Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

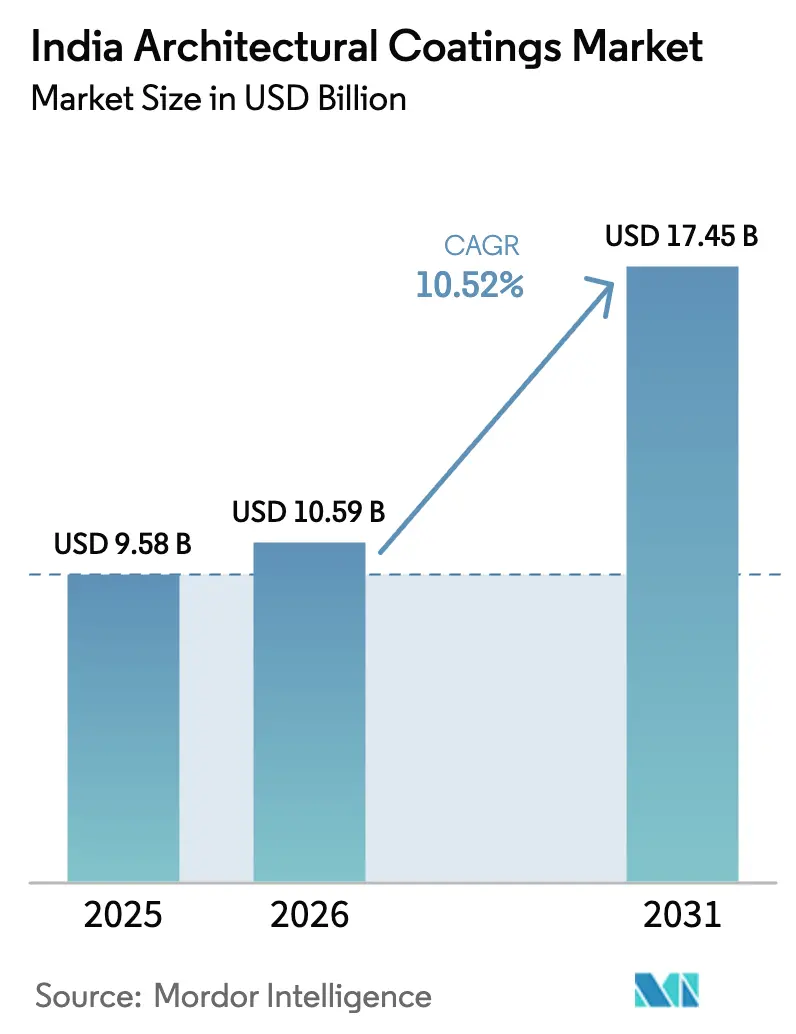

| Base Year Market Size (2025) | USD 9.58 Billion |

| Market Size (2026) | USD 10.59 Billion |

| Market Size (2031) | USD 17.45 Billion |

| Growth Rate (2026 - 2031) | 10.52% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Architectural Coatings Market Analysis by Mordor Intelligence

India Architectural Coatings Market size market size in 2026 is estimated at USD 10.59 billion, growing from 2025 value of USD 9.58 billion with 2031 projections showing USD 17.45 billion, growing at 10.52% CAGR over 2026-2031. Sustained public-sector investment, rising urban disposable incomes, and a steady shift toward environmentally compliant water-borne technologies underpin this expansion. The government’s plan to build 1.12 crore urban homes, the Smart Cities Mission’s focus on sustainable infrastructure, and rapid capacity additions by large conglomerates are together shaping long-term growth prospects. Intensifying competition is fostering wider product availability and sharper price discipline, while evolving consumer tastes are accelerating premiumisation and shortening repaint cycles across metropolitan and emerging cities. Raw-material cost swings linked to crude oil and titanium dioxide remain a notable headwind, yet backward integration and digital supply-chain tools are helping manufacturers cushion margin volatility.

Key Report Takeaways

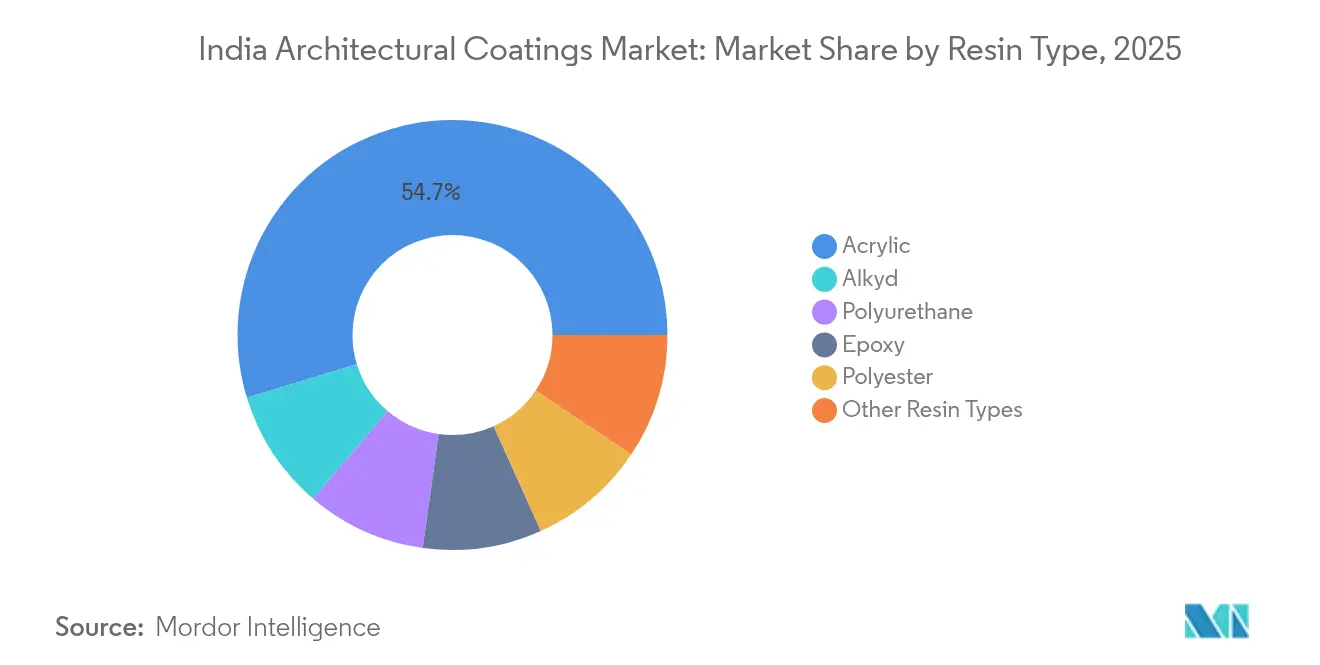

- By resin type, acrylic commanded 54.72% of the India architectural coatings market share in 2025 and is forecast to record the fastest 13.30% CAGR through 2031.

- By technology, water-borne systems held 72.05% revenue share of the India architectural coatings market size in 2025 and are set to expand at 12.04% CAGR to 2031.

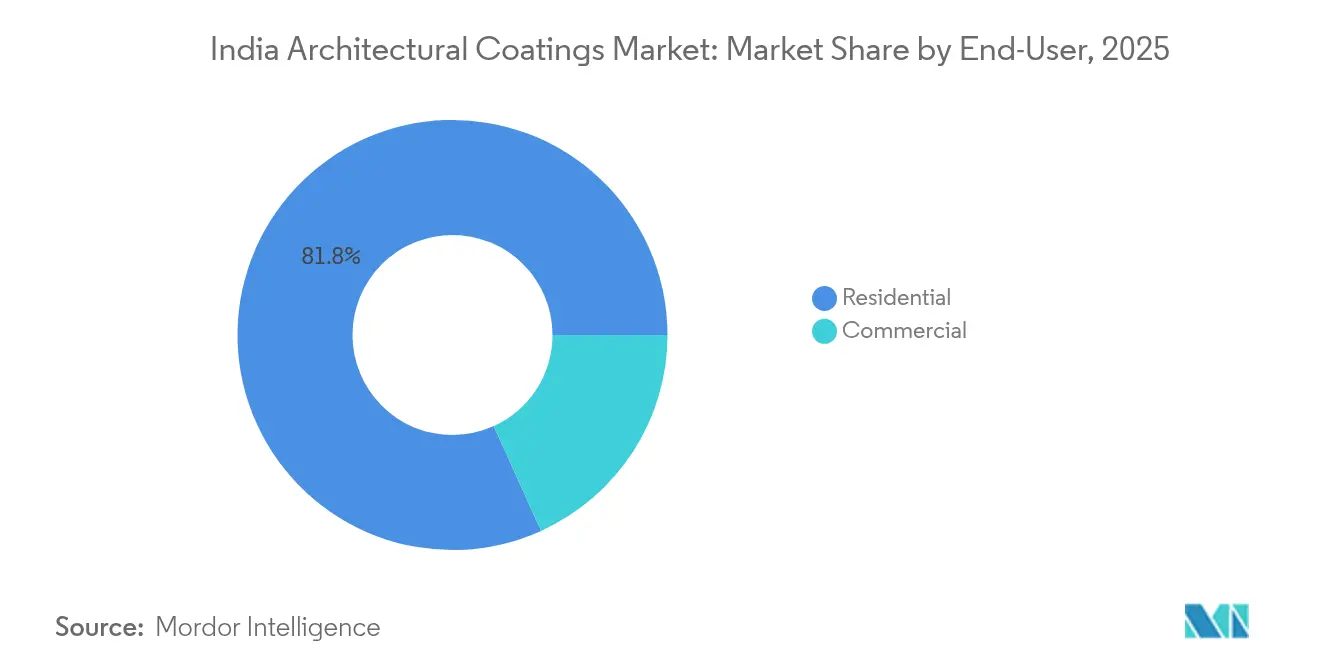

- By end-user, the residential segment accounted for 81.76% of total volume in 2025 and is advancing at an 10.98% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Architectural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government housing and infrastructure push | +2.8% | National, with concentration in Maharashtra, Gujarat, Tamil Nadu | Medium term (2-4 years) |

| Environmental regulation-driven shift to waterborne coatings | +1.9% | National, with stricter enforcement in Delhi NCR, Mumbai, Chennai | Short term (≤ 2 years) |

| Premiumisation and shorter repaint cycles | +2.1% | Urban centers, Tier-1 cities expanding to Tier-2 | Medium term (2-4 years) |

| Rapid capacity expansion and dealer-network densification | +1.7% | National, with focus on underserved rural markets | Long term (≥ 4 years) |

| Point-of-sale tinting kiosks enabling mass-custom colour | +1.4% | Urban and semi-urban markets, gradual rural penetration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Housing and Infrastructure Push

The Pradhan Mantri Awas Yojana has earmarked INR 2.17 lakh crore (USD 26.1 billion) to build 1.12 crore urban homes, creating a multi-year pipeline for exterior and interior coatings demand[1]Business Standard Bureau, “Paint firms ramp up capacity to tap housing boom,” Business Standard, business-standard.com . Complementing this is the Smart Cities Mission, which has allotted INR 2.05 lakh crore for resilient public utilities, transit hubs, and urban rejuvenation that necessitate high-durability finishes. Rural schemes such as the Pradhan Mantri Gramin Awas Yojana, targeting 2.95 crore dwellings, are widening the India architectural coatings market’s geographic footprint. Collectively, these programs ensure a consistent base-load of volume, accelerate organized-sector penetration, and support higher-value product tiers aligned with sustainable-building codes.

Environmental Regulation-Driven Shift to Water-Borne Coatings

The Central Pollution Control Board’s VOC norms and mandatory continuous emission monitoring have prompted manufacturers to adopt low-solvent chemistries[2]Central Pollution Control Board, “VOC Guidelines for Paints and Coatings,” cpcb.nic.in. Several large plants now operate with zero-liquid-discharge processes, underscoring the regulatory pivot to cleaner production. State regulators, most notably in Maharashtra, Delhi NCR, and Tamil Nadu, are conducting stricter plant audits, prompting accelerated capital expenditure (capex) in water-borne assets. Consequently, water-borne products are rising, illustrating successful big-bang compliance, rising consumer eco-awareness, and retailer preference for low-odor options.

Premiumisation and Shorter Repaint Cycles

Urban consumers are increasingly opting for antimicrobial, self-cleaning, and heat-reflective coatings, which command price premiums of 15-20% over conventional emulsions. Enhanced durability is trimming repaint intervals from a historical five-to-seven-year norm to three-to-four years in metros, fuelling recurring demand. Digital visualization apps enable owners to preview designs and colors, reinforcing their willingness to pay more for bespoke aesthetics. This upgrading trend is filtering into Tier 2 cities as household incomes grow and brand familiarity increases. Premiumisation, therefore, contributes meaningfully to revenue growth even when aggregate volumes moderate.

Rapid Capacity Expansion and Dealer-Network Densification

Grasim Industries’ 1,332 million-liter Birla Opus project represents a 40% jump in national capacity and illustrates the India architectural coatings industry’s transformation from oligopolistic to competitive. Incumbents such as Asian Paints have countered with brownfield extensions at Khandala and Kasna, while simultaneously investing in backward-integrated VAE resin plants to contain input costs. Aggressive network roll-outs—Birla targeting 50,000 outlets, Indigo Paints crossing 18,100 dealers—improve last-mile reach, which is essential for capturing rural and semi-urban demand. The scale race is therefore recalibrating pricing strategies, supply reliability, and the penetration of tinting machines.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-oil/TiO₂ price volatility | -1.8% | National, with higher impact on import-dependent manufacturers | Short term (≤ 2 years) |

| Intensifying price competition in value segment | -1.2% | National, particularly acute in rural and semi-urban markets | Medium term (2-4 years) |

| Skilled-painter labour shortages | -0.9% | National, with severe constraints in tier-2 and tier-3 cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil/TiO₂ Price Volatility

Titanium dioxide accounts for roughly 15-20% of the formulation cost, and anti-dumping duties of USD 460-681 per ton on Chinese grades have increased average TiO₂ prices for local manufacturers. Parallel fluctuations in crude-derived solvents inflate resin inputs; every USD 10 per-barrel uptick raises overall material expense by 2-3%. Larger players are hedging currency risk and investing in captive monomer plants; Asian Paints’ INR 200 crore VAE unit is a prime example. Smaller firms, lacking scale or hedging resources, face compressed margins, prompting them to engage in selective SKU rationalization and shorter credit cycles with distributors.

Skilled-Painter Labor Shortages

Approximately 2.5 million construction painters are currently active; however, urban expansion and infrastructure projects have outpaced the training pipelines. Contractors report wage inflation of 12-15% since 2024, eroding developers’ budgets and sometimes delaying projects. Shortages are most acute in Tier 2 and Tier 3 cities, where formal training centers are scarce. To bridge the gap, manufacturers are partnering with vocational institutes and launching app-based matchmaking platforms that connect certified painters to site owners. Upskilling initiatives enhance application quality, which in turn supports the uptake of premium products and reduces callbacks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Acrylic Dominance Drives Performance Standards

Acrylic resins captured 54.72% of the India architectural coatings market share in 2025, thanks to exceptional UV stability and color retention under India’s varied climate. The segment is forecast to log a 13.30% CAGR to 2031, outpacing overall market momentum. Water-borne acrylic emulsions comply readily with VOC caps, reinforcing their primacy in both mass and premium ranges. Alkyd continues to serve economy finishes where cost sensitivity is paramount, though its proportion is slipping as consumers trade up. Polyurethane coatings are gaining favor in commercial interiors needing scuff resistance, while epoxy hybrids address niche flooring and institutional needs. Research and development investments in nano-modified acrylics and silicone-acrylic blends are enhancing washability and anti-microbial features, positioning acrylics as the default choice for high-traffic zones.

Hybridizing acrylic with fluoropolymers or polysiloxanes is widening aesthetic and functional possibilities, including graffiti resistance and heat-reflective roofs. Local producers are scaling backward-integrated monomer facilities to hedge price volatility and assure quality consistency. The trend underscores how acrylic chemistry underwrites sustained innovation and margin defense across the India architectural coatings market.

By Technology: Water-Borne Solutions Reshape Environmental Compliance

Water-borne systems dominated 72.05% of the 2025 volume and are expected to advance at a 12.04% CAGR to 2031, propelled by strict VOC legislation and consumer preference for low-odor products. Superior acrylic-polyurethane hybrids achieve scrub cycles comparable to legacy solvent lines, negating performance trade-offs. Enhanced rheology modifiers have improved flow and leveling, enabling smoother finishes that appeal to premium buyers. As a result, the India architectural coatings market size attached to water-borne products is widening faster than solvent-borne counterparts. Solvent-borne demand persists in metal truss work and high-humidity zones where moisture-tolerant curing is vital, yet its share is receding annually.

Manufacturers are debottlenecking water-based reactors and scaling dispersant capacity to keep pace with demand. Equipment upgrades like stainless-steel vessels and advanced vent-scrubbing curb emissions further, aligning with the Ministry of Environment’s Orange-category mandates. Market education initiatives emphasize health and indoor-air-quality benefits, accelerating mainstream acceptance across both organized retail and project channels.

By End-User: Residential Segment Drives Market Expansion

Residential demand generated 81.76% of 2025 sales and is forecast to rise at a 10.98% CAGR through 2031. Shorter repaint cycles in metros, government-funded housing pipelines, and aspirational home-improvement media are pivotal to this outperformance. Builders are increasingly specifying branded paints for warranty compliance, thereby broadening the size of the India architectural coatings market addressed by organized players. Commercial real-estate projects, though forming a smaller slice, offer higher margins due to stringent aesthetics and durability benchmarks. Smart-city business parks and co-working hubs require advanced acoustic and anti-fungal coatings, expanding the scope for high-specification portfolios.

Institutional buyers—such as hospitals, schools, and government offices—demand antimicrobial, low-odor products to meet hygiene standards. This cohort values vendor reliability and post-sales technical support, favoring firms with strong technical service teams. The residential ascent in tier-2 and tier-3 zones hinges on the spread of dealer networks, the penetration of tinting machines, and aggressive influencer marketing aimed at painters and contractors.

Geography Analysis

Maharashtra and Gujarat anchor the western region’s leadership, accounting for the largest slice of the India architectural coatings market, thanks to their dense urban centers and sizable industrial bases. Sustained housing startups in Mumbai and Pune, as well as industrial corridors such as the Delhi-Mumbai Industrial Corridor, bolster volume. Southern states, including Tamil Nadu, Karnataka, Andhra Pradesh, and Kerala, are expanding at the fastest rate, driven by growth in the technology sector and urban infrastructure upgrades in Bengaluru, Chennai, and Hyderabad. Strict municipal bylaws mandating heat-reflective terrace coats in Chennai’s new buildings are nudging the adoption of specialty finishes.

Northern markets, including Delhi NCR, Punjab, and Haryana, benefit from central government infrastructure allocation and a rigorously enforced anti-pollution regime that accelerates waterborne sales. Delhi’s shift to low-VOC coatings has become a bellwether that other metros are emulating. Eastern states, particularly West Bengal and Odisha, are emerging as the next frontier as ports, steel plants, and logistics hubs spur auxiliary residential and commercial activity. Tier-2 cities, such as Coimbatore, Surat, Lucknow, and Bhubaneswar, exhibit rising repaint frequencies, aligned with growing disposable income and lifestyle aspirations. Distribution depth, rather than primary demand, is the primary gating factor across hinterlands. Rural markets remain largely under-penetrated but represent sizeable latent demand as housing schemes proliferate; success will depend on sachet-sized SKUs, value pricing, and local painter engagement programs.

Competitive Landscape

Technology is defining competitive edges. Automated tinting kiosks reduce inventory and expedite color delivery, while augmented-reality apps enable customers to visualize outcomes, thereby increasing conversion rates. Partnerships with fintechs are enabling BNPL (buy now, pay later) schemes that make premium offerings affordable to middle-income households. Product differentiation is concentrating on functional coatings—anti-viral, low-temperature curing, and solar-reflective variants—where patentable chemistries underpin pricing power. Distribution reach remains king; players are vying to secure painter loyalty through on-site training, loyalty points, and referral bonuses. As dealer density rises, service quality and turnaround times become tie-breakers. Consolidation among mid-tier firms could gather pace if prolonged discounting compresses profitability, potentially redrawing the competitive map by 2030.

India Architectural Coatings Industry Leaders

Asian Paints

Berger Paints India

Kansai Nerolac Paints Limited

AkzoNobel India Ltd

Grasim Industries Limited (Aditya Birla Group)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Asian Paints committed EUR 217 million for a 400 million-liter greenfield plant in Indore to expand its water-based capacity and support sustainable, low-VOC production.

- February 2025: Berger Paints announced an INR 2,000 crore program spanning new facilities in Odisha and Andhra Pradesh, which will add 32,000 metric tons of monthly output to its path toward achieving INR 20,000 crore in revenue by 2030.

India Architectural Coatings Market Report Scope

Commercial, Residential are covered as segments by Sub End User. Solventborne, Waterborne are covered as segments by Technology. Acrylic, Alkyd, Epoxy, Polyester, Polyurethane are covered as segments by Resin.By Resin Type

| Acrylic |

| Alkyd |

| Polyurethane |

| Epoxy |

| Polyester |

| Other Resin Types |

By Technology

| Water-borne |

| Solvent-borne |

By End-User

| Residential |

| Commercial |

| By Resin Type | Acrylic |

| Alkyd | |

| Polyurethane | |

| Epoxy | |

| Polyester | |

| Other Resin Types | |

| By Technology | Water-borne |

| Solvent-borne | |

| By End-User | Residential |

| Commercial |

Market Definition

- COMMERCIAL - The Commercial Sector includes the paints and coatings used for hotels, hospitals, educational institutions, government institutions and malls among others. The scope does not include paints and coatings used for infrastructure applications.

- RESIDENTIAL - This section includes interior and exterior paints and coatings used on residential buildings.

- FLOOR AREA - The total floor area comprises of both existing and new floor area for the sub end users considered in the study.

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific end-user segment and country are selected from a group of relevant variables & factors based on the desk research & literature review; along with primary expert inputs.

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms