Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

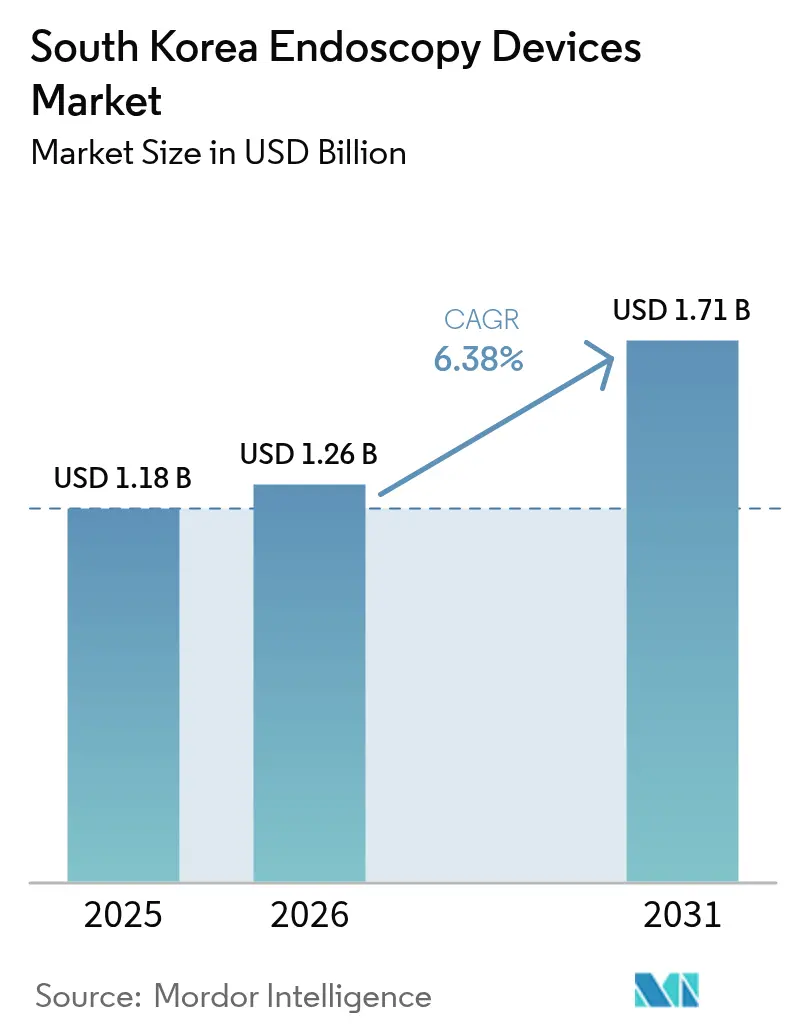

| Base Year Market Size (2025) | USD 1.18 Billion |

| Market Size (2026) | USD 1.26 Billion |

| Market Size (2031) | USD 1.71 Billion |

| Growth Rate (2026 - 2031) | 6.38% CAGR |

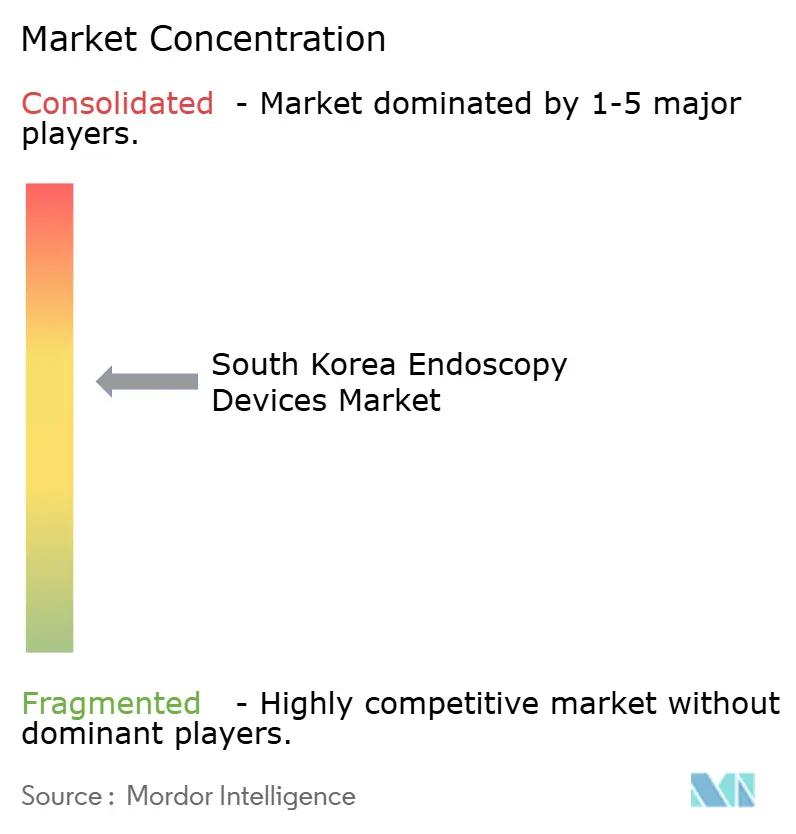

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Endoscopy Devices Market Analysis by Mordor Intelligence

The South Korean endoscopy devices market size was valued at USD 1.18 billion in 2025 and estimated to grow from USD 1.26 billion in 2026 to reach USD 1.71 billion by 2031, at a CAGR of 6.38% during the forecast period (2026-2031). This momentum is fueled by the country’s rapidly ageing population, a high burden of gastrointestinal malignancies and the swift uptake of artificial-intelligence-enabled platforms that deliver ≥95% lesion-detection sensitivity and specificity. Rising procedure volumes under the National Cancer Screening Program, widening reimbursement for complex therapies such as endoscopic submucosal dissection and the growth of ambulatory surgery centres (ASCs) are reinforcing demand. Parallel government policies—including the Digital Medical Products Act (January 2025) and the 1st Master Plan for Fostering and Supporting the Medical Device Industry—are catalysing domestic production and export capacity, while AI-driven decision support systems shorten procedure time and raise diagnostic precision. Counterbalancing forces include high upfront equipment costs, complex reprocessing rules and a shortage of skilled endoscopists outside metropolitan hubs, all of which temper adoption in smaller hospitals and clinics.

Key Report Takeaways

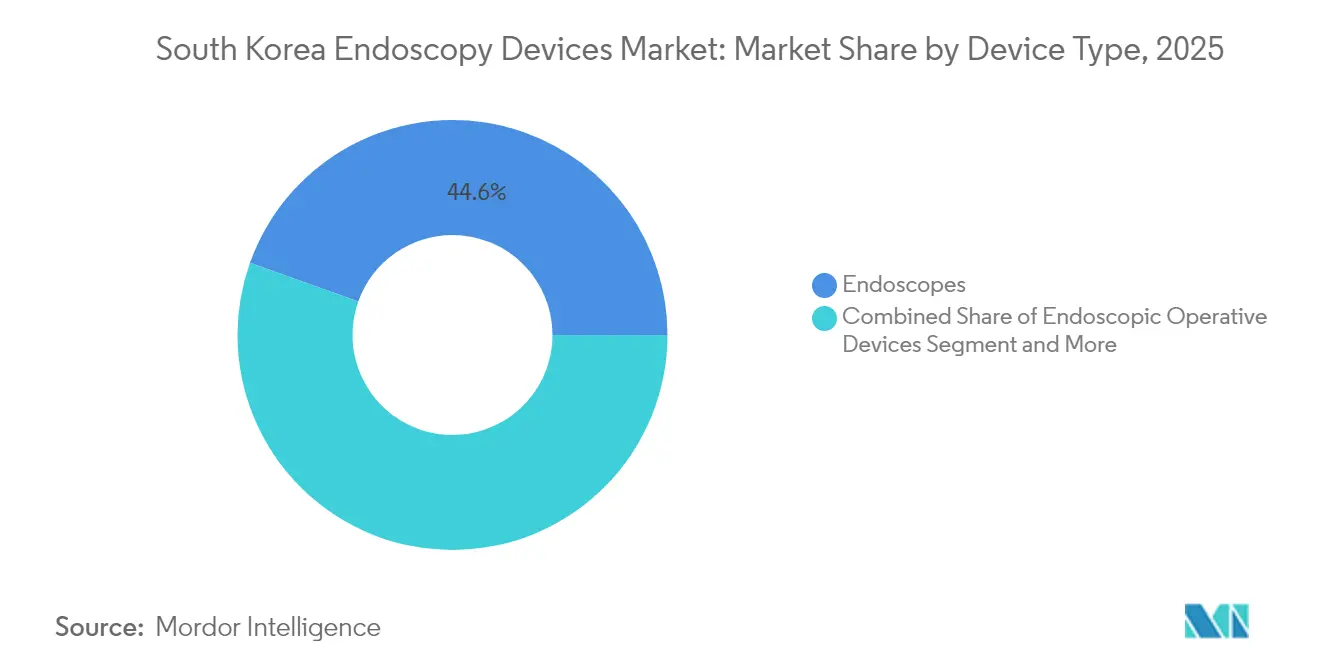

- By device type, endoscopes captured 44.55% of the South Korean endoscopy devices market share in 2025. Capsule endoscopes are projected to expand at a 13.45% CAGR through 2031, the fastest across all device types.

- By application, gastroenterology commanded 54.60% of the South Korean endoscopy devices market size in 2025 and continues to lead total procedure counts. Gynaecology is forecast to record the highest application-level CAGR at 10.6% between 2026-2031.

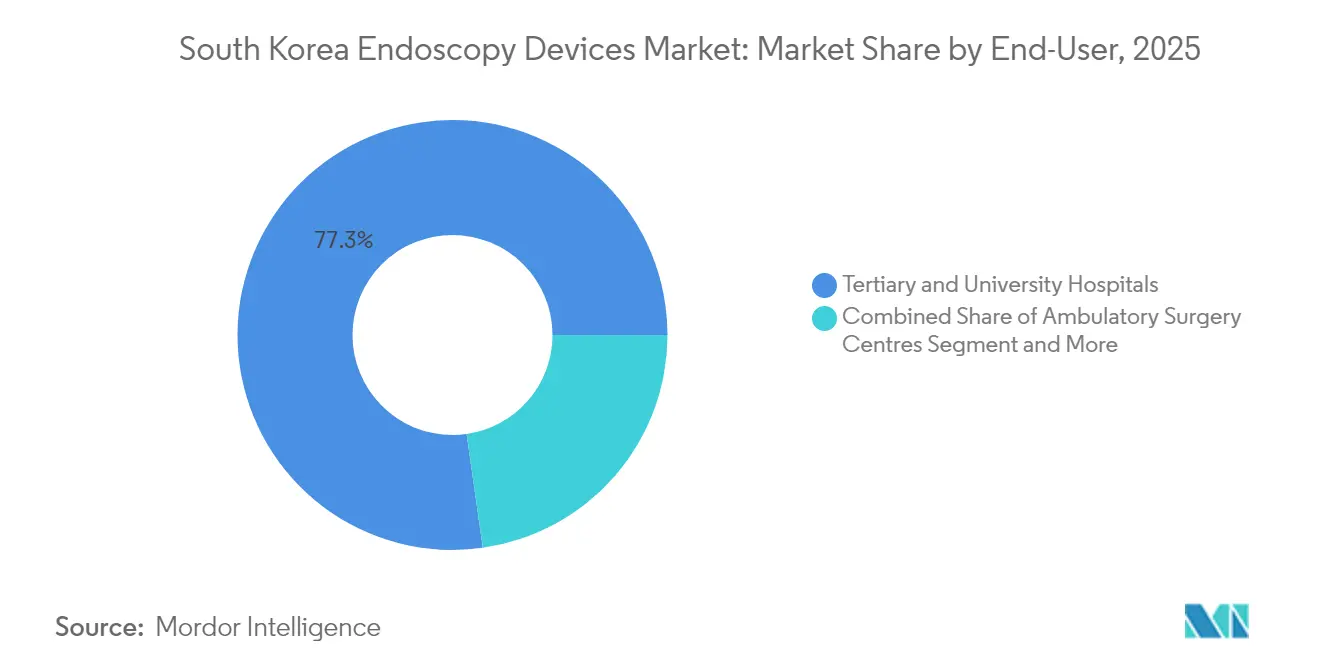

- By end-user, tertiary and university hospitals held 77.25% revenue share in 2025, whereas ASCs are set to grow at a 11.4% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of gastrointestinal & oncological disorders | +1.8% | National, higher in urban centres | Medium term (2-4 years) |

| Expansion of National Health Insurance coverage for advanced procedures | +1.2% | National | Medium term (2-4 years) |

| Government initiatives to strengthen domestic manufacturing | +0.9% | National, industrial hubs | Long term (≥ 4 years) |

| Rising adoption of ambulatory/day-case surgery models | +0.7% | Seoul, Busan, Daegu | Short term (≤ 2 years) |

| Integration of AI & robotics into workflows | +2.1% | National, tertiary hospitals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing burden of gastrointestinal & oncological disorders

South Korea documented 292,221 new cancer cases in 2024, and the gastric-cancer incidence rate of 27.0 per 100,000 ranked third worldwide. While mortality is falling 4.53% annually, the absolute patient pool rises as the median age climbs beyond 45 years. Biennial esophagogastroduodenoscopy under the National Cancer Screening Program has boosted early-stage detection, lifting 5-year survival to >70% among screened cohorts. Together these epidemiological patterns underpin sustained procedure growth, directly supporting the South Korean endoscopy devices market.

Expansion of National Health Insurance coverage for advanced procedures

Universal health coverage now reimburses high-complexity techniques such as endoscopic submucosal dissection (ESD) for early gastric cancer. National registries show a year-on-year increase in ESD since 2018, particularly among patients ≥60 years. Improved affordability propels device demand but reimbursement gaps remain; micro-costing studies reveal National Health Insurance covers only 71.7% of cystoscopy costs at large hospitals, urging policy fine-tuning[1]Uiemo Je & Byeong-Ju Kwon, “A Multicenter Micro-Costing Analysis of Flexible Cystoscopic Procedures in Korea,” icurology.org.

Government initiatives to strengthen domestic manufacturing

The 1st Master Plan (2023-2027) targets top-five global export status for medical devices, with endoscopy identified as a priority. Complementary acts such as the Digital Medical Products Act set streamlined regulatory pathways for AI-enhanced systems effective 2025. These frameworks attract foreign direct investment while accelerating indigenous R&D, reshaping the competitive field and stimulating the South Korean endoscopy devices market[2]Korea Institute for Industrial Economics & Trade, “Korea's Healthcare Industry Set to Take a Big Leap Forward,” investkorea.org.

Rising adoption of ambulatory/day-case surgery models

Seoul, Busan and Daegu report the highest penetration of ASCs, where procedure costs are 60% lower than in hospital outpatient departments and patient turnover is faster. Upper-GI endoscopies dominate ASC caseloads, driving demand for compact, reusable towers and single-use accessory kits suited to high-throughput environments[3]Fred E. Shapiro et al., “Cost Comparison Between ASCs and Hospital Outpatient Departments,” ekja.org. As payers increasingly favour site-neutral payments, the shift to ASCs should continue through 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & lifecycle maintenance costs | −1.2% | Nationwide, stronger in smaller hospitals | Short term (≤ 2 years) |

| Risk of device-related infections and complex reprocessing | −0.8% | National | Medium term (2-4 years) |

| Competition from non-invasive imaging modalities | −0.6% | Urban imaging hubs | Long term (≥ 4 years) |

| Shortage of skilled endoscopists in non-metropolitan areas | −0.9% | Rural provinces | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High capital & lifecycle maintenance costs

A multicentre 2024 micro-costing study placed average cystoscopy costs at USD 100.8 in one flagship Seoul hospital and USD 119.2 at a public facility; reimbursement covered only 71.7% and 60.6% respectively, leaving significant unfunded gaps. Maintenance and reprocessing account for nearly half of lifecycle expenses, discouraging smaller clinics from purchasing premium systems and constraining the South Korean endoscopy devices market in resource-limited settings.

Risk of device-related infections and complex reprocessing requirements

Endoscope-associated infections, although infrequent, persist because channel designs harbour biofilms. A 2024 nationwide survey recorded 98.9% adherence to reprocessing guidelines yet only 56% compliance in transporting contaminated scopes in sealed containers. Growing attention to infection control is fuelling debate on single-use solutions, but each procedure generates 1.34 kg of waste, raising environmental and cost concerns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Endoscopes Maintain Primacy as Capsules Accelerate

The endoscopes segment delivered 44.55% of the South Korean endoscopy devices market share in 2025, anchored by high-volume gastric-cancer screening and the rapid infusion of AI algorithms into conventional video scopes. Visualization systems upgraded to 4K/8K bolster diagnostic confidence in tertiary centres, while operative devices grow steadily on rising therapeutic procedures such as ESD.

Capsule systems are poised for a 13.45% CAGR through 2031, reflecting patient preference for non-invasive technologies and robust connectivity that streams images in real time. Early pilot data show technical completion rates >90% in small-bowel imaging, prompting payer discussions on broader reimbursement. Robotic-assisted platforms, though nascent, achieved an 86.1% technical success rate in colorectal ESD trials and hold promise for complex resections.

By Application: Gastroenterology Dominates Amid Broadening Clinical Footprint

Gastroenterology accounted for 54.60% of the South Korean endoscopy devices market size in 2025 and remains essential to the biennial National Cancer Screening Program that has 50% participation. Procedure volumes have rebounded to pre-pandemic levels for colonoscopy yet lag for gastroscopy among low-income cohorts, underscoring access challenges that still stimulate equipment demand in public facilities.

Gynaecology is the fastest grower at an 10.6% CAGR to 2031, propelled by outpatient hysteroscopy and laparoscopic interventions that minimise recovery time. Pulmonology, neurology/ENT and orthopaedics also expand as single-use bronchoscopes, neuroendoscopes and arthroscopes lower cross-infection risk and facilitate same-day discharge.

By End-User: Tertiary Hospitals Lead While ASCs Surge

Tertiary and university hospitals held 77.25% of revenue in 2025, relying on scale and specialist teams to support investment in AI-ready towers and robotic modules. Their dominance concentrates expertise in metropolitan areas, obliging rural patients to travel for advanced care—a dynamic that underscores the strategic significance of tele-endoscopy platforms.

ASCs, however, are forecast to log a 11.4% CAGR to 2031, energised by payer preference for cost-efficient sites and patient demand for speedier service. Gastroenterology is the anchor specialty in these facilities, where high turnover favours compact, easy-to-sterilise platforms, further broadening the South Korean endoscopy devices market.

Geography Analysis

Metropolitan zones, notably Seoul, Busan and Daegu, conduct the majority of procedures and house most AI-equipped systems, sustaining technological diffusion. Rural provinces lag because only 35% of endoscopists practice outside large cities, amplifying care inequity and lengthening waitlists. The South Korean government’s fee-for-service regime drives higher volumes in urban centres, reinforcing regional imbalances.

Pandemic-era data showed a sharper colonoscopy decline among low-income groups; recovery has remained incomplete for gastroscopy in the medical-aid population, underlining socioeconomic determinants of utilisation researchgate.net. Insurance expansion for advanced techniques is expected to narrow gaps, yet capital-budget constraints still limit adoption of cutting-edge systems outside tertiary hubs.

Continued investment in ASCs—especially in satellite cities—should disperse capacity more evenly. Coupled with mobile endoscopy vans and remote mentoring platforms, these initiatives could redistribute procedure volumes, gradually levelling the geographic spread of the South Korean endoscopy devices market.

Competitive Landscape

Olympus, Fujifilm and HOYA (PENTAX Medical) anchor the market through extensive service networks and continuous product upgrades. Olympus is piloting an “Intelligent Endoscopy Ecosystem” that integrates AI-based detection and automated reporting for release by March 2026. Fujifilm’s ELUXEO 4K offers multi-light imaging and has gained rapid traction in Seoul’s tertiary centres.

Domestic innovators are gaining ground. ENDOROBOTICS developed the ROBOPERA platform, enhancing ESD efficiency and expanding indications for early gastric lesions. Next Biomedical’s NexPowder aims to become the first Korea-registered standard haemostatic agent, addressing post-procedural bleeding gaps. Lunit’s INSIGHT platform adds AI polyp-detection overlays compatible with existing towers, offering a cost-effective upgrade path for smaller hospitals.

Strategic collaborations accelerate innovation: Medtronic’s 2025 distribution agreement with Dragonfly Endoscopy widens access to advanced pancreaticobiliary tools in East Asia. International OEMs often partner local firms for after-sales support, navigating Korea’s rigorous but transparent regulatory environment.

South Korea Endoscopy Devices Industry Leaders

Karl Storz SE & Co. KG

Olympus Corporation

Fujifilm Holdings Corp.

HOYA Corporation (PENTAX Medical)

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Korea University Anam Hospital adopted Roen Surgical’s AI-powered kidney-stone robot, Zamenix, achieving 93.5% stone-clearance in trials.

- January 2025: Korean Practice Guidelines for Gastric Cancer 2024 were issued, refining endoscopic screening recommendations.

South Korea Endoscopy Devices Market Report Scope

As per the scope of this report, endoscopy devices are minimally invasive and can be inserted into natural openings of the human body to observe an internal organ or tissue in detail. These endoscopic surgeries are being performed for imaging procedures and minor surgeries. The South Korea Endoscopy Devices Market is segmented by type of device and application. By type of device, the market is segmented into endoscopes, endoscopic operative devices, and visualization equipment. By application, the market is segmented into gastroenterology, orthopedic surgery, cardiology, gynecology, neurology, and others. Other applications include laparoscopy, bronchoscopy, and urology, among others. The report offers the market sizes and forecasts in value (USD million) for the above segments.

By Device Type

| Endoscopes | Rigid Endoscopes |

| Flexible Endoscopes | |

| Capsule Endoscopes | |

| Robotic-Assisted Endoscopes | |

| Endoscopic Operative Devices | Irrigation/Suction Systems |

| Access Devices & Ports | |

| Wound Protectors | |

| Insufflation Devices | |

| Manual Operative Instruments | |

| Visualization Systems | Endoscopic Cameras |

| SD Visualization | |

| HD Visualization | |

| 4 K / 8 K Visualization | |

| Components | Light Sources |

| Image Processors | |

| Insufflators & Pumps |

By Application

| Gastroenterology |

| Orthopaedic Surgery |

| Cardiology |

| Gynaecology |

| Neurology / ENT |

| Pulmonology / Thoracoscopy |

By End-user

| Tertiary & University Hospitals |

| General & Community Hospitals |

| Ambulatory Surgery Centres (ASCs) |

| Specialty Clinics & Offices |

| By Device Type | Endoscopes | Rigid Endoscopes |

| Flexible Endoscopes | ||

| Capsule Endoscopes | ||

| Robotic-Assisted Endoscopes | ||

| Endoscopic Operative Devices | Irrigation/Suction Systems | |

| Access Devices & Ports | ||

| Wound Protectors | ||

| Insufflation Devices | ||

| Manual Operative Instruments | ||

| Visualization Systems | Endoscopic Cameras | |

| SD Visualization | ||

| HD Visualization | ||

| 4 K / 8 K Visualization | ||

| Components | Light Sources | |

| Image Processors | ||

| Insufflators & Pumps | ||

| By Application | Gastroenterology | |

| Orthopaedic Surgery | ||

| Cardiology | ||

| Gynaecology | ||

| Neurology / ENT | ||

| Pulmonology / Thoracoscopy | ||

| By End-user | Tertiary & University Hospitals | |

| General & Community Hospitals | ||

| Ambulatory Surgery Centres (ASCs) | ||

| Specialty Clinics & Offices | ||

Key Questions Answered in the Report

What is the current size of the South Korean endoscopy devices market?

The South Korean endoscopy devices market size stands at USD 1.26 billion in 2026.

How fast is the market expected to grow?

The sector is projected to post a 6.38% CAGR, reaching USD 1.71 billion by 2031.

Which device segment is growing the quickest?

Capsule endoscopes show the highest momentum with a 13.45% CAGR forecast for 2026-2031.

What application area accounts for the largest revenue share?

Gastroenterology leads with 54.60% of revenue in 2025 thanks to nationwide gastric-cancer screening.

Why are ambulatory surgery centres important to market growth?

ASCs cut procedure costs by 60% versus hospital outpatient departments and drive a projected 11.4% CAGR in device demand through 2031.

Page last updated on: