Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.01 Billion |

| Market Size (2026) | USD 9.37 Billion |

| Market Size (2031) | USD 11.38 Billion |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Cosmeceutical Market Analysis by Mordor Intelligence

The South America cosmeceutical market size is expected to grow from USD 9.01 billion in 2025 to USD 9.37 billion in 2026 and is forecast to reach USD 11.38 billion by 2031 at 3.96% CAGR over 2026-2031. The growing influence of dermatologists, a surge in e-commerce, and the region's rich biodiversity are transforming high-efficacy formulations from luxury items to clinical essentials, allowing for premium pricing in both pharmacies and online platforms. Local pharmaceutical firms are hastening acquisitions to bolster their skin-health portfolios and utilize their established prescription-drug logistics. In response, multinational companies are deploying AI-driven diagnostics, streamlining the journey from virtual consultation to purchase. Regulatory advancements, like ANVISA’s RDC 907/2024 sandbox, are slashing bioactive time-to-market by roughly 18 months, giving an edge to early adopters. While challenges like currency fluctuations, counterfeit infiltration, and gaps in active ingredients pose hurdles, strategies such as product hybridization, smaller packaging, and tamper-proof seals are mitigating risks throughout the value chain.

Key Report Takeaways

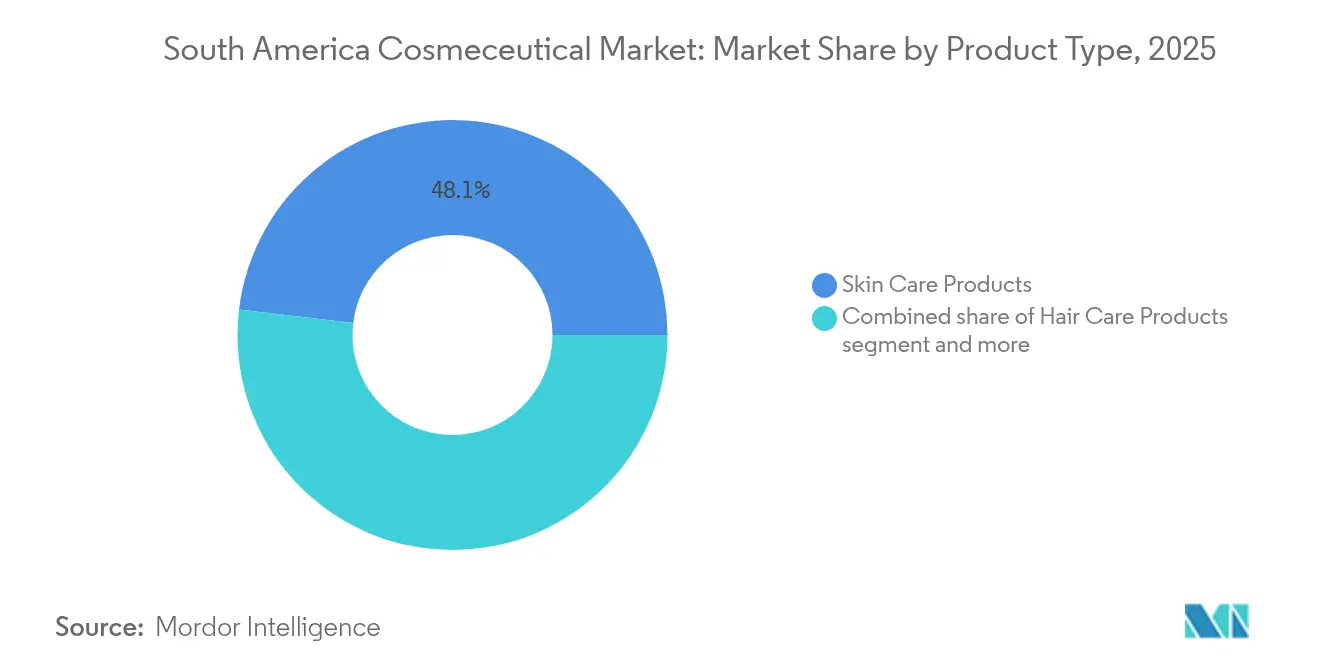

- By product type, Skin Care Products led with 48.10% of the South America cosmeceutical market share in 2025, whereas Hair Care Products are forecast to grow at a 9.45% CAGR through 2031.

- By category, Conventional formulations commanded 67.85% of revenue in 2025, while Natural/Organic products are set to expand at an 8.34% CAGR to 2031.

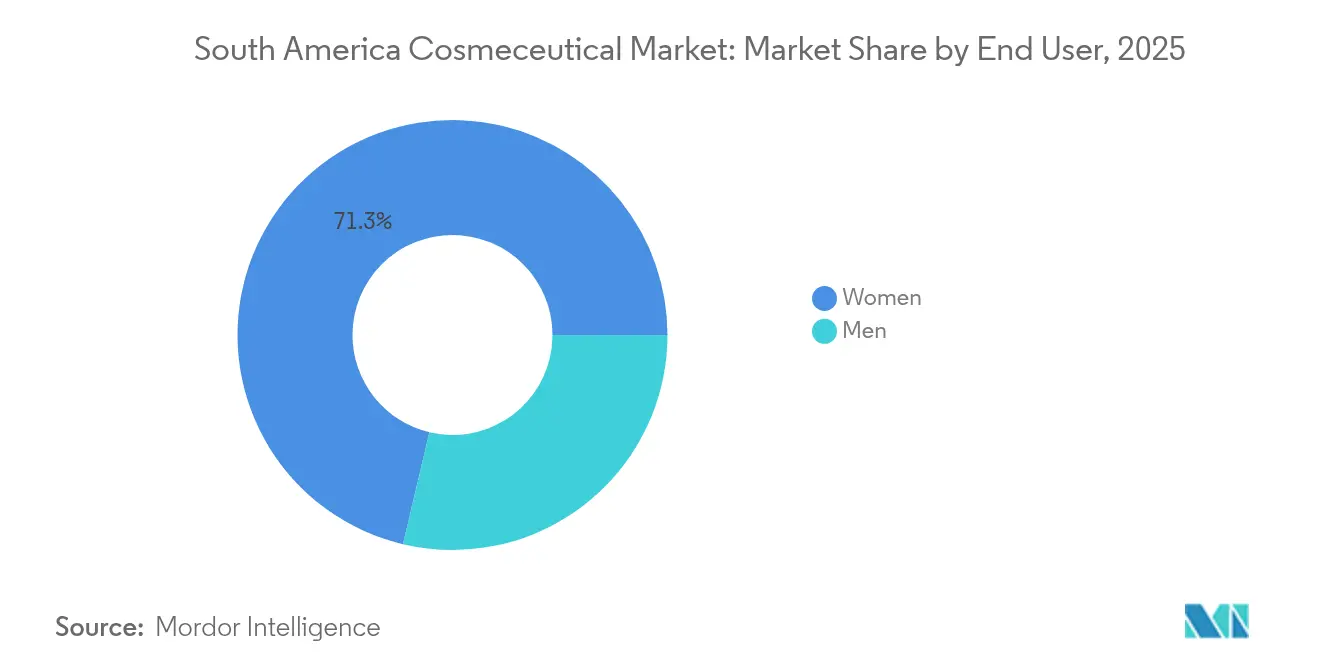

- By end user, Women accounted for 71.30% of 2025 spend, yet the Men’s segment is projected to rise at an 7.66% CAGR through 2031.

- By distribution channel, Supermarkets and hypermarkets captured 46.05% of 2025 sales, while online retail is on track for an 7.85% CAGR to 2031.

- By geography, Brazil held 61.05% of 2025 revenue, and Argentina is expected to record a 7.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Cosmeceutical Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising premium skin-health consciousness and dermatologist influence | +1.2% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Digital and e-commerce penetration in beauty retail | +1.0% | Brazil, Argentina, Chile | Short term (≤ 2 years) |

| Botanical bio-actives from Amazon and Andean biomes | +0.8% | Brazil, Peru, Colombia | Long term (≥ 4 years) |

| AI-driven personalized skin diagnostics and product customization | +0.6% | Brazil, Colombia, Argentina | Medium term (2-4 years) |

| Pharma convergence and mergers and acquisitions fueling high-efficacy formulations | +0.9% | Brazil, Argentina | Short term (≤ 2 years) |

| Physician-dispensed channel expansion via tele-dermatology | +0.5% | Colombia, Brazil, Peru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising premium skin-health consciousness and dermatologist influence

In South America, dermatologists are evolving from mere prescribers to proactive brand advocates, a shift that is transforming cosmeceuticals from optional buys to essential clinical products. Data from ABIHPEC reveals that Brazil's dermocosmetics market is expanding, with brands exclusive to pharmacies reaping the lion's share of revenues[1]Source: Associação Brasileira da Indústria de Higiene Pessoal, Perfumaria e Cosméticos, “Panorama do Mercado 2024,” abihpec.org.br. In 2024, L'Oréal Brazil notched up BRL 3.3 billion (USD 660 million) in sales through pharmacies. With an ambitious goal to double its total revenue by 2027, the company is weaving dermatologist training programs into its market approach. Galderma is marketing hyaluronic acid fillers and PLLA biostimulatory agents as "conscious self-care" for the youth. This move underscores a wider trend: aesthetic treatments and home-use cosmeceuticals are increasingly offered in subscription packages, generating consistent revenue streams that outpace traditional cosmetics. In 2024, Natura reintroduced its Chronos Derma line, now featuring clinically trialed retinol concentrations. This move underscores a pivotal shift: even brands traditionally reliant on direct sales are now prioritizing clinical efficacy over brand legacy. As a result of this physician-driven demand, product lifecycles are shrinking. Formulations lacking peer-reviewed efficacy are swiftly losing ground on shelves to their clinically validated counterparts, often within just 12 to 18 months of their debut.

Digital and e-commerce penetration in beauty retail

In 2024, e-commerce platforms are breaking down the geographic barriers that once shielded retailers in tier-1 cities. This shift allows brands to connect with consumers in secondary markets without the need for physical distribution investments. MercadoLibre, a major player in Latin America, successfully shipped 1.377 billion items in 2024. Notably, 76% of these deliveries were made within 48 hours. This efficiency has effectively addressed the logistics challenges that once limited access to premium cosmeceuticals outside major cities like São Paulo, Buenos Aires, and Bogotá. In October 2024, Natura forged a partnership with MercadoLibre in Brazil. By the end of the year, this collaboration had expanded to Argentina. The partnership seamlessly integrates Natura's 3 million direct-sales consultants with MercadoLibre's fulfillment network. This innovative approach melds personal recommendations with algorithm-driven upselling. Brazilian indie brand, Care Natural Beauty, showcases the potential of direct-to-consumer sales. The brand earns a significant 80% of its revenue from its own e-commerce platform, reserving just 20% for sales through Sephora and other third-party marketplaces. This strategy underscores the viability of maintaining premium pricing without compromising on retailer margins. In 2024, ANVISA, Brazil's health regulatory agency, set up an e-commerce working group[2]Source: Agência Nacional de Vigilância Sanitária, “RDC 907/2024 Regulatory Sandbox,” gov.br/anvisa. Their goal is to standardize online cosmetic sales regulations across states. This move indicates a shift in regulatory perspectives, leaning towards embracing digital-first distribution. In Argentina, the impact of this shift is especially evident. Faced with hyperinflation, consumers began real-time price comparisons across various platforms. This behavior turned transparent online pricing into a significant competitive edge, rather than merely a tactic to undercut prices.

Botanical bio-actives from amazon and Andean biomes

Ingredients derived from biodiversity are evolving from mere marketing narratives to patented actives, now backed by quantified clinical endpoints. This shift is reshaping formulation strategies across the region. In 2024, peer-reviewed studies revealed that oils from the Amazon, specifically piciá, babassu, açaí, and andiroba, showed tangible benefits in reducing transepidermal water loss and boosting collagen synthesis. Such findings provide the necessary efficacy data, allowing these products to command premium prices in pharmacies. Meanwhile, Andean botanicals like quinoa peptides, amaranth lipids, and lupin proteins are making their way into anti-aging products. Their concentrations have been validated through in vitro studies, and patent filings at Brazil's INPI have surged by 22% year-over-year in 2024. In a significant move, Natura's Vision 2050 has set its sights on sourcing from 46 communities spread over 2.2 million hectares of forest. With an ambitious target of expanding to 3.0 million hectares by 2030, Natura is backing its commitment with a substantial investment of BRL 230 million (USD 46 million) over five years, focusing on the bioeconomy. Brazil's Lei 13.123/2015 ensures that when indigenous communities' traditional knowledge aids in commercial formulations, they receive their due royalties. This benefit-sharing mandate for genetic resources creates a regulatory edge for Brazilian brands. Such a framework is challenging for competitors in Asia and North America to emulate, given the absence of similar legislative structures. The implications are profound: brands that forge benefit-sharing agreements now position themselves to dominate supply chains for bioactives, potentially sidelining competitors who might take a decade to find alternative sourcing.

Artificial Inteligence-driven personalized skin diagnostics and product customization

AI-driven diagnostics are shortening the gap between skin assessments and product recommendations, paving a seamless route from consultation to purchase, entirely sidestepping traditional retail. In Colombia, Revieve has teamed up with Beautycalia, utilizing computer vision algorithms to analyze conditions like hyperpigmentation, melasma, and photoaging in real-time. This partnership crafts personalized regimens that consumers can buy directly on the platform. Launched in 2024, Brazil's Vision 12D device employs multispectral imaging to assess skin hydration, elasticity, and sebum levels. This data aids dermatologists in justifying prescription-strength cosmeceuticals over standard over-the-counter options. At in-cosmetics Latin America 2024, L'Oréal unveiled its Mixy platform, enabling consumers to create custom foundation shades in-store through AI color-matching. This innovation not only simplifies SKU complexity but also heightens the sense of personalization. Unilever's Dove brand, pouring over EUR 900 million (USD 990 million) into research and development over two years, has secured more than 20,000 formula patents. These patents feature AI-optimized ingredient blends, tailored for specific skin types identified via digital diagnostics. The message is unmistakable: brands without proprietary diagnostic tools risk being seen as mere commodities, vying only on price, while AI-savvy competitors dominate the premium market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility and inflation are pressuring premium pricing | -0.7% | Argentina, Brazil | Short term (≤ 2 years) |

| High counterfeit penetration eroding consumer trust | -0.5% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Regulatory gaps around dermocosmetics and active-ingredient limits | -0.3% | Argentina, Colombia, Peru | Long term (≥ 4 years) |

| Logistics fragmentation outside tier-1 cities | -0.3% | Brazil, Colombia, Peru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency volatility and inflation pressuring premium pricing

As of December 2024, Argentina's annual inflation rate hit a staggering 117.8%, as reported by INDEC. This surge has significantly curtailed the discretionary spending power of many, pushing premium cosmeceuticals out of reach for middle-income consumers. For instance, a standard 400ml shampoo now retails at ARS 4,855 (approximately USD 4.86), and a basic deodorant is priced at ARS 2,653 (around USD 2.65). Throughout 2024, these products saw monthly price hikes between 1.6% and 3.5%. In response, brands have been compelled to downsize their SKU offerings, ensuring prices remain below the psychologically significant ARS 3,000 mark. Meanwhile, in Brazil, the real's depreciation against the dollar, while not as drastic as Argentina's peso collapse, still exerts margin pressures on brands importing active ingredients from Europe or Asia. This is underscored by ANVISA's stipulation that mandates 95% of L'Oréal Brazil's portfolio be produced locally, highlighting the strategic necessity for brands to localize their supply chains. This currency challenge hits harder for brands focusing on natural or organic formulations. These products often depend on imported certification and testing services, which are priced in hard currency, leading to a cost structure that's 15% to 25% steeper than their conventional counterparts. In light of these challenges, brands are adapting: some are downsizing package sizes, others are cutting back on active-ingredient concentrations to trim input costs, and a few are even stepping away from premium tiers altogether. Such moves, while aimed at preserving short-term sales volumes, risk undermining long-term brand equity. This inflation-induced pivot towards value segments is especially evident in the hair care market. Here, consumers are shifting from high-end salon-exclusive brands to more affordable mass-market alternatives, which promise "good enough" performance at just half the price.

High counterfeit penetration eroding consumer trust

Counterfeit cosmetics pose a significant threat, jeopardizing not just revenues but also consumer safety and brand integrity. In January 2025, INTERPOL's Operation CRETA II seized over 1.3 million counterfeit cosmetics, valued at over USD 50 million[3]Source: INTERPOL, “Operation CRETA II Press Release January 2025,” interpol.int. According to OECD's General Trade-Related Index of Counterfeiting, cosmetics emerged as the most targeted category, boasting a staggering index score of 0.9999. Meanwhile, Operation Crete II, conducted in August-September 2024 across 12 South American nations, confiscated over 11 million illicit products worth USD 225 million. This haul included around 300,000 pharmaceutical items and led to 104 arrests. Brazil's enforcement, anchored in the Industrial Property Law and customs protocols, faces challenges. The Paraná River route, linking Argentina and Brazil, and Andean pathways channeling goods from Bolivia to Chile and Peru, are exploited by organized crime syndicates. These groups even leverage social media to directly market counterfeit products to consumers. A 2024 EUIPO campaign revealed Brazil's staggering annual loss of approximately BRL 345 billion (USD 69 billion) to counterfeiting across all sectors. Cosmetics, with their low entry barriers and high profit margins, account for a significant chunk of this loss. The erosion of trust is particularly pronounced in the natural and organic segments. Here, counterfeiters replicate certification labels, misleading consumers about meeting standards like COSMOS or USDA NOP. This "lemons problem" leaves consumers struggling to differentiate between authentic and fake products, diminishing their willingness to pay for genuine certified items. In response, brands are turning to blockchain authentication, QR code verification, and tamper-evident packaging. However, these protective measures inflate unit costs by 3% to 5%, further squeezing margins in an already sensitive pricing landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hair Care Outpaces Skin Care Growth

In 2025, Skin Care Products held 48.10% market share, while Hair Care Products are projected to grow at a 9.45% CAGR through 2031, driven by the "skinification" trend emphasizing scalp health. In September 2025, Unilever's Dove brand launched 64 new hair care SKUs, supported by a EUR 1 billion (USD 1.1 billion) research and development program and over 20,000 patents utilizing robotics and nanotechnology for ingredient penetration. Natura's 2024 Lumina Anti-Aging Hair Regenerator targets gray hair reversal using biotechnology and Amazonian biodiversity actives, blending cosmeceuticals with regenerative medicine. Brazil, ranked 3rd globally in hair care consumption, saw advertising spending rise from BRL 44.9 billion (USD 9 billion) in 2022 to BRL 60.5 billion (USD 12.1 billion) in 2024, highlighting the category's importance. Anti-aging skin care now incorporates pharmaceutical-grade retinoids and peptides near prescription levels, drawing scrutiny under ANVISA's RDC 965/2025, which regulates active-ingredient limits for OTC products. Tele-dermatology boosts anti-acne products by enabling remote prescriptions of high-efficacy formulations. Sun protection remains key, with BASF's Uvinul TS Hydro, a water-soluble UV filter, addressing the need for lightweight, non-greasy sunscreens in humid climates. Lip and Oral Care Products are expanding with innovations like peptide-infused lip treatments and probiotic oral care solutions.

Hair care growth reflects shifting consumer behavior, with scalp health seen as an extension of facial skin care. Grupo Boticário's Eudora Siàge line uses digital diagnostics for personalized scalp treatments, mirroring AI-driven facial skin care trends. Truss, a Brazilian professional hair care brand, reported 34% growth in salon channels in 2024 by positioning scalp products as clinical solutions. L'Oréal's 2024 launch of a line for wavy, kinky, and curly hair addresses South America's diverse textures, a segment often underserved by global brands. Growth is further supported by combined-use products like cleansing-conditioners and hair removal-moisturizers, catering to 75% of Brazilian men who report limited leisure time. Regulatory oversight in hair care remains minimal compared to skin care, as ANVISA's limits primarily apply to leave-on facial products, allowing higher active-ingredient levels in scalp treatments.

By Category: Natural/Organic Gains Despite Certification Complexity

In 2025, conventional formulations held a 67.85% market share, while natural and organic products are projected to grow at an 8.34% CAGR through 2031, driven by consumer demand for mental health-focused beauty routines. WGSN's 2024 research shows 49% of Brazilians favor products with mental health benefits, prompting brands to position natural ingredients as wellness solutions. Ecocert's COSMOS standard, active in over 130 countries, including Argentina, certifies authentic natural/organic products but raises production costs by 15% to 25% due to imported testing services. Natura's commitment to 100% regenerative sourcing by 2050, supported by BRL 230 million (USD 46 million) in bioeconomy investments, highlights the shift of natural/organic positioning to a core business model. Brazil's Lei 13.123/2015 ensures indigenous communities receive royalties for traditional knowledge used in formulations, adding cost and compliance challenges.

Conventional formulations dominate due to superior efficacy, longer shelf life, and affordability, especially in an inflationary environment. The natural/organic segment faces perception issues, with consumers viewing certified products as less effective, particularly in anti-aging and anti-acne categories. Brands are addressing this by hybridizing formulations, combining natural bioactives like Amazonian oils with synthetic preservatives, creating a "clean clinical" category. Lola From Rio, a vegan Brazilian brand that merged with Skala and gained Advent International's backing in 2024, shows how indie brands can scale in the natural/organic segment while maintaining mass-market pricing. Regulatory oversight is increasing, with ANVISA's RDC 949/2024 requiring brands to substantiate biodiversity sourcing and benefit-sharing claims. The fragmented certification landscape, COSMOS, USDA NOP, Fair Trade, NATRUE, and ISO 16128, creates consumer confusion and compliance burdens for brands in South America.

By End User: Men's Segment Accelerates on Combined-Use Innovation

In 2025, women held a dominant 71.30% share of the market. However, the men's segment is projected to grow at an 7.66% CAGR through 2031, driven by the rising popularity of combined-use products that streamline grooming routines and reduce the need for multiple SKUs. WGSN research highlights double-digit growth for male beauty products in Colombia over the past five years, with 74% of Colombian households purchasing men-specific formulations. In Brazil, male toiletries are shifting toward multifunctional 2-in-1 and 3-in-1 solutions, such as combining cleansing with shaving or integrating hair removal with moisturizing, catering to the 75% of men with less than three hours of daily leisure time. Products like Nivea For Men Cool Kick 2-in-1 exemplify this trend. Post-shave care innovations now incorporate pharmaceutical-grade actives like peptide technology, hyaluronic acid, retinol, and vitamin C, transforming aftershave into a dermocosmetic segment with measurable anti-aging benefits.

The women's segment continues to lead, driven by higher per-capita spending and widespread adoption across skin care, hair care, lip care, and oral care categories. Women also drive tele-dermatology adoption, using remote consultations for hyperpigmentation and melasma, creating recurring revenue streams for physician-dispensed cosmeceuticals. The unisex segment, though not separately quantified, is gaining traction as gender-neutral formulations simplify SKU management and appeal to younger consumers rejecting binary marketing. Men's growth is further supported by shifts in distribution channels, with over 40% of male toiletries sold through hypermarkets and supermarkets, which offer competitive pricing and reduce stigma compared to specialty stores. Brands are reshaping perceptions of cosmeceuticals for men, with Galderma marketing hyaluronic acid fillers and biostimulatory agents as "conscious self-care" rather than vanity. Regulatory frameworks remain neutral, as agencies like ANVISA and ANMAT maintain consistent active-ingredient limits regardless of the end user, enabling brands to expand dermocosmetic formulations into the men's segment without reformulation.

By Distribution Channel: Online Retail Disrupts Traditional Pharmacy Dominance

In 2025, Supermarkets and Hypermarkets held 46.05% of the distribution share, while Online Retail Stores are projected to grow at an 7.85% CAGR through 2031, driven by platform partnerships enhancing delivery speed and reach. Natura's October 2024 partnership with MercadoLibre in Brazil, later extended to Argentina, integrated its 3 million consultants with MercadoLibre's fulfillment network, which shipped 1.377 billion items in 2024, with 76% delivered within 48 hours. Care, Natural Beauty generates 80% of its revenue through its proprietary e-commerce platform, maintaining premium pricing without retailer margin dilution. L'Oréal's partnership with MercadoLibre in Mexico highlights a regional strategy to leverage platform scale for last-mile delivery in fragmented retail markets. ANVISA's 2024 e-commerce working group aims to harmonize online cosmetic sales regulations across Brazilian states, reflecting regulatory adaptation to digital distribution.

Beauty and Health Stores, including pharmacy-exclusive channels, remain vital for dermocosmetics requiring dermatologist endorsements or prescriptions. L'Oréal Brazil reported BRL 3.3 billion (USD 660 million) in pharmacy-channel sales in 2024. Tele-dermatology is driving a hybrid model where consultations occur online, but fulfillment happens through pharmacies that verify prescriptions and provide counseling. Other Distribution Channels, such as direct sales and specialty boutiques, are losing share as consumers prioritize convenience and price transparency. In Argentina, hyperinflation has amplified online retail growth, with transparent pricing becoming a competitive advantage. Counterfeit products remain a challenge, as INTERPOL's Operation CRETA II seized over 1.3 million counterfeit cosmetics in January 2025, many distributed via social media and unregulated e-commerce. Brands are adopting blockchain authentication and QR code verification to combat counterfeits, though these measures increase unit costs by 3% to 5%, compressing margins in a competitive market.

Geography Analysis

In 2025, Brazil held 61.05% of market revenue, solidifying its position as Latin America's largest cosmetics consumer and the third-largest globally, with 43.4% of the regional market. ABIHPEC reported record exports of USD 884 million in 2024, while January-August 2025 exports rose 15.8% to USD 681.6 million. ANVISA's RDC 907/2024 regulatory sandbox enables real-world testing of new ingredients, reducing time-to-market by 18 months and giving Brazilian brands an edge in bioactive formulations. Grupo Boticário's BRL 3.34 billion (USD 668 million) Minas Gerais factory, set for 2028, will boost production by 50%, supporting domestic and export demand. Natura's Vision 2050 targets sourcing from 46 communities across 2.2 million hectares, expanding to 3.0 million hectares by 2030, with BRL 230 million (USD 46 million) in bioeconomy investments. Brazil's reverse logistics program recovered 165,661 tonnes of packaging in 2023, totaling 1 million tonnes since 2013. As of February 2025, the sector employed 7.1 million, with 153,800 direct jobs, a 7.7% increase from 2023.

Argentina, despite 117.8% inflation in December 2024, is the fastest-growing market with a 7.52% CAGR through 2031, driven by exports and regulatory harmonization. Brazilian exports to Argentina rose 65.1% to USD 139.5 million in early 2025, supported by MERCOSUR's Disposición 8067/2024. Argentina's cosmetics exports grew 43.2% year-over-year to USD 253 million in H1 2024, transitioning it to a regional exporter. ANMAT's Decree 1024/2024 deregulated over-the-counter products, expediting dermocosmetics market entry. Natura's partnership with MercadoLibre, extended to Argentina in late 2024, addresses logistics challenges. Currency pressures led brands to introduce smaller SKUs under ARS 3,000 to maintain affordability. In Colombia, tele-dermatology is growing, creating a physician-dispensed channel. INVIMA's Andean Resolution 2310, issued in December 2024, standardized Spanish labeling across Colombia, Ecuador, Peru, and Bolivia. Revieve's partnership with Beautycalia uses AI for hyperpigmentation analysis, offering tailored product recommendations in seconds.

Peru, Chile, and other South American markets are incorporating Andean botanical bioactives into premium formulations at higher rates than Amazon-sourced ingredients. Peru's RENETSA reforms centralized pharmaceutical purchasing, improving access to 50 oncology molecules between 2023 and 2024, with potential benefits for dermocosmetics. Chile's Supreme Decrees 3/2010 and 239/02 regulate cosmetics, while the ISP's GICONA platform streamlines submissions. Natura's Celaya plant in Mexico exports to Peru and Colombia, leveraging Pacific Alliance trade agreements. The Andean Community's draft regulation aims to harmonize cosmetic standards, reducing compliance costs. Brazil's export momentum benefits Paraguay and Uruguay, with Paraguay receiving USD 53.6 million in Brazilian cosmetics exports in early 2025.

Competitive Landscape

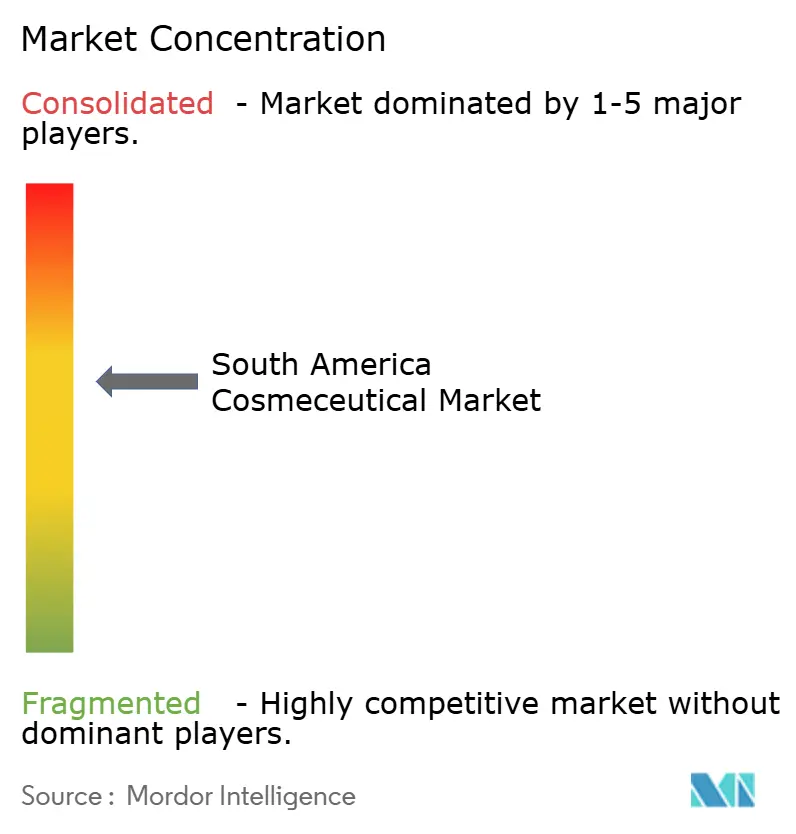

The South America Cosmeceutical Market is moderately consolidated, where local pharmaceutical players are leveraging their established distribution networks, originally built for prescription drugs, to introduce high-efficacy serums exclusively in pharmacy channels. Meanwhile, multinational companies are harnessing AI-driven diagnostics and bioactive formulations, tapping into the region's rich biodiversity. In March 2025, Eurofarma acquired a 60% stake in Dermage, granting the pharmaceutical giant access to retinol and peptide-based formulations. These can be cross-promoted with prescription dermatology drugs at 80,000 pharmacy touchpoints throughout Brazil. In July 2024, Natura launched Natura Ventures, a BRL 50 million (USD 9.2 million) fund, aiming at 15 seed-stage beauty startups in Brazil. This move underscores that industry incumbents are prioritizing innovation ecosystems over traditional internal research and development. Unilever's Dove brand has filed over 20,000 formula patents, integrating robotics and nanotechnology to enhance ingredient penetration. This defensive maneuver not only fortifies their core formulations but also erects significant barriers for smaller competitors.

Brands are now eyeing tele-dermatology channels, where integrating virtual consultations with product sales allows them to earn both consultation fees and product revenue, a feat traditional cosmetics brands find hard to emulate. Indie brands like Care Natural Beauty are making waves, with 80% of their revenue stemming from proprietary e-commerce and just 20% from third-party marketplaces. This showcases the viability of direct-to-consumer economics in maintaining premium pricing without compromising on retailer margins. Technology is at the forefront, Revieve's collaboration with Beautycalia in Colombia and Vision 12D's imaging device in Brazil highlight the swift transition from skin assessment to product recommendation, streamlining the journey from consultation to purchase.

Counterfeit cosmetics pose a significant challenge; INTERPOL's Operation CRETA II seized over 1.3 million counterfeit items worth over USD 50 million in January 2025. This has compelled brands to invest in blockchain authentication and QR code verification, adding 3% to 5% to their unit costs. As the lines blur between pharmaceuticals and beauty, regulatory bodies are taking note. ANVISA's RDC 965/2025 sets concentration limits for over-the-counter actives, benefiting brands with pharmaceutical-grade research and development over traditional cosmetics firms. A noticeable trend is emerging: consumers are placing greater trust in clinical efficacy, with endorsements from dermatologists and peer-reviewed studies taking precedence over celebrity testimonials.

South America Cosmeceutical Industry Leaders

Natura &Co Holding S.A.

Boticário Produtos de Beleza Ltda

L’Oréal SA

Unilever PLC

Beiersdorf AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Unilever launched 64 new Dove hair care SKUs in Brazil, backed by a EUR 1 billion (USD 1.1 billion) global research and development program and over 20,000 formula patents that incorporate robotics and nanotechnology to demonstrate ingredient penetration at the molecular level, positioning the brand to capture the "skinification" trend in scalp care.

- March 2025: Eurofarma acquired a 60% stake in Dermage, a Brazilian dermocosmetics brand specializing in retinol and peptide-based formulations, providing the pharmaceutical giant with access to 80,000 pharmacy touchpoints across Brazil and accelerating the pharmabeauty convergence.

- July 2024: Natura launched Natura Ventures, a BRL 50 million (USD 9.2 million) fund targeting 15 seed-stage Brazilian beauty startups, signaling a strategic shift toward ecosystem investing rather than relying solely on internal research and development for innovation.

South America Cosmeceutical Market Report Scope

South America cosmeceuticals market offers a wide range of products broadly categorized under skin care, hair care, lip care, and oral care. Also, the market covers the products available across distribution channels Supermarket/Hypermarkets, Convenience stores, online Retail, specialist stores, others. Moreover, the study provides an analysis of the cosmeceuticals market in the emerging and established markets across the region, including Brazil, Argentina and Rest od South America.

Product Type

| Skin Care Products | Anti-ageing |

| Anti-acne | |

| Sun Protection | |

| Other Skin-care Products | |

| Hair Care Products | Shampoos and Conditioners |

| Hair Colourants and Dyes | |

| Other Hair-care Products | |

| Lip Care Products | |

| Oral Care Products |

Category

| Conventional |

| Natural/Organic |

End User

| Male |

| Female |

By Distribution Channel

| Supermarkets and hypermarkets |

| Beauty and Health Stores |

| Online Retail Stores |

| Other Distribution Channels |

Geography

| Brazil |

| Argentina |

| Colombia |

| Peru |

| Chile |

| Rest of South America |

| Product Type | Skin Care Products | Anti-ageing |

| Anti-acne | ||

| Sun Protection | ||

| Other Skin-care Products | ||

| Hair Care Products | Shampoos and Conditioners | |

| Hair Colourants and Dyes | ||

| Other Hair-care Products | ||

| Lip Care Products | ||

| Oral Care Products | ||

| Category | Conventional | |

| Natural/Organic | ||

| End User | Male | |

| Female | ||

| By Distribution Channel | Supermarkets and hypermarkets | |

| Beauty and Health Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| Geography | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the South America cosmeceutical market in 2026?

The market stands at USD 9.37 billion in 2026 and is projected to reach USD 11.38 billion by 2031.

Which product type is growing fastest?

Hair care leads growth with a forecast 9.45% CAGR through 2031, outpacing skin care.

Why are Brazilian brands prominent in cosmeceuticals?

Brazil accounts for 61.05% of 2025 revenue, supported by ANVISA’s regulatory sandbox and abundant biodiversity that speeds novel active approvals.

What is driving online sales of cosmeceuticals?

Partnerships such as Natura and MercadoLibre provide 48-hour delivery across major markets, expanding access beyond tier-1 cities.

How are companies combating counterfeit products?

Firms are investing in blockchain authentication and QR code verification, even though these add 3-5% to unit costs.

Which geography shows the highest growth rate?

Argentina is forecast to post a 7.52% CAGR to 2031, aided by streamlined OTC approvals and rising imports from Brazil.

Page last updated on: