Spices, Dry Mixes And Extracts Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

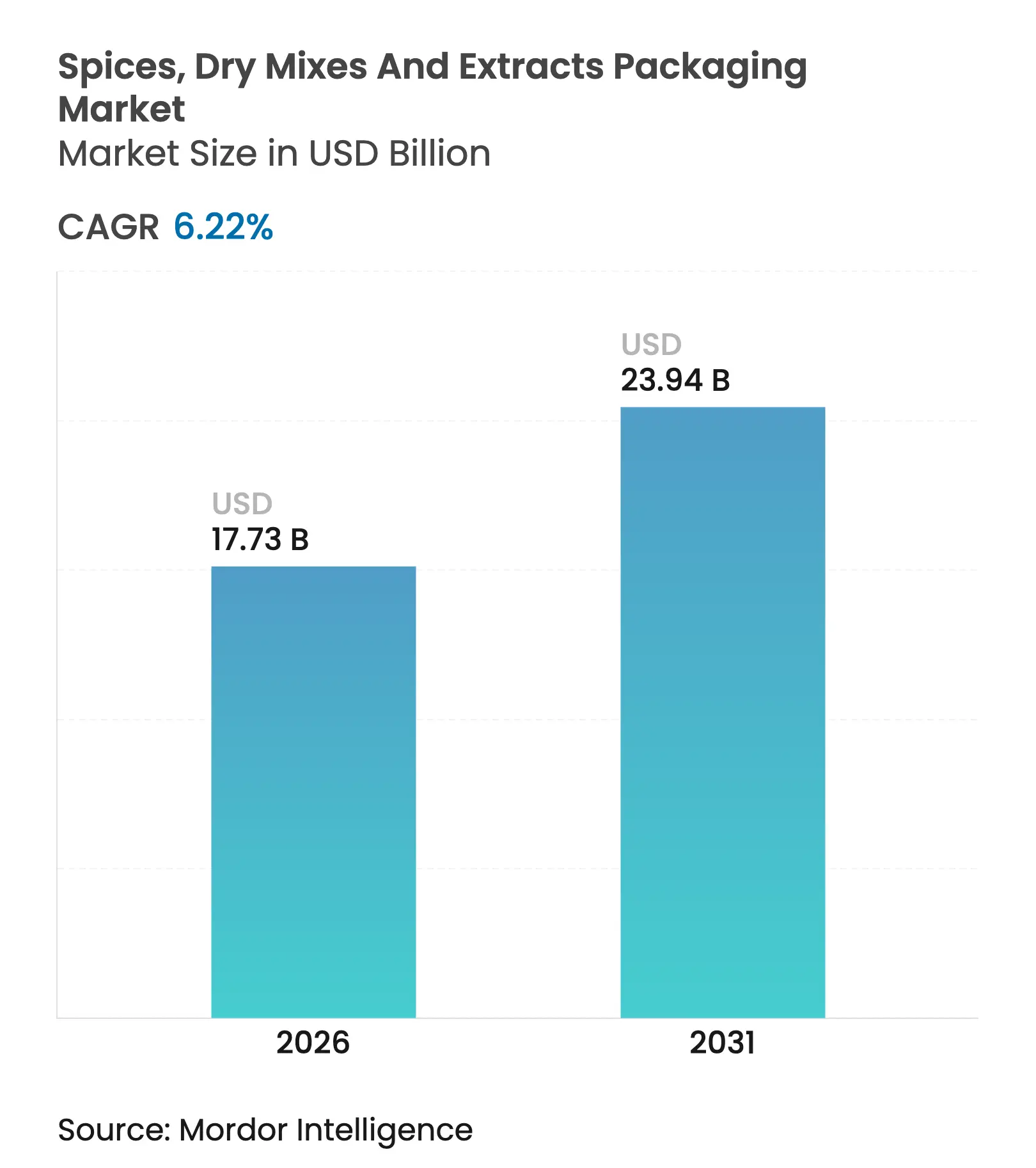

| Market Size (2026) | USD 17.73 Billion |

| Market Size (2031) | USD 23.94 Billion |

| Growth Rate (2026 - 2031) | 6.22 % CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Spices, Dry Mixes And Extracts Packaging Market Analysis by Mordor Intelligence

The global spices, dry mixes, and extracts packaging market size in 2026 is estimated at USD 17.73 billion, growing from 2025 value of USD 16.69 billion with 2031 projections showing USD 23.94 billion, growing at 6.22% CAGR over 2026-2031. This growth outlook highlights the rising preference for single-serve packs, surging e-commerce penetration, and a decisive shift toward sustainable, high-barrier materials that satisfy stringent food-contact rules. Intensifying urbanization in emerging economies, combined with advances in barrier material science, is extending shelf life and aligning with food safety mandates. Supply-chain digitalization boosts traceability, while automation across filling lines reduces waste and raises throughput in cost-sensitive regions. The upturn also reflects demographic changes that increase per-capita spice consumption and encourage portion-controlled formats, which are optimized for online retail logistics. Competitive intensity is moderate: large converters leverage scale efficiencies in film manufacturing, whereas regional players capitalize on proximity to spice-growing hubs and lower labor costs. Resin price volatility remains a headwind; however, converters that pivot to recyclable or compostable structures can secure premium contracts under extended producer responsibility legislation.

Key Report Takeaways

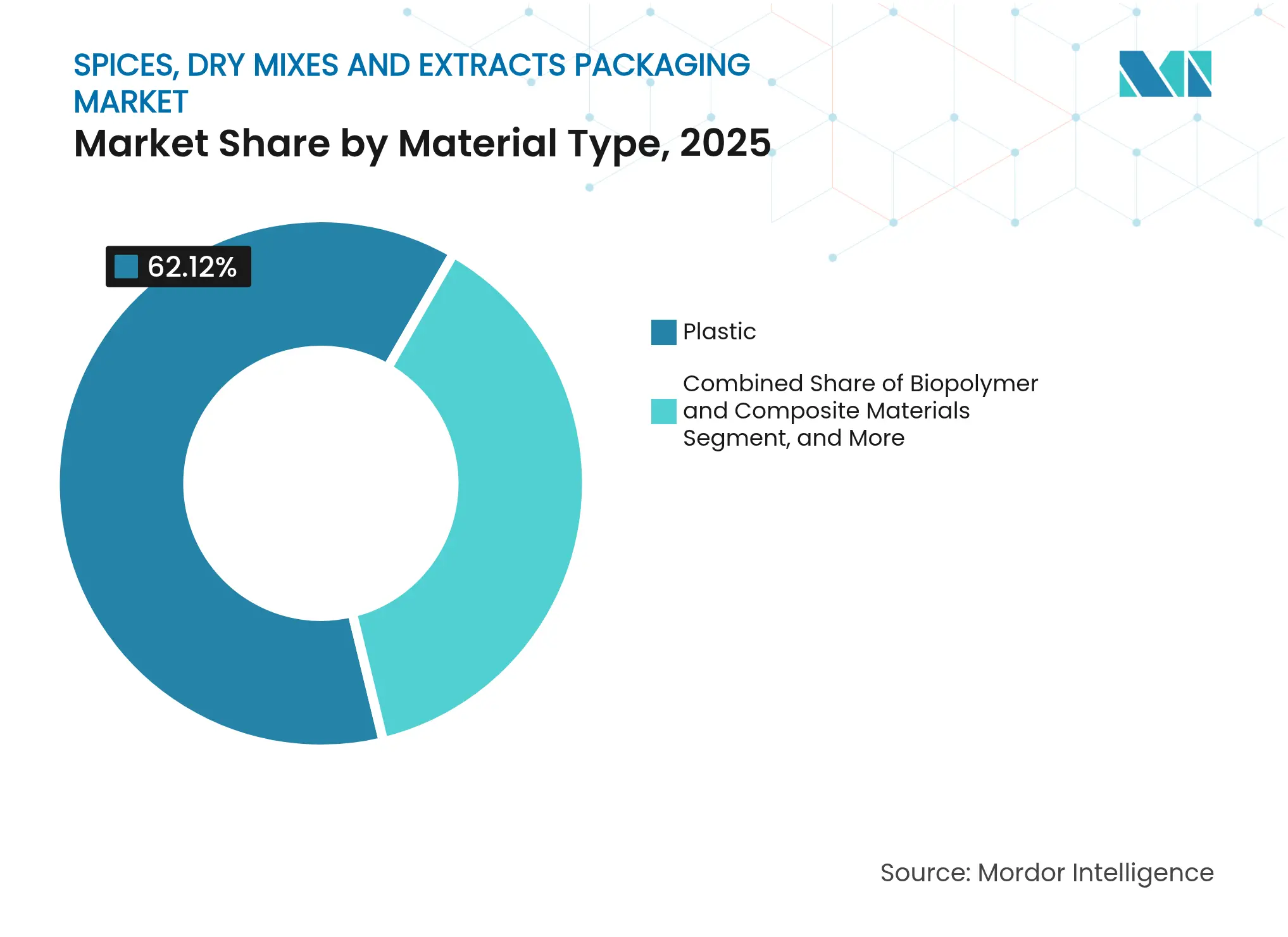

- By material type, plastic held 62.12% of the spices, dry mixes, and extracts packaging market share in 2025, while biopolymer and composite materials are projected to post the fastest 6.92% CAGR through 2031.

- By packaging type, flexible formats captured a 52.05% revenue share in 2025; rigid formats are expected to trail, as flexible solutions are projected to expand at a 6.74% CAGR through 2031.

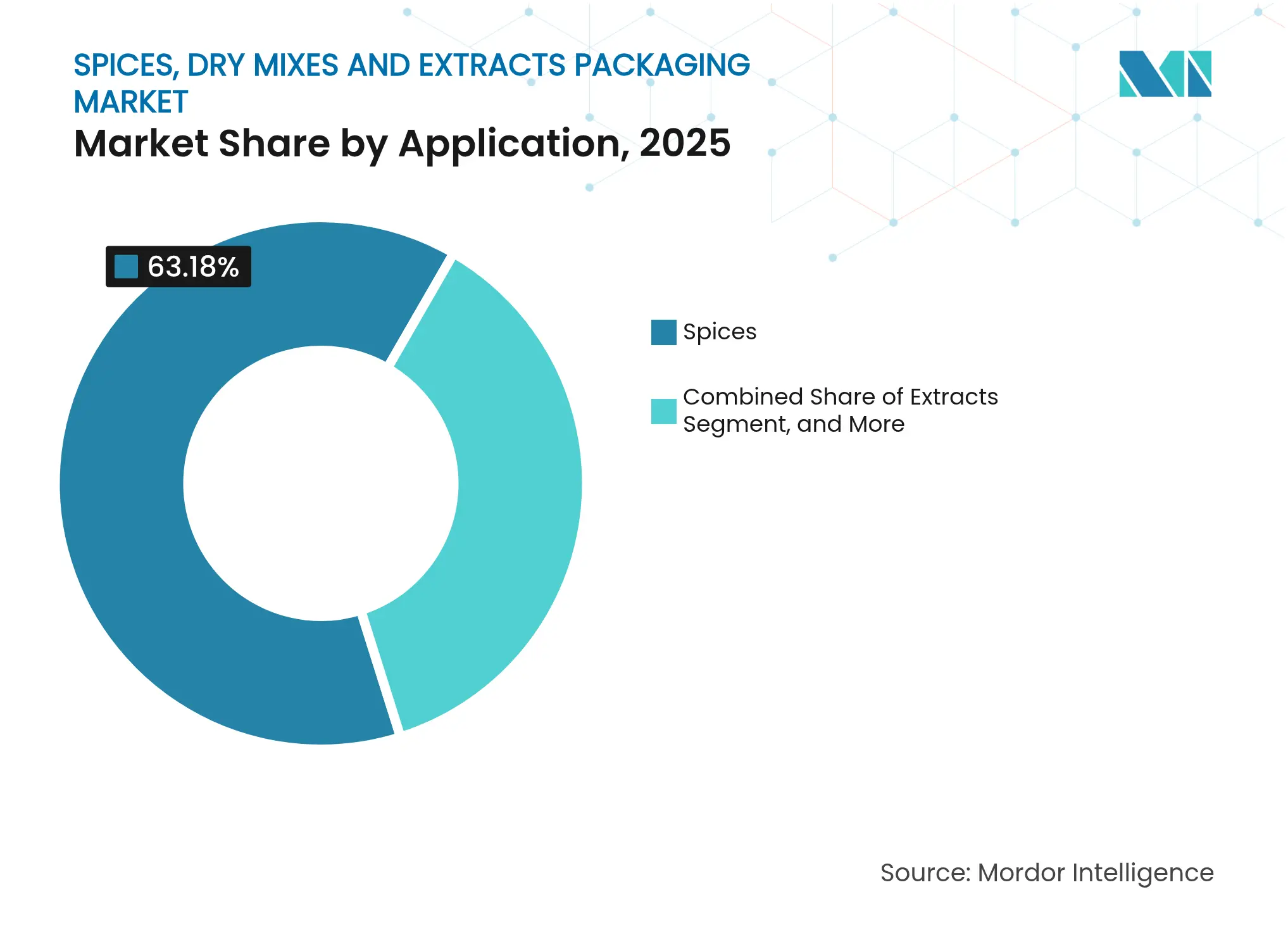

- By application, spices accounted for 63.18% of the spices, dry mixes, and extracts packaging market size in 2025; extracts are expected to grow the fastest at 8.15% CAGR between 2026 and 2031.

- By product type, bags and pouches led with 38.05% share in 2025, whereas bottles and jars are forecast to register the highest 7.32% CAGR from 2025 to 2031.

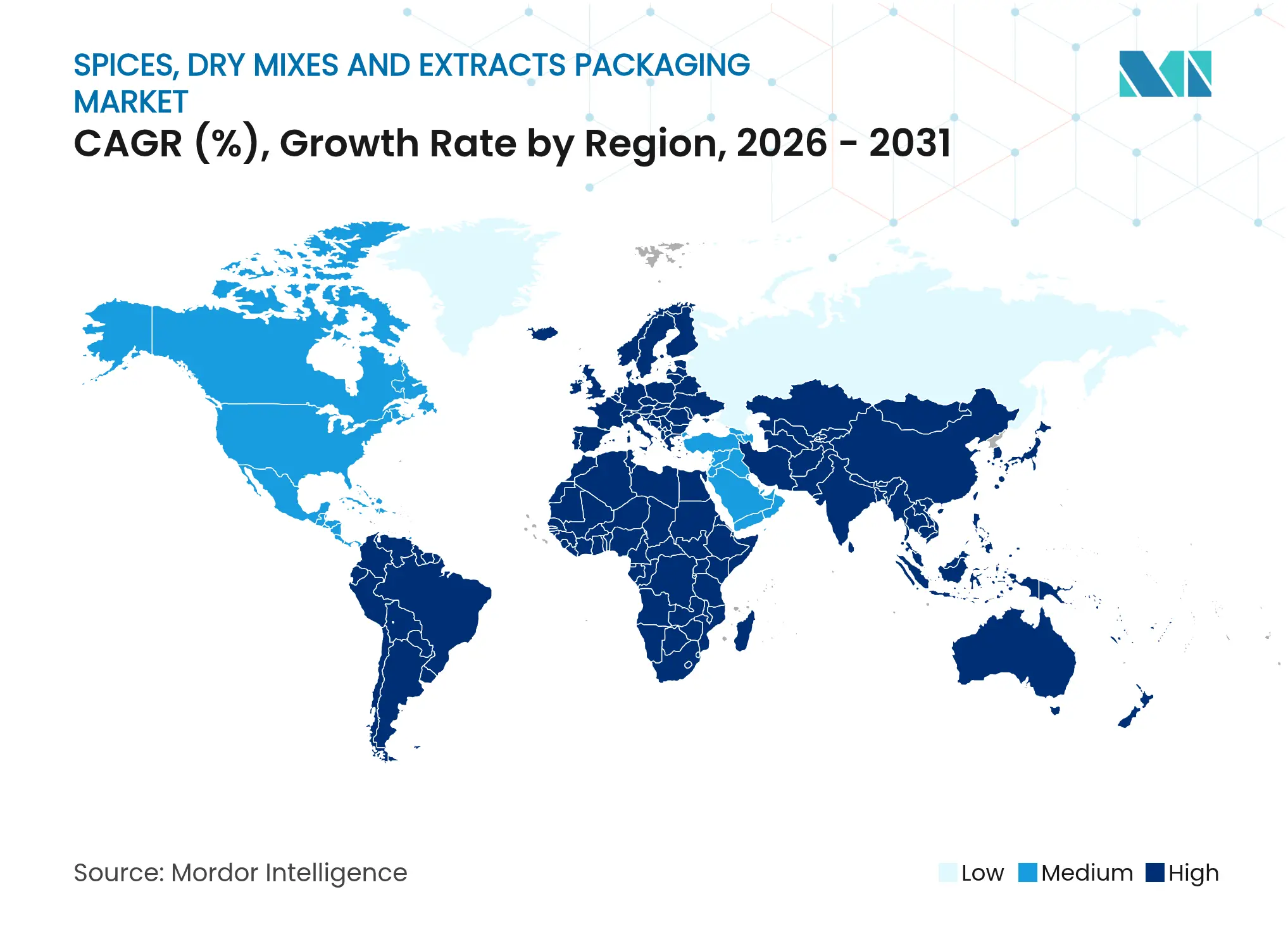

- By geography, Asia-Pacific region commanded a 40.18% revenue share in 2025 and is predicted to expand at a robust 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spices, Dry Mixes And Extracts Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Consumer Preference for Convenient Single-Serve Flexible Packs Rising Consumer Preference for Convenient Single-Serve Flexible Packs | +1.1% | Global, strongest in North America and urban Asia-Pacific | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.1% | Geographic Relevance:Global, strongest in North America and urban Asia-Pacific | Impact Timeline:Medium term (2-4 years) |

Adoption of High-Barrier Sustainable Materials in Dry Spice Formats Adoption of High-Barrier Sustainable Materials in Dry Spice Formats | +0.8% | Europe and North America leading, expanding to Asia-Pacific | Long term (≥ 4 years) | |||

Rapid Expansion of E-commerce and eB2B Fulfilment for Seasonings Rapid Expansion of E-commerce and eB2B Fulfilment for Seasonings | +1.2% | Global, highest in Asia-Pacific and North America | Short term (≤ 2 years) | |||

Automation of Powder Filling Lines in Emerging Markets Automation of Powder Filling Lines in Emerging Markets | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) | |||

Growth of Organically Certified Spice Mixes Requiring Traceable Packaging Growth of Organically Certified Spice Mixes Requiring Traceable Packaging | +0.7% | North America and Europe, expanding to premium Asia-Pacific | Long term (≥ 4 years) | |||

Government Extended-Producer-Responsibility Mandates on Food Packs Government Extended-Producer-Responsibility Mandates on Food Packs | +0.6% | Europe leading, expanding to North America and select Asia-Pacific | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Consumer Preference for Convenient Single-Serve Flexible Packs

Portion-controlled sachets cater to modern lifestyles, characterized by smaller households and on-the-go consumption. The format supports e-commerce economics because lighter packs lower shipping fees and minimize breakage. Updated European guidelines on portion control add regulatory momentum, while advanced barrier films now keep aroma and color stable for longer storage periods. Integrated QR codes enable direct consumer engagement and lot-level traceability, turning packaging into a data-rich marketing channel.[1]European Food Safety Authority, “Packaging and Food Contact Materials,” efsa.europa.eu

Adoption of High-Barrier Sustainable Materials in Dry Spice Formats

Bio-based polyethylene, compostable laminates, and water-borne barrier coatings now match oxygen-transmission performance of multi-layer plastics, allowing converters to meet both carbon-reduction goals and shelf-life requirements. Major food brands mandate these materials, absorbing the 20-30% price premium in exchange for demonstrable sustainability metrics. European carbon-credit schemes offset some cost and accelerate scale-up of production facilities scheduled to come online during 2026-2027.

Rapid Expansion of E-commerce and eB2B Fulfilment for Seasonings

Direct-to-consumer channels demand tamper-evidence, moisture control, and impact resistance to withstand multiple transit nodes. Packaging engineers incorporate shock-absorbing layers and smart sensors that track temperature and humidity, protecting volatile oils and validating freshness upon delivery. For foodservice, bulk pouches with ergonomically placed handles and resealable zippers improve kitchen efficiency. These functional upgrades elevate unit economics for spice producers selling online. [2]U.S. Department of Commerce, “E-commerce Market Analysis,” commerce.gov

Automation of Powder Filling Lines in Emerging Markets

Artificial-intelligence-driven fillers now reach 0.5% fill-weight accuracy at speeds above 200 packs per minute, closing the quality gap between low-cost producers and global incumbents. Automation reduces labor-related variability, enabling compliance with export market traceability rules. Government subsidies for modern equipment in India and Vietnam further propel the adoption of packaging compatible with high-speed lines, locking in demand. [3]International Trade Administration, “Manufacturing Automation in Emerging Markets,” trade.gov

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatile Polymer Resin Prices Compressing Converter Margins Volatile Polymer Resin Prices Compressing Converter Margins | -0.9% | Global, highest in Asia-Pacific and North America | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.9% | Geographic Relevance:Global, highest in Asia-Pacific and North America | Impact Timeline:Short term (≤ 2 years) |

Limited Recycling Infrastructure for Multi-Layer Sachets in Asia Limited Recycling Infrastructure for Multi-Layer Sachets in Asia | -0.5% | Asia-Pacific core, secondary effects in Middle East and Africa | Medium term (2-4 years) | |||

Stringent Global Migration Limits on Recycled Plastics in Food Contact Stringent Global Migration Limits on Recycled Plastics in Food Contact | -0.4% | Global, strictest in Europe and North America | Long term (≥ 4 years) | |||

Supply-Chain Disruptions in Barrier Film Feedstocks Supply-Chain Disruptions in Barrier Film Feedstocks | -0.3% | Global, highest vulnerability in import-dependent regions | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Volatile Polymer Resin Prices Compressing Converter Margins

Polyethylene and polypropylene prices swung 25-40% within a single year, compressing converter margins by up to 20%. Long-term contracts with fixed pricing prevent frequent pass-through to food brands, leaving smaller converters financially exposed. This pressure accelerates consolidation as firms seek scale advantages and hedging sophistication.

Limited Recycling Infrastructure for Multi-Layer Sachets in Asia

Most sachets combine PET, PE, and aluminum, making them incompatible with existing mechanical recycling lines. In the absence of viable take-back programs, regulators are considering restrictions on non-recyclable formats. Converters must either invest in chemical recycling or redesign their products into mono-material films that meet the evolving waste-management rules across high-growth Asian markets.

Segment Analysis

By Material Type: Plastic Dominance Faces Sustainable Disruption

Plastic retained 62.12% share of the spices, dry mixes, and extracts packaging market in 2025 because of unmatched barrier characteristics and supply-chain familiarity. Yet the biopolymer and composite segment is growing at 6.92% CAGR, underpinned by brand commitments to carbon neutrality and mandates such as the European Single-Use Plastics Directive. Early adopters benefit from carbon-credit incentives that help narrow the cost gap. Paper-based formats serve niche organic brands where compostability takes precedence over barrier performance, while metal and glass remain in premium gift assortments.

The transition toward sustainable materials also drives R&D in hybrid structures that combine plant fibers with bio-based coatings, delivering oxygen-transmission rates of less than 1 cc/m²/day without the need for aluminum layers. These hybrids can be integrated into existing paper waste streams, thereby sidestepping the hurdles of multi-layer recycling. However, limited global production capacity suppresses near-term volumes, keeping fossil-based films prevalent in high-speed, cost-sensitive applications. As new plants reach scale by 2027, cost parity is likely to occur, reshaping the procurement strategies of leading spice brands.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Type: Flexible Formats Drive Market Evolution

Flexible packs held 52.05% share and are projected to expand faster than rigid formats, as lighter weight lowers freight costs and automated lines favor roll-stock input. Reclosable zippers and slider tops now preserve barrier integrity after opening, addressing past convenience gaps. Mono-material flexible structures enhance recyclability and align with emerging extended producer responsibility fees.

Rigid bottles and jars continue to hold a strong presence on shelves in specialty channels. Glass, enhanced with lightweighting technology, reduces breakage risk while maintaining premium cues. PP jars containing 30% post-consumer resin meet recycled-content quotas in Europe and parts of North America. Nonetheless, the flexible segment’s 6.74% CAGR indicates brand migration toward variants that balance cost, convenience, and sustainability.

By Application: Spices Lead While Extracts Surge

Spices dominated with 63.18% share, reflecting the volume nature of whole, ground, and blended products across both retail and foodservice. Extracts, although smaller, will grow at an 8.15% CAGR as food manufacturers and home cooks seek concentrated flavor solutions. Extract packaging demands light-blocking layers and high oxygen barriers to protect volatile oils, leading to the adoption of aluminum-free laminates with nano-coatings that achieve comparable opacity.

Dry mixes capitalize on consumer desire for time-saving meal prep. Flow-agent formulations allow larger stand-up pouches that pour evenly, reducing clumping in humid climates. Smart labels that reveal hydration ratios or recipe suggestions elevate perceived value. Across all applications, IoT-enabled freshness indicators are initially introduced on extract products due to their higher price points and quality sensitivity.

Note: Segment shares of all individual segments available upon report purchase

By Product Type: Traditional Formats Face Innovation Pressure

Bags and pouches retained their leadership position at 38.05% share, underpinned by low material costs and versatility. Innovations such as laser-scored easy-tear openings and corner spouts improve functionality. Bottles and jars, projected at 7.32% CAGR, ride the premiumization wave and consumer inclination toward reusable containers. Lightweight glass achieves a 15% reduction in freight emissions compared to legacy formats, helping retailers meet their carbon targets.

Cartons serve institutional clients needing stackable, moisture-resistant packaging for bulk spices. New barrier coatings extend shelf life without foil, making recycling easier. Canisters with resealable lids are ideal for gift assortments and premium blends. Across formats, QR codes that guide users to origin videos build trust and differentiate commodity spices in crowded online marketplaces.

Geography Analysis

Asia-Pacific accounted for 40.18% of the global spices, dry mixes and extracts packaging market in 2025 and is accelerating at a 7.55% CAGR. Urbanization, rising middle-class incomes, and local access to raw spices spur regional demand. Governments in India and Indonesia have initiated modernization grants for automated packaging lines, enhancing export competitiveness. Yet recycling infrastructure lags, pushing brands toward mono-material solutions that satisfy prospective collection mandates.

North America shows steady demand as consumers trade up to organic and traceable spice variants. Brands integrate post-consumer resin to comply with state recycled-content laws, and e-commerce drives adoption of shatter-proof pouches that reduce shipping claims. Europe leads sustainability innovation, incentivizing compostable films through carbon-credit systems and enforcing strict migration limits, stimulating material science partnerships among converters.

South America, the Middle East and Africa post growing consumption as diversified diets introduce global cuisines. Limited cold-chain logistics heighten the need for barrier-rich packaging to preserve flavor integrity during long transit times. Foreign direct investment in regional packaging plants aims to shorten lead times and comply with country-of-origin labeling. Together, these geographies present future upside once regulatory landscapes stabilize and waste-management capacities improve.

Competitive Landscape

Market Concentration

The spices, dry mixes, and extracts packaging market is moderately concentrated. Top multinational converters exploit technology scale and global distribution, while regional firms compete on responsiveness and proximity to spice-growing basins. Scale players deploy artificial intelligence-enabled defect detection systems to ensure film uniformity and reduce scrap rates. Automation investments also hedge against labor cost escalation in low-cost regions.

Sustainability differentiation drives mergers and partnerships focused on bio-based polymers and chemical recycling. Intellectual property filings related to plant-derived barrier coatings increased sharply through 2024, with leading firms securing patents that secure material exclusivity. White-space opportunities emerge in blockchain-enabled traceability, where packaging data is integrated into supplier audits for organic certification. Service offerings, such as design-for-e-commerce and regulatory consulting, further blur the traditional boundaries between film suppliers and value-added partners.

Spices, Dry Mixes And Extracts Packaging Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Amcor announced a USD 150 million investment in sustainable packaging technology development focusing on compostable barrier films for food applications.

- September 2024: Mondi completed the USD 85 million acquisition of an Indian flexible-packaging converter, expanding its spices footprint in Asia-Pacific.

- August 2024: Sealed Air Corporation launched the ProActive line featuring integrated freshness sensors for premium spice and extract packs.

- July 2024: Huhtamaki formed a joint venture with a Japanese technology company to develop QR-enabled smart packaging for Asian food markets.

Table of Contents for Spices, Dry Mixes And Extracts Packaging Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Consumer Preference for Convenient Single-Serve Flexible Packs

- 4.2.2Adoption of High-Barrier Sustainable Materials in Dry Spice Formats

- 4.2.3Rapid Expansion of E-commerce and eB2B Fulfilment for Seasonings

- 4.2.4Automation of Powder Filling Lines in Emerging Markets

- 4.2.5Growth of Organically Certified Spice Mixes Requiring Traceable Packaging

- 4.2.6Government Extended-Producer-Responsibility Mandates on Food Packs

- 4.3Market Restraints

- 4.3.1Volatile Polymer Resin Prices Compressing Converter Margins

- 4.3.2Limited Recycling Infrastructure for Multi-Layer Sachets in Asia

- 4.3.3Stringent Global Migration Limits on Recycled Plastics in Food Contact

- 4.3.4Supply-Chain Disruptions in Barrier Film Feedstocks

- 4.4Industry Value Chain Analysis

- 4.5Impact of Macroeconomic Factors on the Market

- 4.6Regulatory Landscape

- 4.7Technological Outlook

- 4.8Porter's Five Forces Analysis

- 4.8.1Bargaining Power of Suppliers

- 4.8.2Bargaining Power of Buyers

- 4.8.3Threat of New Entrants

- 4.8.4Threat of Substitutes

- 4.8.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Material Type

- 5.1.1Plastic

- 5.1.2Paper

- 5.1.3Glass

- 5.1.4Metal

- 5.1.5Biopolymer and Composite Materials

- 5.2By Packaging Type

- 5.2.1Flexible

- 5.2.2Rigid

- 5.3By Application

- 5.3.1Spices

- 5.3.2Dry Mixes

- 5.3.3Extracts

- 5.4By Product Type

- 5.4.1Bags and Pouches

- 5.4.2Bottles and Jars

- 5.4.3Cartons and Boxes

- 5.4.4Canisters and Can

- 5.4.5Other Product Types

- 5.5By Geography

- 5.5.1North America

- 5.5.1.1United States

- 5.5.1.2Canada

- 5.5.1.3Mexico

- 5.5.2South America

- 5.5.2.1Brazil

- 5.5.2.2Argentina

- 5.5.2.3Rest of South America

- 5.5.3Europe

- 5.5.3.1United Kingdom

- 5.5.3.2Germany

- 5.5.3.3France

- 5.5.3.4Spain

- 5.5.3.5Italy

- 5.5.3.6Rest of Europe

- 5.5.4Asia-Pacific

- 5.5.4.1China

- 5.5.4.2India

- 5.5.4.3Japan

- 5.5.4.4Australia

- 5.5.4.5South Korea

- 5.5.4.6Rest of Asia-Pacific

- 5.5.5Middle East and Africa

- 5.5.5.1Middle East

- 5.5.5.1.1Saudi Arabia

- 5.5.5.1.2United Arab Emirates

- 5.5.5.1.3Turkey

- 5.5.5.1.4Rest of Middle East

- 5.5.5.2Africa

- 5.5.5.2.1South Africa

- 5.5.5.2.2Kenya

- 5.5.5.2.3Rest of Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products AND Services, and Recent Developments)

- 6.4.1Amcor Plc

- 6.4.2Mondi Plc

- 6.4.3Sealed Air Corporation

- 6.4.4Sonoco Products Company

- 6.4.5Constantia Flexibles GmbH

- 6.4.6Huhtamaki Oyj

- 6.4.7Winpak Ltd.

- 6.4.8Coveris Holding SA

- 6.4.9Uflex Ltd.

- 6.4.10International Paper Company

- 6.4.11Tetra Pak International SA

- 6.4.12Smurfit WestRock

- 6.4.13ProAmpac Holdings LLC

- 6.4.14Printpack Inc.

- 6.4.15Eagle Flexible Packaging

- 6.4.16Uniflex Packaging LLC

- 6.4.17O F Packaging Pty Ltd

- 6.4.18Glenroy Inc.

- 6.4.19Paharpur 3P

- 6.4.20Silgan Holdings Inc.

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1White-Space and Unmet-Need Assessment

Global Spices, Dry Mixes And Extracts Packaging Market Report Scope

Spices are available in whole, ground, and paste forms in consumer and bulk packages. Most traditional packaging materials used in the past, such as paper packaging, tinplate packaging, jute bags, etc., are being replaced by plastic packaging materials. Plastic packaging materials are preferred because they are lightweight, easy to access, compatible, hygienic, machineable, printable, heat sealable, and have selective barrier properties.

The market is segmented by material type (plastic, paper), type of packaging (flexible, rigid), product (bottles and jars, pouches and bags, boxes and cartons, canisters, and other products), end user (restaurant, household, other end-user industries), and geography (North America, Asia-Pacific, Europe, Middle East, and Africa). The report offers market forecasts and size in value (USD) for all the above segments.