Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

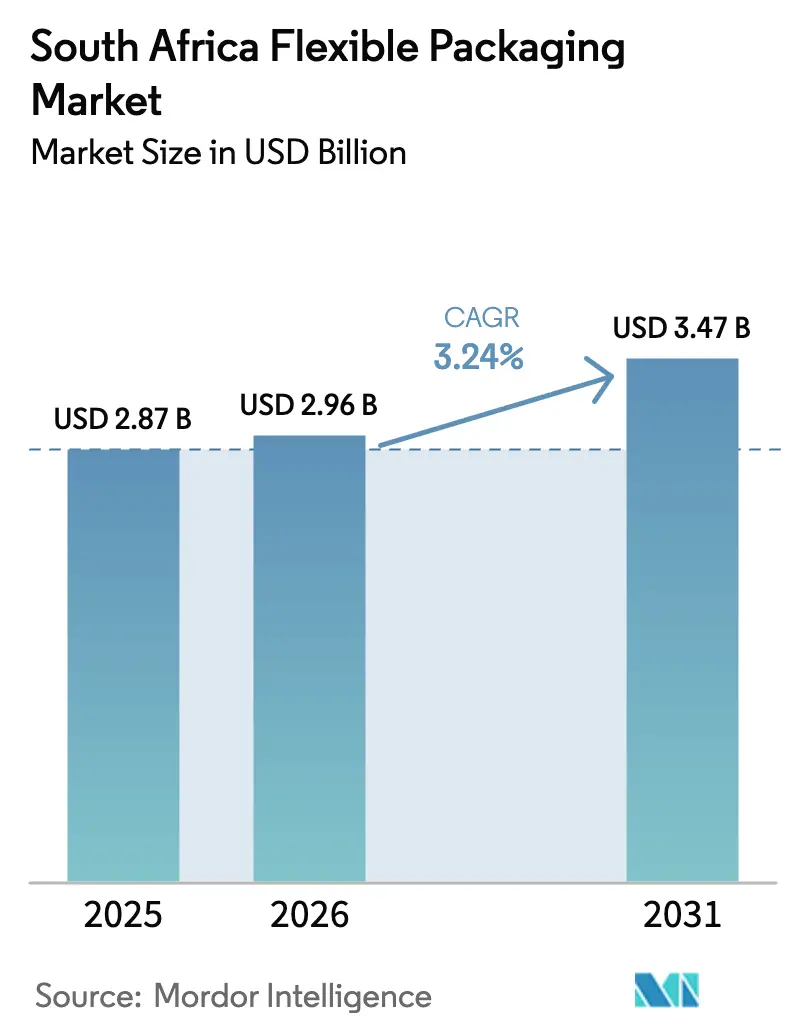

| Base Year Market Size (2025) | USD 2.87 Billion |

| Market Size (2026) | USD 2.96 Billion |

| Market Size (2031) | USD 3.47 Billion |

| Growth Rate (2026 - 2031) | 3.24% CAGR |

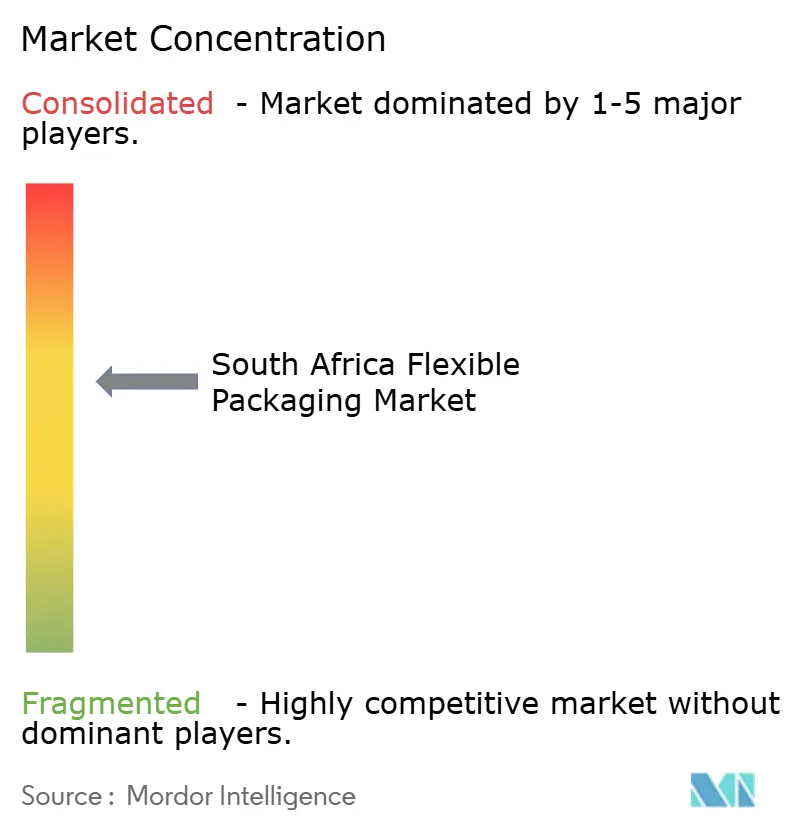

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Flexible Packaging Market Analysis by Mordor Intelligence

South Africa flexible packaging market size in 2026 is estimated at USD 2.96 billion, growing from 2025 value of USD 2.87 billion with 2031 projections showing USD 3.47 billion, growing at 3.24% CAGR over 2026-2031. The measured growth trajectory reflects a maturing consumer base that increasingly values sustainability, convenience, and digital engagement. Spending growth in food processing, personal care, and e-commerce prompts steady investments in mono-material films, recyclable pouches, and high-definition digital printing. At the same time, Extended Producer Responsibility (EPR) legislation pushes producers toward designs that simplify end-of-life recovery, supporting wider adoption of bioplastics and paper-based laminates. Currency volatility and polymer price swings add cost pressure, yet established converters use long-term supply contracts and lightweight designs to protect margins. Innovation around refill formats and on-the-go portions keeps the South Africa flexible packaging market competitive, even as overall GDP growth remains modest.

Key Report Takeaways

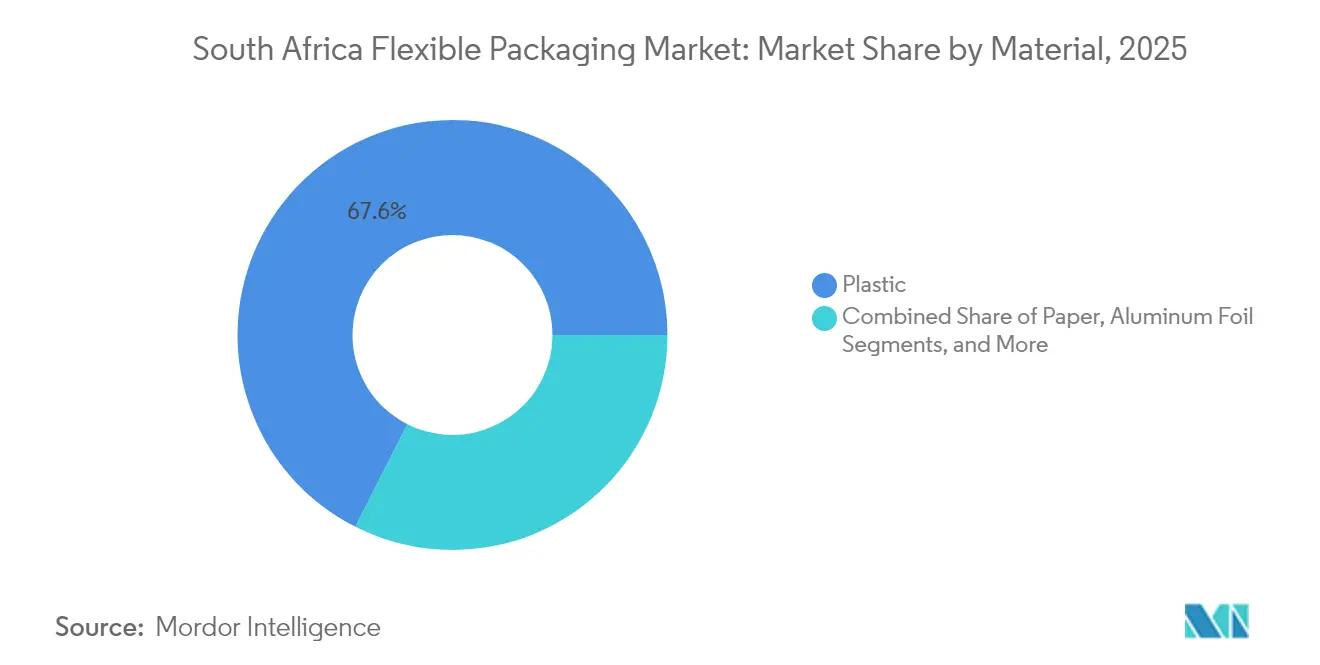

- By material, plastic held 67.55% of South Africa flexible packaging market share in 2025, while bioplastics and compostables are projected to advance at a 5.56% CAGR to 2031.

- By product type, pouches led with 46.62% revenue share in 2025; sachets and stick packs are forecast to expand at a 4.47% CAGR to 2031.

- By end-user industry, food processing captured 30.05% of the South Africa flexible packaging market size in 2025, whereas personal care and cosmetics are advancing at a 4.71% CAGR through 2031.

- By printing technology, flexography commanded 44.58% of the South Africa flexible packaging market size in 2025, while digital printing shows the strongest outlook with a 4.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of e-commerce and demand for convenient packaging | +0.8% | Gauteng, Western Cape | Medium term (2-4 years) |

| Growth of food and beverage processing sector | +0.7% | KwaZulu-Natal, Western Cape | Long term (≥4 years) |

| Rising demand for personal care and cosmetics | +0.6% | Major urban centers | Medium term (2-4 years) |

| Private-label penetration in modern grocery retail | +0.5% | Nationwide | Short term (≤2 years) |

| Mandatory EPR accelerating recyclable materials | +0.4% | Nationwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expansion of E-commerce and Demand for Convenient Packaging

Rapid growth from 27 million online shoppers in 2022 to a projected 37.9 million in 2027 transforms last-mile logistics and packaging metrics. Return rates close to 40% in online channels versus 5-10% in stores encourage brands to specify durable, resealable pouches that survive reverse flows without secondary packaging. Quick-commerce fulfillment drives demand for lighter formats that cut dimensional weight yet protect high-frequency orders. Subscription services push premium stand-up designs that elevate unboxing and brand storytelling. Amcor’s mono-material refill pouch for L’Oréal cuts resin usage by 75%, showcasing how e-commerce catalyzes flexible formats.

Growth of Food and Beverage Processing Sector

Food service sales reached USD 5.5 billion in 2023 and climbed 27% year-on-year, anchoring baseline demand for portionable, on-the-go wrappers. [1]U.S. Department of Agriculture FAS, “Food Service - Hotel Restaurant Institutional Annual,” fas.usda.gov Township expansion requires low-cost but rugged laminates that endure informal distribution. Health-focused shoppers choose transparent, high-barrier films that showcase clean ingredients. Craft beverages adopt metallized pouches that combine crisp graphics with oxygen protection, while ready-to-eat meals rely on microwave-able lidding that supports convenience dinner occasions.

Rising Demand for Personal Care and Cosmetics

Refill pouches and mono-material sachets dominate new product rollouts as premium beauty brands target sustainability goals without sacrificing aesthetics. Unilever doubled packaging R&D spending to accelerate recyclable stand-up formats and digital color-matching that predicts shade shifts when using recycled content. [2]Waqas Qureshi, “Unilever Boosts Investment in Packaging R&D,” packagingnews.co.uk Spouted pouches for shampoos and lotions appeal to e-commerce buyers seeking leak-proof delivery and sample programs. Metallized films still feature in luxury lines, marrying barrier performance with shimmer effects that lift shelf appeal.

Mandatory EPR Accelerating Recyclable Materials

Since late 2020, EPR rules require producers to finance collection and recycling, prompting a pivot to mono-material polyethylene and polypropylene films that pass recyclability tests. MetPac-SA and Fibre Circle coordinate compliance, giving scale players an advantage over small converters that lack reporting systems. Life-cycle assessments, due within five years of adoption, reinforce design-for-recycling across new launches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental Concerns and Recycling Infrastructure Gaps | -0.6% | National, acute in rural and township areas | Long term (≥ 4 years) |

| Polymer Price Volatility and Rand Fluctuations | -0.4% | National, import-dependent manufacturers most affected | Short term (≤ 2 years) |

| Competition from Rigid and Reusable Packaging | -0.3% | National, premium segments and industrial applications | Medium term (2-4 years) |

| Low Adoption of Advanced Barrier-Film Recycling Tech | -0.2% | National, limited by capital investment requirements | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental Concerns and Recycling Infrastructure Gaps

Flexible films often escape curbside systems because multi-layer laminates are hard to sort, so households question recyclability claims, especially outside main metros. The result is higher landfill leakage that weighs on brand reputation. Agglomeration technologies for dirty film waste remain scarce and capital intensive, constraining collection pilots and local upcycling ventures.

Polymer Price Volatility and Rand Fluctuations

With most resin grades imported, converters face twin shocks from oil-linked feedstock prices and currency swings. Middle-East oversupply depresses polyethylene values but also destabilizes contracts, while the Rand’s sharp moves undermine hedging for SMEs. Tight credit terms then squeeze working capital, exposing firms with fixed-price FMCG contracts to margin erosion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastic Maintains Scale Leadership Amid Bio-Shift

Plastic accounted for 67.55% of the South Africa flexible packaging market in 2025 thanks to the proven cost-to-performance ratio of polyethylene and bi-oriented polypropylene. The segment continues to dominate mass food, beverage, and household applications because converters already own optimized extrusion and print assets. Yet the South Africa flexible packaging market size tied to bioplastics and compostables is projected to grow 5.56% annually through 2031, sustained by EPR scorecards and retailer pledges. Paper-based laminates attract brands seeking curbside-ready claims and lower carbon footprints, while foil remains the go-to for moisture-sensitive dairy and pharma SKUs. Over the outlook, global suppliers like Mondi are scaling hybrid paper-plastic designs that meet toughness targets without compromising recycling.

Rising mono-material demand drives film makers to invest in high-density PE lines that deliver stiffness and heat resistance without complex barrier tie layers. Local polymer modifiers now offer compatibilizers that ease mechanical recycling, expanding feedstock for domestic film re-extrusion. As the South Africa flexible packaging market aligns with circular metrics, converters tout cradle-to-cradle certifications to win premium tenders, limiting share loss to rigid alternatives.

By Product Type: Pouches Sustain Leadership, Sachets Accelerate

Pouches held 46.62% share of the South Africa flexible packaging market in 2025 due to their billboard display, reseal features, and low shipping weight. High-definition digital print extends shelf impact and supports seasonal graphics, while laser-scored tear openings improve consumer convenience. Sachets and stick packs, forecast to rise 4.47% per year, meet urban single-serve snacking and rural affordability. They also underpin influencer sampling campaigns that depend on low-cost distribution.

Films and wraps protect fresh produce, dairy, and food-service wraps that must stay transparent for quality inspection. Bags and sacks address bulk fertilizers and construction additives needing puncture resistance, whereas lidding films secure ready-meal trays. The South Africa flexible packaging market share for label sleeves benefits from craft beverage brands that target differentiation via contour wraps compatible with shrink tunnels.

By End-User Industry: Food Dominates, Personal Care Gains Speed

Food processing captured 30.05% of the South Africa flexible packaging market size in 2025 because snacks, baked goods, and meat categories rely on oxygen and moisture barriers that delay spoilage. Volume players such as Tiger Brands trigger large order runs that maximize flexographic economies. Personal care packaging, advancing at 4.71% CAGR, pivots on refill pouches and luxury sachets filled with serums, gels, and hair masks marketed online.

Beverage up-trading supports metallized or paper-based solutions for premium craft beers, while healthcare lines adopt high-barrier laminates certified for pharmacopoeia compliance. Chemical and industrial drums increasingly specify multi-layer liners that prevent contamination and facilitate reuse. These niche requirements shave the South Africa flexible packaging market into many micro-opportunities where specialty converters earn resilient margins.

By Printing Technology: Flexography Holds Scale, Digital Rises

Flexography owned 44.58% of the South Africa flexible packaging market in 2025, favored for large SKUs where plate costs amortize fast. Eight-color CI presses now deliver photo-realistic graphics that once required rotogravure. Still, digital presses show the steepest growth at 4.93% CAGR by enabling SKU proliferation, regional promotions, and serialized QR codes without plates.

Hybrid press investments, pairing inkjet units with flexo decks, give converters a path to variable data alongside high-speed solids. Rotogravure remains viable for overwraps and long-run condiment sachets but suffers from cylinder lead times. Screen and cold-foil units serve narrow tactile effects on prestige cosmetic pouches. Converters that blend digital workflows with EPR-compliant inks position themselves as first-choice partners for agile brand owners, reinforcing a smoother South Africa flexible packaging market evolution.

Geography Analysis

Gauteng and Western Cape account for more than half of national output because these provinces cluster head-office decision makers, modern retail, and export-oriented food factories. Household consumption rose 2.3% year-on-year in Q4 2024, supporting retail pack volumes despite a 3.2% contraction in wider manufacturing. KwaZulu-Natal leverages port access to import resins and export packaged foods across the Southern African Development Community, while Eastern Cape’s automotive corridor drives demand for industrial liners and component wraps.

Rural provinces lag on recycling infrastructure, but township markets buy significant sachet volumes due to low unit pricing. National EPR frameworks create uniform compliance, allowing converters to pool post-consumer film waste from multiple cities for re-processing. Cape Town’s circular-economy pilot showcases how branded drop-off points increase film collection rates, offering a template for roll-out elsewhere.

South Africa’s customs union links enable local converters to serve Namibia, Botswana, and Eswatini without additional tariffs, augmenting export orders that fill spare capacity. Nevertheless, cross-border sales face currency misalignment and logistics bottlenecks that encourage warehousing near main highways. This regional gateways strategy limits shipment distances and buffers the South Africa flexible packaging market against domestic macro-volatility.

Competitive Landscape

The competitive field mixes local majors and globally backed entrants, creating a moderately concentrated arena with room for specialist players. Nampak trimmed non-core plastics assets worth R2.7 billion (USD 149 million) in 2024 to focus on beverage cans and diversified packaging, channeling capex into can-line debottlenecking. [4]Nampak, “Nampak Announces 2024 Results,” nampak.com Mpact’s 2024 revenue reached R10 billion (USD 553 million), reflecting improved board-mill efficiencies and selective acquisitions that deepen vertical integration.

Global players such as Amcor, Mondi, and Mauser Packaging build scale through partnerships that supply recycled content, sustainable papers, and industrial drums. Amcor’s tie-up with Kolon Industries develops chemically recycled polyester that meets food-grade specs, while Mondi’s Štětí expansion lifts kraft paper capacity, enabling dual sourcing for paper-based pouches.

Digital capabilities now separate incumbents: converters installing HP Indigo or Xeikon presses pitch hyper-short runs to niche cosmetics labels, capturing value pockets overlooked by legacy flexo houses. Compliance strength around EPR data reporting also influences tender awards as brand owners seek low-risk suppliers. As these factors converge, the South Africa flexible packaging market gravitates toward multi-plant groups that marry R&D depth, asset breadth, and circular-economy credentials.

South Africa Flexible Packaging Industry Leaders

Amcor plc

Mondi plc

Constantia Flexibles Group GmbH

Huhtamaki Oyj

Sonoco Products Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Mpact Group forecast a stronger 2025 after completing portfolio restructuring and reporting improved EBITDA.

- March 2025: Amcor introduced paper-based packaging for dry beverage mixes to replace plastic multilayer films.

- February 2025: Mauser Packaging Solutions bought a South African plastic drum business to expand chemical-grade container capacity.

- February 2025: Mondi completed five capital projects, including a new Štětí paper machine that boosts kraft output.

South Africa Flexible Packaging Market Report Scope

The study covers the flexible packaging market tracked in terms of consumption and is limited to flexible packaging products made from plastic, paper, and aluminum. The South Africa Flexible Packaging Market is segmented by Product Type (Bags and Pouches, Films and Wraps) and End-users (Food, Beverage, Healthcare and Pharmaceutical).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Material

| Plastic | Polyethylene (PE) |

| Bi-Oriented Polypropylene (BOPP) | |

| Cast Polypropylene (CPP) | |

| Polyvinyl Chloride (PVC) | |

| Other Plastics | |

| Paper | |

| Aluminum Foil | |

| Bioplastics/Compostable | |

| Other Materials |

By Product Type

| Pouches |

| Bags and Sacks |

| Films and Wraps |

| Sachets and Stick Packs |

| Labels and Sleeves |

| Lidding and Seals |

By End-User Industry

| Food | Baked Goods |

| Snacks | |

| Meat, Poultry and Seafood | |

| Confectionery | |

| Pet Food | |

| Other Food Products | |

| Beverage | |

| Healthcare and Pharmaceutical | |

| Personal Care and Cosmetics | |

| Industrial and Chemical | |

| Other End-User Industries |

By Printing Technology

| Flexography |

| Rotogravure |

| Digital |

| Other Printing Technologies |

| By Material | Plastic | Polyethylene (PE) |

| Bi-Oriented Polypropylene (BOPP) | ||

| Cast Polypropylene (CPP) | ||

| Polyvinyl Chloride (PVC) | ||

| Other Plastics | ||

| Paper | ||

| Aluminum Foil | ||

| Bioplastics/Compostable | ||

| Other Materials | ||

| By Product Type | Pouches | |

| Bags and Sacks | ||

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Labels and Sleeves | ||

| Lidding and Seals | ||

| By End-User Industry | Food | Baked Goods |

| Snacks | ||

| Meat, Poultry and Seafood | ||

| Confectionery | ||

| Pet Food | ||

| Other Food Products | ||

| Beverage | ||

| Healthcare and Pharmaceutical | ||

| Personal Care and Cosmetics | ||

| Industrial and Chemical | ||

| Other End-User Industries | ||

| By Printing Technology | Flexography | |

| Rotogravure | ||

| Digital | ||

| Other Printing Technologies | ||

Key Questions Answered in the Report

What is the current value of the South Africa flexible packaging market?

The market is valued at USD 2.96 billion in 2026 and is projected to reach USD 3.47 billion by 2031.

How fast is demand for sustainable materials growing?

Bioplastics and compostable formats are forecast to expand at a 5.56% CAGR through 2031, significantly outpacing traditional plastics.

Which product type leads sales in flexible packaging?

Pouches hold 46.62% revenue share, driven by their light weight, reseal features, and strong shelf appeal.

Which end-user segment is advancing the quickest?

Personal care and cosmetics are growing at a 4.71% CAGR as refill systems and e-commerce sampling boost volume.

How will EPR regulations influence packaging design?

Producers must fund collection and recycling, so many new launches now favor mono-material PE or PP films that can be mechanically recycled.

What printing technology is gaining momentum?

Digital printing shows the highest growth, with a 4.93% CAGR, because it supports short runs, personalization, and rapid product launches.

Page last updated on: