Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

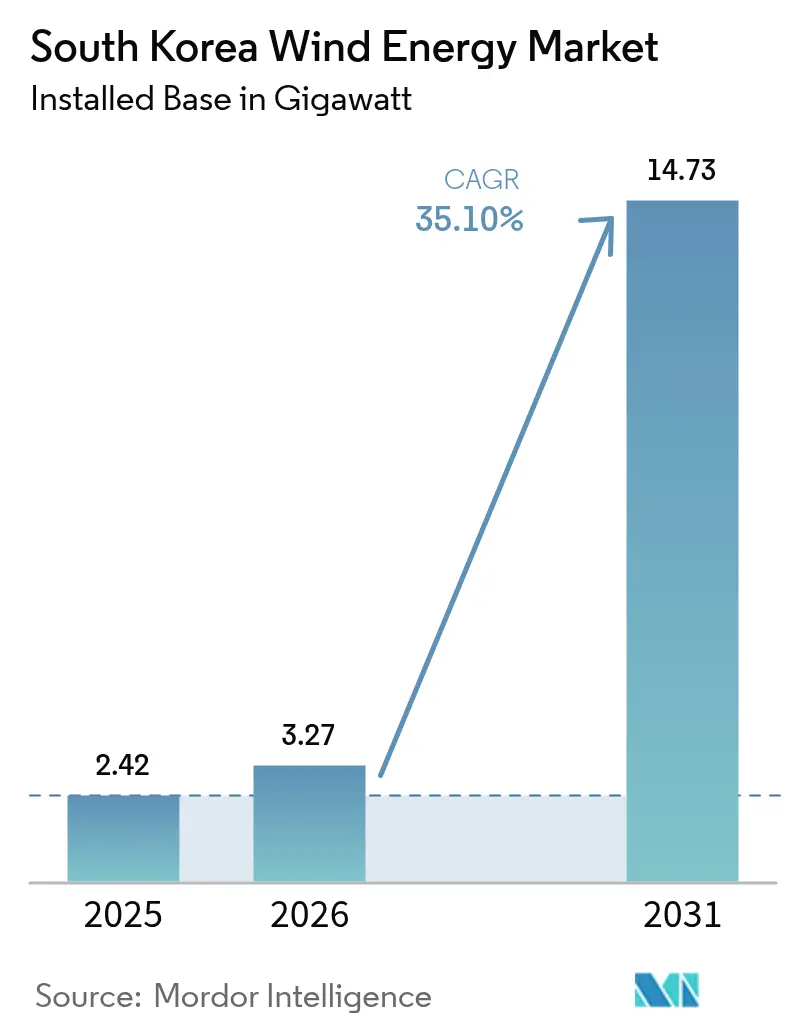

| Base Year Market Size (2025) | 2.42 gigawatt |

| Market Volume (2026) | 3.27 gigawatt |

| Market Volume (2031) | 14.73 gigawatt |

| Growth Rate (2026 - 2031) | 35.10% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Wind Energy Market Analysis by Mordor Intelligence

South Korea Wind Energy Market size in 2026 is estimated at 3.27 gigawatt, growing from 2025 value of 2.42 gigawatt with 2031 projections showing 14.73 gigawatt, growing at 35.10% CAGR over 2026-2031.

Strong policy support under the Green New Deal, rapid offshore build-out, and rising corporate power-purchase agreements (PPAs) underpin this sustained expansion. Developers are pivoting from incremental onshore additions toward utility-scale offshore arrays that leverage Korea’s shipbuilding capacity, export-credit insurance, and localized high-voltage cables to compress project timelines and costs. Floating-wind technology validated off Ulsan in 2024 now unlocks deep-water East Sea resources, while turbine upsizing to 8–15 MW platforms lowers balance-of-system costs and boosts capacity factors. Competition intensifies as European majors ally with chaebols, yet permitting, grid congestion, and typhoon-grade design standards cap near-term installation rates and pressure project returns.

Key Report Takeaways

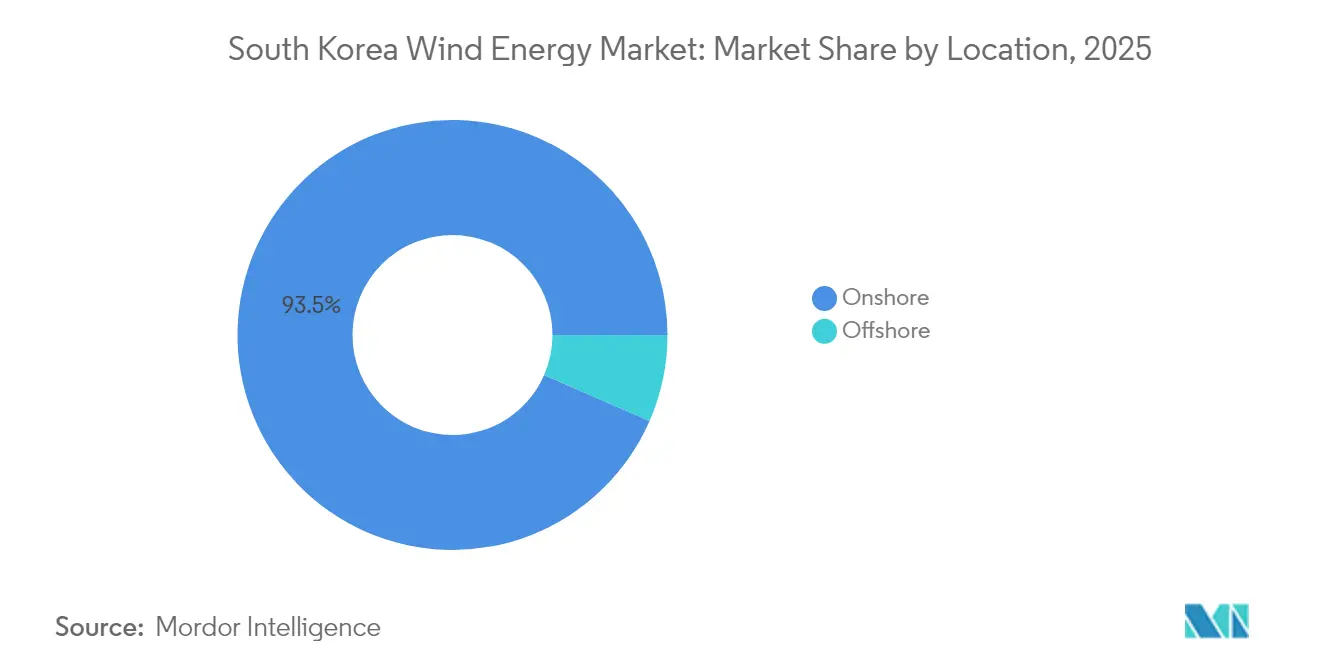

- By location, onshore wind held 93.45% of the South Korea wind energy market share in 2025, while offshore capacity is forecast to compound at 72.90% CAGR through 2031.

- By turbine capacity, the 3–6 MW class accounted for 66.90% of the South Korean wind energy market size in 2025; the above-6 MW segment is projected to expand at a 40.20% CAGR to 2031.

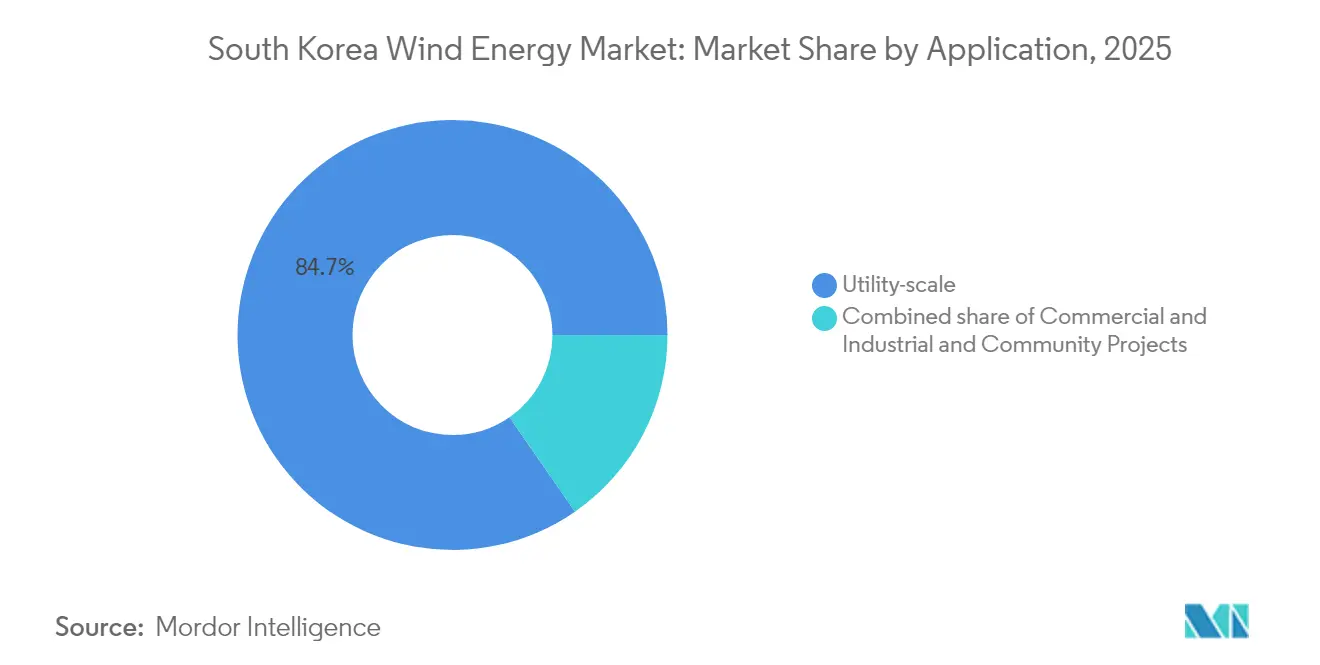

- By application, utility-scale projects captured 84.65% of the South Korea wind energy market size in 2025 and are slated to grow at a 38.10% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Green New Deal & 9th Basic Plan Mandating 12 GW Offshore by 2030 | +12.5% | National, Jeolla & Gyeongsang | Long term (≥ 4 years) |

| Floating-Wind Testbed off Ulsan Reducing Deep-Sea Project Risk | +6.8% | Ulsan, Busan, East Sea | Medium term (2-4 years) |

| Corporate PPAs From Korean Tech Giants Unlocking Long-Term Offtake | +5.2% | National, Seoul-Incheon belt | Medium term (2-4 years) |

| Jeju Carbon-Free Island 2030 Accelerating Onshore Repowering | +3.1% | Jeju Island | Short term (≤ 2 years) |

| Export Credit Insurance for Renewable OEMs Lowering Financing Cost | +2.9% | National | Medium term (2-4 years) |

| High-Voltage K-SUPCON Cable Localization Boosting Domestic Content | +4.3% | West & South Sea zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Green New Deal & 9th Basic Plan Mandating 12 GW Offshore by 2030

Government alignment between the Green New Deal stimulus and the 9th Basic Plan provides an enforceable target to install 12 GW of offshore wind by 2030, an eighty-five-fold jump from the 142 MW operating base. This statutory goal obliges the grid operator to finance transmission upgrades, while the draft Special Act on wind power promises consolidated permitting and clear service-level timelines. Jeollanam-do’s 75 trillion KRW investment program underpins local port deepening, substation upgrades, and training centers that shorten construction lead times. Policy coupling with the national hydrogen roadmap has widened the revenue stack, as offshore projects will supply green hydrogen electrolyzers co-located at the Sinan and Mokpo industrial zones. State-led coordination reduces offtake uncertainty, lowering capital-cost premiums for private developers. These measures anchor the medium-term uplift in the South Korean wind energy market outlook.

Floating-Wind Testbed off Ulsan Reducing Deep-Sea Project Risk

A 1 GW floating-wind testbed administered by the Korea Research Institute of Ships & Ocean Engineering validates mooring systems that withstand typhoon loads and 60-meter waves, derisking future deployments in Korea’s steep continental shelf waters.[1]Korea Research Institute of Ships & Ocean Engineering, “Floating Wind Testbed Overview,” kriso.re.kr Prototype trials confirm that 15 MW turbines mounted on semi-submersible hulls meet structural codes, and proximity to Ulsan’s shipyards cuts platform transport costs by 30%. The acquisition of the 1.125 GW MunmuBaram project by Hexicon after Shell’s exit illustrates sustained foreign appetite for floating projects.[2]Maritime Executive Staff, “Hexicon Acquires Korean Floating Wind Project,” maritime-executive.com Successful scale-up will open more than 300 % in additional technically viable acreage along the East Coast, reinforcing long-term South Korean wind energy market growth.

Corporate PPAs From Korean Tech Giants Unlocking Long-Term Offtake

Direct PPAs introduced in 2021 dismantle the Korea Electric Power Corporation monopoly by allowing large corporations to contract electricity directly from generators. Hyundai Motor has already locked in 610 GWh annually for twenty years, an agreement worth about USD 500 million.[3]Hyundai Motor Group, “Hyundai Motor Signs 610 GWh Renewable PPA,” hyundaimotorgroup.com Samsung Electronics, LG Chem, and an expanding cluster of data-center operators are lining up similar procurement, each time bypassing renewable-certificate volatility and giving lenders twenty-year cash-flow visibility. Corporate demand is shifting bidding dynamics: developers who align projects with PPA windows secure lower financing spreads, enabling faster construction schedules. These contracts, therefore, inject near-term momentum into the South Korean wind energy market.

Jeju Carbon-Free Island 2030 Accelerating On-Shore Repowering

Jeju has set a binding objective to meet all electricity demand with renewables by 2030, and wind is expected to deliver around 60 % of the target capacity. Limited land availability has turned attention to repowering, replacing 2-MW legacy machines with 6-MW models on existing pads, and re-using interconnection rights. Early deployments show capacity factors rising by 15 percentage points, while integrated storage reduces curtailment risk. Jeju’s success strengthens public acceptance and will likely guide similar repowering programs in Ulleung and Chuja archipelagos. Repowering keeps development costs lower than greenfield builds, reinforcing mid-term tailwinds in the South Korean wind energy market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Permit Bottlenecks From “One-Stop” EIA System Delay FID | -5.7% | National, Jeolla & Gyeongsang | Short term (≤ 2 years) |

| Grid Congestion in Southwest Coast Limiting Curtail-Free Dispatch | -4.2% | Jeolla offshore clusters | Medium term (2-4 years) |

| Fisheries & Military Exclusion Zones Shrinking Developable Sites | -3.8% | West & South Sea waters | Long term (≥ 4 years) |

| High LCoE Due to Typhoon-Grade Design Standards | -6.1% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Permit Bottlenecks From “One-Stop” EIA System Delay FID

The Environmental Impact Assessment regime remains sequential despite its “one-stop” branding, obliging developers to clear maritime, military, and cultural reviews in turn rather than concurrently.[4]Energy Global Editors, “EIA Approvals Continue to Slow Korean Wind Projects,” energyglobal.com The Haewoori offshore wind project illustrates the stress: the EIA consultation spanned 28 months, well above the twelve-month OECD benchmark. Government plans to devolve authority to provincial agencies could truncate processing time, yet agency staffing levels must rise to handle a bulging pipeline. Until execution gaps close, slow approvals will trim the near-term growth rate built into the South Korean wind energy market.

Grid Congestion in Southwest Coast Limiting Curtail-Free Dispatch

Southwestern corridors were designed for point-source coal rather than distributed renewables, and the resulting bottlenecks have forced wind farms to curtail during peak output. Korea Electric Power Corporation’s USD 15 billion reinforcement plan includes a multi-terminal direct-current (MTDC) offshore backbone that will ferry power directly to Seoul load centers. Construction delays linked to fishing cooperatives and coastal permitting challenge this solution, so AI-enabled dispatch optimization is a stopgap. Until physical upgrades arrive, network saturation will subtract several points from the CAGR of the South Korean wind energy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Offshore Surge Eclipses Onshore Maturity

Offshore installations, which accounted for just 6.55% of capacity in 2025, are expected to eclipse onshore assets by 2031 as developers race to meet the 12 GW target, propelling the South Korean wind energy market toward coastal industrialization. Onshore repowering adds efficiency but only modest net capacity, whereas floating foundations unlock East Sea sites that were previously inaccessible due to depths of 100 meters.

Offshore success reconfigures supply chains: Korean shipyards fabricate semi-submersibles, LS Cable provides localized subsea arrays, and domestic content rules channel spending into Korean steel, electronics, and port infrastructure. High capacity factors of 35–40% offset capex premiums and justify grid reinforcement to Seoul-Incheon load centers, confirming offshore wind as the dominant growth engine of the South Korean wind energy market.

By Turbine Capacity: Gigawatt-Scale Machines Redefine Project Economics

The 3–6 MW class delivered 66.90% of installations in 2025; however, above-6 MW turbines will command future build-outs as fewer, larger machines reduce balance-of-system costs by 20–30%. Units above 6 MW achieve capacity factors exceeding 40% in offshore zones, enhancing grid stability and facilitating KEPCO’s integration agenda.

Demand outstrips domestic nacelle capacity of 1–1.5 GW per year, creating a near-term import gap from Europe. Doosan and Hyosung’s planned expansions for 2025-2026 aim to close this deficit, reinforcing the South Korean wind energy industry’s ambition to export typhoon-class turbines to Japan and Taiwan.

By Application: Utility-Scale Dominance Reflects Grid-Centric Policy

Utility-scale arrays held 84.65% of installations in 2025 and will grow at 38.10% CAGR through 2031 as KEPCO favors ≥ 500 MW projects that connect directly to 345 kV and 765 kV networks. REC auctions, long-term PPAs, and concessional finance endorse large arrays that spread fixed costs over gigawatt volumes.

Commercial-and-industrial (C&I) buyers, led by semiconductor and battery makers, account for roughly 10% of capacity, using direct PPAs to hedge carbon risk. Community projects remain below 5% due to higher financing costs and limited offtake assurances, although Jeju’s benefit-sharing model may spur incremental growth if replicated on the mainland.

Geography Analysis

Concentration along the Southwest Coast makes the region the largest contributor to installed capacity and pipeline volume, thanks to stable 8 m/s average wind speeds and shallow seabed conditions. The Jeollanam-do government’s 8.2 GW flagship complex alone represents more than 10% of the global offshore project pipeline. Complementary investments in port dredging, haul-road widening, and turbine-blade staging areas keep logistics costs competitive, anchoring the Southwest as the centerpiece of the South Korean wind energy market. A corresponding USD 1.1 billion fisheries compensation fund has eased early-stage pushback, illustrating how targeted community benefits can smooth social license risks.

Ulsan, on the southeast peninsula, is pivoting from hydrocarbons to floating wind, leveraging giant dry docks and fabrication yards that once built drilling rigs. The 1.125 GW MunmuBaram project will field 15 MW turbines tethered 70 km offshore, validating deep-water layouts. Ulsan City’s memorandum with local universities to train 3,000 technicians by 2027 addresses skilled-labor gaps, positioning the port as a floating-wind export hub for the wider Asia-Pacific region. This specialization differentiates the locale and injects diversity into the South Korean wind energy market footprint.

Jeju Island offers a living laboratory for smart-grid integration, energy storage pairing, and turbine repowering under its Carbon-Free Island 2030 initiative. Wind already meets a third of peak load, and the island will require 2 GW of added renewables, 60% of which is expected to come from wind, to reach full self-sufficiency. Grid-connected battery banks ease curtailment, while predictive weather data from the Korea Meteorological Administration optimizes dispatch. Jeju’s demonstrable success feeds learning loops that the mainland grid operator now embeds in expansion blueprints, strengthening operational resilience across the national South Korean wind energy market.

Competitive Landscape

The market is moderately concentrated, with the top five developers controlling 55–60% of offshore capacity in development, while onshore assets are distributed among 15–20 independent companies. Offshore consortia combine European capital and technology with Korean regulatory experience and supply chains; examples include Ørsted–SK E&S and Equinor–Korea East-West Power.

SK E&S’s vertically integrated model secures offtake, subsea cables, and turbine supply within the chaebol, easing financing and accelerating construction. Hanwha’s diversified approach pairs wind with solar and green hydrogen to meet corporate buyer demand under bundled PPAs.

Doosan Enerbility’s 8 MW typhoon-class turbine wins orders by offering 15–20% lower delivered costs than imported models, helped by export credit insurance and Busan tower capacity expansions. Smaller firms, such as Elenergy, pilot wind-storage hybrids, carving out niches around curtailment mitigation in congested grids.

Overall, strategic moves center on supply-chain localization, scaling up floating wind, and corporate PPAs that shift revenue away from wholesale markets, shaping the competitive landscape of the South Korean wind energy market.

South Korea Wind Energy Industry Leaders

Ørsted A/S

Vestas Wind Systems A/S

Doosan Enerbility Co., Ltd.

Equinor ASA

Siemens Gamesa Renewable Energy S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Vena Energy announced a USD 200 million investment in the Yoki offshore wind farm project in South Korea.

- February 2025: South Korea finalized its 11th Basic Plan for Electricity Supply and Demand, lifting renewable targets to 121.9 GW by 2038.

- December 2024: South Korea awarded 1.9 GW in its third offshore wind auction at prices set near KRW 177,000/MWh.

- October 2024: Hyundai Motor signed Korea’s largest renewable supply contract, locking in 610 GWh annually over 20 years.

South Korea Wind Energy Market Report Scope

The wind is used to produce electricity by converting the kinetic energy of air in motion into electricity. By rotating the rotor blades, wind transforms kinetic energy into rotational energy. The rotational energy is transferred to the generator through a shaft, thereby generating electrical power. For each segment, the market sizes and forecasts have been done based on installed capacity (GW). The South Korea wind energy market report includes:

By Location

| Onshore |

| Offshore |

By Turbine Capacity

| Up to 3 MW |

| 3 to 6 MW |

| Above 6 MW |

By Application

| Utility-scale |

| Commercial and Industrial |

| Community Projects |

By Component (Qualitative Analysis)

| Nacelle/Turbine |

| Blade |

| Tower |

| Generator and Gearbox |

| Balance-of-System |

| By Location | Onshore |

| Offshore | |

| By Turbine Capacity | Up to 3 MW |

| 3 to 6 MW | |

| Above 6 MW | |

| By Application | Utility-scale |

| Commercial and Industrial | |

| Community Projects | |

| By Component (Qualitative Analysis) | Nacelle/Turbine |

| Blade | |

| Tower | |

| Generator and Gearbox | |

| Balance-of-System |

Key Questions Answered in the Report

How large is the South Korea wind energy market in 2026?

Installed capacity is projected at 3.27 GW in 2026.

What is the forecast CAGR for South Korean wind capacity to 2031?

Capacity is expected to expand at a 35.10% CAGR, reaching 14.73 GW by 2031.

Why are offshore projects growing faster than onshore in Korea?

Offshore arrays benefit from the 12 GW Green New Deal mandate, higher capacity factors, and floating-wind advances that unlock deep-water sites.

Which turbine segment will dominate future Korean installations?

Above-6 MW turbines are set to grow at 40.20% CAGR, driven by 8-15 MW platforms that lower per-MW installation costs.

How are corporate PPAs shaping Korean wind development?

Tech giants like Samsung and SK Hynix sign 15-20-year PPAs that secure revenue streams, enabling non-recourse financing for large offshore farms.

What grid upgrades are planned to handle new offshore capacity?

KEPCO will build 765 kV lines linking Jeolla wind zones to Seoul-Incheon by 2028, funded under a KRW 4.2 trillion plan.

Page last updated on: