Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

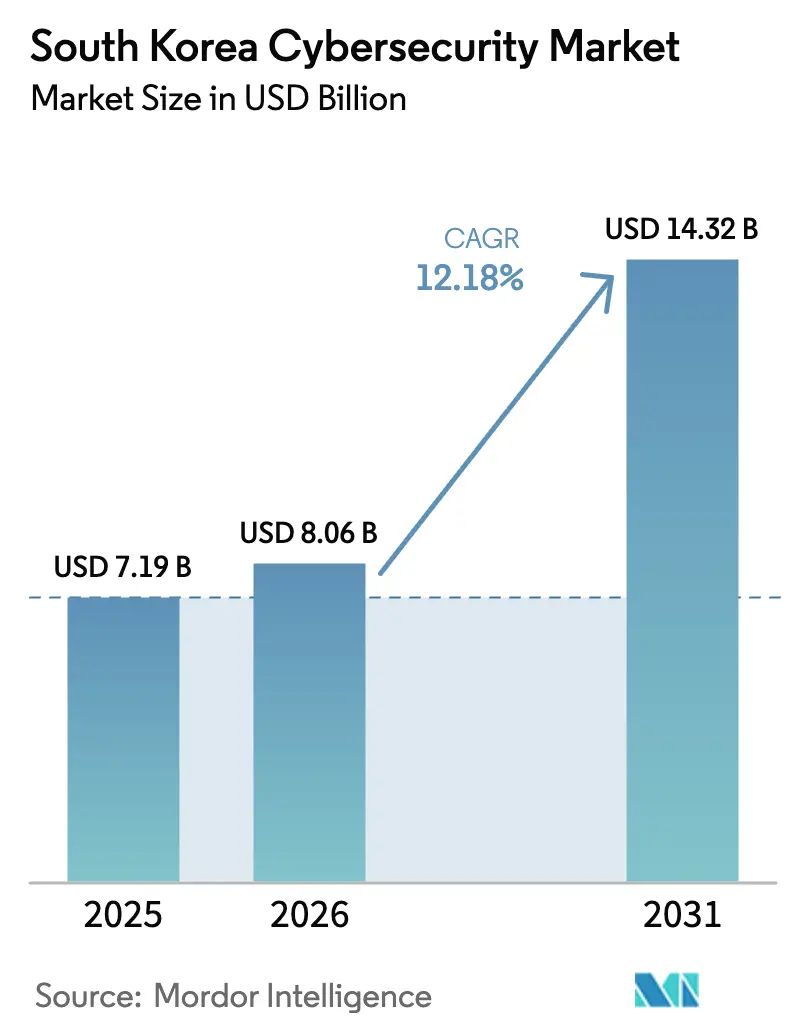

| Base Year Market Size (2025) | USD 7.19 Billion |

| Market Size (2026) | USD 8.06 Billion |

| Market Size (2031) | USD 14.32 Billion |

| Growth Rate (2026 - 2031) | 12.18% CAGR |

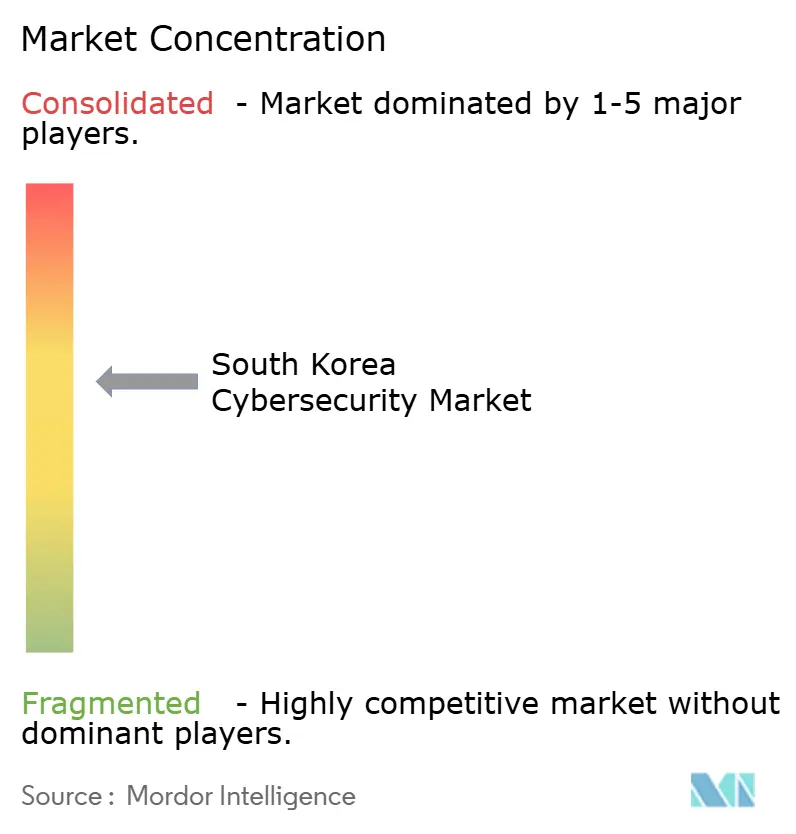

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Cybersecurity Market Analysis by Mordor Intelligence

The South Korea cybersecurity market size was valued at USD 7.19 billion in 2025 and estimated to grow from USD 8.06 billion in 2026 to reach USD 14.32 billion by 2031, at a CAGR of 12.18% during the forecast period (2026-2031). Heightened state-sponsored attacks, expanding 5G and edge roll-outs, and the government’s cloud-first Digital New Deal program are combining to accelerate security spend. Large enterprises remain the biggest buyers, yet small and medium enterprises (SMEs) are quickly raising their budgets as cyber insurance mandates and breach fines tighten. Vendors that deliver identity-centric, zero-trust architectures and managed detection and response services are capturing most growth. Local champions AhnLab, SK Shieldus, and Samsung SDS are scaling AI-driven analytics to defend against the 1.62 million daily hostile probes recorded in 2024, while global leaders Palo Alto Networks and Cisco deepen partnerships to offer unified SASE platforms. Rising salary inflation among scarce security specialists, together with heavy reliance on imported tooling, continues to push total cost of ownership 15–25% above domestic alternatives, leaving room for locally built quantum-resistant solutions.

Key Report Takeaways

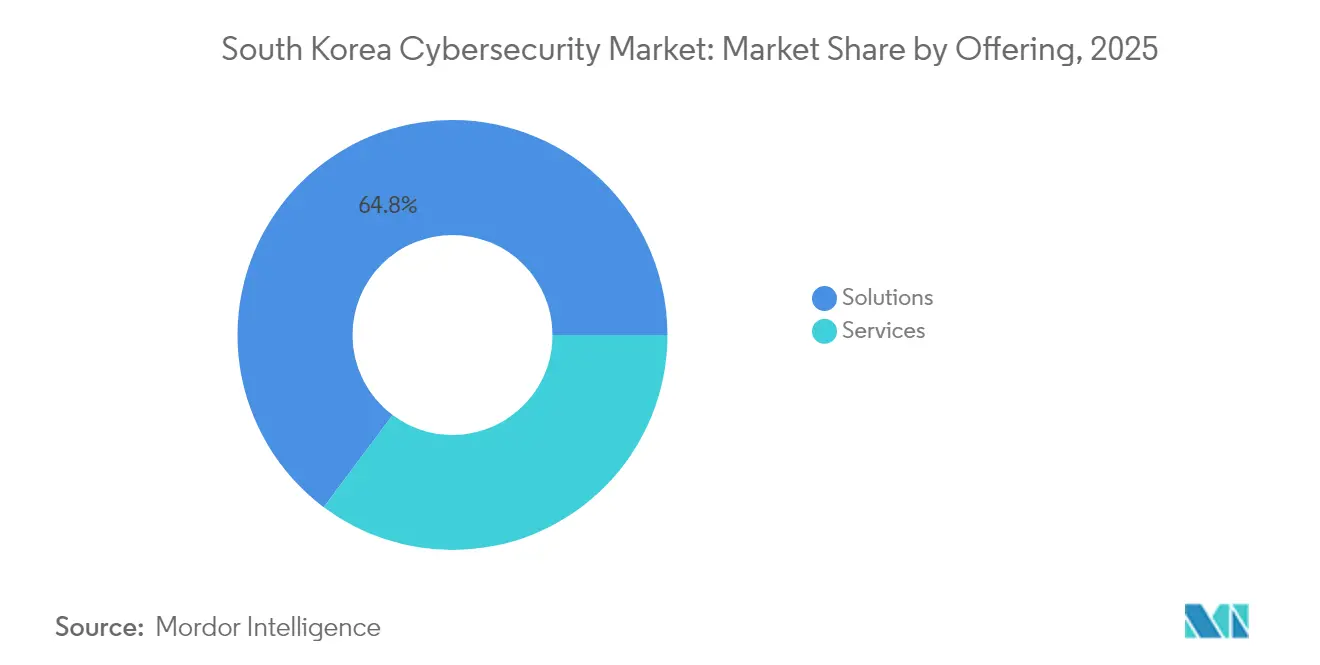

- By offering, solutions retained 64.78% of the South Korea cybersecurity market share in 2025, whereas managed services are projected to register the fastest 14.21% CAGR through 2031.

- By deployment mode, cloud models accounted for 52.27% share of the South Korea cybersecurity market size in 2025 and are set to advance at a 15.42% CAGR to 2031.

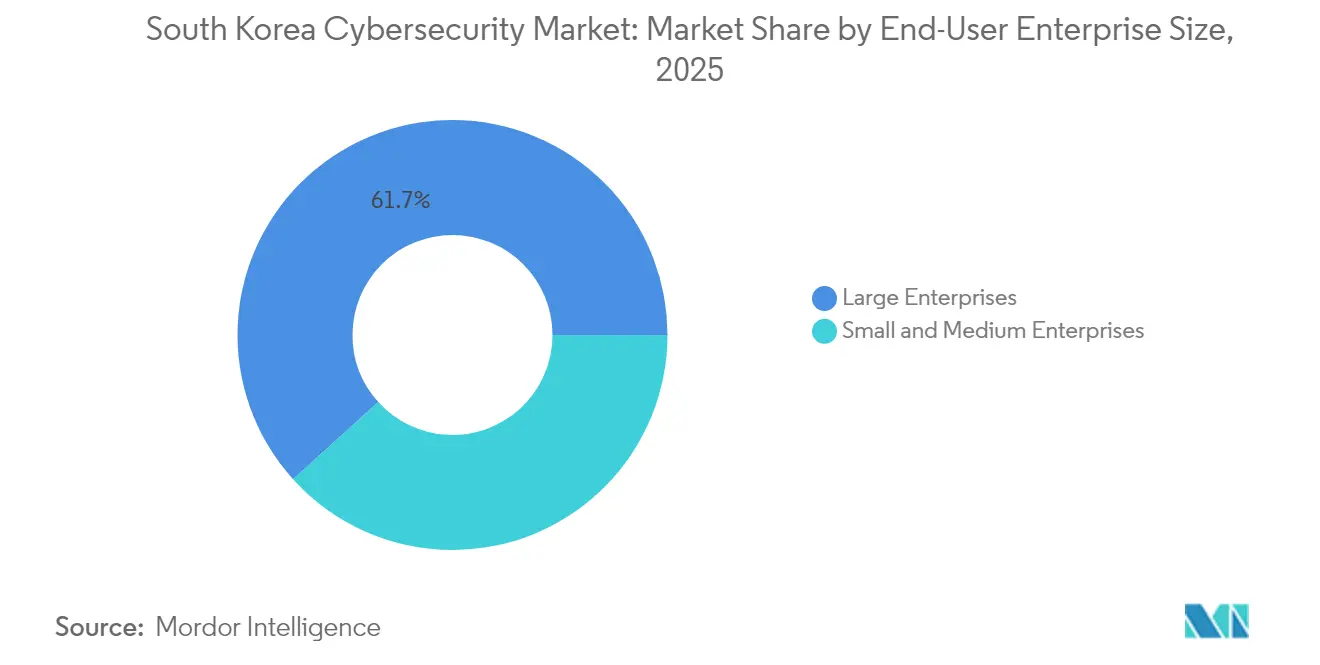

- By end-user enterprise size, large enterprises held 61.70% revenue share in 2025; SMEs are forecast to be the fastest risers at 13.78% CAGR.

- By end-user vertical, BFSI led with 31.40% revenue share in 2025, while healthcare is poised for a 15.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Korea Cybersecurity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| State-sponsored cyber-espionage escalation from North Korea | +3.2% | National, Seoul metro | Long term (≥ 4 years) |

| 5G and edge roll-out expanding attack surface | +2.8% | National, major cities | Medium term (2–4 years) |

| Digital New Deal and cloud-first mandate | +2.5% | National | Medium term (2–4 years) |

| Smart-factory and OT security demand | +1.9% | Industrial belts | Long term (≥ 4 years) |

| Enterprise shift to zero-trust and SASE | +1.4% | National | Short term (≤ 2 years) |

| Stricter PIPA and Network Act compliance fines | +1.1% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

State-sponsored Cyber-espionage Escalation from North Korea

Daily hostile probes averaged 1.62 million in 2024, cementing geopolitical tension as the primary growth catalyst for the South Korea cybersecurity market [1] Korea JoongAng Daily staff, “South Korea Faces 1.6 Million Daily Cyberattacks,” koreajoongangdaily.joins.com. The April 2025 SK Telecom breach, orchestrated with BPFdoor malware, leaked 26.96 million records and erased USD 494.6 million in market capitalization, triggering mandatory threat-hunting across telecom and defence contractors. The National Intelligence Service is now monitoring 3,200 critical facilities, while defence primes reinforce AI-based behavioural analytics that command premium pricing.

5G and Edge Roll-out Expanding Attack Surface

The installation of 80,000 5G base stations by 2024 and swift edge-computing adoption exposed 36 legacy LTE vulnerabilities, widening opportunities for lateral attacks. Operators such as SK Telecom are deploying carrier-grade firewalls to ring-fence traffic, and enterprises are adding micro-segmentation to secure IoT endpoints. Demand for near-real-time intelligence feeds is lifting revenue for cloud-delivered network analytics platforms.

Digital New Deal and Cloud-First Mandate

Government outlays of KRW 58.2 trillion (USD 44.8 billion) through 2025 have baked cloud migration into every public tender. Samsung SDS’ cloud division surged 23% to KRW 652.9 billion (USD 502.2 million) in Q1 2025 on the back of these contracts. The policy requires holistic security posture management, driving uptake of CSPM and CWPP suites that automatically enforce encryption and access controls.

Smart-Factory and OT Security Demand

Targeting 30,000 smart factories by 2025, South Korea’s industrial upgrade is colliding with poorly protected OT networks. Korea Electric Power Corporation weathered 34 incidents in H1 2024, prompting roll-out of hardened firewalls and anomaly detection on power grids. Manufacturers such as Hyundai and LG are funnelling budget into industrial IPS and digital twin monitoring to shield intellectual property.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-talent deficit and salary inflation | –2.1% | National, Seoul corridor | Long term (≥ 4 years) |

| Import-dependence raises TCO and supply-chain risk | –1.7% | National | Medium term (2–4 years) |

| Low security awareness among non-Seoul SMEs | –1.3% | Secondary cities | Medium term (2–4 years) |

| Cultural reluctance to disclose breaches | –0.9% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-talent Deficit and Salary Inflation

Qualified analysts earn KRW 58–96 million (USD 44,600–73,800) annually and vacancies are growing 15% a year, stretching budgets and slowing complex roll-outs. Universities supply limited hands-on training, so firms pivot to managed services, yet automation cannot fully offset the gap.

Import-dependence Raises TCO and Supply-chain Risk

Foreign toolsets cost 15–25% more over lifecycle owing to licensing and support fees, and geopolitical frictions threaten updates and patches. Government incentives encourage domestic R&D, but feature depth still trails imported products, forcing operators into hybrid stacks that complicate governance.

*Our updated forecasts treat driver/restraint impacts as directional, not additive. The revised impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Accelerate Despite Solutions Dominance

Solutions continued to generate 64.78% of 2025 revenue for the South Korea cybersecurity market, benefiting from sustained perimeter upgrades and identity platform refresh cycles. Managed security services, however, are charting a 14.21% CAGR to 2031 as clients outsource 24×7 monitoring and incident response. The SK Telecom breach prompted a wave of external audits, lifting demand for forensic analysis and remediation engagements. Network security appliances remain the highest-value solution class, yet unified XDR suites that collapse endpoint, email, and cloud analytics onto one console are gaining adoption. Funding momentum is evident in AI SPERA’s USD 8.5 million round that will scale automated detection for midsized clients.

Service providers are bundling compliance consulting to steer organizations through PIPA and Network Act obligations, an attractive path for SMEs unable to retain in-house counsel. As a result, the South Korea cybersecurity market size captured by services is projected to widen its share incrementally each year, improving margin mixes for integrators and telcos.

By Deployment Mode: Cloud Transformation Accelerates

Cloud deployments commanded 52.27% of revenue in 2025 and are expanding at 15.42% CAGR as government, BFSI, and healthcare workloads migrate. Prisma SASE upgrades in 2025 underscore the pivot to single-vendor platforms blending secure web gateway, zero-trust network access, and SD-WAN services. The South Korea cybersecurity market benefits from automatic patching and elastic scaling, although shared-responsibility confusion continues to spawn misconfigurations.

Hybrid topologies still dominate critical infrastructure segments that must retain on-premise controls for latency or sovereignty. Consequently, vendors offering consistent policy enforcement across clouds and data centers are securing longer contracts. Automated CSPM and container-security modules now ship pre-integrated, lowering deployment times by 30% and thus influencing purchase decisions.

By End-User Enterprise Size: SME Growth Outpaces Enterprise Investments

Large enterprises held 61.70% of 2025 revenue, but SMEs are slated to post 13.78% CAGR as cyber insurance clauses force baseline controls. Webcash and SK Shieldus have packaged endpoint defence, email filtering, and encrypted backup into monthly subscriptions, removing upfront capex for smaller firms. This tiered pricing model reduces sales cycles and is expected to lift the South Korea cybersecurity market size within the SME bracket to more than USD 2.28 billion by 2031.

Enterprises push deeper into AI-powered threat-hunting and SOAR automation, integrating playbooks that cut dwell time by 45%. Many adopt a co-managed approach, retaining core strategy in-house while offloading log-analysis spikes to MSSPs. The dual track allows vendors to cross-sell advanced modules once foundational controls are mature.

By End-User Vertical: Healthcare Surge Challenges BFSI Leadership

BFSI retained 31.40% of spending in 2025, but ransomware-plagued hospitals are seizing budgets fastest with a 15.28% CAGR outlook. Daily losses of USD 2 million during overseas hospital outages shook Korean boards into fast-tracking endpoint isolation and immutable backup roll-outs. Telemedicine growth and connected devices widen the threat plane, fuelling demand for zero-trust segmentation around patient records.

Banks and insurers sustain high outlays on anti-fraud analytics, multi-factor authentication, and mobile payment shielding. Telecom operators, utilities, and defence integrators meanwhile emphasise OT-specific safeguards that map to IEC 62443 frameworks. The South Korea cybersecurity market share enjoyed by industrial users is forecast to edge higher once smart-factory pilots graduate into scaled roll-outs.

Geography Analysis

Seoul’s metropolitan cluster accounted for nearly 59.10% of 2025 revenue, driven by headquarters of ministries, banks, and hyperscalers that collectively operate the densest array of critical assets. Concentration fosters a virtuous ecosystem: skilled labour, venture funding, and mature MSSPs co-locate, raising security baselines and pulling in further investment. Conversely, SMEs in Busan, Daegu, and Incheon lag in awareness, leaving pockets of vulnerability that attackers increasingly exploit.

Busan’s rise as a fintech and blockchain port city introduces bespoke demands for smart-contract audits, while its logistics hubs adopt supply-chain threat monitoring. Daegu’s automotive cluster is channelling budgets into SCADA firewalling and anomaly detection as it rolls out smart-factory infrastructure. National labs are pushing frontier research: Korea Institute of Science and Technology surpassed a 14% photon-loss threshold for quantum error correction in 2024, materially advancing domestic quantum-resistant cryptography capabilities that will feed into future state procurement. Government equalisation funds under the Digital New Deal are incentivising regional security incubators, yet talent scarcity outside Seoul continues to hamper project timelines. The South Korea cybersecurity market therefore shows a bifurcation where metropolitan organisations migrate to zero-trust and SASE frameworks ahead of regional peers, reinforcing managed-service uptake in outer provinces.

Competitive Landscape

The field remains moderately fragmented: the top three local vendors plus five global heavyweights control just under 60% of spend, keeping pricing competitive yet allowing niche specialists to emerge. AhnLab dominates endpoint affairs with tailored Korean-language telemetry, SK Shieldus leverages telecom reach to bundle network security with 5G services, and Samsung SDS converts cloud contracts into recurring security revenue. Among global players, Palo Alto Networks leads SASE roll-outs, Cisco integrates campus and data-center defences, and Microsoft brings identity and productivity telemetry into Sentinel analytics.

Acquisitions and joint ventures are elevating platform completeness. CrowdStrike and Fortinet aligned in January 2025 to knit endpoint signals into firewall policy enforcement, pre-empting threat escalation. Check Point’s Quantum Force appliance widened throughput four-fold via AI offload chips, grabbing telco proof-of-concepts. Domestic patent filings jumped 18% in 2024, led by quantum-safe signature schemes and unsupervised deep-learning NIDS engines, suggesting that intellectual-property depth will become a core moat for local contenders.

Regulatory alignment with the forthcoming AI Basic Act compels vendors to disclose model provenance and bias controls, favouring those with transparent development pipelines. Vendors able to bake explainability into detection alerts are expected to win public-sector tenders.

South Korea Cybersecurity Industry Leaders

IBM Corporation

Check Point Software Technologies Ltd

AVG Technologies (Avast Software s.r.o.)

Fortinet Inc.

Palo Alto Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Samsung SDS reported 23% YoY cloud revenue growth to KRW 652.9 billion (USD 502.2 million) on Digital New Deal contracts.

- February 2025: Fortinet posted USD 1.54 billion Q1 revenue, with SASE ARR at USD 1.15 billion.

- January 2025: CrowdStrike entered talks to acquire Action1 for USD 1 billion while partnering with Fortinet on integrated endpoint-to-firewall protection

- January 2025: South Korea enacted the AI Basic Act, requiring transparency mechanisms for high-impact AI and driving new compliance controls.

South Korea Cybersecurity Market Report Scope

Cybersecurity solutions help organizations monitor, report, and counter cyber threats to maintain data confidentiality. The adoption of cybersecurity solutions is expected to grow in line with the rising internet penetration among developing and developed countries. The need for cybersecurity has increased as every system in today's world is connected to the internet, making data more accessible to cybercriminals.

The South Korea cybersecurity market is segmented by offerings (solutions [application security, cloud security, data security, identity access management, infrastructure protection, integrated risk management, network security, end-point security, and other solution types] and services [professional services and managed services]), by deployment (On-premise, and cloud), by organization size (SMEs, large enterprises), by end-user vertical (BFSI, healthcare, IT and telecom, industrial and defense, retail, energy and utilities, manufacturing, and other end-user industries). The market sizes and forecasts are provided in terms of value in (USD) for all the above segments.

By Offering

| Solutions | Application Security |

| Cloud Security | |

| Data Security | |

| Identity and Access Management | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Network Security Equipment | |

| Endpoint Security | |

| Other Services | |

| Services | Professional Services |

| Managed Services |

By Deployment Mode

| On-Premise |

| Cloud |

By End-User Vertical

| BFSI |

| Healthcare |

| IT and Telecom |

| Industrial and Defense |

| Manufacturing |

| Retail and E-commerce |

| Energy and Utilities |

| Manufacturing |

| Others |

By End-User Enterprise Size

| Small and Medium Enterprises (SMEs) |

| Large Enterprises |

| By Offering | Solutions | Application Security |

| Cloud Security | ||

| Data Security | ||

| Identity and Access Management | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Network Security Equipment | ||

| Endpoint Security | ||

| Other Services | ||

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Mode | On-Premise | |

| Cloud | ||

| By End-User Vertical | BFSI | |

| Healthcare | ||

| IT and Telecom | ||

| Industrial and Defense | ||

| Manufacturing | ||

| Retail and E-commerce | ||

| Energy and Utilities | ||

| Manufacturing | ||

| Others | ||

| By End-User Enterprise Size | Small and Medium Enterprises (SMEs) | |

| Large Enterprises | ||

Key Questions Answered in the Report

What is the current value of the South Korea cybersecurity market?

The market is valued at USD 8.06 billion in 2026 and is set to expand at a 12.18% CAGR to 2031.

Which segment grows fastest within the market?

Managed security services register the quickest pace with a 14.21% CAGR, driven by talent shortages and 24×7 monitoring needs.

How large is the cloud deployment opportunity?

Cloud models already hold 52.27% revenue share and are projected to grow at 15.42% CAGR as the Digital New Deal mandates cloud-first strategies.

Why is healthcare security spending accelerating?

Hospitals endured multimillion-dollar ransomware losses, pushing the vertical toward a 15.28% CAGR through 2031.

What hampers market growth the most?

A severe cyber-talent shortage inflates salaries and caps project throughput, subtracting an estimated 2.1 percentage points from CAGR forecasts.

Page last updated on: