Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

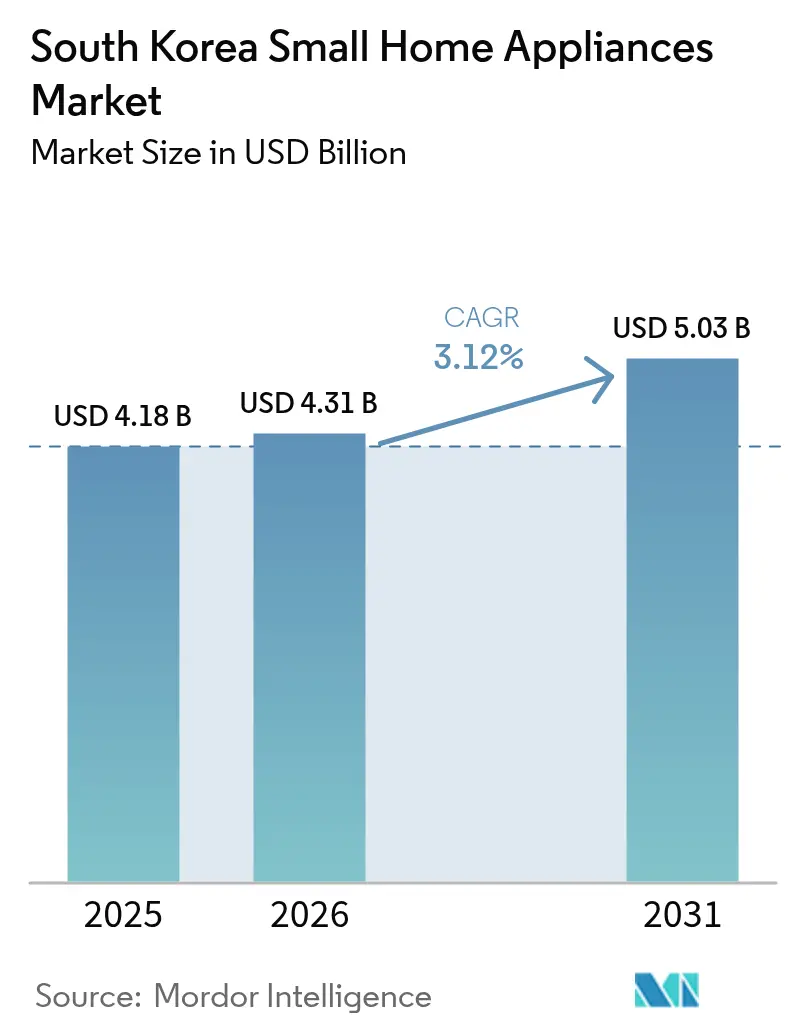

| Base Year Market Size (2025) | USD 4.18 Billion |

| Market Size (2026) | USD 4.31 Billion |

| Market Size (2031) | USD 5.03 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Small Home Appliances Market Analysis by Mordor Intelligence

South Korea small home appliance market size in 2026 is estimated at USD 4.31 billion, growing from 2025 value of USD 4.18 billion with 2031 projections showing USD 5.03 billion, growing at 3.12% CAGR over 2026-2031. Current growth is underpinned by rapid single-person household formation, premium appliance adoption, and accelerating smart-home integration, while economic headwinds and supply chain risks temper the overall trajectory. Robust government incentives for energy-efficient designs, surging demand for premium coffee equipment, and widening e-commerce penetration collectively foster healthy revenue expansion. At the same time, semiconductor supply volatility, household debt constraints, and fragmented rural service networks introduce structural challenges that manufacturers must navigate. Increasing ESG scrutiny and the rollout of standardized IoT protocols further compel brands to prioritize energy footprints and interoperability in future product roadmaps.

Key Report Takeaways

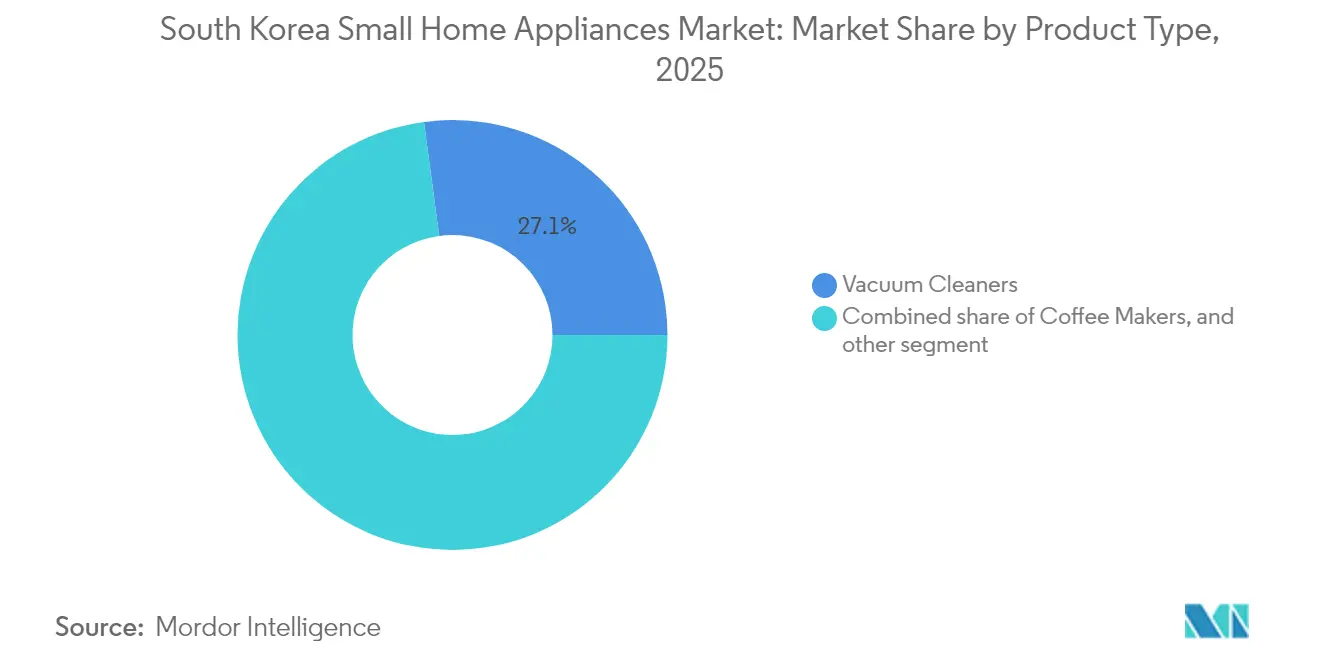

- By product type, vacuum cleaners led with 27.12% of the South Korea small home appliance market share in 2025; smart robotic models are forecast to advance at a 13.95% CAGR through 2031.

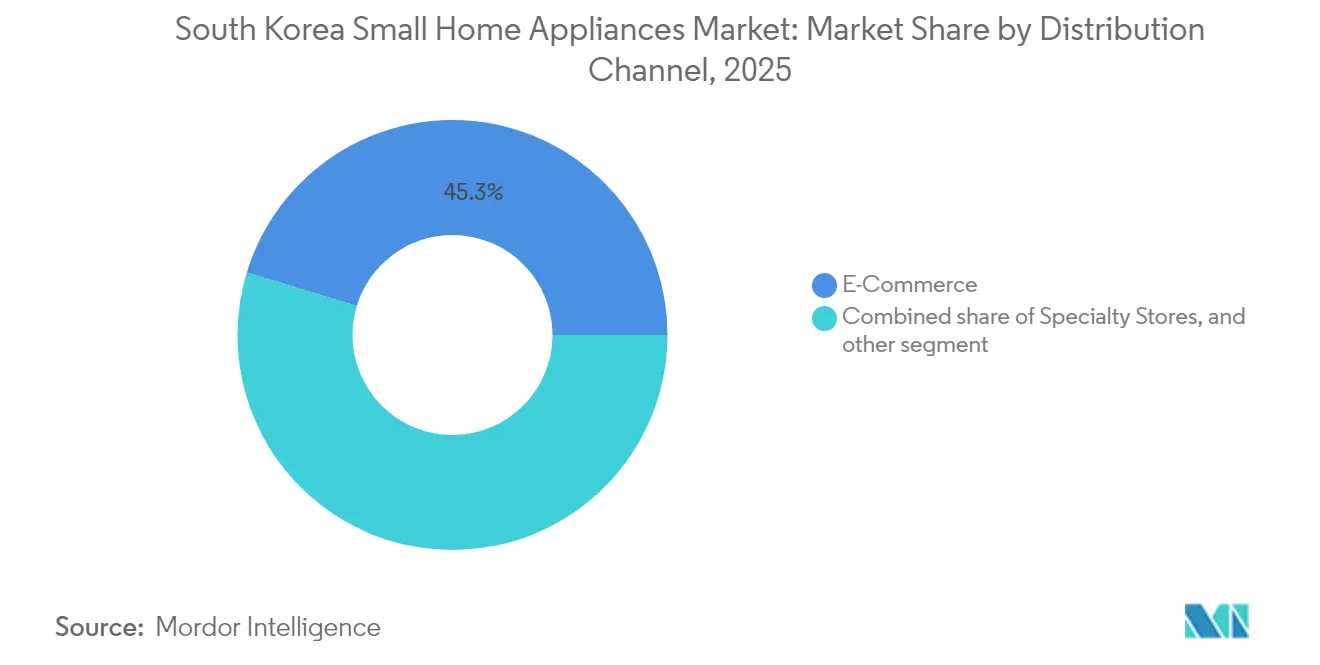

- By distribution channel, e-commerce accounted for 45.30% of the South Korea small home appliance market size in 2025 and is growing at a 15.05% CAGR toward 2031.

- By technology, energy-efficient appliances captured 46.70% of the South Korea small home appliance market size in 2025, while smart-connected units are expanding at a 15.60% CAGR to 2031.

- By geography, the Seoul Capital Area commanded 52.10% revenue share of the South Korea small home appliance market in 2025, whereas Jeju Province is projected to post an 11.05% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Small Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of single-person households | +0.8% | Seoul Capital Area, major urban centres | Medium term (2-4 years) |

| Rising demand for premium coffee culture equipment | +0.5% | Seoul Capital Area, affluent urban areas | Short term (≤ 2 years) |

| Government subsidies for high-efficiency motors & inverters | +0.4% | National, metro focus | Medium term (2-4 years) |

| Growth of quick-commerce grocery platforms bundling appliances | +0.3% | Seoul Capital Area, secondary cities | Short term (≤ 2 years) |

| ESG-driven investor pressure on appliance energy footprints | +0.2% | National, early in Seoul & Busan | Long term (≥ 4 years) |

| Emergence of Korean smart-home ecosystems (Matter, Zigbee) | +0.3% | Seoul Capital Area, tech-forward homes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Single-Person Households

Single-person households reached 42% of all Korean households in 2024, totalling 9.93 million units, and this demographic now decisively shapes appliance demand[1]Min-sik Yoon, “Solo Living: A New Norm in Seoul,” The Korea Herald, koreaherald.com . Compact, multi-purpose designs gain traction because urban dwellers value space savings, illustrated by Samsung’s Bespoke AI Laundry Combo that combines wash-and-dry functions and cuts footprint. Elevated willingness to pay for automation fosters rapid uptake of smart vacuums and subscription-based services. Mobile-first shopping habits, over 60% of e-commerce transactions occur via phone, further streamline digital discovery, and reinforce e-commerce dominance[2]Bank of Korea, “Economic Outlook (May 2025),” bok.or.kr . As single residents often inhabit premium micro-apartments, they increasingly favour AI-enabled, energy-efficient appliances that integrate seamlessly into smart-home ecosystems.

Rising Demand for Premium Coffee Culture Equipment

The increasing annual coffee consumption among adults is driving significant investments in premium home-brewing equipment, reflecting a shift toward enhanced at-home coffee experiences. De’Longhi's Household division reported a 6.9% increase in revenue during Q2 2024, attributed primarily to the strong performance of its coffee device segment. This growth highlights the division's ability to capitalize on consumer demand within the coffee appliance market. Korean consumers exhibit notable price elasticity when quality enhancements are clear, gravitating to machines that automate grind sizing, pressure, and temperature. Connectivity remains pivotal because AI algorithms can replicate barista preferences, further elevating premium positioning.

Government Subsidies for High-Efficiency Motors & Inverters

In Q1 2024, Samsung's energy-efficient air conditioners achieved significant market penetration, supported by the Korea Energy Agency's regulatory and financial initiatives. The agency's mandatory 1-5 efficiency labeling system effectively removed low-performing models from the market, ensuring only high-efficiency products remain competitive. Simultaneously, the High-Efficiency Appliance Rebate program reduced acquisition costs, making energy-efficient appliances more accessible to consumers. Foreign manufacturers have also been encouraged to invest in local production facilities for inverter motors, driven by attractive incentives such as cash subsidies and seven-year tax exemptions. This strategic policy framework has reshaped consumer behavior, with energy efficiency ratings now serving as a critical determinant of product quality. As a result, brands dependent on conventional motor technologies are experiencing increased competitive pressure to innovate. This shift in market dynamics has led to heightened investments in research and development, particularly in advanced technologies like inverter compressors and BLDC motors, which are being integrated across diverse product portfolios to meet evolving consumer expectations and regulatory standards.

Growth of Quick-Commerce Grocery Platforms Bundling Appliances

Coupang's dominance in South Korea's e-commerce market enables the company to strategically cross-sell products such as mixers, kettles, and vacuums by integrating them into the purchasing process for everyday food items. This approach leverages consumer buying patterns to enhance product visibility and drive additional sales. Kurly likewise now stocks small appliances to elevate basket size and retention. Bundling thrives in a mobile-centric ecosystem, pairing impulse buys with one-hour grocery delivery and shrinking the path to purchase. Data-driven algorithms recommend appliances that mirror household grocery patterns, improving conversion and enabling smaller challenger brands to gain visibility. Quick-commerce’s speed and convenience, therefore, intensify price competition for brick-and-mortar electronics retailers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Economic slowdown is impacting discretionary spend | -0.7% | National, stronger in rural areas | Short term (≤ 2 years) |

| High household debt levels are limiting credit-based purchases | -0.5% | National, urban focus | Medium term (2-4 years) |

| Fragmented after-sales service outside metro areas | -0.3% | Rural regions, secondary cities | Long term (≥ 4 years) |

| Semiconductor supply volatility for IoT chipsets | -0.2% | National, smart segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Economic Slowdown Impacting Discretionary Spend

GDP growth was revised to just 0.8% for 2025, dragging consumer sentiment to its weakest since 2008 and depressing retail volumes[3]Chae-Yeon Kim, “Samsung's AI-Powered Robot Vacuum…,” kedglobal.com . Consumers with high price sensitivity are prioritizing essential replacements or repairs over investing in premium upgrades. The decline in housing values is diminishing wealth effects, with a more pronounced impact observed in regions outside Seoul. Ongoing political gridlock is delaying the implementation of fiscal stimulus measures, thereby extending the timeline for demand recovery in the market for high-value smart appliances. Although projected interest rate cuts in late 2025 may alleviate credit costs, this potential benefit is unlikely to fully mitigate the risks posed by global trade uncertainties, which continue to jeopardize employment in export-driven industries.

High Household Debt Levels Limiting Credit-Based Purchases

Korea’s household debt-to-GDP ratio remains among the OECD’s highest, constraining disposable income and curbing installment purchases for appliances. Lenders have tightened underwriting standards, making zero-interest plans rarer for mid-range models. Subscription services offer a workaround; LG projects KRW 2 trillion (USD 1.4 billion) in subscription appliance revenue for 2024[4]U.S. Department of Agriculture, “South Korea Food Ecommerce Market,” usda.gov . Consumers burdened by servicing costs may choose to terminate agreements prematurely, posing significant challenges in accurately projecting customer lifetime value. This scenario necessitates that manufacturers adopt a data-driven approach to balance the pursuit of aggressive customer acquisition strategies with the effective management of credit-risk exposure. By leveraging analytical tools and predictive modeling, manufacturers can better assess risk profiles and optimize acquisition efforts to ensure sustainable growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Robotic Leadership in Vacuum Cleaners

Vacuum cleaners held 27.12% of the South Korea small home appliance market share in 2025, while robotic variants are projected to grow at a 13.95% CAGR to 2031. The South Korean small home appliance market size for robotic vacuums will therefore expand rapidly as AI navigation, self-empty docks, and voice control become standard. By August 2024, Samsung's Bespoke AI Steam model had achieved significant market penetration, reflecting how local manufacturers strategically capitalized on enhanced security features and ecosystem integration to disrupt the dominance of Chinese competitors. Coffee makers form the next growth hotspot, propelled by premiumization and rising café culture. Specialized cooking gadgets like air fryers and waffle makers diversify revenue streams and cater to niche culinary trends among single-person households. Regulatory efficiency mandates spur R&D investment in inverter motors across product lines, ensuring future models blend performance with lower power consumption.

Sustained health consciousness sustains demand for juicers and blenders, while grills and toasters benefit from compact kitchen layouts in studio apartments. Manufacturers embed IoT chips even in smaller categories, unlocking app-based recipes and predictive maintenance alerts. Subscription or lease-to-own schemes emerge for higher-priced robotic vacuums, smoothing affordability against economic uncertainty. Cross-category brand ecosystems foster customer stickiness as consumers prefer uniform interfaces across multiple appliances. Consequently, product innovation centres on multi-functionality, smart-home compatibility, and ESG-aligned materials to capture premium margins in a maturing landscape.

By Distribution Channel: E-Commerce Dominance Reshapes Retail

E-commerce platforms commanded 45.30% of the South Korea small home appliance market size in 2025 and are slated to rise at a 15.05% CAGR, cementing digital leadership. The South Korean small home appliance market thrives on mobile shopping habits that account for a significant share of online transactions, allowing impulse purchases triggered by flash deals and influencer reviews. Quick-commerce services shorten delivery windows to hours, further eroding the relevance of physical showrooms for entry-level goods. Yet, tactile evaluation remains vital for high-end devices; thus, multi-brand stores adopt hybrid models offering on-site demos with online price matching. Specialty outlets pivot toward curated premium assortments and after-sales consultancy to safeguard share.

Cross-border e-commerce now contributes 6.3% of foreign platform sales in home appliances, introducing global competition and broader brand variety. Social-commerce livestreams gain prominence as micro-influencers demo real-time product performance, driving conversion through time-bound coupons. Brands optimize last-mile logistics via dark stores and pick-up lockers, enhancing convenience while cutting costs. Data-rich platforms like Coupang analyse grocery baskets to recommend complementary appliances, elevating average order value. Traditional retailers embracing omnichannel capacity can still prosper, though failure to digitize risks accelerated decline amid relentless online expansion.

By Technology: Smart Connectivity Accelerates Despite Efficiency Leadership

In 2025, energy-efficient units accounted for 46.70% of the South Korea small home appliance market, driven by the implementation of rebate programs and mandatory labelling requirements. However, despite their significant market share, smart-connected appliances are projected to grow at a robust CAGR of 15.60% during the forecast period, reflecting the market's transition toward AI-enabled solutions. Increasing consumer demand for features such as Wi-Fi connectivity, app-based controls, and voice integration has redefined these functionalities as standard expectations, relegating traditional models to lower-priced segments. Furthermore, the introduction of Matter 1.3 has enhanced interoperability across devices, effectively addressing prior compatibility challenges that impeded the adoption of smart appliances.

Samsung and LG synchronize efficiency and intelligence, touting 45% energy savings alongside personalized automation. Firmware-based updates extend product lifecycles and unlock recurring revenue via premium cloud services. Conventional appliances remain relevant for budget-constrained rural buyers but steadily cede urban shelf space to connected variants. As electricity tariffs rise, efficiency and smart management together define purchase criteria, encouraging R&D convergence of inverter tech, BLDC motors, and on-device machine learning. Over time, industry margins will hinge more on software subscriptions than hardware alone, reshaping competitive dynamics.

Geography Analysis

The Seoul Capital Area held 52.10% revenue share in 2025, a concentration reflecting higher disposable incomes, dense single-person living, and superior after-sales infrastructure. Affluent tech-savvy consumers here quickly adopt AI-enabled solutions and influence nationwide trends through social media. Chungcheong benefits from spillover demand owing to its proximity to Seoul and expanding industrial bases, though price sensitivity remains greater than in the capital. Yeongnam, anchored by Busan and Daegu, forms the second-largest regional market but faces export-linked economic volatility that mildly restrains premium purchases.

Honam and Gangwon exhibit slower uptake owing to rural demographics, aging populations, and service limitations. Government rural revitalization campaigns may stimulate future demand, yet near-term growth centres on urban agglomerations. Jeju Province stands out with an 11.05% CAGR forecast through 2031, driven by luxury residential developments appealing to retirees and remote workers seeking resort lifestyles. Tourism infrastructure upgrades spur sales of compact, energy-efficient appliances for rental apartments and boutique hotels. E-commerce mitigates geographic service gaps by providing direct transport to islands, but installation services still lag, presenting white space for specialized logistics firms.

Regional disparities drive manufacturers to tailor portfolios: Seoul receives cutting-edge smart-home-ready SKUs, while rural outlets emphasize durability and value. Marketing communications likewise diverge, highlighting convenience and automation in metros versus reliability and energy savings in countryside messaging. In sum, expansion beyond Seoul requires localized after-sales partnerships, modular self-service designs, and digital channels that bypass traditional retail bottlenecks.

Competitive Landscape

In 2024, dominant players captured a significant share of the market, indicating a moderately concentrated competitive environment while leaving room for niche competitors to carve out opportunities. Samsung and LG have solidified their market leadership by capitalizing on robust domestic brand equity, substantial investments in artificial intelligence research and development, and the creation of integrated ecosystems that effectively lock customers into their proprietary cloud platforms. By August 2024, Samsung's growing market share in the robot vacuum segment demonstrated the success of its rapid market entry strategy, supported by differentiated features such as advanced cybersecurity capabilities. This strategic approach underscores the importance of innovation and speed-to-market in maintaining a competitive edge within the evolving market landscape.

Specialists like Cuckoo and Coway carve out defensible positions in water and wellness devices, while international entrants such as Dyson and De’Longhi focus on premium niches. Competitive tactics revolve around AI enhancement, energy efficiency leadership, and seamless Matter-compliant connectivity. Marketing budgets increasingly funnel into live-stream and social-commerce campaigns aimed at Gen-Z renters who favor flexible ownership formats. Supply-chain resilience and domestic component sourcing gain strategic weight amid chip volatility, prompting alliances with local fabs.

Price competition intensifies in the middle tiers where Chinese brands exploit scale and low-cost structures. Korean incumbents counter by bundling extended warranties, subscription filter deliveries, and cloud analytics dashboards. Meanwhile, ESG reporting requirements raise compliance costs, advantaging larger players with sophisticated sustainability programs. Overall, rivalry will escalate around software differentiation and customer-lifetime-value maximization rather than hardware specs alone, redefining success metrics in the next five years.

South Korea Small Home Appliances Industry Leaders

Samsung Electronics

LG Electronics

Cuckoo Electronics

Coway

Philips Domestic Appliances

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Samsung Electronics and Google Cloud have strengthened their collaboration by incorporating Google Cloud's generative AI capabilities into Samsung's latest home AI companion robot, Ballie. Scheduled for consumer release this Summer, Ballie is designed to facilitate seamless, conversational interactions. The robot will assist users in efficiently managing home environments by performing tasks such as adjusting lighting, welcoming visitors, customizing schedules, setting reminders, and more.

- April 2025: Dyson introduced the Airwrap Coanda 2x hairstyler in South Korea at KRW 879,000 (USD 609), marking a new premium product launch despite the company’s 2024 sales decline.

- March 2025: Samsung Electronics unveiled the 2025 Bespoke AI Jet Ultra cordless vacuum delivering 400 W suction power, positioning it as the world’s most powerful stick vacuum.

- March 2025: Samsung rolled out its Home AI suite with Bixby-enabled scheduling and Knox security integration, introducing a platform-level expansion that links all Bespoke appliances.

South Korea Small Home Appliances Market Report Scope

The report covers a complete background analysis of the South Korean Small Home Appliance Market, which includes an assessment of the parental market, emerging trends in the segments and regional market, and significant changes in market dynamics and market overview. The report also offers qualitative and quantitative assessments, by analyzing the data gathered from industry analysts and market participants across various key points in the value chain. The market is segmented by Product into Vacuum Cleaners, Mixer/Juicer/Blenders, Toasters, Coffee Machines, Air Purifiers, and Other Products, Distribution Channel into Multi-Brand Stores, Exclusive Stores, Online, and Others. The report offers market size and forecasts for the South Korea Small Home Appliances Market in value (USD million) for all the above segments.

By Product Type

| Coffee Makers |

| Food Processors |

| Grills and Toasters |

| Vacuum Cleaners |

| Juicers and Blenders |

| Other Small Appliances (Waffle Makers, Egg Cookers, Air Fryers, Kettles, etc.) |

By Distribution Channel

| Multi-Branded Stores |

| Specialty Stores |

| E-Commerce |

| Other Distribution Channels |

By Technology

| Smart / Connected Appliances |

| Energy-Efficient (? 5-Star, Inverter) Appliances |

| Conventional Appliances |

By Geography

| Seoul Capital Area |

| Chungcheong Region |

| Yeongnam Region |

| Honam Region |

| Gangwon Province |

| Jeju Province |

| By Product Type | Coffee Makers |

| Food Processors | |

| Grills and Toasters | |

| Vacuum Cleaners | |

| Juicers and Blenders | |

| Other Small Appliances (Waffle Makers, Egg Cookers, Air Fryers, Kettles, etc.) | |

| By Distribution Channel | Multi-Branded Stores |

| Specialty Stores | |

| E-Commerce | |

| Other Distribution Channels | |

| By Technology | Smart / Connected Appliances |

| Energy-Efficient (? 5-Star, Inverter) Appliances | |

| Conventional Appliances | |

| By Geography | Seoul Capital Area |

| Chungcheong Region | |

| Yeongnam Region | |

| Honam Region | |

| Gangwon Province | |

| Jeju Province |

Key Questions Answered in the Report

How large is the South Korea small home appliance market in 2026?

The South Korea small home appliance market size reached USD 4.31 billion in 2026 and is forecast to hit USD 5.03 billion by 2031.

Which product segment leads unit sales?

Vacuum cleaners dominate with 27.12% share, and robotic variants are the fastest growers at 13.95% CAGR through 2031.

Why is e-commerce so influential in appliance sales?

Mobile-first shopping habits and quick-commerce bundling give e-commerce a 45.30% market share and a 15.05% CAGR lead.

How do government policies affect appliance demand?

Rebates on high-efficiency models, coupled with stringent labelling regulations, are driving consumer adoption of energy-efficient and smart appliances.

Which region shows the highest future growth?

Jeju Province is projected to log an 11.05% CAGR to 2031 due to lifestyle migration and tourism-driven housing upgrades.

What role does ESG play in product development?

Investor and regulatory pressure compel brands to focus on energy reduction, recycled materials, and transparent sustainability metrics.

Page last updated on: