Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

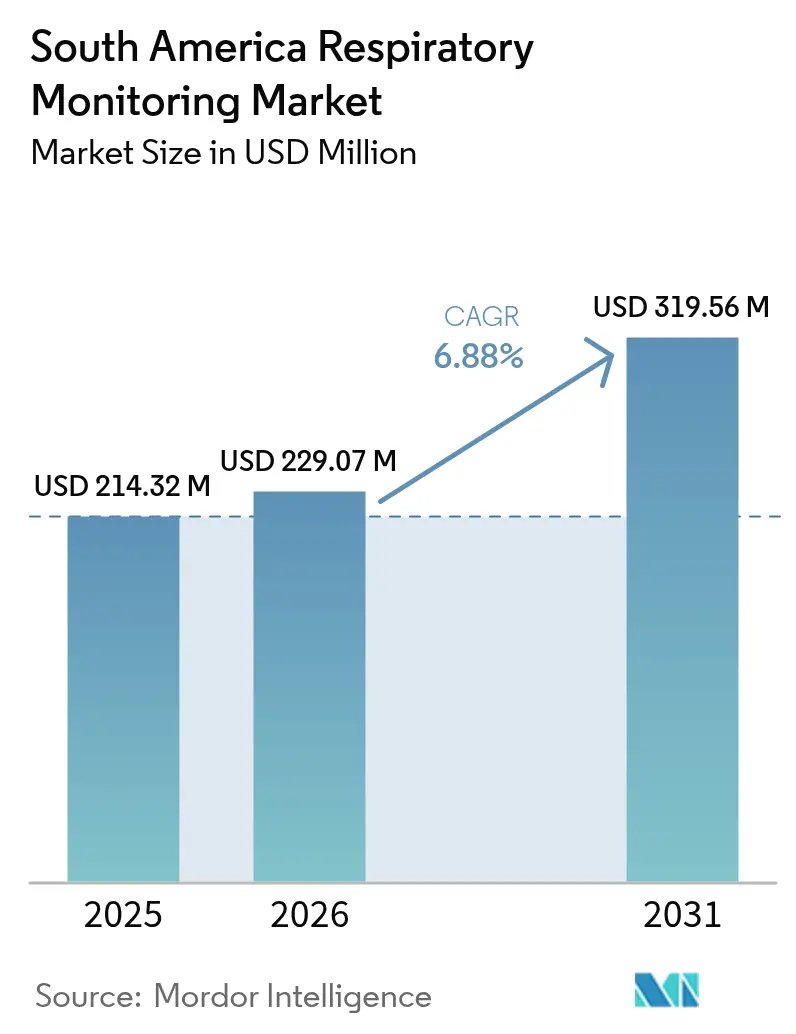

| Base Year Market Size (2025) | USD 214.32 Million |

| Market Size (2026) | USD 229.07 Million |

| Market Size (2031) | USD 319.56 Million |

| Growth Rate (2026 - 2031) | 6.88% CAGR |

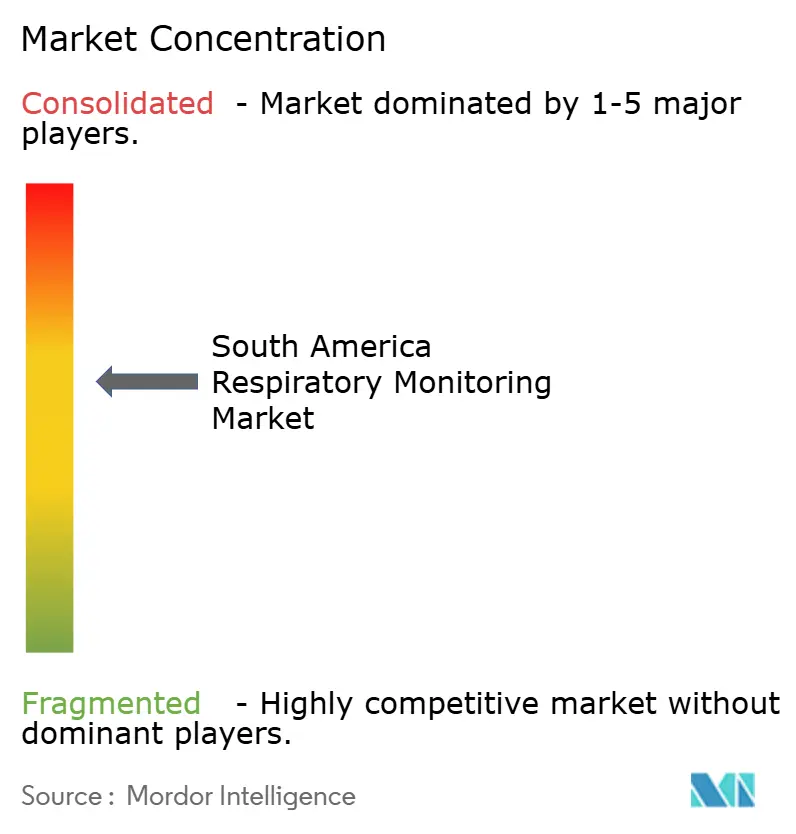

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Respiratory Monitoring Market Analysis by Mordor Intelligence

South American respiratory monitoring market size in 2026 is estimated at USD 229.07 million, growing from 2025 value of USD 214.32 million with 2031 projections showing USD 319.56 million, growing at 6.88% CAGR over 2026-2031. Digitization lessons learned during the pandemic, supportive regulatory shifts, and an aging population living longer with chronic respiratory diseases jointly underpin this steady expansion. Governments are simplifying device approvals, broadband penetration is enabling real-time data transfer, and patients are seeking continuous, home-based care that blends hardware with cloud analytics. Together, these trends are accelerating product rollout, broadening clinical applications, and opening new commercial pathways across the region. Brazil’s health ministry confirmed the lowest COVID-19 case load since 2020 in early 2025, yet national agendas still prioritize respiratory readiness, screening, and surveillance programs. Colombia’s 192% surge in respiratory telecare visits during the pandemic left a lasting digital foundation. COPD prevalence in Greater São Paulo sits at 15.8%, with 87.5% of cases undiagnosed, underscoring a large latent market for screening equipment. Capnographs, AI-enabled wearables, and cloud-connected platforms are gaining momentum, while home-care services record double-digit growth as reimbursement frameworks widen.

Key Report Takeaways

- By device type, spirometers led with a 32.70% revenue share in 2025, while capnography is set to grow at a 13.58% CAGR through 2031.

- By technology, conventional table-top units held 34.05% of the South American respiratory monitoring market share in 2025; AI-integrated and cloud-connected devices will rise at a 16.02% CAGR to 2031.

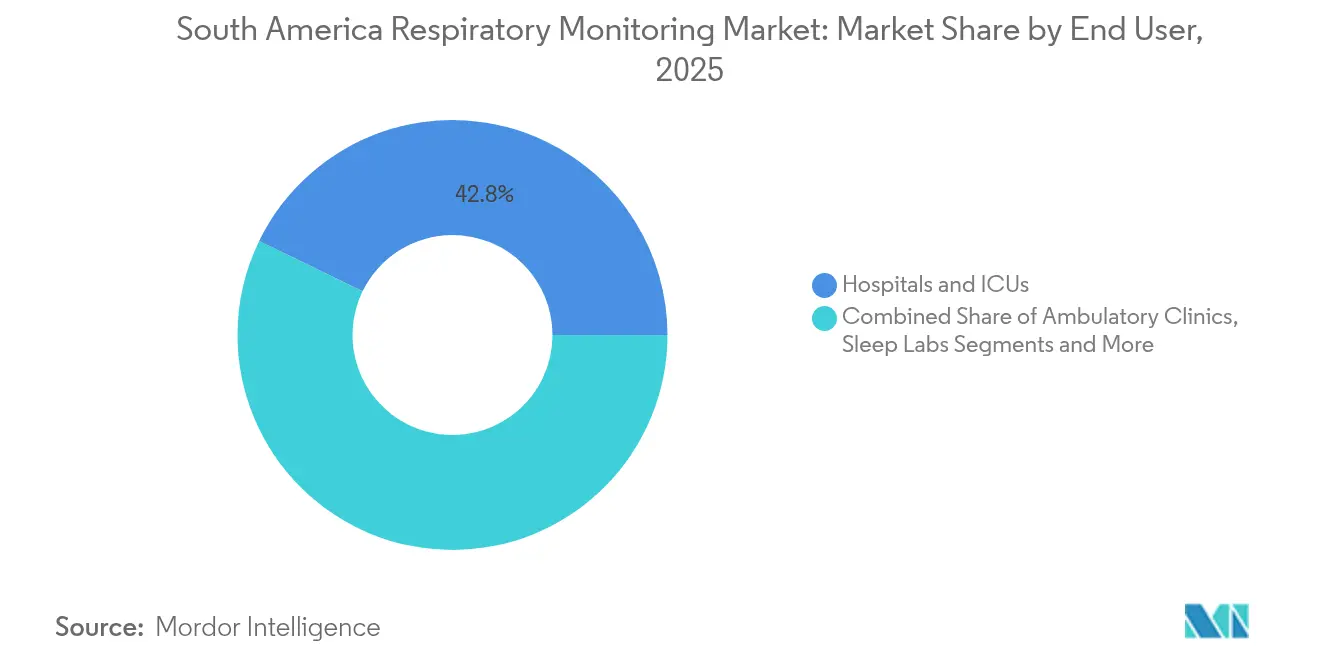

- By end user, hospitals and ICUs commanded 42.80% of the South American respiratory monitoring market size in 2025; home-care settings are projected to expand at 14.45% CAGR to 2031.

- By application, COPD accounted for 35.60% demand in 2025, whereas sleep apnea monitoring is growing at 13.82% CAGR.

- By country, Brazil captured 49.70% of 2025 revenues, while Colombia is forecast to lead growth at 11.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Respiratory Monitoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising COPD and asthma prevalence | +1.80% | Brazil, Argentina, Chile | Long term (≥ 4 years) |

| Increasing adoption of home-based respiratory monitoring | +1.50% | Urban Brazil, Colombia, Argentina | Medium term (2-4 years) |

| Technological shift toward wearable/connected devices | +1.20% | Brazil, Chile (early adoption) | Medium term (2-4 years) |

| Expansion of tele-pulmonology reimbursement in South America | +0.90% | Brazil, Colombia, Argentina | Short term (≤ 2 years) |

| Stricter occupational-safety norms in mining and agribusiness | +0.60% | Colombia, Peru, Chile mining regions | Long term (≥ 4 years) |

| Government programs for early COPD detection | +0.30% | Brazil, Argentina public health systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising COPD and Asthma Prevalence

Chronic respiratory conditions remain the region’s most persistent health challenge. COPD affects 15.8% of adults over 40 in São Paulo, and 48.4% of diagnosed patients across Argentina, Brazil, and Colombia recorded at least one severe exacerbation during a five-year follow-up, raising hospital readmission rates and costs.[1]World Bank, “Digital Health in Latin America,” worldbank.org Mining-linked pneumoconiosis reaches 42.3% among underground workers in Cundinamarca, Colombia, reinforcing the need for continuous occupational monitoring. South America’s demographic shift toward older age groups, compounded by urban pollution, ensures COPD and asthma remain primary growth engines for the South American respiratory monitoring market.

Increasing Adoption of Home-Based Respiratory Monitoring

Telemonitoring first scaled during COVID-19 and has since matured into a standard care pathway. The Brazilian Association of Sleep Medicine formalized tele-PAP guidelines that improved equipment adherence and lowered clinic load.[2]Paulo Camargos et al., “COPD Prevalence in São Paulo,” SciELO, scielo.brHome sleep tests validated by the ELSA-Brasil cohort showed strong diagnostic concordance, proving that reliable results do not require lab settings. Chile’s chronic respiratory home-care pilots reported higher patient satisfaction and better quality-of-life scores, bolstering payer confidence. With broadband and smartphone penetration climbing, clinicians can now supervise treatment plans remotely, fueling growth in the South American respiratory monitoring market.

Technological Shift Toward Wearable/Connected Devices

Artificial intelligence and miniaturized sensors are moving respiratory assessments from periodic clinic visits to 24/7 observation. Wearable acoustic devices, smart textiles, and IoT platforms now track lung parameters continuously, feeding clinicians predictive dashboards that flag exacerbations early. Validation studies show smart garments reaching correlation coefficients exceeding 0.8 against optical motion capture systems, meeting medical-grade accuracy thresholds. Cloud-based analytics transform raw signals into actionable insights, enabling timely therapeutic adjustments and driving the next adoption wave across the South American respiratory monitoring market.

Expansion of Tele-Pulmonology Reimbursement in South America

Policymakers recognize remote care’s cost savings and reach. Brazil’s Unified Health System rolled out national Tele-ICU services that link 40 hospitals and trained 14,800 professionals; user satisfaction scores remain high. Argentina’s decentralized sleep apnea network processed nearly 500 tests in two years, cutting wait times and travel expenses. Regional insurers increasingly cover virtual consults and connected device data review, cementing revenue streams for vendors operating in the South American respiratory monitoring market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost Of Advanced Devices | -2.10% | Global, with acute impact in Argentina & Rest of South America | Medium term (2-4 years) |

| Limited Reimbursement For Diagnostic Procedures | -1.80% | Brazil & Argentina core, moderate spillover to Colombia & Chile | Long term (≥ 4 years) |

| Poor Last-Mile Logistics In Amazon And Andean Interiors | -1.40% | Brazil Amazon region, Peru & Bolivia highlands, rural Colombia | Short term (≤ 2 years) |

| Shortage Of Trained Pulmonary Technicians | -1.20% | Global, with concentration in smaller markets outside Brazil-Argentina corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Advanced Devices

State hospitals and rural clinics struggle to fund AI-ready platforms that cost multiples of basic spirometers. Cheaper pulse oximeters often lack clinical validation, while premium sensors remain out of reach for many facilities, delaying technology refresh cycles. Supply-chain constraints and currency volatility add further pressure, tempering immediate penetration rates inside the South American respiratory monitoring market.

Limited Reimbursement for Diagnostic Procedures

Financing gaps persist. In São Paulo, 82.3% of identified COPD patients receive no pharmacotherapy, reflecting broader under-funding challenges.[3]Patricia Rangel et al., “COPD Treatment Gaps in Brazil,” Brazilian Journal of Medical and Biological Research, bjmbb.org Colombia’s 2025 premium hike of 5.36% lags medical inflation, squeezing provider budgets. Uneven reimbursement discourages investment in comprehensive monitoring suites and pushes clinicians to prioritize urgent care over proactive screening.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Spirometers Anchor Diagnostics While Capnographs Surge

Spirometers remain the cornerstone of pulmonary evaluation, accounting for 32.70% of 2025 revenues. Rigorous guidelines from the Latin American Thoracic Association standardize test protocols and secure ongoing purchases for primary and secondary care centers. Peak-flow meters support routine self-management, whereas full polysomnography systems address a growing sleep-disorder workload.

Capnographs post the fastest 13.58% CAGR thanks to integrations within multi-parameter monitors that visualize ventilation in real time. Partnerships such as Masimo and Philips expand installed bases in ICUs and surgical suites, reinforcing networked care models. Pulse oximetry continues to spread through home-care packs, while niche research sensors cater to specialized procedures.

By Technology: AI-Integrated Platforms Disrupt Conventional Tableside Tools

Conventional table-top hardware held 34.05% of the South American respiratory monitoring market share in 2025. Hand-held devices add portability for outpatient screening, and wireless adapters streamline data uploads to electronic records. Yet the momentum clearly favors intelligent, cloud-connected systems, which exhibit a 16.02% CAGR. Smart masks and AI-driven ventilator algorithms convert high-frequency data into forecasts of decompensation, allowing timely intervention. Vendors that combine firmware updates, analytics dashboards, and secure cloud storage continue to outpace pure hardware rivals in the South American respiratory monitoring market.

By End User: Home-Care Growth Challenges Hospital Dominance

Hospitals and ICUs contributed 42.80% of 2025 sales, reflecting legacy purchasing cycles and critical-care needs. Sleep labs, specialty clinics, and occupational health centers follow in volume. Home-care now grows 14.45% per year as payers accept remote device data in reimbursement submissions and patients favor comfort and convenience. Certified tele-respiratory programs support device dispatch, onboarding, and outcome tracking, shifting revenue away from bedside equipment toward subscription-based monitoring platforms within the South American respiratory monitoring market.

By Application: COPD Leads but Sleep Disorders Gain Momentum

COPD accounted for 35.60% usage in 2025 and remains the prime driver of baseline spirometry, oximetry, and capnography demand. Asthma maintains a stable patient base, while occupational lung diseases spur targeted screening efforts. Sleep apnea monitoring grows 13.82% annually, aided by low-cost home polygraphy kits and expanding scientific evidence linking untreated OSA with cardiovascular risk. This dual focus ensures balanced demand across chronic and episodic respiratory conditions inside the South America respiratory monitoring market.

Geography Analysis

Brazil delivered 49.70% of total revenues in 2025, underpinned by ANVISA’s streamlined approval routes, national telehealth scale-ups, and a population exceeding 200 million. Tele-ICU networks and primary-care financing reforms embed digital respiratory tools into everyday practice. Argentina leverages a mixed public-private system that speeds technology trials and niche product uptake. Colombia, forecast at 11.93% CAGR, benefits from insurance modernization and strict mining safety laws that boost surveillance spending. Chile’s clinical-trial incentives and Peru’s rural telemedicine push round out the geographic tapestry shaping growth avenues for the South America respiratory monitoring market.

Argentina benefits from decades of respiratory research, yielding qualified clinicians and established reference centers. Multi-payer reimbursement supports quick adoption of polygraphy and home PAP adherence tracking, while decentralized sleep apnea networks show that low-cost diagnostic hubs can thrive outside large cities. Fungal lung infections and overlap syndromes widen the patient pool needing periodic monitoring, further supporting device demand.

Colombia, Peru, and Chile illustrate emerging potential. Colombia’s digital push during COVID-19 normalized telecare among both patients and physicians, while mining safety codes obligate annual lung-function tests. Peru’s fragmented insurance landscape creates space for modular, subscription-based devices that bypass capital constraints. Chile positions itself as a regional innovation springboard due to streamlined ethics approvals, lower study costs, and proactive investment incentives for medical technology. Collectively these markets diversify revenue streams and stabilize the South America respiratory monitoring market against single-country fluctuations.

Competitive Landscape

Market concentration is moderate. ResMed leverages a strong cloud ecosystem that pairs connected PAP devices with subscription analytics tools. The firm reported 9-12% Latin America revenue growth through 2025, driven by rising sleep-health awareness and night-time oximetry kits. Philips and Masimo combine complementary sensor portfolios to embed capnography and regional oximetry into modular bedside monitors. At the same time, ZOLL’s acquisition of Vyaire ventilator lines broadens its presence in critical-care ventilation. Medtronic’s recent launch of a mobile ECMO platform illustrates how incumbents extend into advanced respiratory life support.

Start-ups scale rapidly in wearable acoustics, smart textiles, and AI-driven risk stratification, often partnering with public hospitals for real-world validation studies. Regulatory harmonization, cloud hosting within national borders, and cybersecurity guidance from PAHO reduce entry barriers.

Over the forecast horizon, competition in the South American respiratory monitoring market will pivot on longitudinal data services, clinical-decision dashboards, and integrated reimbursement support rather than on standalone hardware performance alone.

South America Respiratory Monitoring Industry Leaders

Dragerwerk AG

Koninklijke Philips N.V.

Medtronic Plc

Masimo

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: ZOLL closed the acquisition of select Vyaire Medical ventilator product lines, including Bellavista and LTV systems.

- September 2024: Medtronic introduced VitalFlow, an intra-hospital ECMO system designed for transport-ready cardiopulmonary support.

- June 2024: Masimo and Philips deepened their collaboration to integrate NomoLine capnography into IntelliVue MX monitors.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the South America respiratory monitoring market as all devices whose primary purpose is to record or display breathing-related parameters, flow, pressure, volume, gas concentration, or oxygen saturation, during diagnosis, triage, treatment, or long-term follow-up across clinical and home settings. According to Mordor Intelligence, this spans spirometers, peak-flow meters, polysomnography systems, gas analyzers, pulse oximeters, and capnographs that are sold new through medical distributors, e-commerce, or direct hospital tenders across Brazil, Argentina, and the Rest of South America.

Scope exclusion: purely therapeutic ventilators and oxygen concentrators are outside this sizing.

Segmentation Overview

- By Device Type

- Spirometers

- Peak Flow Meters

- Sleep Test/Polysomnography Devices

- Gas Analyzers

- Pulse Oximeters

- Capnographs

- Other Devices

- By Technology

- Conventional Table-top

- Hand-held

- Wearable / Patch-based

- Wireless-enabled (Bluetooth/Wi-Fi)

- AI-integrated & Cloud-connected

- By End-user

- Hospitals & ICUs

- Ambulatory Surgical & Specialty Clinics

- Sleep Laboratories & Diagnostic Centres

- Home-Care Settings

- Occupational Health & Industrial Sites

- By Application

- COPD

- Asthma

- Sleep Apnea

- Pulmonary Fibrosis & ILD

- Respiratory Infections (incl. COVID-19)

- Others

- By Country

- Brazil

- Argentina

- Rest of South America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed pulmonologists, biomedical engineers, and medical-device distributors in Sao Paulo, Buenos Aires, and Bogota, followed by surveys of home-care providers. These conversations validated installation rates outside capital cities, clarified public versus private procurement splits, and stress-tested model assumptions on device replacement cycles.

Desk Research

We began by mapping disease burden and care infrastructure through open datasets from the Pan American Health Organization, Brazil's DATASUS, Argentina's INDEC health accounts, UN Comtrade customs codes for HS 901819, and peer-reviewed journals that track COPD and asthma prevalence. Trade association briefings from the Latin American Thoracic Society and import duty filings refined typical device mix and channel margins. Company filings collected through D&B Hoovers and news streams on Dow Jones Factiva offered supplier revenue cues and recent average selling prices. The sources mentioned illustrate, rather than exhaust, the secondary pool that underpins our evidence base.

Market-Sizing & Forecasting

A top-down demand pool was built by reconstructing procedure volumes from hospitalization records and home-care enrollments, then applying device usage frequencies and replacement intervals. Select bottom-up roll-ups of leading supplier shipments and channel checks anchored unit counts. Core variables, COPD and asthma prevalence, ICU bed additions, sleep-lab penetration, home-care reimbursement policy shifts, and average selling price erosion, drive the model. A multivariate regression links these indicators to annual device uptake, while ARIMA smoothing manages short horizon fluctuations. Gaps in supplier data are bridged by proportional allocation using import value shares and verified clinician usage norms.

Data Validation & Update Cycle

We triangulate outputs against import statistics, hospital purchase disclosures, and sampled distributor invoices. An anomaly review panel reworks any variance above five percent before sign-off. Models refresh every twelve months, with mid-cycle checks when material regulatory or epidemic events emerge, ensuring clients receive an up-to-date baseline.

Why Mordor's South America Respiratory Monitoring Baseline Stand Out for Reliability

Published figures often diverge because firms choose different regional cuts, bundle therapeutic hardware, or uplift values with undisclosed mark-ups.

Key gap drivers include some publishers merging Latin America with the Caribbean, others counting ventilators and oxygen systems, and many relying on global ASP benchmarks without validating local discounts or currency movements.

Mordor's study isolates monitoring-only devices, applies country-specific price audits, and updates exchange rates at each refresh, which tempers extremes seen elsewhere.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 214.32 million (2025) | Mordor Intelligence | - |

| USD 1.40 billion (2024) | Regional Consultancy A | Bundles therapeutic ventilators and covers wider Latin America |

| USD 199.74 million (2025) | Trade Journal B | Omits Colombia and relies on 2023 ASPs without inflation adjustment |

These contrasts show that Mordor's disciplined scope, variable selection, and annual refresh cadence produce a balanced, transparent baseline that decision-makers can trace back to clear, reproducible steps.

Key Questions Answered in the Report

What is the current size of the South America respiratory monitoring market?

The market is valued at USD 229.07 million in 2026 and is projected to reach USD 319.56 million by 2031.

Which device category leads sales in South America?

Spirometers account for the largest revenue share at 32.70% thanks to their established role in routine lung-function testing.

How fast is the home-care segment growing?

Home-care settings are forecast to grow at a 14.45% CAGR between 2026 and 2031 as telemonitoring gains reimbursement support.

Which technology segment shows the highest growth potential?

AI-integrated and cloud-connected devices post the fastest 16.02% CAGR, reflecting demand for continuous, data-driven care.

Why does Colombia present an attractive growth opportunity?

The country combines a 11.93% forecast CAGR with new mining safety laws and a post-pandemic telehealth infrastructure that encourages respiratory equipment adoption.

Page last updated on: