Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

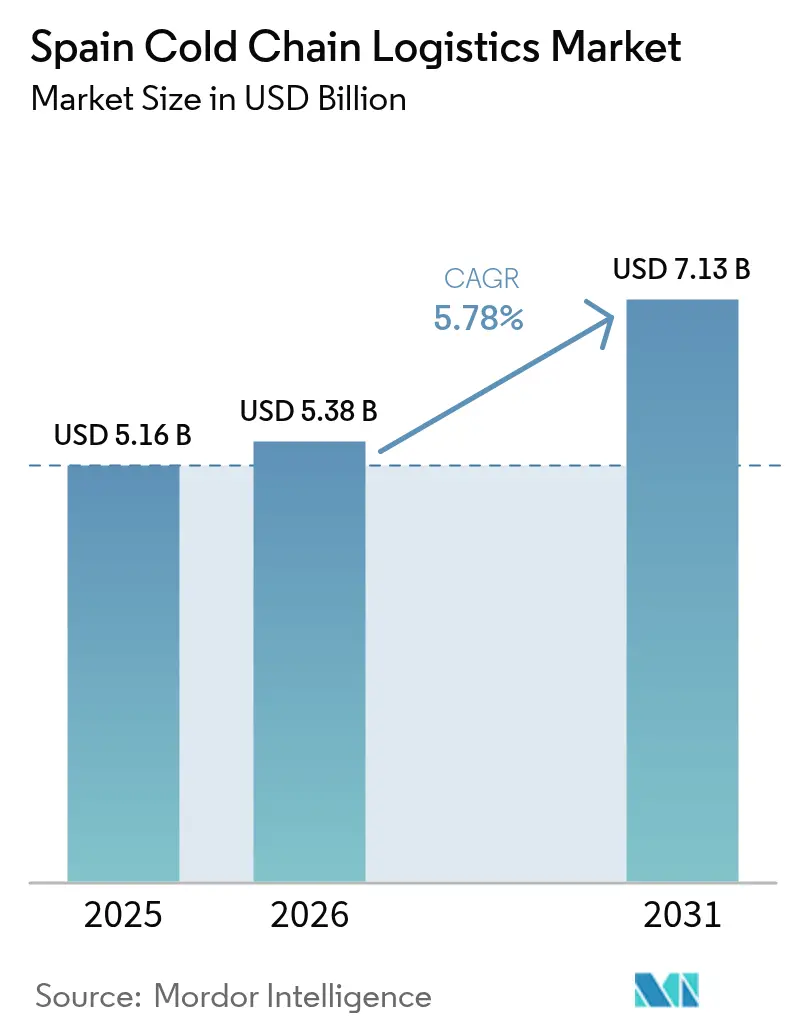

| Base Year Market Size (2025) | USD 5.16 Billion |

| Market Size (2026) | USD 5.38 Billion |

| Market Size (2031) | USD 7.13 Billion |

| Growth Rate (2026 - 2031) | 5.78% CAGR |

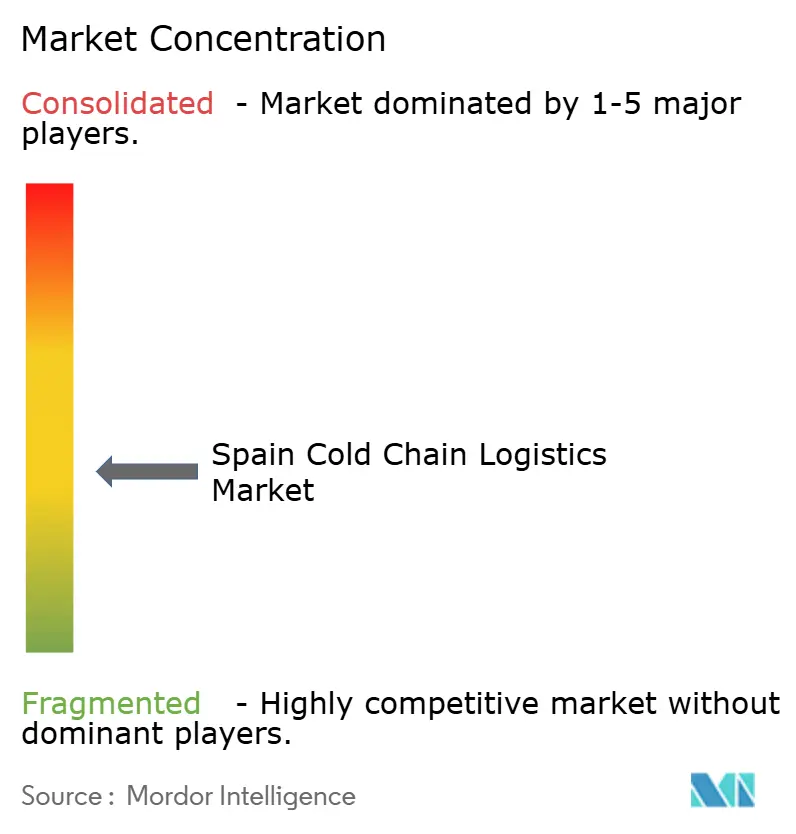

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Cold Chain Logistics Market Analysis by Mordor Intelligence

The Spain cold chain logistics market size is expected to grow from USD 5.16 billion in 2025 to USD 5.38 billion in 2026 and is forecast to reach USD 7.13 billion by 2031 at 5.78% CAGR over 2026-2031.

The expansion is propelled by rising demand for frozen convenience foods, export growth to Northern Europe, and the pharmaceutical sector’s shift to gene and cell therapies that require ultra-low-temperature handling. Retailer ESG traceability mandates encourage nationwide deployment of IoT sensors that document temperature and location in real time, while European green-hydrogen incentives support investment in low-carbon refrigeration that cuts both emissions and electricity costs. Deep-sea reefer corridors linking Spanish ports with Italy and France reduce road congestion and align with EU sustainability goals, while domestic supermarket chains continue their network expansion, intensifying demand for temperature-controlled urban warehousing. Against this backdrop, operators contend with diesel price volatility, accelerated F-gas phase-down costs, seasonal labour shortages, and periodic port congestion, which compress margins and require continuous investment in automation, alternative fuels, and workforce development.

Key Report Takeaways

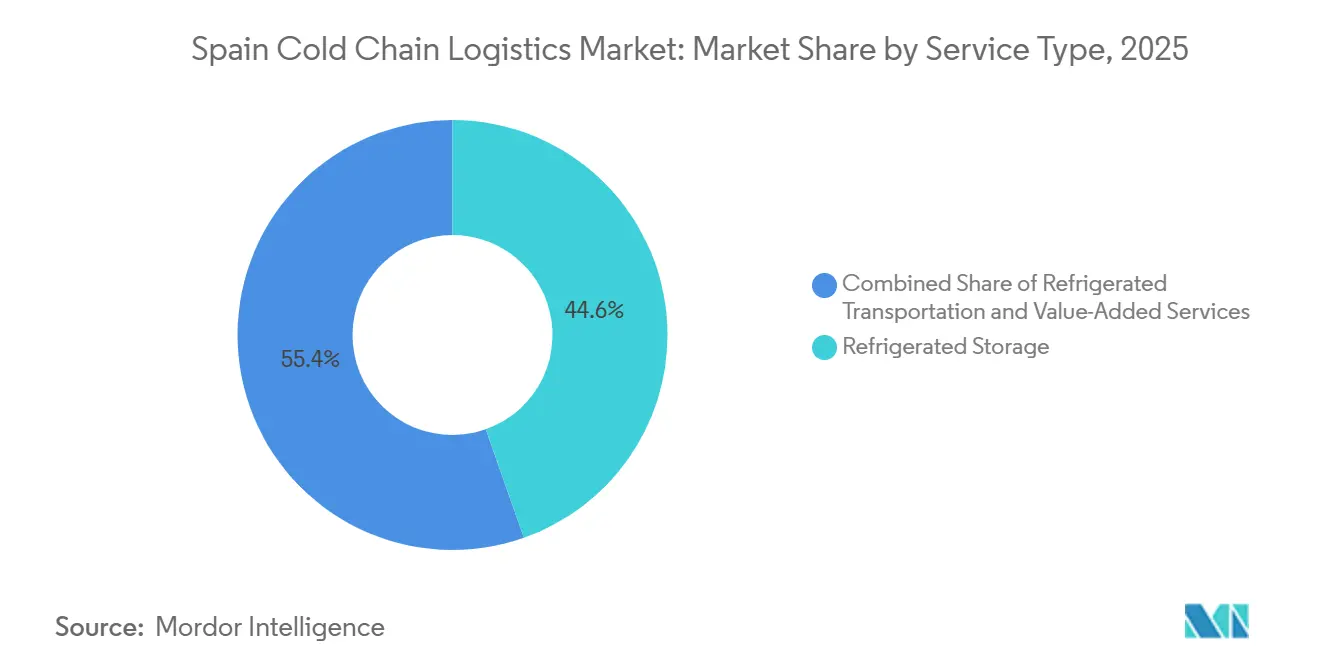

- By service type, refrigerated storage held 44.6% of the Spain cold chain logistics market share in 2025, while value-added services advance at a 7.7% CAGR to 2031.

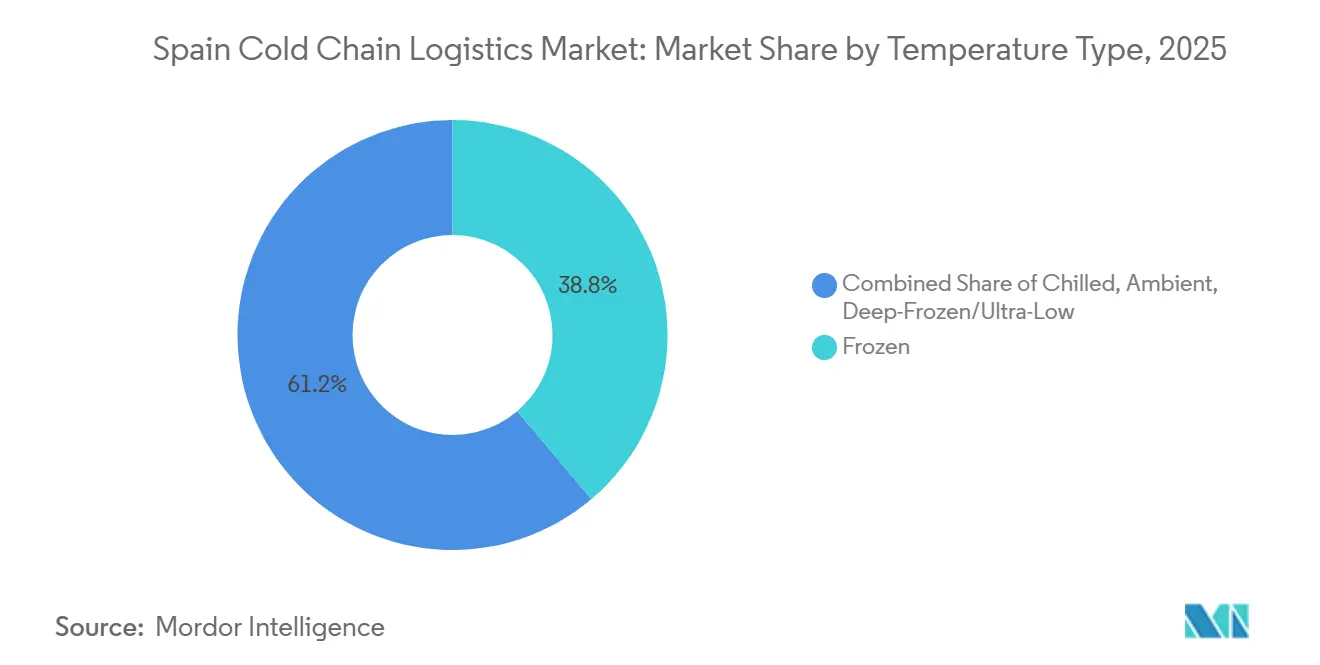

- By temperature type, frozen applications commanded 38.8% share of the Spain cold chain logistics market size in 2025, and the chilled segment is forecast to expand at a 7.13% CAGR through 2031.

- By application, meat and poultry accounted for a 21.5% share of the Spain cold chain logistics market size in 2025, whereas pharmaceuticals and biologics recorded the highest projected CAGR at 8.06% over 2026-2031.

- By region, Andalusia led with 21.7 of % Spain cold chain logistics market share in 2025; the Valencia region is poised to grow fastest at a 6.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Cold Chain Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in frozen ready-meal consumption | +0.9% | Madrid, Barcelona, Valencia | Short term (≤ 2 years) |

| Double-digit growth in agri-food exports to Northern EU | +1.2% | Andalusia, Murcia, Valencia corridors | Medium term (2-4 years) |

| Retailer ESG traceability mandates boosting IoT adoption | +0.7% | National, early adoption in Catalonia | Short term (≤ 2 years) |

| EU green-hydrogen incentives powering low-carbon refrigeration | +0.5% | Barcelona, Valencia, Seville industrial zones | Long term (≥ 4 years) |

| Gene-therapy import boom demanding –80 °C logistics | +0.6% | Madrid, Barcelona, pharma hubs | Medium term (2-4 years) |

| Mediterranean short-sea reefer ferry corridors expansion | +0.4% | Valencia, Barcelona, and Tarragona coasts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Frozen Ready-Meal Consumption

Spanish dual-income households and an aging population increasingly prefer frozen ready meals that reduce cooking time and curb food waste. Frozen aisle floor space in new supermarkets rose 25% during Q1 2025, requiring daily replenishment supported by reliable urban cold storage and last-mile distribution. Logistics providers that pair 18 °C storage with rapid order-picking services enjoy premium contracts, while IoT monitoring helps them maintain product integrity during final-mile drops.

Double-Digit Growth in Agri-Food Exports to Northern EU

Spain’s EUR 69.6 billion (USD 75.9 billion) agrifood export sector achieved 3% volume and 5.9% value growth in H1 2024, led by fruits, vegetables, and premium seafood bound for Germany, the Netherlands, and Belgium. Infrastructure upgrades worth EUR 150 million (USD 163.5 million) on the Mediterranean Corridor shorten rail transit to Rotterdam and Hamburg, supporting higher-frequency intermodal reefer services that command reliable -2 °C to 5 °C conditions. Exporters favor providers holding GDP certification and multi-country labeling skills, amplifying demand for value-added services that document origin and cold chain history.

Retailer ESG Traceability Mandates Boosting IoT Adoption

From 2025, supermarket groups will be required to provide end-to-end temperature and location data to comply with the Corporate Sustainability Reporting Directive. Spanish logistics firms, therefore, install sensor platforms that track pallets from farm gate to store cooler, creating audit trails that satisfy both food-safety and carbon-footprint disclosures[1]European Commission, “Corporate sustainability reporting,” finance.ec.europa.eu . Operators with cloud dashboards gain an edge in tenders, while smaller fleets lacking digital funding risk exclusion from national procurement rosters.

EU Green-Hydrogen Incentives Powering Low-Carbon Refrigeration

Spain targets 4 GW of electrolyzer capacity by 2030 and directs grants covering up to 40% of equipment costs for hydrogen-powered industrial systems[2]ACCIONA, “ACCIONA Energía to build one of Spain's largest green hydrogen plants,” acciona.com . Large cold stores in Barcelona free-trade zones pilot fuel-cell generators that cut Scope 1 emissions and bypass costly F-gas retrofits. Early adopters build resilience against future carbon taxation and attract multinational tenants that commit to science-based targets, despite higher upfront investment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Diesel-price volatility is squeezing reefer trucking margins | –0.6% | National haulage corridors | Short term (≤ 2 years) |

| Accelerated F-gas phase-down forcing legacy system retirements | –0.5% | Older industrial zones nationwide | Medium term (2-4 years) |

| Seasonal labor gaps in cross-dock & pick-pack operations | –0.3% | Andalusia, Murcia, Valencia harvest peaks | Short term (≤ 2 years) |

| Peak-season port congestion at Valencia is hindering export flows | –0.2% | Valencia port complex | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Diesel-Price Volatility Squeezing Reefer Trucking Margins

Fuel accounts for up to 35% of refrigerated haulage costs, making it the single most volatile expense for many operators. During 2024–2025, sharp and unpredictable swings in retail diesel prices squeezed margins, particularly for small fleets that lack the financial buffers or contractual leverage of larger operators. In many cases, fuel surcharge mechanisms written into transport contracts lagged behind real-time price changes, meaning carriers absorbed the short-term spikes themselves. This created cash-flow pressure and forced some operators to make difficult trade-offs, such as delaying maintenance, reducing route flexibility, or renegotiating delivery schedules with clients.

Accelerated F-Gas Phase-Down Forcing Legacy System Retirements

EU Regulation 2024/573 advances HFC quotas 40% below prior roadmaps, elevating refrigerant prices and pushing cold stores toward natural alternatives. A mid-capacity retrofit can cost EUR 1 million (USD 1.18 million), straining family-owned warehouses in Andalusia and Catalonia [3]. Consolidation is expected as investors acquire non-compliant sites and finance ammonia or CO₂ upgrades. In the short term, operators face operational disruption during retrofits and higher financing needs, while in the longer term, the transition is likely to accelerate modernization of Europe’s cold storage infrastructure and improve energy efficiency across the sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Value-Added Services Capture Premium Margins

Refrigerated storage captured 44.6% of the Spain cold chain logistics market share in 2025 as nationwide capacity exceeded 3.5 million m³. However, Value-added services are forecast to outpace the overall Spain cold chain logistics market at a 7.7% CAGR through 2031 by bundling quality inspection, cross-docking, and multi-language labeling, thereby shortening lead times for exporters. Operators integrate public and private warehousing, automated pallet‐shuttles, and IoT tracking to enhance throughput and justify premium fees.

Demand rises for consolidated contracts covering storage, road-rail drayage, and documentation support, especially among agrifood exporters targeting German and Dutch retail chains. Diesel cost volatility compresses line-haul margins, encouraging fleets to partner with rail providers on 600 km-plus routes where locomotive haul reduces per-unit emissions and shields against fossil-fuel surcharges.

By Temperature Type: Chilled Segment Gains Pharmaceutical Momentum

Frozen applications accounted for 38.8% of the Spain cold chain logistics market size in 2025, driven by meat, seafood, and frozen bakery distribution. The chilled 0 °C-5 °C band will grow faster, at a 7.13% CAGR, fueled by vaccine and biologic logistics plus year-round produce exports. Energy-efficient multi-zone warehouses segregate frozen and chilled rooms, cutting power consumption by 12% compared with single-temperature buildings.

IoT probes in pharmaceutical consignments trigger alerts within 60 seconds of any deviation, helping limit spoilage claims. Deep-frozen -80 °C space remains scarce outside Madrid and Barcelona, yet gene-therapy import volumes justify new facilities charging three- to four-times standard pallet rates. Operators pursue ISO 23412 certification to reassure drug sponsors of the integrity of the chain of custody.

By Application: Pharmaceutical Biologics Command Growth Premium

Meat and poultry retained a 21.5% share of the Spain cold chain logistics market size in 2025, but pharmaceuticals and biologics posted the strongest 8.06% CAGR as therapy pipelines mature. Retail frozen ready meals, ice cream, and plant-based meat analogs bolster frozen demand, while fresh berries and leafy vegetables support chilled flows.

Ready-to-eat meals expand with urban dark-kitchen suppliers requiring twice-daily -18 °C replenishment. Fish and seafood logistics increasingly employ super–freezing at -30 °C to preserve sashimi-grade tuna bound for Japan. Vaccine and clinical-trial material lanes grow by double digits, requiring dedicated GDP-approved loading docks and redundant monitoring.

Geography Analysis

Andalusia delivered a 21.7% share in Spain cold chain logistics market size in 2025 on the back of citrus and strawberry exports routed through Algeciras. Valencia Region will post the fastest 6.34% CAGR, as EUR 150 million (USD 176.7 million) in Mediterranean Corridor rail enhancements slash transit times to Lyon and Rotterdam by 90 minutes. Barcelona benefits from cross-border flows to France and Germany, while Madrid hosts inland distribution centers that link coastal ports with central consumption areas. Galicia and the Basque Country specialize in seafood and industrial food manufacturing, respectively, each attracting targeted cold storage upgrades to support export niches. Regional policy packages now pair port dredging with tax incentives for adjacent logistics parks to attract foreign direct investment and modernize legacy facilities.

Central Spain leverages Guadalajara-Marchamalo dry-port rail links that open in 2025, cutting Valencia-to-Madrid trucking by 37% and freeing coastal highway capacity[4]Autoridad Portuaria de Tarragona, “Terminal Guadalajara-Marchamalo,” porttarragona. cat . Madrid’s pharma cluster demands stringent GDP compliance, which supports investments in redundant cooling and backup power.

Northwest Galicia remains the seafood gateway, moving 210,000 t of frozen fish through Vigo in 2025 with super-chilling to -30 °C on board. Andalusia dominates horticultural exports, with Huelva and Almeria producing strawberries and tomatoes shipped to Germany under chilled conditions within 48 hours. Murcia’s produce surge squeezes trucking capacity every spring, spurring seasonal charters of rail reefers. Basque Country manufacturers of prepared meals and refrigerated sauces now access EU-funded Y-Vasca rail tunnels, expected to carry 40% of regional freight by 2030.

Competitive Landscape

The Spain cold chain logistics market hosts roughly 250 active operators. The top five, including Lineage Logistics, STEF, DHL, Primafrio, and Carreras Grupo, account for an estimated 48% of combined revenue, signaling moderate concentration. Lineage operates nine Spanish sites after its Grupo Fuentes acquisition, leveraging global scale to standardize WMS and sustainability reporting.

STEF invests EUR 40 million (USD 47.1 million) annually in Iberian automation to speed cross-dock throughput. DHL earmarks EUR 2 billion (USD 2.37 billion) for EMEA health-logistics expansion, adding -80 °C chambers in Madrid and Barcelona. Domestic fleets such as Primafrio pioneer Volvo FH Electric tractors, branding low-carbon haulage to secure supermarket contracts.

Technology disruptors like Exotec install Skypod robots in six Spanish warehouses, shrinking order cycle time by 50% and raising picking accuracy above 99.7%. Capital-intensive F-gas retrofits and hydrogen pilots are expected to accelerate mergers as small depots seek scale or exit.

Spain Cold Chain Logistics Industry Leaders

Primafrio

STEF Iberia

Lineage Logistics Spain

DHL Supply Chain Spain

Carreras Grupo Logístico

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DHL Group announced a major expansion of its Airfreight Cold Chain Network with dedicated pharma capacity and Boeing 777 freighter service connecting Europe to the United States.

- January 2026: Primafrio opened a new logistics centre in Lleida (Vilapark Industrial Estate) with 15,000 m² space, including a refrigerated warehouse for cross-docking, groupage, and consolidation of temperature-sensitive goods.

- January 2026: ID Logistics began construction of a multiclient cold logistics platform in Telde (Gran Canaria) with roughly 13,000 m², including specific space for refrigerated and pharmaceutical storage. This reinforces geographical coverage in the Canary Islands and enhances proximity to shipping and air connections.

- December 2025: ID Logistics Iberia placed the first stone on a new 80,000 m² logistics campus in Pulsar Logistics Park, Tortola de Henares, near Guadalajara. This strategic expansion will support multiclient cold chain operations.

Spain Cold Chain Logistics Market Report Scope

By Service Type

| Refrigerated Storage | |

| Refrigerated Transportation | Road |

| Rail | |

| Sea | |

| Air | |

| Value-Added Services |

By Temperature Type

| Chilled (0-5 °C) |

| Frozen (-18-0 °C) |

| Ambient |

| Deep-Frozen / Ultra-Low (less than-20 °C) |

By Application

| Fruits and Vegetables |

| Meat and Poultry |

| Fish and Seafood |

| Dairy and Frozen Desserts |

| Bakery and Confectionery |

| Ready-to-Eat Meals |

| Pharmaceuticals and Biologics |

| Vaccines and Clinical Trial Materials |

| Chemicals and Specialty Materials |

| Other Perishables |

By Region

| Andalusia |

| Catalonia |

| Valencia Region |

| Madrid and Central Spain |

| Others |

| By Service Type | Refrigerated Storage | |

| Refrigerated Transportation | Road | |

| Rail | ||

| Sea | ||

| Air | ||

| Value-Added Services | ||

| By Temperature Type | Chilled (0-5 °C) | |

| Frozen (-18-0 °C) | ||

| Ambient | ||

| Deep-Frozen / Ultra-Low (less than-20 °C) | ||

| By Application | Fruits and Vegetables | |

| Meat and Poultry | ||

| Fish and Seafood | ||

| Dairy and Frozen Desserts | ||

| Bakery and Confectionery | ||

| Ready-to-Eat Meals | ||

| Pharmaceuticals and Biologics | ||

| Vaccines and Clinical Trial Materials | ||

| Chemicals and Specialty Materials | ||

| Other Perishables | ||

| By Region | Andalusia | |

| Catalonia | ||

| Valencia Region | ||

| Madrid and Central Spain | ||

| Others | ||

Key Questions Answered in the Report

How large will Spain’s temperature-controlled logistics sector be by 2031?

It is forecast to reach USD 7.13 billion, advancing at a 5.78% CAGR over 2026-2031.

Which service type is expanding fastest?

Value-Added Services, including tasks such as labeling and cross-docking, should grow at a 7.7% annual rate through 2031.

Why is chilled capacity gaining momentum?

Rising pharmaceutical shipments and fresh-produce exports require stringent 0 °C–5 °C conditions, driving a 7.13% CAGR in the chilled segment.

Which region offers the quickest growth opportunity?

Valencia Region benefits from upgrades to the Mediterranean Corridor rail network and is projected to grow at a 6.34% CAGR.

What key regulation affects refrigeration equipment choices?

EU Regulation 2024/573 accelerates F-gas phase-down, making natural refrigerants such as ammonia or CO₂ the preferred long-term options.

How are operators tackling diesel-price volatility?

Larger fleets hedge fuel costs and pilot electric or hydrogen trucks, while integrated rail services help dilute diesel exposure on long hauls.

Page last updated on: