Africa Data Center Storage Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

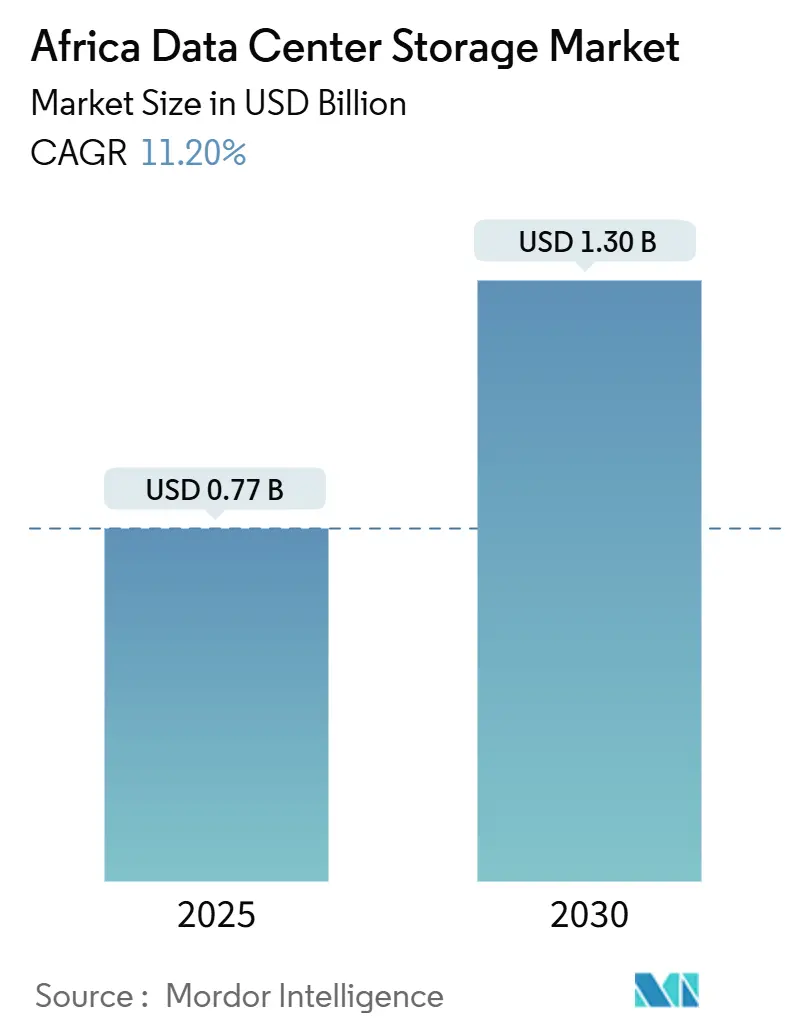

| Market Size (2025) | USD 0.77 Billion |

| Market Size (2030) | USD 1.30 Billion |

| Growth Rate (2025 - 2030) | 11.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Data Center Storage Market Analysis by Mordor Intelligence

The Africa Data Center Storage Market size is estimated at USD 0.77 billion in 2025, and is expected to reach USD 1.30 billion by 2030, at a CAGR of 11.20% during the forecast period (2025-2030).

The Africa data center storage market size reached USD 0.77 billion in 2025 and is projected to register an 11.2% CAGR, lifting value to USD 1.30 billion by 2030. The market’s current momentum is underpinned by sovereign-cloud mandates, hyperscale capital flows, and renewable-energy innovations that collectively lower barriers to large-scale digital infrastructure. National data-sovereignty policies in Egypt, Kenya, and Nigeria are anchoring predictable demand from public-sector workloads, while submarine-cable landings are making regional hubs more attractive to global cloud providers. Vendor competition is shifting toward energy-efficient architectures as power availability and carbon-reduction pledges influence procurement. Skills shortages in certified storage engineering continue to favor managed-services offerings, opening consolidation opportunities for suppliers able to absorb foreign-exchange risk and localize support. Across 2025–2030 the Africa data center storage market will reflect a progressive transition from capacity-centric HDD arrays to performance-led flash and NVMe platforms, especially where artificial-intelligence workloads demand low-latency I/O.

Key Report Takeaways

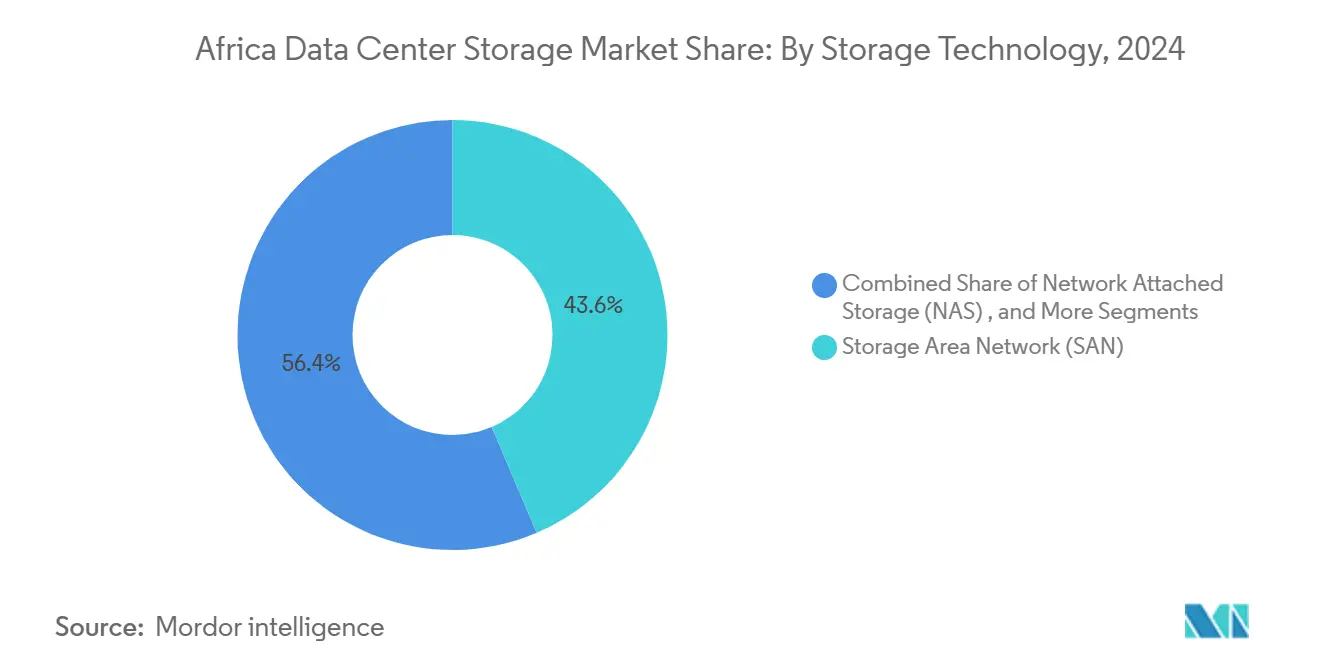

- By storage technology, Storage Area Network solutions captured 43.6% of Africa data center storage market share in 2024; Network Attached Storage is forecast to expand at a 14.2% CAGR through 2030.

- By storage type, HDD arrays accounted for a 46.8% share of the Africa data center storage market size in 2024, whereas all-flash arrays are advancing at a 13.4% CAGR to 2030.

- By data-center type, colocation facilities led with 56.4% revenue share in 2024; hyperscalers and cloud providers record the highest projected CAGR at 16.5% through 2030.

- By end user, IT and telecommunications held 34.4% revenue share in 2024, while healthcare and life sciences is the fastest-growing segment at a 13.8% CAGR to 2030.

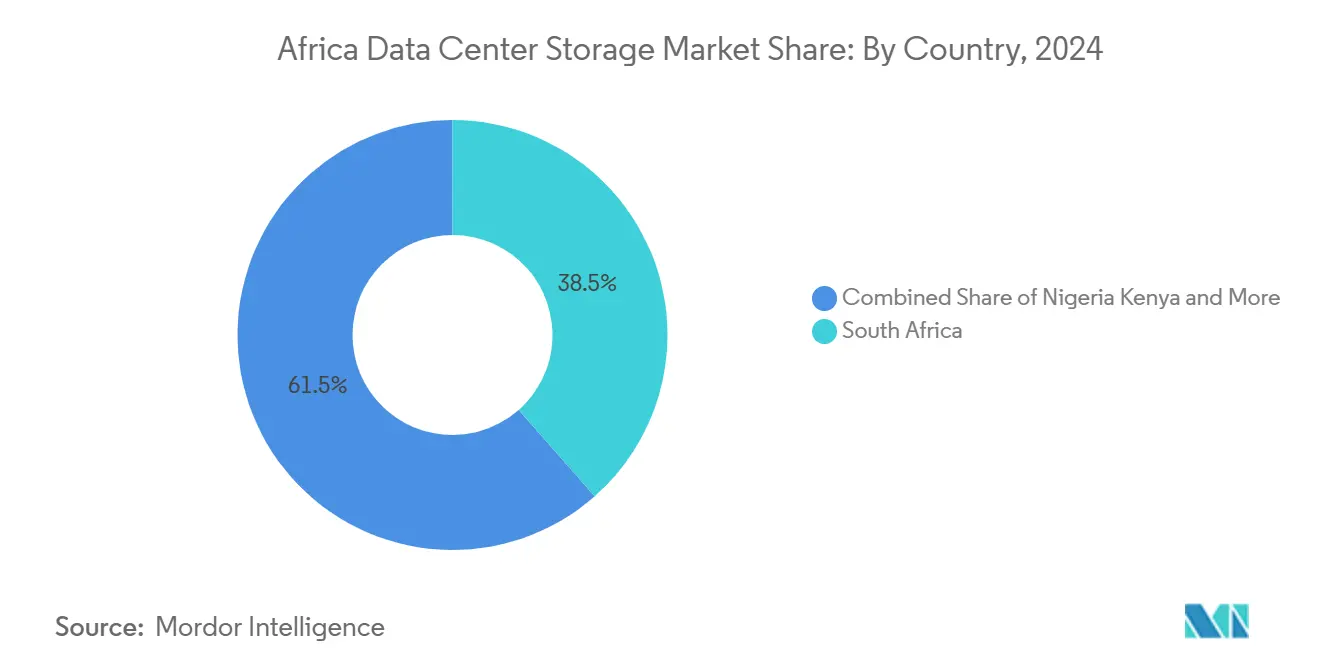

- By geography, South Africa contributed 38.5% of the Africa data center storage market size in 2024; Nigeria is growing the quickest at 13.2% CAGR to 2030.

Africa Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government- and telecom-led digitization | +2.1% | Nigeria, Kenya, Egypt | Medium term (2-4 years) |

| Hyperscale and colocation investments | +2.8% | South Africa, Nigeria, Kenya, Morocco | Long term (≥ 4 years) |

| SME cloud adoption surge | +1.9% | Nigeria, Kenya, Ghana | Short term (≤ 2 years) |

| HDD-to-flash energy transition | +1.4% | South Africa, Egypt, Morocco | Medium term (2-4 years) |

| Submarine-cable edge enablement | +1.6% | Coastal markets: South Africa, Nigeria, Kenya, Morocco, Egypt | Long term (≥ 4 years) |

| Fintech data-residency regulations | +1.2% | Nigeria, Kenya, South Africa, Ghana | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Government- and Telecom-Led Digitization Initiatives

Sovereign-cloud programs across Egypt, Algeria, and Ethiopia are reshaping enterprise storage procurement as state bodies build national data hubs that standardize security and interoperability. Egypt’s 120-petabyte Government Data and Cloud Computing Center inaugurated in 2024 has become a regional reference site, catalyzing similar facilities that anchor domestic workloads and reduce cross-border latency. New regulatory frameworks mandate local hosting of sensitive datasets, paying dividends to vendors able to certify compliance while offering multi-protocol storage to meet hybrid-cloud requirements. Telecom operators, notably Safaricom and MTN, are complementing government efforts by bundling edge colocation with 5G roll-outs, which further lifts demand for scalable storage nodes in secondary cities. Over the medium term these public-sector anchor tenants will temper market volatility and sustain recurrent revenue streams for providers that align with evolving national standards.

Surge in Hyperscale and Colocation Data-Center Investments

Global hyperscalers are injecting unprecedented capital into regional facilities, cementing Africa’s ascent from peripheral hosting location to strategic cloud growth engine. Microsoft’s USD 1 billion geothermal-powered complex in Kenya illustrates how energy innovation is becoming a prerequisite for large-scale deployment.[1]Microsoft, “Microsoft to Invest $1 Billion in Geothermal-Powered Data Center in Kenya,” microsoft.com Equinix’s USD 390 million five-year plan across Johannesburg and Lagos signals a long-term commitment to local interconnection ecosystems.[2]Equinix, “Equinix to Invest $390 Million in South African Expansion,” equinix.com These projects introduce economies of scale that compress $/GB pricing while elevating technical baselines such as NVMe over Fabrics adoption. Colocation providers are responding with build-to-suit halls and green-power purchase agreements that make them attractive partners for hyperscalers lacking direct land or grid access. As cross-connect demand rises, storage vendors positioned in channel alliances with facility operators gain faster market entry and early-mover credibility.

Accelerated SME Cloud Adoption

Small and midsize African enterprises are leapfrogging on-premises infrastructure by embracing domestic cloud services that satisfy data-residency mandates and lower capex. Government-backed entrepreneurship programs in Ghana and Rwanda subsidize cloud onboarding, accelerating multi-tenant demand for elastic storage. Fintech start-ups, pressured by real-time transaction monitoring and local processing rules, are driving continuous growth in object and file storage capacity. The result is heightened need for workload-aware tiering that balances SSD performance with HDD economics, favoring suppliers able to integrate adaptive caching and consumption-based pricing. Short sales cycles and word-of-mouth reference deals in the SME space present a near-term volume opportunity for vendors bundling training, billing, and cybersecurity services.

Transition from HDD to Flash Arrays for Energy Efficiency

Data-center operators across South Africa and Egypt are pivoting toward flash-centric architectures to reduce operational power draw and floor-space usage. Seagate’s life-cycle analysis shows manufacturing emissions for HDDs are lower, yet flash arrays deliver stronger watts-per-IOPS once installed.[3]Seagate Technology, “HDD and SSD Life-Cycle Assessment White Paper,” seagate.com Teraco’s 120 MW solar investments exemplify how renewable energy availability pairs well with low-latency SSD storage, especially as AI inference tasks rise. Vendors are now offering hybrid configurations that auto-tier hot datasets to NVMe drives while relegating cold archives to high-capacity helium HDDs, achieving a balanced sustainability profile. Energy-based SLAs are emerging in colocation contracts, and storage suppliers that quantify kilowatt reductions can command premium positioning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unreliable power supply | -1.8% | Sub-Saharan Africa (ex-South Africa) | Long term (≥ 4 years) |

| Multi-vendor performance issues | -0.9% | Enterprise segments | Medium term (2-4 years) |

| Shortage of certified storage engineers | -1.1% | Nigeria, Kenya, Ghana | Medium term (2-4 years) |

| Currency-driven CAPEX inflation | -1.4% | Nigeria, Ghana, Kenya | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited and Unreliable Power Supply Elevating TCO

Chronic electricity shortfalls in markets such as Zambia, Tanzania, and Côte d’Ivoire continue to inflate the total cost of operating data centers. Government policies now compel facilities to source backup generation, but diesel dependence escalates opex and complicates carbon reporting. Operators therefore favor storage arrays that deliver high performance per watt, pushing suppliers toward controller chiplets, advanced compression, and intelligent spin-down for bulk drives. Power constraints also accelerate the adoption of micro-edge sites that run on solar-battery hybrids, where equipment must tolerate voltage fluctuations and higher ambient temperatures. Vendors that embed predictive power-quality analytics and remote firmware updates mitigate downtime risk for customers navigating unstable grids.

Shortage of Certified Storage Engineers

The pool of professionals certified on SAN zoning, NVMe over TCP, and advanced data-reduction techniques remains shallow across most African economies. As a result, enterprises struggle to maintain heterogeneous environments combining legacy Fibre Channel frames with modern software-defined storage. Major vendors are rolling out remote-managed offerings, orchestration templates, and Kubernetes operators that abstract low-level complexity, thereby reducing reliance on scarce mid-level engineers. Training alliances, such as those between OEMs and polytechnics, are beginning to widen the talent funnel, yet the medium-term gap still restrains large-scale migrations. This scarcity elevates vendor stickiness once a platform is chosen, intensifying competition around ease-of-deployment and automation depth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: SAN Dominance Faces NAS Disruption

SAN maintained leadership with 43.6% share of the Africa data center storage market in 2024, buoyed by entrenched deployments in core banking and government workloads that require deterministic throughput. Network Attached Storage, however, is set to chip away at this lead through a 14.2% CAGR, aided by AI and analytics applications that thrive on scalable file-sharing protocols. Enterprises introducing containerized microservices are finding NAS easier to integrate with Kubernetes CSI drivers, while SAN continues to hold critical OLTP databases where latency spikes carry financial risk. Direct-Attached Storage persists in edge nodes, offering a low-cost fail-fast architecture for content-delivery caches. Object storage, although still niche, is gaining regulatory traction for immutable backup compliance.

In outlook, SAN suppliers are augmenting Fibre Channel with NVMe-FC to sustain relevance, while NAS vendors introduce scale-out clusters that deliver multi-metadata-server resilience and single-namespace simplicity. Dell’s PowerScale upgrades illustrate this hybrid-performance push, showcasing AI-tuned throughput that permits real-time model training. The Africa data center storage market will therefore see converged designs that expose block, file, and object protocols within unified appliances, ensuring buyers can stage workloads without forklift upgrades. As capital budgets remain sensitive to foreign-exchange swings, multi-protocol versatility will increasingly influence total acquisition cost assessments.

By Storage Type: Flash Arrays Accelerate Despite HDD Resilience

HDD arrays retained 46.8% of total revenue in 2024 thanks to unmatched dollars-per-terabyte economics suitable for surveillance, media repositories, and compliance archives across the Africa data center storage market. Yet all-flash arrays are tracking a 13.4% CAGR as hyperscalers and fintechs prioritize 100 µs latency for AI inference and digital-payment reconciliation. Western Digital’s 100 TB HAMR roadmap keeps spinning media relevant in exabyte-scale deployments. In parallel, tier-0 storage is shifting toward QLC-based NVMe drives with dynamic wear-levelling, which lowers cost gaps while preserving performance.

Hybrid architectures merge these tiers, calling policy-driven engines that analyze access frequency and transparently migrate blocks, thus optimizing operating expenditure. Sustainability considerations will remain prominent: Seagate’s carbon‐footprint study reveals HDDs emit fewer manufacturing emissions than SSDs, steering eco-sensitive buyers toward mixed media estates. Over the forecast horizon, suppliers capable of orchestrating auto-tiering across HDD, TLC, and QLC SSD will capture share as customers seek equilibrium between green metrics and workload performance.

By Data Center Type: Hyperscalers Drive Market Transformation

Colocation facilities captured 56.4% revenue in 2024, propelled by enterprises divesting from on-premises rooms and seeking carrier-neutral interconnectivity within the Africa data center storage market. Hyperscalers and cloud providers, however, are expanding fastest at 16.5% CAGR as they localize compute zones to comply with in-country data statutes. Microsoft’s ZAR 5.4 billion Cape Town and Johannesburg expansions create anchor tenants whose scale influences regional price points and technical standards. Huawei’s Nigeria cloud region signals a widening footprint of mainland China vendors in West Africa.

Edge micro-data-centers are emerging around cell towers and industrial campuses, where latency below 20 ms is vital for IoT and video analytics. These distributed sites often adopt disaggregated storage nodes with NVMe-over-TCP links back to central pods, forming a mesh that balances performance with hardware cost. Both colocation and hyperscale environments now stipulate renewable energy ratios, compelling storage suppliers to demonstrate power-efficient controllers and granular telemetry for carbon accounting.

By End User: Healthcare Emerges as Growth Leader

The IT and telecommunications vertical maintained 34.4% of 2024 revenue, sustaining demand for petabyte-scale content caching and subscriber data management. Healthcare and life sciences is the fastest riser, charting a 13.8% CAGR as electronic-health-record mandates and genomic research require secure, high-throughput storage. Grifols Egypt’s plasma-derivative project underscores how life-science production chains rely on validated storage for regulatory traceability. BFSI continues to modernize through containerized cores and fraud-detection analytics, prompting upgrades from RAID-10 HDD to latency-sensitive NVMe tiers.

Government agencies remain pivotal buyers, driven by citizen-service digitization and electronic-archives standardization. Media and entertainment companies increasingly adopt collaborative NAS clusters to edit and stream UHD content, while manufacturing firms, though cautious on capex, begin integrating edge storage within smart-factory pilots. Industry-specific compliance—HIPAA analogues in health, PCI-DSS for payments—shapes procurement, making turnkey encryption and auditing indispensable.

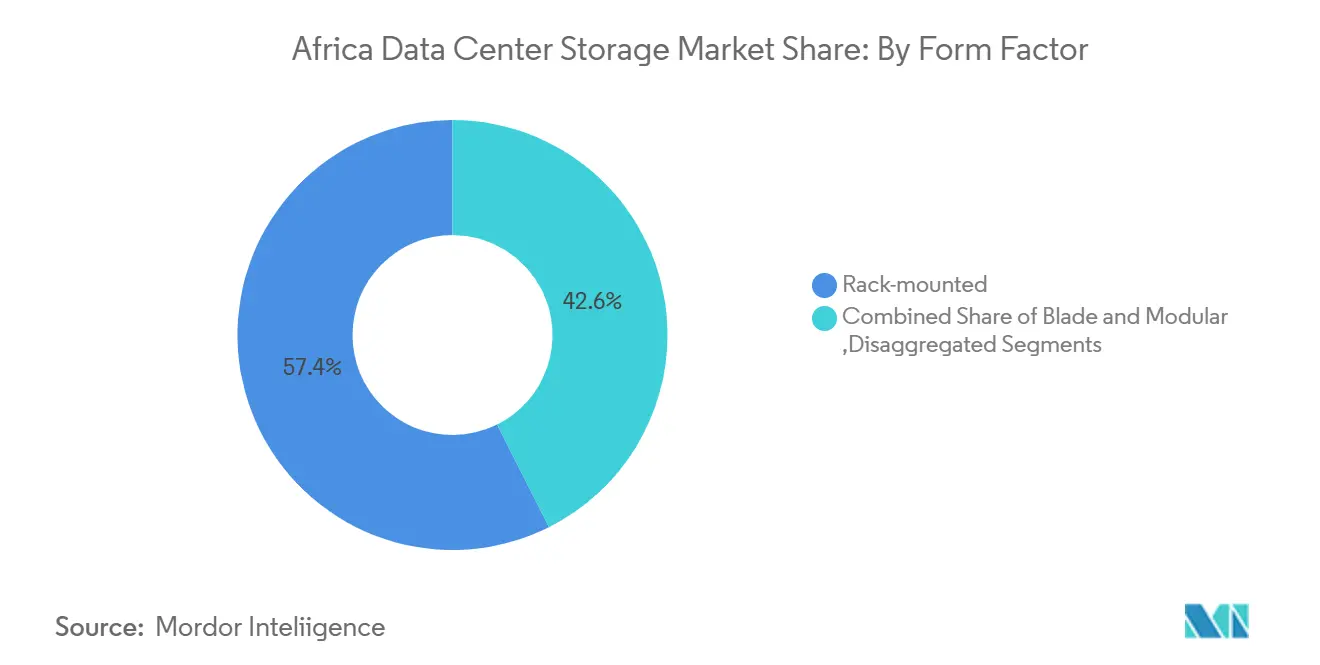

By Form Factor: Disaggregated Solutions Gain Momentum

Rack-mounted appliances delivered 57.4% of 2024 shipments due to compatibility with standard 19-inch cabinets that dominate African facilities. Disaggregated and composable infrastructures, projected to grow at 15.7% CAGR, allow independent scaling of compute, GPU, and storage sleds via CXL and Ethernet fabric. Dell’s DC-MHS blueprint reflects vendor consensus that modularity eases refresh cycles and aligns with circular-economy goals. Blade and modular servers stay relevant where high-density compute meets stringent power envelopes, notably in metro edge sites.

Composable ecosystems enable operators to pool NVMe drives across a rack and allocate them on demand, driving up utilization and cutting stranded capacity. Hitachi’s long-haul storage virtualization over 600 km proves that geographically separated assets can perform as a single array without sacrificing consistency. As African telcos deploy nationwide 5G backbones, these capabilities will allow them to stage low-latency storage near subscribers while managing it from central NOC locations.

By Interface: NVMe Adoption Accelerates Performance Transition

SAS/SATA interfaces still accounted for 53.4% shipments in 2024 due to broad OS support and cost-efficient drive ecosystems, but NVMe is accelerating at 15.6% CAGR as AI and data-science pipelines demand microsecond latency. Pure Storage’s GenAI Pod integrates NVIDIA GPUs with NVMe fabric, showcasing a vertical stack tailored for model training. Fibre Channel retains a niche in legacy SAN estates, and iSCSI persists where 10 GbE networks dominate.

NVMe over Fabrics adoption hinges on affordable RDMA-capable switches that hyperscalers can import in bulk. Dell’s ObjectScale update enabling S3 over RDMA illustrates how object storage is also entering the NVMe era, improving GPU utilization by removing network bottlenecks. Hybrid controllers that expose SAS, SATA, and NVMe front-ends within a single chassis will shield customers from premature forklift upgrades while easing incremental transition to high-speed protocols.

Geography Analysis

South Africa held 38.5% of 2024 revenue owing to robust fiber backbones, established financial hubs, and renewable-energy investments that underpin large-scale storage deployments. Teraco’s USD 680 million debt raise to add 100 MW capacity illustrates ongoing hyperscale appetite; the operator targets 200 MW installed by 2027 while sourcing 50% power from solar arrays. Domestic banks and mining conglomerates, early adopters of SAN clusters, now transition toward hybrid NVMe-flash arrays for AI-driven risk modeling and predictive maintenance, cementing South Africa’s position as a performance-tier market within the Africa data center storage market.

Nigeria, posting 13.2% CAGR to 2030, benefits from a booming fintech scene, an 85% mobile-broadband penetration, and federal directives for local data residency. Huawei’s Lagos cloud region is channeling investment into Tier III facilities, while local providers offer price points tailored to naira-denominated budgets. SMEs shift to object storage for compliance logs, and state governments in Lagos and Abuja deploy archival arrays to digitize land records, broadening demand beyond financial services.

Kenya’s renewable-energy mix attracts sustainability-minded hyperscalers; Microsoft’s geothermal facility in Naivasha exemplifies how green-power availability dictates site selection. Egypt, leveraging Suez Canal connectivity and government data-center megaprojects, positions itself as a North Africa bridge to Europe and the Gulf. Morocco, with Oracle’s twin public-cloud regions, complements this triangle by offering a proximate, low-latency jump-off to Iberian networks. In the rest of Africa, submarine-cable landings stimulate smaller coastal economies, yet unreliable grid power and currency volatility still temper near-term uptake.

Competitive Landscape

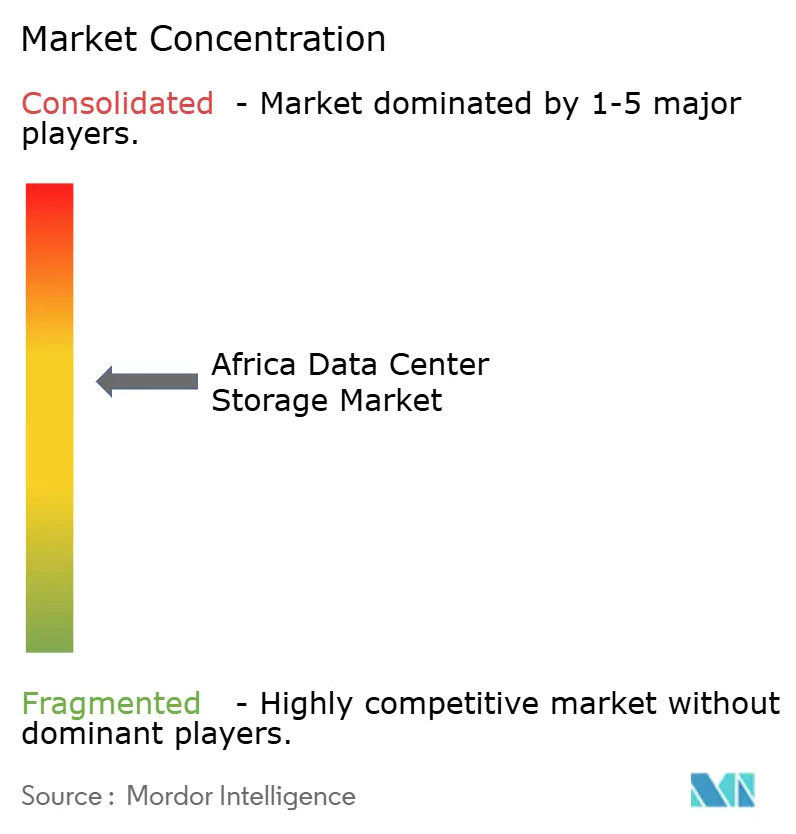

The Africa data center storage market features a mid-tier fragmentation profile where no supplier controls more than 15% regional revenue. Global incumbents—Dell Technologies, Hewlett Packard Enterprise, Pure Storage—leverage established VAR ecosystems and reference wins with banks and telcos. Regional specialists such as Africa Data Centres, Teraco, and Raxio Group build proximity and power-assured facilities, then partner with OEMs for integrated offerings. Raxio’s USD 100 million IFC debt package accelerates its reach into Ethiopia, Mozambique, and the Democratic Republic of Congo, emphasising a carrier-neutral blueprint that appeals to OTT platforms.

Market differentiation increasingly revolves around AI-optimized arrays, immutable-snapshot ransomware protection, and end-to-end energy telemetry. Hitachi Vantara’s alliance with Axiz squares unmet country coverage by bundling training, certified support, and localized spares depots, mitigating the chronic engineer shortfall. Meanwhile, Cassava Technologies’ tie-up with NVIDIA to build Africa’s first AI factory introduces consumption-based GPU storage bundles tailored for model serving, setting new performance baselines.

Africa Data Center Storage Industry Leaders

Dell Inc.

Hewlett Packard Enterprise

Pure Storage Inc.

Huawei Technologies Co. Ltd.

Kingston Technology Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Raxio Group secured USD 100 million debt financing from the International Finance Corporation to fund data-center builds in Ethiopia, Mozambique, and the Democratic Republic of Congo.

- March 2025: Microsoft pledged an additional USD 300 million to expand AI infrastructure within its Cape Town and Johannesburg cloud regions, elevating total investment to ZAR 5.4 billion.

- March 2025: Cassava Technologies and NVIDIA announced an agreement to construct Africa’s first AI factory in South Africa, furnishing secure GPU resources for regional enterprises.

- February 2025: Oracle revealed plans for a new cloud region in Kenya, complementing its dual-region rollout in Morocco.

- November 2025: Teraco raised ZAR 11.8 billion debt to add 100 MW capacity and develop utility-scale solar farms.

- October 2025: INTRO Technology and Oman Data Park signed a USD 450 million MOU to build the Kemet Data Centre in Egypt’s Suez Canal Economic Zone.

- September 2025: Raxio launched a Tier III data center in Côte d’Ivoire, expanding its West Africa footprint.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Africa data center storage market as the annual value, in US dollars, of all dedicated storage hardware and controller software deployed inside commercial colocation, cloud, hyperscale, enterprise, and edge data center facilities across the continent. Devices covered include network-attached, storage-area, direct-attached, object, and flash arrays, as well as the related management software that ships bundled with the hardware.

Scope exclusion: Consumer external drives, CCTV DVRs, and tape libraries used solely for broadcast or archival workflows are not counted.

Segmentation Overview

- By Storage Technology

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Direct Attached Storage (DAS)

- Object and Tape Storage

- By Storage Type

- Traditional HDD Arrays

- All-Flash Arrays (AFA)

- Hybrid Storage

- By Data Center Type

- Colocation Facilities

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By End User

- IT and Telecommunication

- BFSI

- Government and Public Sector

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- By Form Factor

- Rack-mounted

- Blade and Modular

- Disaggregated / Composable

- By Interface

- SAS / SATA

- NVMe

- Fibre Channel and iSCSI

- By Country

- South Africa

- Nigeria

- Kenya

- Egypt

- Morocco

- Rest of Africa

Detailed Research Methodology and Data Validation

Primary Research

We interviewed facility managers at tier-3 colocation sites in Johannesburg, Lagos, Nairobi, and Cairo, OEM channel heads serving West Africa, and CIOs in BFSI and telecom enterprises. These discussions clarified average rack densities, flash-migration timelines, and typical pricing corridors, allowing us to cross-check desk findings and adjust assumptions where required.

Desk Research

Our analysts compiled foundational inputs from open, high-credibility sources such as the International Telecommunications Union's data-traffic dashboards, Africa Data Centres Association capacity surveys, TeleGeography submarine-cable maps, South African Revenue Service customs codes for HS 8471 and 8473, and Central Bank filings that reveal local ICT capex trends. Company 10-Ks, investor decks, and procurement notices enriched shipment estimates, while D&B Hoovers furnished revenue splits for suppliers active in Africa. Regulatory notes from the African Union's Digital Transformation Strategy helped verify data-sovereignty triggers. The list is illustrative; many other public and paid references were consulted during validation.

Market-Sizing & Forecasting

A hybrid top-down and bottom-up model is employed. We first project the continent's installed rack base using announced megawatt builds and utilization ratios, then multiply by forecast terabytes per rack and blended $/GB to deliver a preliminary value. Supplier roll-ups, channel checks, and sampled average-selling-price times shipped units provide a bottom-up sense check that guides any recalibration. Key variables include new hyperscale megawatt additions, regional data-traffic growth, flash-to-disk price spreads, rack density change, and enterprise cloud-migration rates. Multivariate regression, supported by scenario analysis for power-grid constraints, underpins the 2025-2030 outlook. Where shipment gaps exist, we impute values from import traces and warranty registrations, applying conservative uplift factors tested in prior cycles.

Data Validation & Update Cycle

Outputs pass three layers of review: automated variance scans, peer analyst checks, and senior sign-off. Anomalies exceeding set thresholds trigger re-contact with primary sources. Reports refresh yearly; major hyperscale investment announcements or tariff changes prompt interim updates, and a last-mile audit is completed just before client delivery.

Why Our Africa Data Center Storage Baseline Earns Trust

Published estimates often differ because firms vary geography, product scope, and refresh cadence.

Key gap drivers here include whether software licenses are bundled, if self-built hyperscaler capacity is counted, and the currency conversion date applied. Mordor's scope aligns strictly to storage hardware and attached management software deployed within African facilities, excludes construction spend, and converts to USD at the IMF annual average, thereby avoiding double counting and rate noise.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.77 B (2025) | Mordor Intelligence | - |

| USD 0.69 B (2025) | Regional Consultancy A | Omits hybrid arrays and uses lower ASP benchmarks |

| USD 0.69 B (2025) | Trade Journal B | Captures only hardware shipments, excludes bundled software support |

| USD 2.71 B (2023) | Global Consultancy A | Covers Middle East & Africa and folds in power & cooling equipment |

The comparison shows smaller regional studies narrow their scope, while broader global ones inflate totals by mixing adjacent spend buckets. By selecting clear boundaries, verifying volumes with on-the-ground interviews, and refreshing annually, Mordor delivers a balanced, transparent baseline that users can reproduce and defend.

Key Questions Answered in the Report

What is the current size of the Africa data center storage market?

The Africa data center storage market size stands at USD 0.77 billion in 2025 and is projected to reach USD 1.30 billion by 2030.

Which storage technology leads the market?

Storage Area Network solutions lead, holding 43.6% share in 2024, although Network Attached Storage is growing faster at a 14.2% CAGR.

Why are hyperscalers investing heavily in Africa?

Data-residency laws, renewable-energy potential, and under-sea cable connectivity motivate hyperscalers to localize cloud regions, accelerating market growth

Which country shows the fastest growth?

Nigeria posts the highest forecast CAGR at 13.2% through 2030, driven by fintech expansion and local cloud adoption.

How are power constraints influencing storage choices?

Operators favor energy-efficient flash arrays and hybrid architectures to curb operational power draw, especially in regions with unreliable grids.

What is the key restraint hindering market expansion?

Limited availability of certified storage engineers constrains complex deployments, prompting demand for managed services and automation-driven solutions.

Page last updated on: