Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

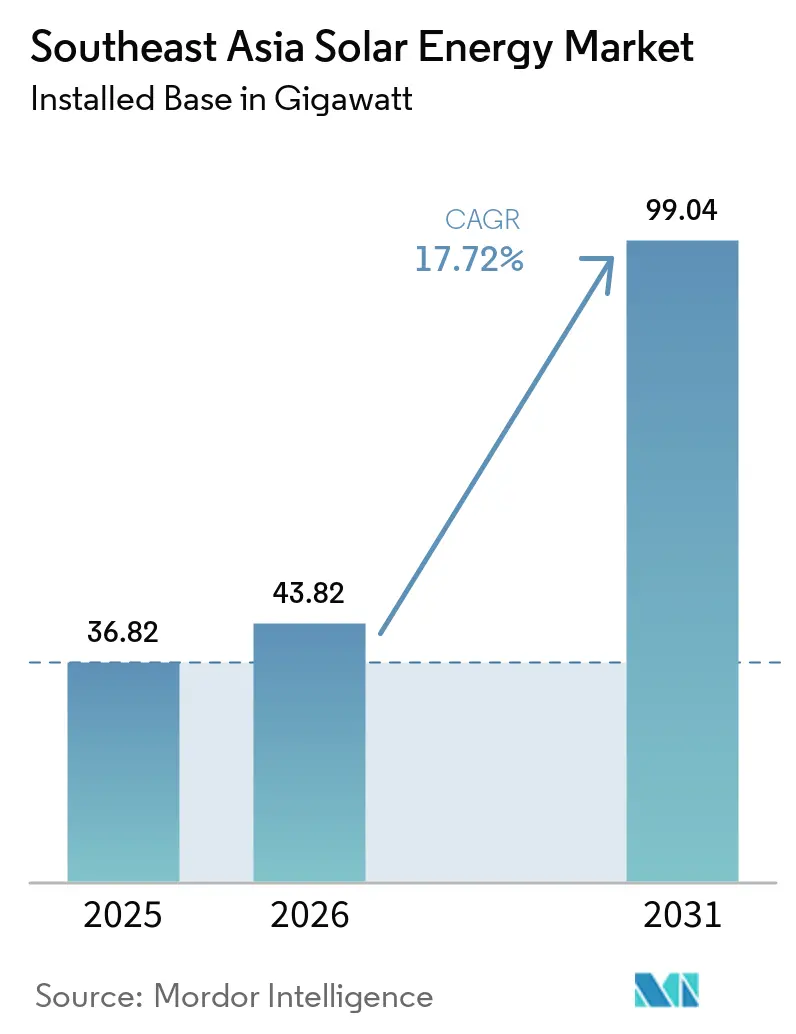

| Base Year Market Size (2025) | 36.82 gigawatt |

| Market Volume (2026) | 43.82 gigawatt |

| Market Volume (2031) | 99.04 gigawatt |

| Growth Rate (2026 - 2031) | 17.72% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Solar Energy Market Analysis by Mordor Intelligence

The Southeast Asia Solar Energy Market size in terms of installed base is expected to increase from 36.82 gigawatt in 2025 to 43.82 gigawatt in 2026 and reach 99.04 gigawatt by 2031, growing at a CAGR of 17.72% over 2026-2031.

Momentum stems from binding carbon-neutral pledges, sharply lower TOPCon module prices, and the operational Lao-Thai-Malaysian-Singapore transmission corridor that unlocks cross-border offtake. Utility-scale developers gain from vertically-integrated Chinese suppliers that offer 700 W-class modules at USD 0.056 per W, while commercial and industrial (C&I) rooftops reach grid parity as retail tariffs rise in Vietnam, Thailand, and Malaysia.[1]EnergyTrend, “TOPCon Module Price Trends,” energytrend.com Floating PV and agrivoltaics help mitigate land scarcity, and battery costs falling toward USD 80 per kWh by late 2026 strengthen solar-plus-storage economics. Nevertheless, land-use conflicts, weak distribution grids, and cyclone-related insurance premiums temper deployment speed, highlighting the need for USD 170 billion in region-wide grid and generation capex by 2030.[2]Asian Development Bank, “Southeast Asia Energy Transition Investment Requirements,” adb.org

Key Report Takeaways

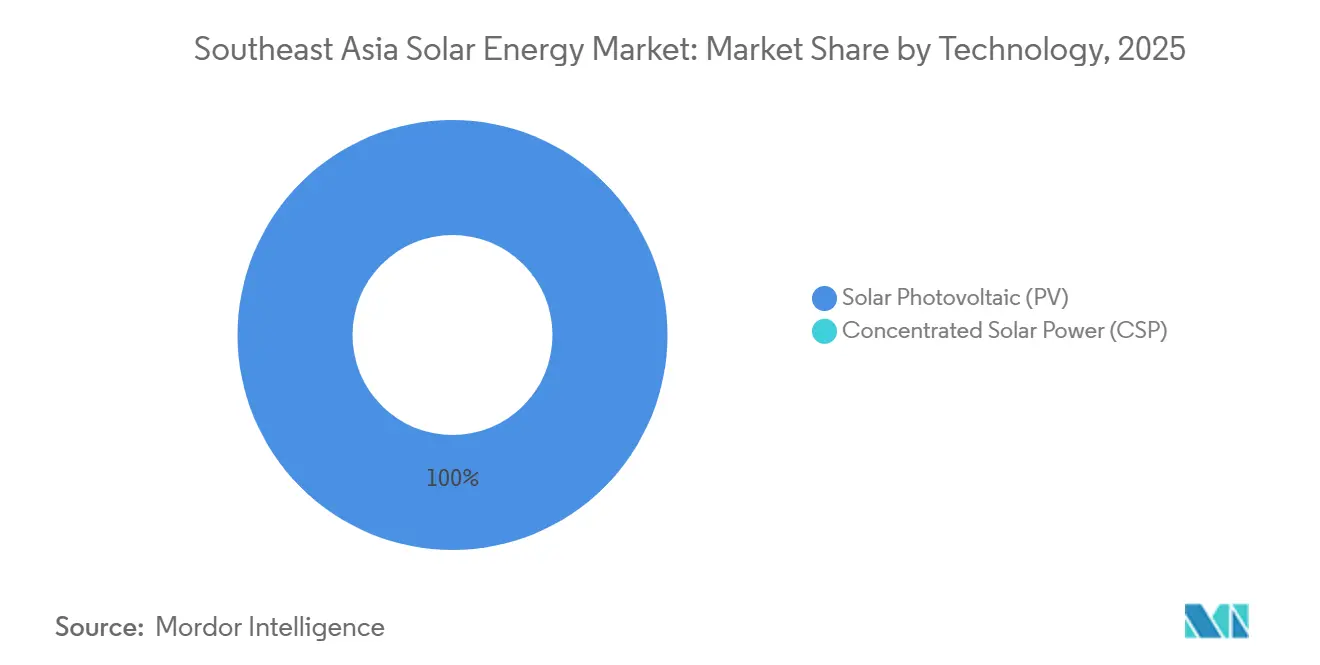

- By technology, photovoltaic systems accounted for 100% of installed capacity in 2025, while concentrated solar power remained negligible.

- By grid type, on-grid installations held 88.3% of the Southeast Asia solar energy market share in 2025, whereas off-grid systems are expected to post a 23.1% CAGR through 2031.

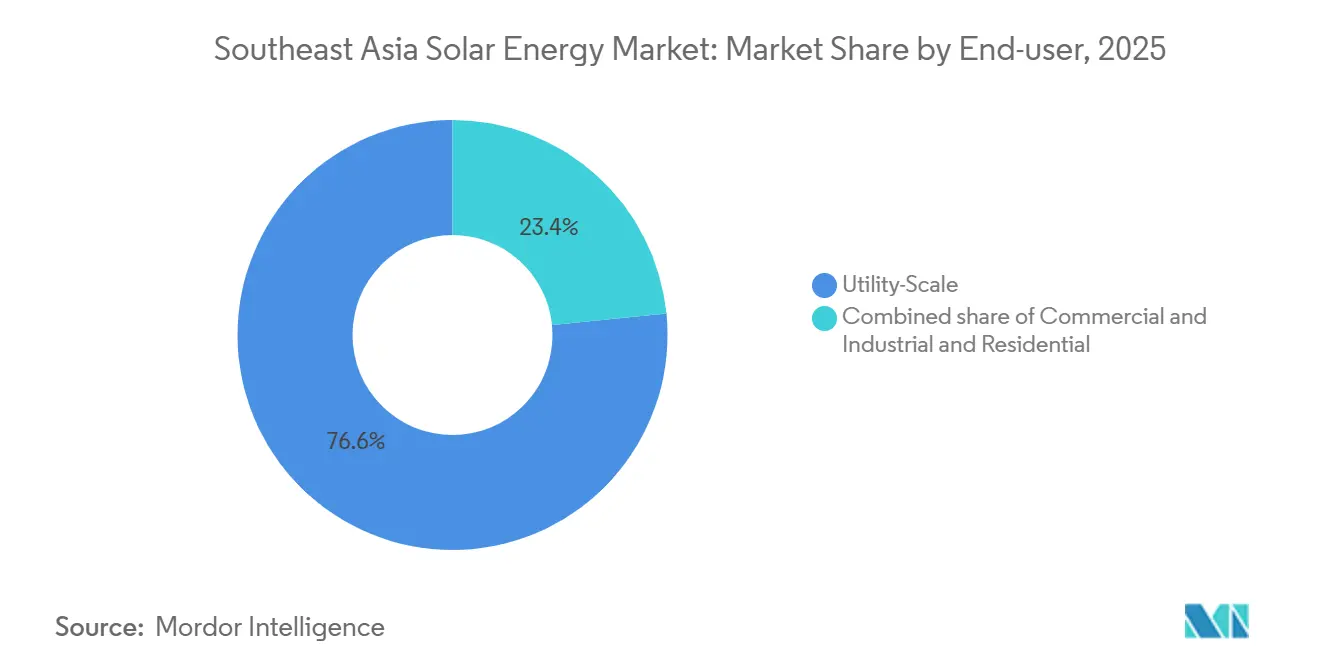

- By end user, utility-scale plants led with 76.6% share of the Southeast Asia solar energy market size in 2025, whereas residential rooftops are expected to grow at a 21.9% CAGR between 2026 and 2031.

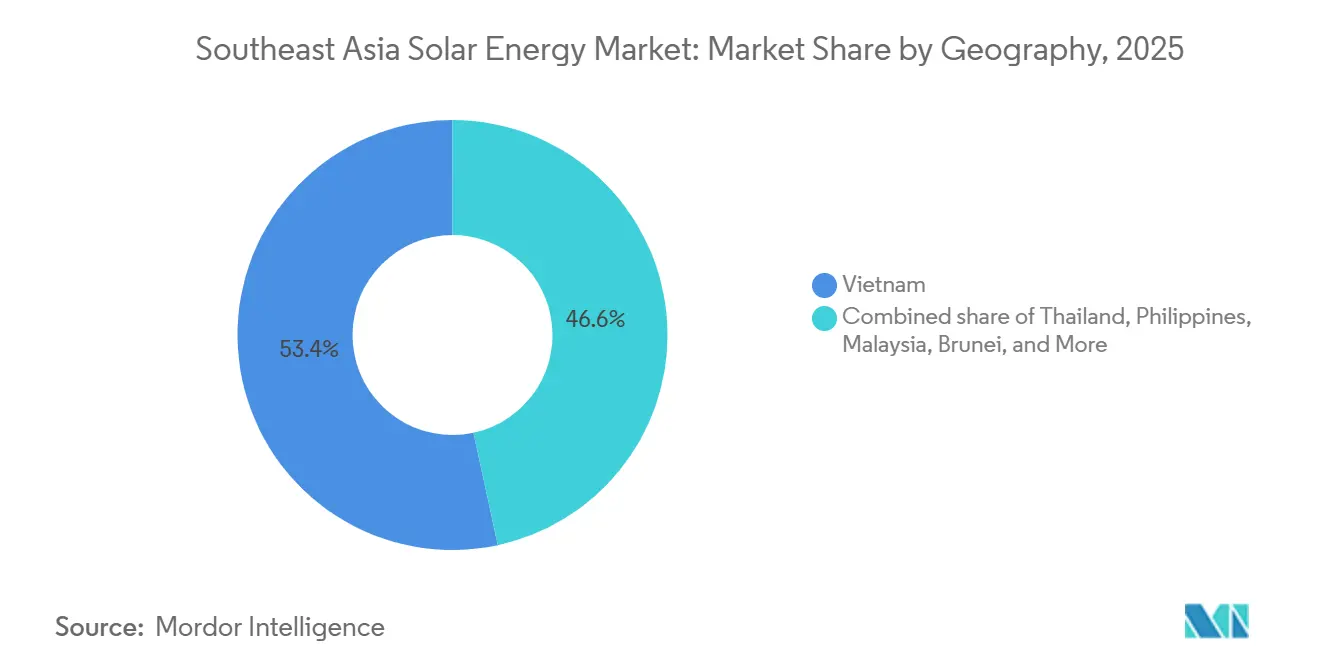

- By geography, Vietnam dominated with 53.37% share in 2025, while Brunei represents the fastest-growing country at 51.03% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Solar Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated National RE Targets And Carbon-Neutral Pledges | 3.20% | Philippines, Malaysia, Vietnam, Brunei | Medium term (2-4 years) |

| Rapid Cost Decline Of Mono-PERC And TOPCon PV Modules | 4.10% | Vietnam, Thailand, Indonesia manufacturing hubs | Short term (≤ 2 years) |

| Grid-Parity Rooftop PV For C&I Users | 2.80% | Vietnam, Thailand, Malaysia, Singapore | Short term (≤ 2 years) |

| ASEAN Cross-Border Power-Trade Pilot | 1.90% | Malaysia, Singapore, Thailand, Lao PDR | Long term (≥ 4 years) |

| Green-Hydrogen Export Ambitions Driving Utility-Scale Solar Pipelines | 2.30% | Malaysia, Indonesia, spillover to Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated National RE Targets And Carbon-Neutral Pledges

Member states adopted the APAEC 2026-2030 roadmap that lifts the renewables share target to 45% of installed capacity by 2030, anchoring offtake certainty for utility-scale projects.[3]Department of Energy Philippines, “Green Energy Auction Program,” doe.gov.ph The Philippines’ Green Energy Auction aims to procure 25 GW annually from 2027, including 3.2 GW of solar in its sixth round. Malaysia’s National Energy Transition Roadmap raises the 2050 renewables goal to 70% and mandates that public buildings secure 20% green power within three years.[4]Malaysia Ministry of Energy, “National Energy Transition Roadmap,” mestecc.gov.my Brunei’s NDC 3.0 commits to a 20% emissions cut by 2035 and 30% renewables share despite severe land constraints. These policies unlock concessional finance, yet will succeed only if grid bottlenecks and the USD 170 billion funding gap are closed.

Rapid Cost Decline Of Mono-PERC And TOPCon PV Modules

TOPCon captured 87.6% of global shipments in 2025, with mass-production efficiency hitting 26% and module prices sliding to USD 0.056 per W in February 2026. Capacity offshoring to Vietnam, Malaysia, and Thailand helped Chinese manufacturers circumvent U.S. duties, ensuring a plentiful regional supply. LONGi’s hybrid back-contact cell reached 27.81% efficiency, and its tandem cell hit a record 34.85%, pointing to further balance-of-system savings. In Vietnam, C&I rooftops already save 15-20% versus grid tariffs, and Malaysian NEM 3.0 participants post five-year paybacks, illustrating how falling hardware costs trigger self-generation uptake. The same cost trajectory erodes coal competitiveness, especially in Indonesia, where captive coal totals 21 GW.

Grid-Parity Rooftop PV For C&I Users

Retail tariff escalation, net-metering reforms, and sub-USD 0.06 per W module prices drove rooftop parity by 2025 in Thailand, Malaysia, and Vietnam. Thailand’s sandbox projects yielded 15-30% bill reductions, spurring 3,668 MW of approved feed-in-tariff solar through 2030. Malaysia’s Corporate Green Power Program allotted 800 MW for contract-for-difference virtual PPAs in 2025. Singapore’s Cleantech Solar installed a 10 MWp floating array for Cargill, showing how water surfaces compensate for land scarcity. Vietnam’s Hoa Phat Dung Quat Steel added 22.5 MWp of N-type modules, illustrating industrial appetite for onsite generation. Corporations thus move from passive consumption to proactive decarbonization.

ASEAN Cross-Border Power-Trade Pilot

Operational since 2025, the Lao-Thai-Malaysian-Singapore corridor transmits up to 200 MW of renewable electricity, offering a blueprint for regional balancing. Singapore granted six conditional approvals totaling 3 GW of solar-plus-storage imports from Indonesia’s Riau Islands, including Vanda Renewable Energies’ 2 GWp plant with 4.4 GWh storage. Trina Solar supplies 1.2 GW of TOPCon modules to the project, underlining vendor confidence. Malaysia’s 2.5 GW Kenyir hybrid solar-hydro scheme pairs power exports with hydrogen production. Yet financing and regulatory harmonization hurdles could delay multilateral expansion, especially where sovereignty concerns persist.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Land-Availability Conflicts In High-Irradiance Zones | −2.4% | Vietnam, Thailand, Philippines | Medium term (2-4 years) |

| Weak Distribution-Grid Infrastructure In Secondary Cities | −1.8% | Indonesia, Philippines, Vietnam | Long term (≥ 4 years) |

| Rising Module-Level Import Tariffs | −1.3% | Vietnam, Malaysia, spillover to Thailand, Cambodia | Short term (≤ 2 years) |

| Cyclone-Related Asset-Risk Premiums | −0.9% | Philippines, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Land-Availability Conflicts In High-Irradiance Zones

Agriculture, mining, and forest protection compete with solar siting in Vietnam, Thailand, and the Philippines, raising land prices and sparking permit delays. Lam Dong province froze 14 Vietnamese projects over forest-conversion breaches, threatening 12 GW of existing capacity and prompting arbitration notices from foreign investors. Philippine land-use conversion can add 18-24 months and PHP 2-3 million per ha in transaction costs. Brunei caps terrestrial solar to <200 MW owing to 55% forest-reserve rules, pushing rooftop adoption despite higher capex per W. Floating PV now forms 31% of Indonesia’s pipeline but costs 15-20% more than ground-mounts and faces typhoon exposure. Agrivoltaics offers relief but lacks mature regulation.

Weak Distribution-Grid Infrastructure In Secondary Cities

Curtailment, interconnection delays, and costly inverter upgrades plague Indonesia, the Philippines, and Vietnam. Indonesia needs USD 15 billion to align grids with a 28 GW renewables target by 2030. Philippine grid delays left July 2023’s green auction only 31% awarded, despite a PHP 905 billion transmission expansion plan by NGCP. Vietnam’s southern grid lost 6% of transmitted energy in 2025 due to reactive-power shortages. EGAT’s THB 500 billion debt constrains Thai reinforcement works. Mini-grids fill gaps, but their USD 0.81-1.61 per kWh costs exceed retail tariffs sixfold.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: PV Dominance Reflects Humid-Tropical Realities

Solar photovoltaic systems commanded the entire Southeast Asia solar energy market in 2025, matching the overall 17.72% CAGR outlook to 2031. Concentrated solar power failed to gain traction because monsoon cloud cover keeps direct normal irradiance below CSP thresholds. Within PV, TOPCon’s rise reshapes balance-of-system economics, while LONGi’s 34.85% tandem cell milestone hints at future gains. Bifacial modules on reservoir and desert-like Thai sites boost yield up to 15%, further lowering levelized costs. JinkoSolar shipped 1.187 GW to Thailand in 2025, obtaining 34% share of that national sub-market. The absence of CSP keeps manufacturing focused on crystalline silicon, reinforcing local industrial clusters in Malaysia and Vietnam.

Second-generation heterojunction (HJT) modules are entering pilot procurement after Huasun and Haier signed a gigawatt-scale agreement in March 2026, a sign that efficiency arms-race dynamics will persist. Efficiency upgrades cut land intensity, an advantage in Singapore and Brunei, where ground parcels are scarce. The Southeast Asia solar energy industry also benefits from lower thermal mismatch losses because TOPCon’s temperature coefficient suits equatorial climates. Combined with utility batteries heading below USD 80 per kWh, PV remains the uncontested technology pathway for the next decade.

By Grid Type: Off-Grid Surge Targets Diesel Displacement

On-grid assets held 88.3% of installed capacity in 2025, leveraging economies of scale and state-utility power purchase agreements that anchor finance. However, off-grid growth at 23.1% CAGR through 2031 underscores the diesel-displacement case in island and hinterland communities. In the Philippines, more than 2.8 million residents rely on subsidized diesel at PHP 16-25 per kWh; solar mini-grids halve costs and end fuel price swings. Myanmar’s Kan Byin microgrid cut energy costs 50% and extended daily service to 24 hours with only 110 SunPower panels and a 75 kW battery. Such examples illustrate why the Southeast Asia solar energy market size for off-grid solutions, though small, is growing rapidly.

Removal of net-metering in Indonesia under Regulation 2/2024 shifts rooftop incentives toward self-consumption, favoring larger C&I users over households. Grid-connected plants face midday curtailment in Vietnam’s southern provinces due to transformer limits, while off-grid sites sidestep such bottlenecks but confront higher capex. Policymakers now pilot results-based grants and blended finance to shrink cost gaps. As battery prices decline, hybrid mini-grids could achieve parity sooner, especially where diesel subsidies strain fiscal budgets, reinforcing long-run off-grid relevance within the Southeast Asia solar energy market.

By End User: Residential Rooftops Gain Amid C&I Maturity

Utility-scale projects accounted for 76.6% of demand in 2025 as governments chased gigawatt-class targets and export corridors. Residential rooftops, though only a fraction of current capacity, will expand at 21.9% CAGR, supported by lease models and cheap batteries. Malaysia’s NEM 3.0 reports 86.8% self-consumption and five-year homeowner paybacks, showcasing a bankable template. In Thailand, energy-regulator pilots yielded 60% self-consumption rates and 30% bill cuts, catalyzing a 1,000 MW solar-plus-storage carve-out. Vietnam’s steel and food-processing complexes illustrate C&I maturity: Hoa Phat Dung Quat’s five-phase 79.2 MWp plan and Cargill’s 10 MWp floating array attest to industrial appetite. Falling storage prices amplify residential value through time-of-use arbitrage and resilience benefits.

Utility developers still dominate headline volumes; EVN’s 100 MW Phuoc Thai 2 and VinEnergo’s 300 MW Dien Bien 1 are emblematic. Yet residential and C&I expansion broadens market depth and distributes economic gains more evenly. Over time, diversified end-user profiles will shelter the Southeast Asia solar energy market from policy volatility that typically affects large centralized PPAs.

Geography Analysis

Vietnam generated 53.37% of regional capacity in 2025, thanks to ambitious Power Development Plan VIII milestones of 34.7 GW by 2035 and 136.6 GW by 2050. EVN’s Phuoc Thai 2 delivers 168 million kWh annually, while the 380 MWp KN Srêpốk 3 floating plant signed a direct PPA with Samsung that begins construction in July 2026. Yet retroactive tariff cuts and land-law enforcement threaten 12 GW of capacity, reducing investor confidence. Southern-grid curtailment adds further complexity as transmission losses exceed 6%.

Brunei, though tiny, posts a 51.03% CAGR outlook to 2031. Its 1,044 MW rooftop potential can supply up to 36% of domestic generation, compensating for strict forest-reserve rules that cap ground-mount projects GOV.BN. Indonesia, Thailand, Malaysia, the Philippines, and Singapore split the remaining capacity. Indonesia secured three Singapore export approvals totaling 3 GW, including Singa Renewables’ 1 GW venture and Vanda’s 2 GWp plant. Trina’s 1.2 GW supply deal underscores hardware readiness.

Thailand’s draft PDP 2023-2037 targets 50% renewables by 2036, but EGAT’s debt hampers grid upgrades. Malaysia’s roadmap envisions 2.5 GW of floating solar-hydro hybrids, and its Corporate Green Power Program stimulates virtual PPAs. The Philippines seeks 25 GW annual auction volumes yet still battles transmission delays that left 2023’s tender undersubscribed. Singapore’s 6 GW import target equals one-third of national demand, reflecting a strategy of regional sourcing over domestic build-out. Collectively, these dynamics confirm an uneven but converging push toward massive solar deployment across the Southeast Asia solar energy market.

Competitive Landscape

Chinese vertically-integrated giants, Canadian Solar, JinkoSolar, Trina Solar, and LONGi, anchor module supply, offering bankable warranties and multi-GW factories in Malaysia, Vietnam, and Thailand. JinkoSolar captured 34% of Thai shipments and opened a Bangkok hub in 2025. LONGi retains top-tier bankability and sets new efficiency records, while Trina’s Vertex N 700 W lineup underpins utility bidders seeking higher yields. U.S. trade duties disrupted export markets, prompting capacity reallocations to the Middle East and North Africa, but also spurring OCI’s 2.7 GW wafer investment in Vietnam to supply “clean” components.

Regional independent power producers, Vena Energy, Scatec, AC Energy, and Sembcorp, compete on hybrid portfolios and customer-centric PPAs. Scatec and Aboitiz won a 68 MW floating project on the Magat reservoir under a 20-year PPA in November 2025. Sembcorp’s pending Alinta Energy purchase deepens its regional footprint. New entrants such as VinEnergo tout a 10 GW launch slate and a 100 GW aspiration within three years, signaling intensifying competition.

Critical-mineral vertical integration emerges as a disruptive theme. Chinese battery majors, CATL, Gotion, CNGR, and Huayou, pour billions into Indonesia’s nickel hubs, creating cradle-to-grave solar-plus-storage value chains. Huasun’s HJT supply deal with Haier suggests another efficiency leap on the horizon. Altogether, rivalry is robust but not yet hyper-fragmented, giving top players latitude to preserve margins within the Southeast Asia solar energy market.

Southeast Asia Solar Energy Industry Leaders

Canadian Solar Inc.

JinkoSolar Holding Co. Ltd

Trina Solar Limited

Thai Solar Energy Public Company Limited

Scatec ASA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Huasun Photovoltaic Technology and Qingdao Haier inked a GW-scale heterojunction module procurement agreement for zero-carbon industrial park projects.

- January 2026: JinkoSolar signed 300 MW of Tiger Pro 3 module distribution deals with four Thai partners, reinforcing its shipment leadership.

- January 2026: OCI Holdings commenced operations at a 2.7 GW wafer plant in Vietnam, with plans to double capacity within six months.

- November 2026: Scatec and Aboitiz Renewables secured a 20-year PPA for a 68 MW floating solar project on Magat reservoir, Philippines.

Southeast Asia Solar Energy Market Report Scope

Solar energy is the heat and radiant light from the Sun that can be harnessed through technologies such as solar power (used to generate electricity) and solar thermal energy (used for applications like water heating).

The Southeast Asia Solar Energy Market is segmented by technology, grid type, end-user, and geography. By technology, the market is segmented into solar photovoltaic (PV) and concentrated solar power (CSP). By grid type, the market is segmented into on-grid and off-grid. By end-user, the market is segmented into utility-scale, commercial and industrial (C&I), and residential. By geography, the market is segmented into Vietnam, Indonesia, Philippines, Thailand, Malaysia, Singapore, and Rest of Southeast Asia. For each segment, market sizing and forecasts have been conducted based on installed capacity (GW).

By Technology

| Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) |

By Grid Type

| On-Grid |

| Off-Grid |

By End-User

| Utility-Scale |

| Commercial and Industrial (C&I) |

| Residential |

By Component (Qualitative Analysis)

| Solar Modules/Panels |

| Inverters (String, Central, Micro) |

| Mounting and Tracking Systems |

| Balance-of-System and Electricals |

| Energy Storage and Hybrid Integration |

By Geography

| Vietnam |

| Indonesia |

| Philippines |

| Thailand |

| Malaysia |

| Singapore |

| Rest of South East Asia |

| By Technology | Solar Photovoltaic (PV) |

| Concentrated Solar Power (CSP) | |

| By Grid Type | On-Grid |

| Off-Grid | |

| By End-User | Utility-Scale |

| Commercial and Industrial (C&I) | |

| Residential | |

| By Component (Qualitative Analysis) | Solar Modules/Panels |

| Inverters (String, Central, Micro) | |

| Mounting and Tracking Systems | |

| Balance-of-System and Electricals | |

| Energy Storage and Hybrid Integration | |

| By Geography | Vietnam |

| Indonesia | |

| Philippines | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Rest of South East Asia |

Key Questions Answered in the Report

How large will Southeast Asia's installed solar capacity be by 2031?

It is forecast to reach 99.04 GW, more than doubling current levels.

Which country currently leads deployment?

Vietnam held 53.37% of regional capacity in 2025 thanks to ambitious PDP VIII targets.

Which country is expected to have fastest growth?

Brunei is projected to expand solar capacity at 51.03% CAGR through 2031.

Why are TOPCon modules so popular in the region?

They combine 26% efficiency with FOB prices of USD 0.056 per W, driving immediate LCOE reductions.

What risks could slow future build-out?

Land-use conflicts, weak distribution grids, rising trade tariffs, and cyclone-related insurance premiums all dampen momentum.

Page last updated on: