexity of serving 17,000 islands, titanium-dioxide cost volatility, and Thailand-Malaysia VOC benchmarks that outpace local regulations temper the rate of progress. Producers differentiate by localizing capacity, shortening delivery lead times, and scaling tinting systems that allow precise color selection while reducing inventory holdings.

Key Report Takeaways

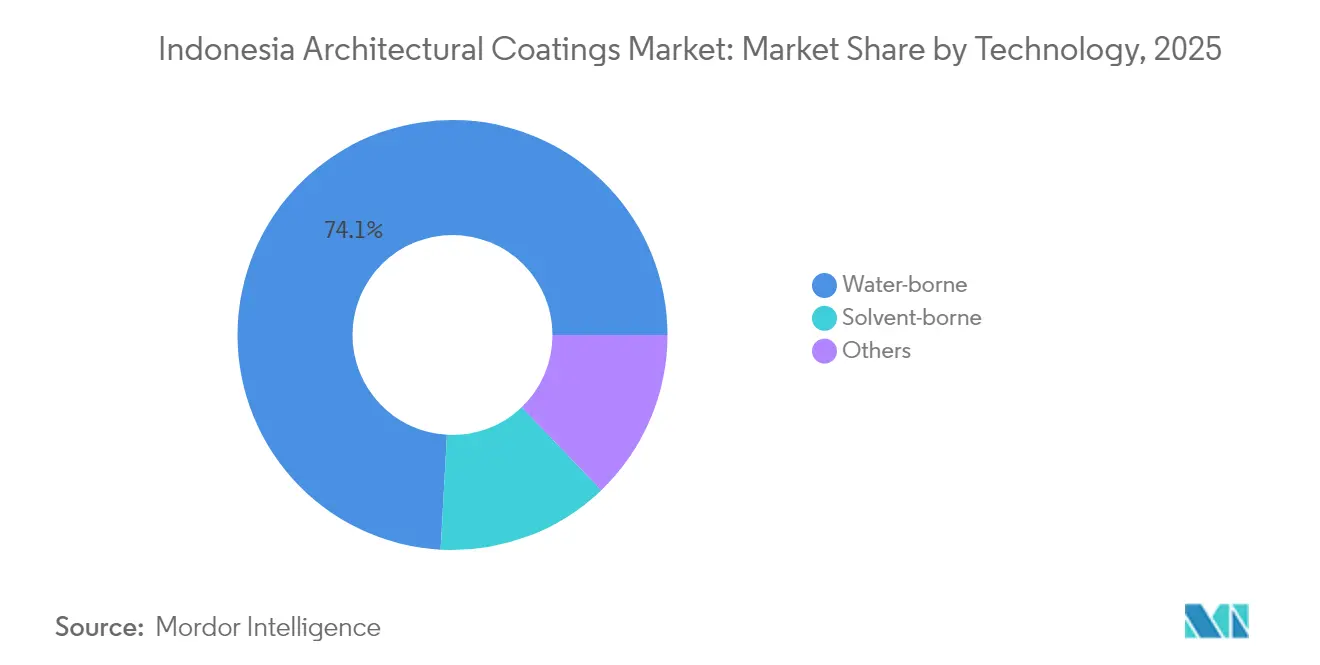

- By technology, water-borne coatings held 74.12% of Indonesia architectural coatings market share in 2025 and are advancing at a 3.79% CAGR through 2031.

- By resin, acrylic dominated with 41.68% share of the Indonesia architectural coatings market size in 2025, while polyurethane is projected to expand at 3.66% CAGR to 2031.

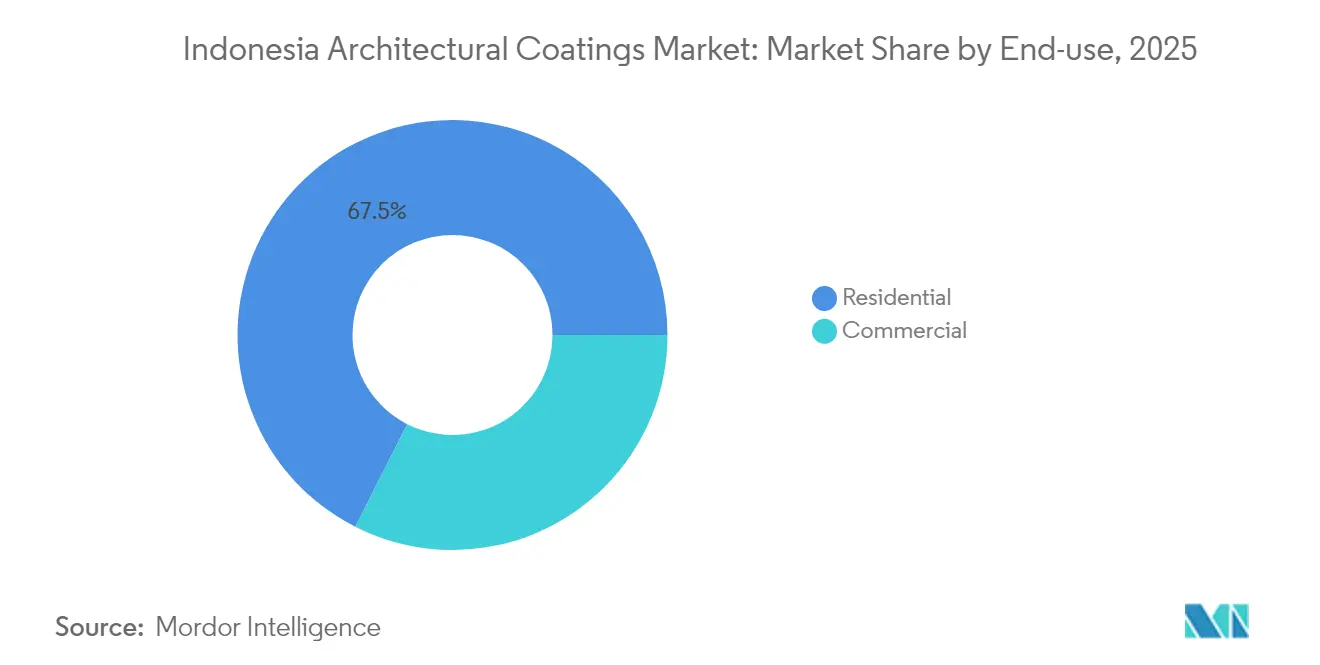

- By end-use, residential captured 67.53% revenue share in 2025; commercial registers the swiftest growth at 3.57% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led social housing push | +0.8% | National, concentrated in Java and urban centers | Medium term (2–4 years) |

| Growing disposable income in tier-2 and tier-3 cities | +0.6% | Emerging urban areas outside Jakarta | Long term (≥ 4 years) |

| Surge in e-commerce paint retailing | +0.4% | National, higher penetration in Java and Sumatra | Short term (≤ 2 years) |

| Green-building certification incentives | +0.3% | Major cities, especially Jakarta | Medium term (2–4 years) |

| Rapid hotel-resort pipeline in Bali and East Nusa Tenggara | +0.2% | Tourism-focused provinces | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-Led Social Housing Push Accelerates Volume Demand

Indonesia’s 3 million-unit annual social housing target converts sporadic project orders into multi-year framework agreements that guarantee baseline offtake for large paint producers. Housing authorities directly coordinate with suppliers, allowing factory line scheduling and just-in-time delivery that cut warehousing cost and semi-finished goods waste[1]Real Estate Indonesia (REI), “Program 3 Juta Rumah…,” rei.or.id. PT Avia Avian earmarked IDR 250–300 billion (USD 16.2 million) toward a Cirebon water-based plant to improve West Java fulfillment speed and lower freight charges into the Jakarta–Bandung corridor. Modular construction methods used in rural sites require quick-dry, scuff-resistant finishes that keep pace with accelerated assembly timetables, boosting demand for high-solids, rapid-cure acrylics. Foreign credit lines from Qatar and the UAE underpin future phases, granting order-book visibility well past domestic budget cycles.

Growing Disposable Income in Tier-2 and Tier-3 Cities Expands Premium Segments

Rising prosperity among 52 million middle-class Indonesians transforms decorative paint purchasing from functionality-driven to aesthetics-led. Consumers in Surabaya, Makassar, and Pontianak increasingly weigh cleanability, sheen retention, and odor ratings when selecting wall finishes, enabling manufacturers to retail higher-margin premium ranges that once found traction only in Jakarta malls. Nippon Paint’s tri-tier portfolio, economy, mid, prestige, achieved 26% top-of-mind brand recall after rolling out 700 tinting kiosks in provincial hardware stores. Computerized dispensers cut mismatch risk, instill confidence in color choice, and support premiumization strategies.

Surge in E-Commerce Paint Retailing Transforms Distribution Models

Online sales shave layers off the traditional wholesaler–retailer chain, letting producers ship direct from regional hubs to end users across thousands of islands. Hybrid models pair web ordering with local tinting to guarantee same-day color pick-up, as shown by PaintPro’s AI-based dispenser that replicates any shade with 100% accuracy. Digital storefronts host how-to videos, coverage calculators, and chat-based technical support that lower contractor training costs and drive brand loyalty. Water-borne SKUs benefit most because their lower hazmat classification reduces shipping paperwork and damage risk.

Green-Building Certification Incentives Drive Sustainable Product Adoption

Jakarta by-law 38/2012 compels large developments to pursue Greenship ratings, pushing specifiers toward low-VOC emulsions certified by Singapore Green Label or GBCI. Government e-catalog rules that favor listed green items protect the pricing integrity of compliant offerings. The PROPER scorecard, used in public reporting of corporate environmental performance, further motivates factories to reformulate away from aromatic solvents.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile titanium-dioxide pricing | -0.5% | Global supply impact, all Indonesian producers | Short term (≤ 2 years) |

| Slow adoption of VOC regulations vs. neighbors | -0.3% | National framework lag | Long term (≥ 4 years) |

| High logistics cost across archipelago | -0.4% | Eastern provinces and remote islands | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Slow Adoption of VOC Regulations Versus Neighbors Creates Competitive Disadvantages

Malaysia enforces 500 g/L VOC caps for interior alkyds; Singapore goes lower at 300 g/L. Indonesia retains voluntary SNI benchmarks, delaying market demand for advanced resin systems and limiting export eligibility to regulated ASEAN economies. Domestic suppliers thus walk a fine line: invest early in VOC-cutting equipment or risk obsolescence once mandatory limits arrive after 2027 public-consultation rounds.

High Logistics Costs Across Archipelago Limit Market Penetration

Liquid paint’s bulky, hazmat-classified nature inflates shipping rates that already run 22% above mainland Southeast Asian averages to reach Maluku and Papua. Producers therefore maintain micro-warehouses at secondary ports, tying up working capital and constraining SKU breadth. Local powder facilities, such as AkzoNobel’s Cikarang line, help for industrial jobs yet do little for decorative emulsions that dominate retail turnover.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Dominance Accelerates Environmental Compliance

Water-borne products controlled a 74.12% Indonesia architectural coatings market share in 2025, and the segment is projected to widen its lead at a 3.79% CAGR through 2031, outpacing the broader Indonesia architectural coatings market. That momentum stems from local humidity that slows solvent flash-off, making water-based latexes easier to apply and less odorous for occupied dwellings. Rising retailer acceptance of automated tinting ensures consistent shade reproducibility across thousands of colorants, removing one of the last barriers to mass adoption.

Solvent-borne enamels remain essential where abrasion, hydrocarbon exposure, or very low film-build temperatures exceed the functional window of acrylic emulsions. The “Others” bucket, led by powder and UV-curables, edges upward on industrial projects but still represents a single-digit slice of the Indonesia architectural coatings market size, constrained by the need for dedicated application equipment and higher upfront capex for contractors. The regulatory tilt of the B3 hazardous-substance rules nudges city projects toward water media, signaling a long-term contraction of conventional solvent lines.

By Resin Type: Polyurethane Innovation Challenges Acrylic Leadership

Acrylic maintained 41.68% of Indonesia architectural coatings market share in 2025 owing to balanced cost-performance and entrenched supply chains feeding residential wall paints. Polyurethane currently sits at a smaller base yet will clock 3.66% CAGR to 2031, double that of acrylic, as water-borne PU dispersions gain adoption for commercial floors where chemical resistance and scuff durability justify a premium. In 2025, new low-odor hybrid resins combining acrylic backbone flexibility with PU cross-link density entered the catalogues of PT Propan Raya, targeting condominium lobbies and food courts.

Alkyd retains traction in solvent gloss enamels sold through hardware channels, while epoxy systems thrive in industrial secondary containment and warehouse flooring. Polyester powders, galvanized by AkzoNobel’s domestic line, court furniture OEM coats. Novel self-cross-linking chemistries executed in pilot batches at Cikarang research and development centers signal the next wave of high-solids, moisture-cured options capable of meeting prospective VOC reductions without sacrificing throughput.

By End-Use: Commercial Growth Outpaces Residential Volume Leadership

Residential builds, fueled by state housing drives and middle-income family upgrades, formed 67.53% of total revenue in 2025, a sizeable portion of the Indonesia architectural coatings market size. Bulk supply deals to government agencies push producers toward pallet-sized drop-shipments of standard whites and pastels; mastery of fill-rate reliability confers a competitive edge.

Commercial projects such as shopping centers, office towers, and resort complexes, post 3.57% CAGR to 2031, eclipsing residential’s pace. These jobs specify multi-coat systems with anti-microbial additives or elastomeric crack-bridging layers, widening the average selling price per liter. Green-building credits further elevate the share of water-based polyurethane clear coats and epoxy-modified primers in high-traffic lobbies. Contractors’ preference for reliable color match across refurbishment cycles enhances stickiness of branded products.

Geography Analysis

Java is anchored by Jakarta’s mega-projects and the Bekasi-Cikarang industrial corridor. Concentrated consumer density and integrated toll-road networks trim outbound freight times to under 24 hours, enabling next-day deliveries that underpin aggressive promotional campaigns. West Java hosts clusters of formulation plants whose proximity to key ports curtails import duty on titanium dioxide and acrylic monomers, reinforcing Java’s supply chain advantage.

Sumatra, with its palm-oil and petrochemical hub in Riau, consumes protective coatings for tank farms and conveyor systems, thus offering cross-selling potential into architectural refurbishments of workers’ housing estates. The Medan–Tebing-Tinggi highway has also catalyzed suburban developments adopting mid-tier decorative emulsions with anti-mold claims suitable for high rainfall. Kalimantan’s IKN Nusantara government precinct orders premium low-VOC coatings to satisfy green-building targets exceeding 75% compliance, presenting early-mover gains for certified suppliers able to mobilize technical support teams on site.

Eastern archipelagos wrestle with elevated freight premiums yet enjoy rising tourist investment in Labuan Bajo, Flores, and Lombok. Hotel chains specify moisture-curing polyurethane topcoats for wooden decking and façade boards exposed to sea spray. Bali’s design-conscious clientele drives quick turnover of trend palettes, evidenced by 2025 color launches centered on warm earth tones that echo local terracotta architecture. Sulawesi’s nickel-processing boom attracts expatriate housing demand, supporting balanced retail-commercial sales volumes even as commodity price cycles influence broader regional income.

Competitive Landscape

The market is moderately fragmented. Indonesia’s supplier roster blends multinationals, AkzoNobel, Nippon Paint, Jotun, with entrenched nationals such as PT Avia Avian and PT Propan Raya. Nippon Paint leverages loyalty programs that bundle color-consulting services for developers alongside warranties extending 8–10 years, securing specification dominance in multi-tower apartment clusters. Jotun debuted an immersive Studio concept store in Karawang in February 2025, pairing AR visualizers with sample boards to accelerate selection decisions for the booming West Java corridor. New entrants eye white spaces in VOC-compliant niche lines, though barriers include B3 licensing and fragmented retail shelf space. Digital ordering, last-mile tinting, and predictive analytics for demand planning now separate leaders from mid-pack rivals.

Indonesia Architectural Coatings Industry Leaders

AkzoNobel N.V.

Jotun

Nippon Paint Holdings Co., Ltd.

Avian Brands

Mowilex

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Asian Paints completed divestment of Indonesian operations, selling 100% stakes in PT Asian Paints Indonesia and PT Asian Paints Color Indonesia to Omega Property Investments Pty Ltd, Australia.

- February 2025: Jotun Indonesia opened its first flagship store on Java in Karawang, West Java, under the Jotun Studio retail concept, with interactive color selection and consulting services.

Indonesia Architectural Coatings Market Report Scope

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.By Technology

| Water-borne |

| Solvent-borne |

| Others |

By Resin Type

| Acrylic |

| Alkyd |

| Epoxy |

| Polyester |

| Polyurethane |

| Other Resin Types |

By End-Use

| Residential |

| Commercial |

| By Technology | Water-borne |

| Solvent-borne | |

| Others | |

| By Resin Type | Acrylic |

| Alkyd | |

| Epoxy | |

| Polyester | |

| Polyurethane | |

| Other Resin Types | |

| By End-Use | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms