Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

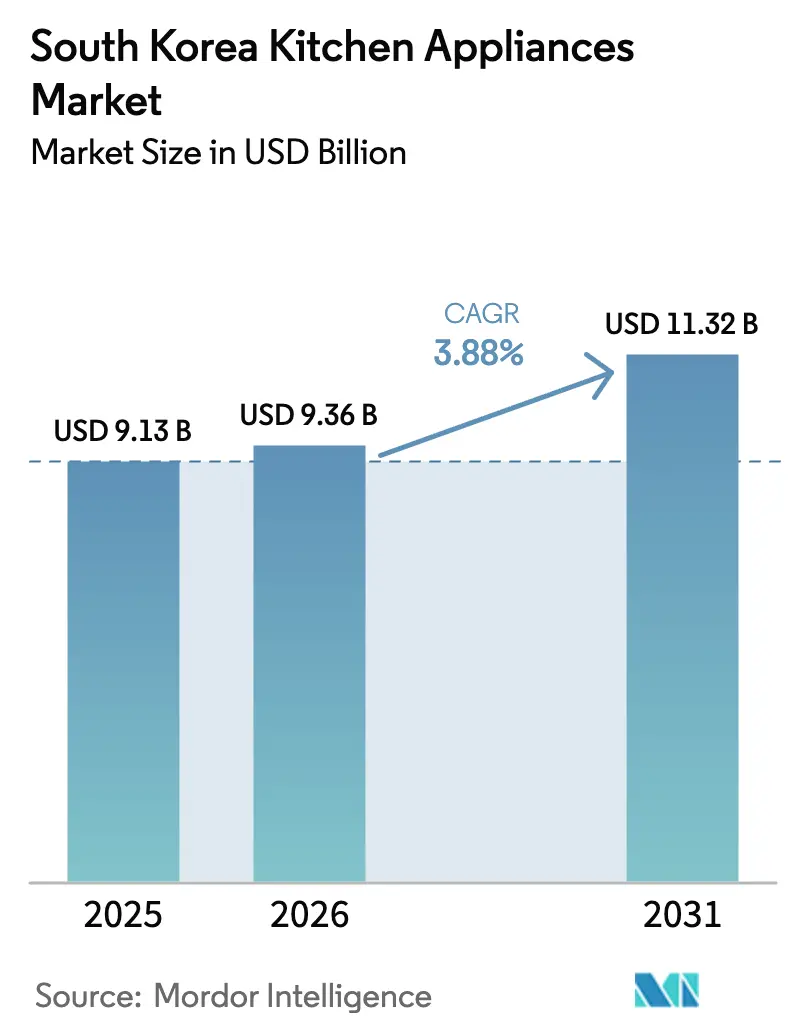

| Base Year Market Size (2025) | USD 9.13 Billion |

| Market Size (2026) | USD 9.36 Billion |

| Market Size (2031) | USD 11.32 Billion |

| Growth Rate (2026 - 2031) | 3.88% CAGR |

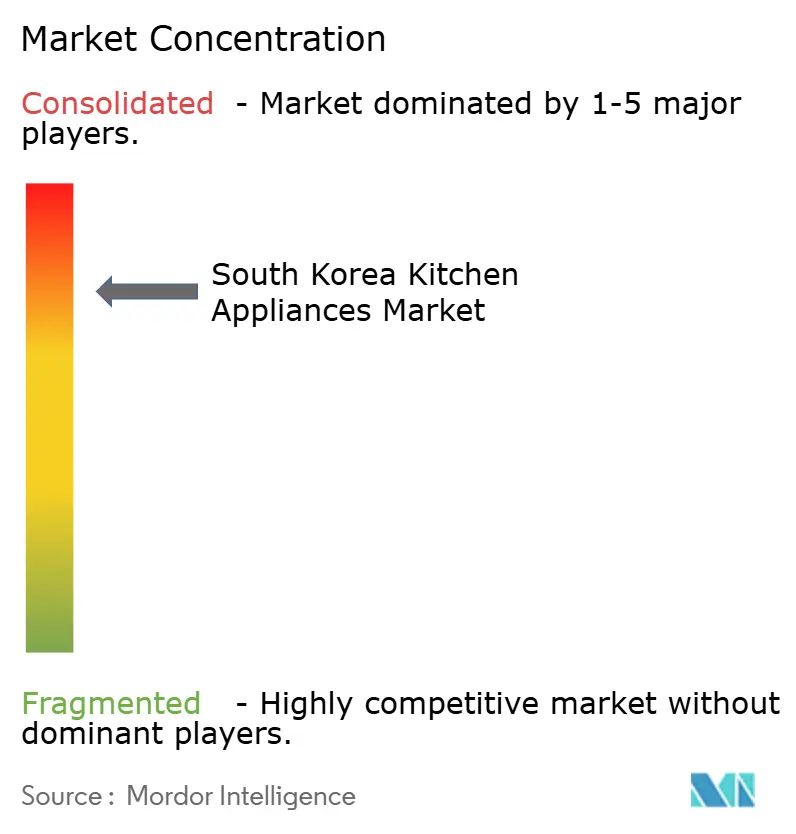

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Kitchen Appliances Market Analysis by Mordor Intelligence

The South Korea Kitchen Appliances Market size is expected to increase from USD 9.13 billion in 2025 to USD 9.36 billion in 2026 and reach USD 11.32 billion by 2031, growing at a CAGR of 3.88% over 2026–2031. Mature ownership of core categories drives growth toward higher-value replacements and connected features that justify premium pricing, supporting stable value expansion in the market. Policy incentives for Grade-1 efficiency units are accelerating upgrade cycles for refrigerators, dishwashers, and cooking products, which align with national energy goals and help lift the premium mix[1]International Energy Agency, “Korea 2025 - Energy Policy Review,” International Energy Agency, iea.org. The Korea Energy Agency’s rebate program has boosted interest in certified energy savers, making it easier for brands to steer buyers toward connected models with software-enabled features. Rapid e-commerce adoption with heavy logistics investment by platforms has raised delivery expectations, which is shifting more big-ticket transactions online in the South Korea kitchen appliances market.

Key Report Takeaways

- By product type, refrigerators and freezers led with 27.91% of the South Korea kitchen appliances market share in 2025, while dishwashers are forecast to expand at a 3.98% CAGR to 2031.

- By end user, the residential segment held 76.42% of the South Korea kitchen appliances market size in 2025 and is advancing at a 4.16% CAGR through 2031.

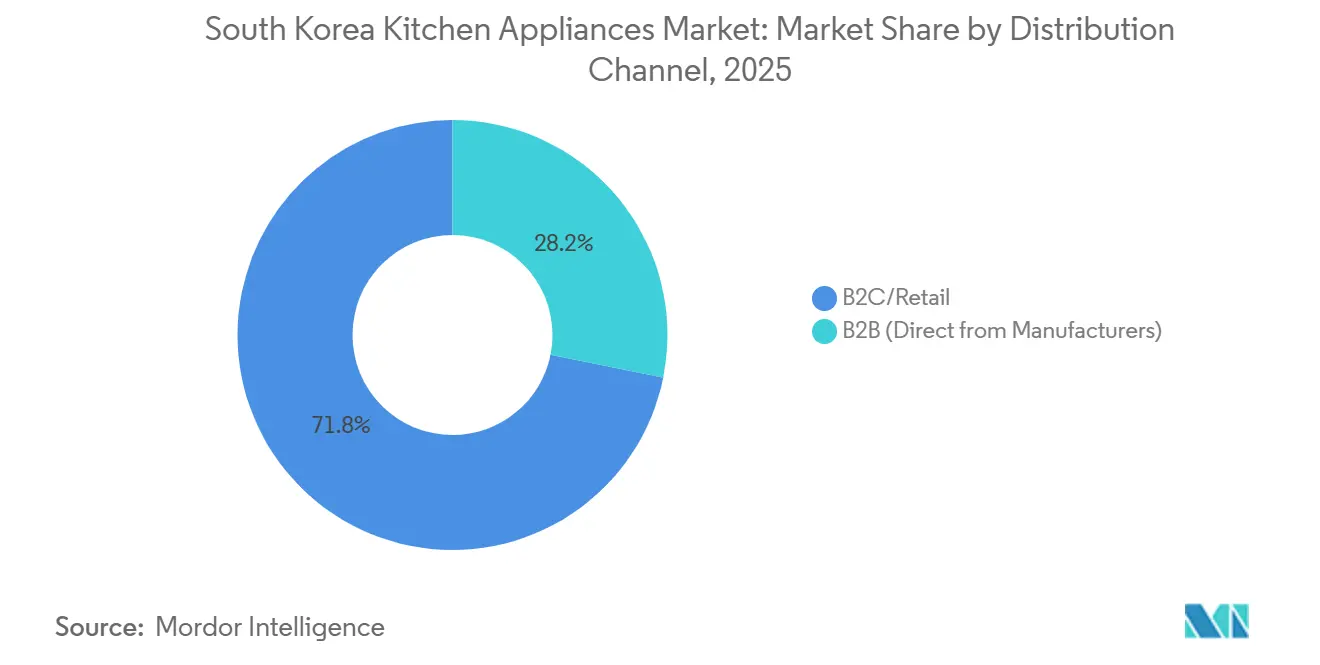

- By distribution channel, B2C/retail accounted for 71.84% of the South Korea kitchen appliances market share in 2025, and the online subsegment is projected to grow at a 4.83% CAGR through 2031.

- By geography, the Seoul Capital Area captured 39.23% of the South Korea kitchen appliances market share in 2025, and Gangwon Province is the fastest-growing region at a 4.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Kitchen Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High broadband & 5G penetration enabling smart-appliance adoption | +0.9% | National, with Seoul Capital Area and Busan leading at 55%+ 5G subscription penetration | Medium term (2-4 years) |

| Apartment renewal boom driving replacement demand | +0.7% | Seoul Capital Area, Chungcheong Region (urban renewal corridors) | Medium term (2-4 years) |

| Government "Energy Frontier" subsidies for Class-1 efficiency units | +0.6% | National | Short term (≤ 2 years) |

| Rapid growth of same-day e-commerce (Coupang, SSG.com) | +0.8% | Seoul Capital Area, spill-over to the Chungcheong and Gangwon regions | Short term (≤ 2 years) |

| An aging population seeking convenience-oriented small appliances | +0.5% | National, with the highest impact in Jeolla Region and rural areas (23.69% elderly ratio) | Long term (≥ 4 years) |

| Ultra-compact form-factor designs for micro-housing trends | +0.4% | Seoul Capital Area, Busan, Incheon (high-density urban centres) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Broadband & 5G Penetration Enabling Smart-Appliance Adoption

South Korea’s broadband footprint and 5G adoption rank among the highest in the OECD, which provides a reliable foundation for connected kitchen devices and over-the-air updates[2]Organisation for Economic Co-operation and Development, “Fibre and 5G drive OECD digital transformation as broadband markets mature,” OECD, oecd.org. Samsung’s CES 2026 showcase introduced AI Vision Inside on its Bespoke refrigerator line, which recognizes foods and supports a large-format display for guided tasks that benefit from stable connectivity[3]Samsung Global Newsroom, “[CES 2026] A Home Companion Making Daily Life More Effortless,” Samsung Electronics, samsung.com. LG’s ThinQ ecosystem now supports food recognition and recipe support across premium lines, which reflects the tight coupling of app services with hardware in the market. The government has prioritized appliance innovation within broader industry policy, which sustains investment in AI features and standards that enable interoperability at scale. Industry recognition of on-device AI progress further validates the push toward secure, data-aware product experiences that lift the appeal of premium models.

Apartment Renewal Boom Driving Replacement Demand

Flexible housing concepts are enabling residents to reconfigure kitchen footprints without heavy demolition, which supports demand for modular, built-in appliances that fit new layouts. Public-sector investments in school kitchen facilities and equipment upgrades are also driving institutional replacement cycles, which favour high-throughput dish care and food prep systems that meet safety standards[4]The Rockefeller Foundation, “Building a Public Good: Policy and Infrastructure Development in South Korea’s Universal Free Environment-Friendly School Lunch Program,” The Rockefeller Foundation, rockefellerfoundation.org. National programs that centralize sorting, storage, and distribution in School Meal Service Support Centres have expanded, which creates a steady demand stream for commercial-grade refrigeration and compliance-ready equipment. Cost-sharing rules in the Act on School Meal Services guide facility planning and procurement, which adds predictability to public kitchen upgrades. These dynamics support recurring replacement activity in urban households and institutions, which reinforces a value-led growth path for the South Korea kitchen appliances market.

Government "Energy Frontier" Subsidies for Class-1 Efficiency Units

The energy-efficiency rebate program offers a 10% refund, capped per individual, on Grade-1 appliances and has been funded through a dedicated supplementary budget, which accelerates replacement demand. The Korea Energy Agency runs the current scheme and covers a wide set of categories, including refrigerators, kimchi refrigerators, dishwashers, and rice cookers, which supports broad eligibility. Stackable brand promotions can lift total savings and strengthen the case for upgrading to premium, connected models that meet efficiency criteria, which supports mix expansion in the market. The regulator has also proposed new efficiency management coverage for additional categories such as air fryers, which will bring ratings and potential efficiency nudges to fast-growing segments. Public-sector buildings are expected to use high-efficiency appliances, which adds a defined commercial demand pool for top-rated units in the coming cycles.

Rapid Growth of Same-Day E-Commerce (Coupang, SSG.com)

Online sales captured a significant percentage of domestic retail by late 2025, and leading platforms continue to invest in logistics speed that makes same-day or next-day delivery a baseline expectation. Platform-level competition among Coupang, Naver, and SSG.com has pushed new programs such as Today Delivery and expanded overnight windows, which extend fast fulfillment to more regions. Gmarket and CJ Logistics have partnered on a guaranteed delivery date offer that covers a large assortment, including kitchenware and home appliances, which improves predictability for buyers of bulky goods in the market. Consumer satisfaction scores for dawn delivery rank very high in national evaluations, which signals that logistics performance is now central to channel choice for household devices. Cross-border e-commerce has added breadth to available products and price points in home appliances and electronics, which reinforces the online shift in the South Korea kitchen appliances market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Saturated household-ownership levels in core categories | -0.5% | National, particularly the Seoul Capital Area and other mature metro regions | Long term (≥ 4 years) |

| Flat population growth is limiting the new-buyer pool | -0.4% | National, with acute impact in rural Jeolla and Gangwon regions experiencing depopulation | Long term (≥ 4 years) |

| Semiconductor supply tightness is raising BOM costs | -0.3% | National (supply chain affects all manufacturers) | Medium term (2-4 years) |

| Stricter e-waste & plastic recycling compliance costs | -0.3% | National (Ministry of Environment regulations) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Saturated Household-Ownership Levels in Core Categories

Penetration for refrigerators and washing machines exceeds 95%, which shifts the growth engine from volume to replacement activity with an emphasis on premium features. The result is a stronger focus on design, energy savings, and connected functions that can motivate upgrades even when current units still operate. These conditions favour incumbents that deliver reliable service networks and consistent app experiences across cooking and refrigeration. Portfolio planning has moved toward higher-spec models in the South Korea kitchen appliances market, which elevates average selling prices in mature categories. In this plan, ecosystem integration and energy-rating credentials help sustain value growth even as unit growth remains limited.

Stricter E-Waste & Plastic Recycling Compliance Costs

The expanded Extended Producer Responsibility framework, effective in 2026, has widened coverage to include more electrical and electronic goods, which increases compliance costs and reporting needs for manufacturers. The rules require signing with licensed recyclers and submitting annual plans and performance reports, which adds administrative load alongside cash outlays tied to volumes in the market. Authorities have also announced a standard per-kilogram recycling cost for plastics, which sets a clear baseline for expense planning. A government-led certification plan aims to scale the use of recycled plastics in appliances, which can raise initial testing and verification costs before economies of scale set in. Over time, these steps should support circularity and provide differentiation benefits to brands with strong compliance capabilities in the South Korea kitchen appliances market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Premiumization and AI Integration Reshape Category Hierarchy

Refrigerators and freezers led the category with 27.91% in 2025, while dishwashers are the fastest-growing large appliance with a projected 3.98% CAGR to 2031 in the South Korea kitchen appliances market. AI-enabled refrigeration now offers features like food recognition, inventory cues, and guided recipes that increase daily utility and support step-up pricing. Premium ovens and cooktops are integrating camera-based cooking support and connected controls, which help standardize outcomes and reduce guesswork for time-pressed households. In parallel, Grade-1 energy ratings and rebate eligibility encourage upgrades to better-rated models in refrigeration and dish care, which dovetails with sustainability goals in the South Korea kitchen appliances market. This combination of energy performance and software features anchors a replacement-led path for value capture, which aligns with mature ownership dynamics in urban apartments.

Small appliances continue to benefit from compact living and single-person households, with rice cookers, air fryers, and compact ovens optimized for limited counter space in the kitchen appliances market. Upgrades to multi-function units that pair app support with reliable heating and cleaning performance are common, which sustains premiumization even in countertop devices. Regulatory steps to place air fryers under efficiency management from 2026-2027 will likely introduce more transparent ratings, which can help buyers prioritize energy savings during replacements. Brands that maintain consistent software roadmaps across categories can deliver smoother user journeys and longer engagement windows, which support higher retention over time in the South Korea kitchen appliances market. These attributes help makers protect share in crowded aisles where entry-level imports compete mostly on price rather than integrated experiences in the South Korea kitchen appliances industry.

By End User: Residential Dominance and Subscription Models Redefine Ownership

The residential segment accounts for 76.42% in 2025 and is projected to grow at a 4.16% CAGR through 2031, which reflects steady replacement cycles and preference for convenience features in the South Korea kitchen appliances market. Subscription bundles that include maintenance and periodic upgrades are gaining traction with city households, which reduces the need for large upfront payments and keeps devices current. Coway’s growth in rental accounts, including millions of subscribers in Korea, underscores the appeal of service-first programs that ensure uptime for water and air systems. Digital advisors that match products to household size and usage patterns are becoming part of the online journey, which helps buyers select the right mix with fewer in-store visits in the South Korea kitchen appliances market. These elements work together to shorten effective upgrade intervals and to channel buyers toward better-performing devices that qualify for rebates and deliver daily value.

Commercial demand is anchored by institutional kitchens, hospitality, and foodservice, where energy-efficient refrigeration and high-capacity dish care are priorities in the South Korea kitchen appliances market. Schools and public facilities plan equipment within defined standards and budget cycles, which creates predictable procurement for compliant units. Hotels and restaurants upgrade fleets to induction and AI-assisted ovens to lift efficiency and consistency, which reduces operating costs and helps with staffing challenges. Brands that package equipment with multi-year service contracts and uptime commitments can better meet commercial expectations, which strengthens loyalty and repeat orders in the South Korea kitchen appliances market. These practices fortify the commercial base and cushion cyclicality that may appear in discretionary residential buying.

By Distribution Channel: Online Surge and Logistics Wars Transform Retail Landscape

B2C retail holds 71.84% in 2025, and within it, the online subsegment is growing the fastest at 4.83% CAGR through 2031 as speed and convenience become decisive in the South Korea kitchen appliances market. Same-day and overnight programs now cover more geographies, which raises expectations even for bulky deliveries that require two-person handling and on-site installation. Gmarket’s guaranteed delivery date offer with CJ Logistics spans roughly 150,000 items, including kitchenware and home appliances, which increases predictability for time-sensitive orders in the market. Cross-border channels continue to widen the assortment, with home appliances and electronics rising steadily as a share of online sales baskets. These shifts are pushing retailers to tighten omnichannel execution and to integrate service scheduling into checkout flows in the South Korea kitchen appliances market.

B2B distribution is shaped by institutional tenders and service-backed contracts that price on volume, which creates a steady base across public and commercial kitchens in the market. Store networks continue to support in-person testing of premium lines, while digital channels handle most of the research and configuration steps. Policy constraints on large-format retail operating hours limit the dawn-delivery role of offline outlets, which indirectly favours logistics-first platforms that face no such restrictions in the South Korea kitchen appliances market. High satisfaction with dawn delivery has made fast shipping a standard, which compels all sellers to match service levels or risk share loss. As a result, the South Korea kitchen appliances market is consolidating around players that excel at digital merchandising, last-mile precision, and reliable post-delivery support.

Geography Analysis

The Seoul Capital Area accounts for 39.23% in 2025, reflecting higher incomes, dense single-person living, and strong adoption of compact built-in solutions in the South Korea kitchen appliances market. Same-day delivery coverage is deepest in and around the capital, which raises consumer expectations for installation-ready deliveries even for large items. Premium showrooms in core districts continue to influence purchase journeys, though a greater share of transactions now closes online after in-store testing. Urban renewal projects in extended corridors maintain replacements of built-in suites that fit flexible kitchen layouts, which sustains value capture in the market. These factors reinforce Seoul’s role as the centre of premium adoption and connected-kitchen usage.

Chungcheong has seen improvements in overnight coverage, which enables next-morning delivery of eligible products and narrows the logistics gap with the capital in the South Korea kitchen appliances market. Modular apartment design in secondary cities supports built-in replacements that favour flush-fit appliances with higher efficiency ratings, which aligns with national energy goals. In Jeolla, older age structures are shaping demand toward easy-to-use small appliances and rental service bundles, which reduce the burden of maintenance. The Rest of South Korea category, which includes Busan and Daegu, benefits from hospitality and manufacturing activity, which supports B2B orders alongside resilient household replacements.

Gangwon Province is projected to grow the fastest at a 4.04% CAGR through 2031, which reflects infrastructure upgrades and the expansion of broadband and 5G coverage into rural areas in the kitchen appliances market. The province’s hospitality nodes in ski and coastal areas sustain demand for commercial-grade dish care and refrigeration, which complements household upgrades. Aging populations in rural regions are shaping interest in intuitive water purifiers and rice cookers with simple interfaces that reduce daily friction. As digital commerce expands coverage, households outside the capital can access a wider assortment and tighter delivery windows, which lifts service expectations in the South Korea kitchen appliances market. These trends broaden the geographic demand base while keeping Seoul as the anchor for premium upgrades and software-led adoption.

Competitive Landscape

The South Korea kitchen appliances market is concentrated, with Samsung Electronics and LG Electronics together controlling about half of the category revenues, which reflects strong ecosystems, R&D depth, and nationwide service networks. Product roadmaps feature on-device AI and app-centric workflows, which connect cooking and refrigeration to content and assistance that deepen engagement. LG’s premium lines continue to emphasize guided cooking and sensor-supported features under its ThinQ umbrella, which integrates with wider smart-home routines in the South Korea kitchen appliances market. The strong domestic brand preference, omnichannel execution, and compliance capabilities raise barriers for new entrants that cannot match service reach or ecosystem cohesion. These features anchor premium pricing power in replacement cycles that dominate mature categories.

Subscription-led models complement premium equipment strategies by lowering upfront costs and guaranteeing maintenance, which sustains satisfaction over long ownership periods in the South Korea kitchen appliances market. Coway’s subscriber milestones highlight appetite for bundled care and easy filter replacement, which fit the needs of aging households and busy urban professionals. Policy alignment on recycled materials standards helps incumbents who invest in certification and vendor auditing, which turns compliance work into a strategic advantage. As fast logistics becomes table stakes, brands are investing in delivery-readiness features like packaging durability and seamless installation scheduling, which reduces friction in online conversion for the South Korea kitchen appliances market. This convergence of product, service, and logistics continues to define competitive differentiation in high-density urban markets.

International players participate in premium and niche segments with targeted built-in lines and specialty countertop devices, which adds diversity to the assortment without displacing domestic leaders in the market. Global trade dynamics have influenced manufacturing footprints for exports to North America, which led some firms to expand near-shore production to manage tariffs and delivery times. In Korea, strong expectations for service coverage and software updates make ecosystem fit an important factor in product selection. Regulatory progression on energy labelling and recycling adds momentum to eco-design investment, which favours companies with larger R&D budgets and robust supply governance. These elements collectively sustain high concentration and premium outcomes in the South Korea kitchen appliances market.

South Korea Kitchen Appliances Industry Leaders

Samsung Electronics Co., Ltd.

LG Electronics Inc.

Cuckoo Electronics Co., Ltd.

Coway Co., Ltd.

Winia Electronics (Daewoo)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Samsung Electronics showcased its Bespoke AI 4-Door Flex refrigerator with AI Family Hub+ at CES 2026, integrating Google Gemini as the first Large Language Model embedded directly into kitchen appliance hardware. The AI Vision Inside technology automatically recognizes processed foods without manual registration and monitors when items are added or removed, pushing recipe recommendations via the 32-inch touchscreen and enabling voice-commanded door opening. The innovation addresses a persistent consumer pain point, manual inventory tracking, and positions Samsung to capture premium-segment growth as smart refrigerators migrate from novelty to necessity in tech-savvy Seoul households.

- December 2025: LG Electronics unveiled its LG SIGNATURE AI lineup at CES 2026, expanding the premium brand to ten product categories, including refrigerator, oven range, dishwasher, and hood-combined microwave. The refrigerator features conversational AI based on Large Language Models that supports natural-language interactions for tailored recipe suggestions and AI Fresh technology that monitors user patterns to pre-cool the interior up to two hours before anticipated door opening. The oven range integrates Gourmet AI, which uses an internal camera to identify over 85 dishes and automatically select ideal cooking settings, and AI Browning, which monitors bread baking and sends ThinQ app notifications when preset doneness is reached.

- March 2025: KD Navien launched its new kitchen appliance brand Navien Magic in March 2025, following the acquisition of sales rights for gas stoves, electric stoves, and electric ovens from SK Magic. The expansion aims to implement a new kitchen system by integrating Navien Magic products with 3D air hoods and ventilation air purifiers to enhance indoor air quality management through smoke control during cooking. KD Navien selected chef Edward Lee as the first advertising model, with outdoor and online banner ads released on March 11, 2025, and TV commercials and digital videos planned later that month.

- March 2025: Coway Co., Ltd. won the Red Dot Design Award 2025 Best of the Best for its ICON Pro Water Purifier, marking the third consecutive year achieving the top honor. The ICON Pro, launched in October 2024, features a smart-control wheel, compact design, a Dual-Speed Extraction System for faster water dispensing, and a Smart Auto-Sterilization System. The recognition reinforces Coway’s design leadership in water purification, where it holds a strong position in tankless technology and has surpassed 10 million rental subscribers.

South Korea Kitchen Appliances Market Report Scope

The South Korea kitchen appliances market comprises a wide range of appliances designed to support food preparation, cooking, storage, and kitchen efficiency for residential and commercial users. The market is segmented by product, end user, distribution channel, and geography. By product, the market is segmented into large kitchen appliances and small kitchen appliances. Large kitchen appliances include refrigerators & freezers, dishwashers, range hoods, cooktops, ovens, and other large kitchen appliances, while small kitchen appliances include food processors, juicers and blenders, grills and roasters, air fryers, coffee makers, electric cookers, toasters, electric kettles, counter-top ovens, and other small kitchen appliances. By end user, the market is segmented into residential and commercial. By distribution channel, the market is segmented into B2C/retail (including multi-brand stores, exclusive brand outlets, online, and other distribution channels) and B2B (direct from manufacturers). By geography, the market is segmented into the Seoul Capital Area, the Chungcheong Region, the Gangwon Province, the Jeolla Region, and the rest of South Korea. The report offers the market size in value terms in USD for all the above-mentioned segments.

By Product

| Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | |

| Range Hoods | |

| Cooktops | |

| Ovens | |

| Other Large Kitchen Appliances | |

| Small Kitchen Appliances | Food Processors |

| Juicers and Blenders | |

| Grills and Roasters | |

| Air Fryers | |

| Coffee Makers | |

| Electric Cookers | |

| Toasters | |

| Electric Kettles | |

| Counter-top Ovens | |

| Other Small Kitchen Appliances |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C / Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B (Direct from Manufacturers) |

By Geography

| Seoul Capital Area |

| Chungcheong Region |

| Gangwon Province |

| Jeolla Region |

| Rest of South Korea |

| By Product | Large Kitchen Appliances | Refrigerators & Freezers |

| Dishwashers | ||

| Range Hoods | ||

| Cooktops | ||

| Ovens | ||

| Other Large Kitchen Appliances | ||

| Small Kitchen Appliances | Food Processors | |

| Juicers and Blenders | ||

| Grills and Roasters | ||

| Air Fryers | ||

| Coffee Makers | ||

| Electric Cookers | ||

| Toasters | ||

| Electric Kettles | ||

| Counter-top Ovens | ||

| Other Small Kitchen Appliances | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C / Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B (Direct from Manufacturers) | ||

| By Geography | Seoul Capital Area | |

| Chungcheong Region | ||

| Gangwon Province | ||

| Jeolla Region | ||

| Rest of South Korea | ||

Key Questions Answered in the Report

What is the current South Korean kitchen appliances market size, and how fast is it growing?

The South Korean kitchen appliances market size is USD 9.36 billion in 2026 and is projected to reach USD 11.32 billion by 2031 at a 3.88% CAGR.

Which product segment leads and which is growing the fastest in South Korea?

Refrigerators and freezers lead with 27.91% share in 2025, while dishwashers post the fastest growth at a 3.98% CAGR to 2031.

How dominant is the residential segment in South Korea's kitchen appliances?

Residential accounts for 76.42% in 2025 and is set to grow at a 4.16% CAGR through 2031, supported by premium upgrades and service-led ownership models.

Page last updated on: