Soil Stabilization Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 27.23 Billion |

| Market Size (2031) | USD 34.92 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Soil Stabilization Market Analysis by Mordor Intelligence

The Soil Stabilization Market size is projected to expand from USD 26.05 billion in 2025 and USD 27.23 billion in 2026 to USD 34.92 billion by 2031, registering a CAGR of 5.10% between 2026 to 2031. Governments and private developers are shifting from patch-and-repair approaches toward proactive, long-lifecycle ground improvement to curb deferred-maintenance costs and embodied-carbon liabilities. The American Society of Civil Engineers cites a USD 2.6 trillion infrastructure funding gap in the United States that is now translating into multiyear demand for cost-effective stabilization techniques. At the global level, the OECD estimates that USD 6.9 trillion per year through 2030 is required to meet infrastructure needs—roads, railways, and industrial platforms where stabilized subgrades are non-negotiable. Rising scrutiny of cement and lime emissions is accelerating the adoption of polymer, enzyme, and microbial binders that achieve comparable strength with a fraction of the carbon footprint. Supply-chain realignments such as nearshoring in North America and the e-commerce warehousing boom in Asia-Pacific are expanding commercial-site foundations, a sub-sector advancing faster than residential and industrial construction.

Key Report Takeaways

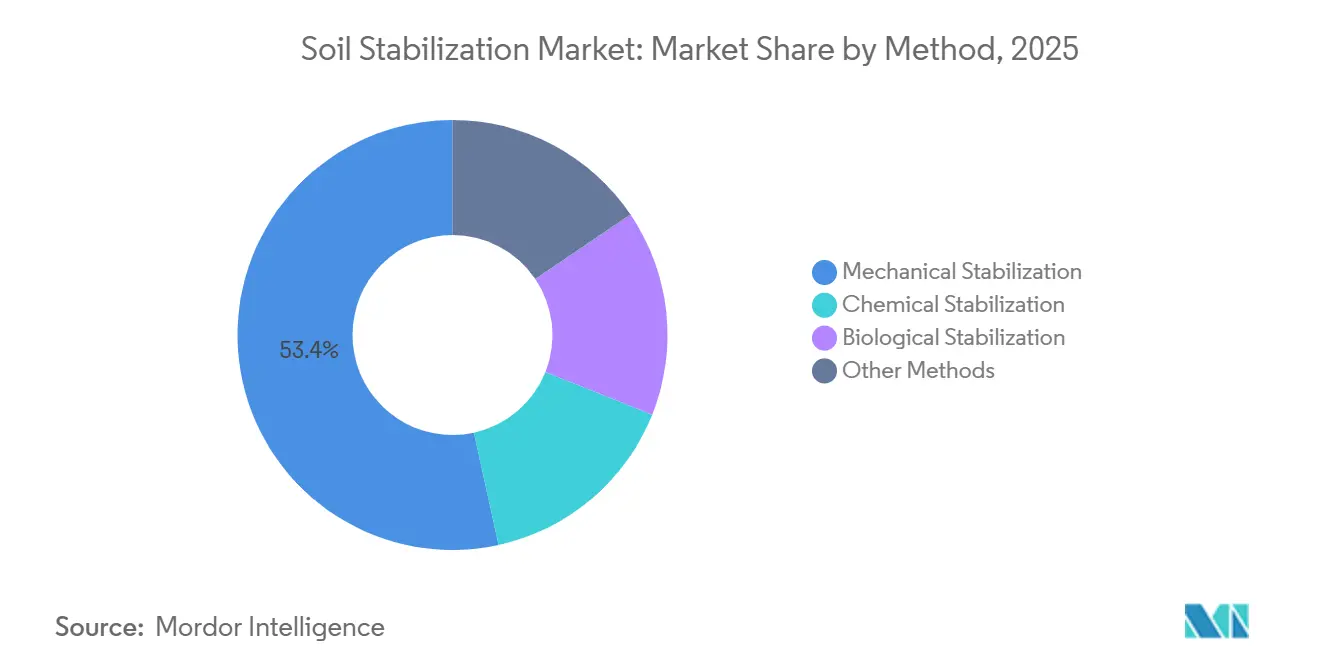

- By method, mechanical stabilization led with 53.44% of the soil stabilization market share in 2025, while biological stabilization is projected to post the fastest 5.79% CAGR through 2031.

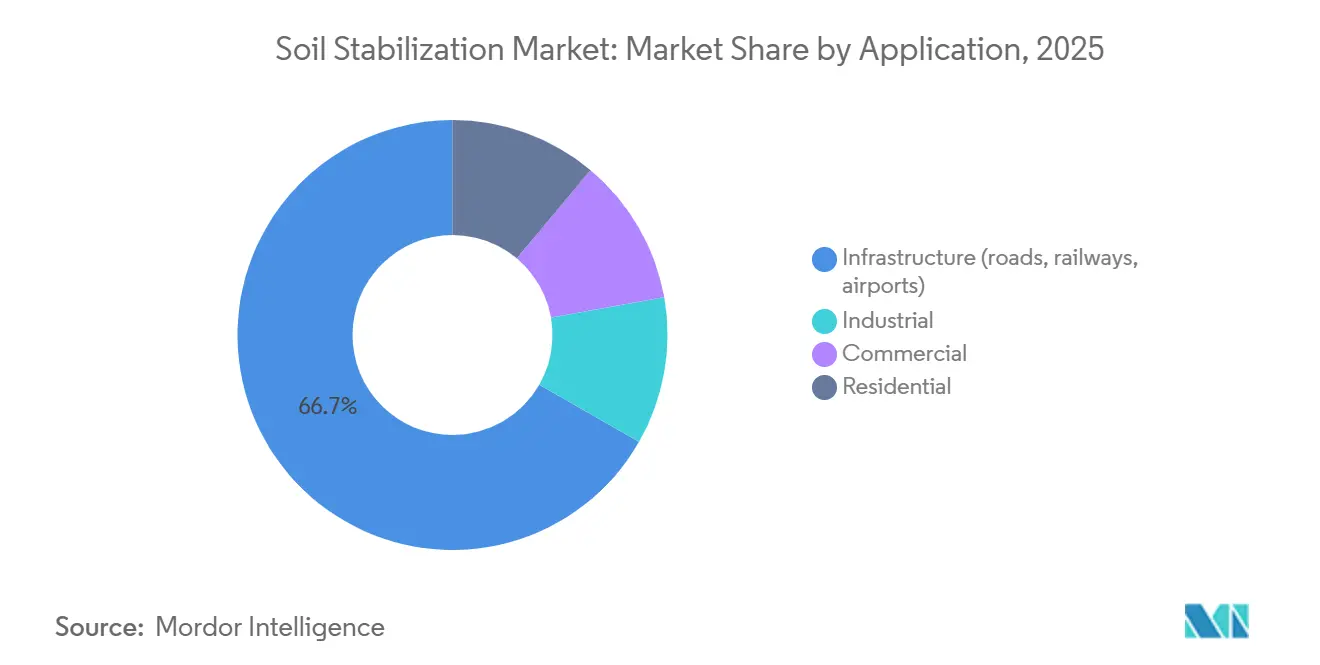

- By application, infrastructure accounted for 66.71% of the soil stabilization market share in 2025, while commercial is forecast to expand at a 5.70% CAGR through 2031.

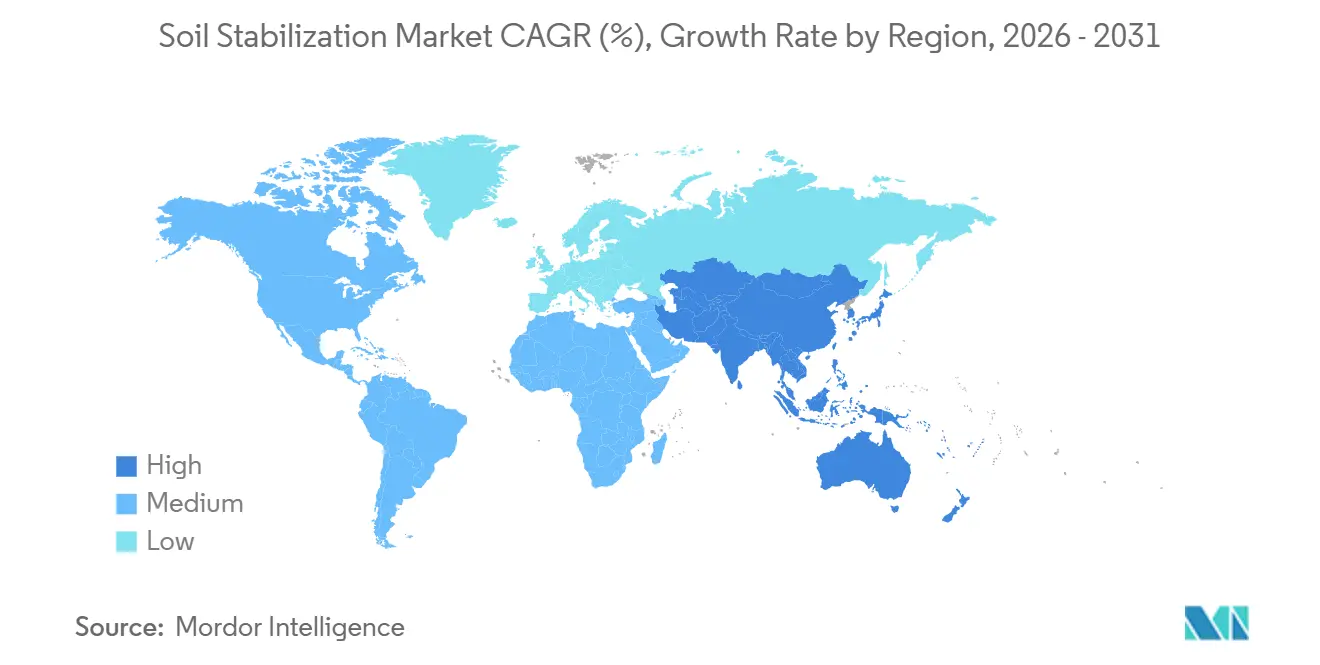

- By geography, Asia-Pacific captured 42.39% of the soil stabilization market share in 2025 and is advancing at a 6.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Soil Stabilization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in global infrastructure and road-building programmes | +1.8% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Urban-driven industrial and commercial land development | +1.2% | APAC core, spill-over to MEA and South America | Medium term (2-4 years) |

| Stricter performance and carbon regulations for pavements | +1.0% | North America and EU, early adoption in APAC urban centers | Long term (≥ 4 years) |

| Climate-resilient infrastructure spending | +0.7% | Global, prioritized in coastal and flood-prone regions | Long term (≥ 4 years) |

| Renewable mega-projects requiring ground improvement | +0.4% | APAC, Middle-East, and select EU markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growth in Global Infrastructure and Road-Building Programs

The United States Infrastructure Investment and Jobs Act earmarks USD 1.2 trillion, of which USD 550 billion is new federal expenditure on roads, bridges, and transit systems; by early 2026 more than 7,000 projects had moved into procurement, each requiring subgrade preparation or pavement recycling. India’s Bharatmala Pariyojana and Pradhan Mantri Gram Sadak Yojana collectively span 34,800 kilometers of highways and rural roads that specify lime or cement treatment for black-cotton soils. China’s 14th Five-Year Plan funnels bond-financed investments into high-speed rail and rural connectors crossing expansive clay and loess, where compaction and chemical binders prevent seasonal heave. The World Bank delivered USD 50.8 billion in climate finance during fiscal 2025, funding irrigation and feeder-road upgrades across sub-Saharan Africa and Southeast Asia that deploy stabilization to curb washouts. Maintenance economics reinforce the trend: every USD 1 spent on timely maintenance averts USD 1.50 in later reconstruction outlays, pushing agencies toward full-depth reclamation and in-place recycling[1]Federal Highway Administration, “Lifecycle Benefits of Full-Depth Reclamation,” fhwa.dot.gov .

Urban-Driven Industrial and Commercial Land Development

UN projections show the urban population climbing from 3.9 billion in 2020 to 6.3 billion by 2050, intensifying demand for industrial parks, data centers, and logistics hubs on marginal peri-urban soils. Warehouse floor-plates exceeding 50,000 m² in India’s National Industrial Corridor Program rely on cement and polymer binders to transform soft clays into high-bearing foundations. Data-center operators stipulate differential-settlement limits of 25 mm across 30 m, driving uptake of deep soil mixing and polymer-modified layers. Mexico’s nearshoring surge concentrates factories on expansive clays along the U.S. border, where lime stabilization mitigates shrink-swell risks. Gulf mega-projects such as NEOM integrate stabilization to guard pavements against wind-blown sand and settlement on sabkha crusts.

Stricter Performance and Carbon Regulations for Pavements

The U.S. EPA’s Carbon-Reducing Materials for Our Roads program funds state DOTs that cut pavement embodied carbon through alternative binders. California’s Buy Clean Act sets global-warming-potential ceilings for cement used in state projects, spurring enzyme and biopolymer adoption. The EU Carbon Removal Certification Framework quantifies sequestration in construction materials, creating credits for microbial-induced calcite precipitation. Cement manufacture already contributes about 8% of global CO₂ emissions, and lime emits 0.9-1.2 kg CO₂ per kg of product, placing traditional binders under decarbonization pressure. Field pilots in Australia and the Netherlands confirm enzyme stabilizers can deliver compressive strengths within 15% of lime-treated controls at one-tenth of the carbon footprint.

Climate-Resilient Infrastructure Spending

Climate disasters generated USD 1.6 trillion in losses in the 2010s, seven times the 1970s average, prompting agencies to fortify assets against flood, subsidence, and heat. The World Bank’s Global Facility for Disaster Reduction and Recovery co-finances low-volume roads in monsoon regions, specifying stabilization for erosion resistance. Bangladesh and Vietnam insert cement-bentonite cut-off walls in embankments to block saltwater intrusion, lengthening coastal-road life. Arctic permafrost thaw in Canada and Alaska is tackled with insulating layers and thermosyphons coupled to mechanical compaction. Dust-suppression polymers keep African rural roads trafficable during drought, reducing regrading cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Environmental and lifecycle-CO₂ concerns over chemical binders | -0.6% | North America and EU, emerging in APAC urban centers | Medium term (2-4 years) |

| Skills and awareness gaps in emerging economies | -0.3% | Sub-Saharan Africa, South Asia, and rural Latin America | Short term (≤ 2 years) |

| Substitution by next-gen geosynthetics and geocells | -0.2% | Global, with faster adoption in EU and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Environmental and Lifecycle-CO₂ Concerns Over Chemical Binders

Cement and lime face scrutiny for carbon intensity and potential alkaline leachate that can mobilize heavy metals. Cement accounts for 8% of global CO₂ emissions; lime emits up to 1.2 kg CO₂ per kg produced[2]International Energy Agency, “Cement Tracking Report 2025,” iea.org . EU lifecycle studies show that substituting 50% of cement with slag or fly-ash cuts embodied carbon 30-40% but supply constraints limit scale. California and Dutch agencies now require pre-treatment testing whenever lime is specified near groundwater. Investment is flowing into microbial-induced calcite precipitation that binds soil with negligible direct emissions yet still faces curing-time and field-scale challenges.

Skills and Awareness Gaps in Emerging Economies

Advanced methods such as enzyme dosing, biopolymer mixing, and deep soil mixing demand trained crews and quality controls lacking in many developing regions. The International Labour Organization reports construction-sector skill shortages compounded by an aging workforce and under-funded vocational systems. Poor access to on-site pH and moisture testing diminishes enzyme efficacy. Procurement officials often default to cement because lifecycle costing is unfamiliar. Donor programs now bundle capacity-building workshops and demonstration plots, yet diffusion remains uneven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Method: Mechanical Dominance Meets Biological Disruption

Mechanical stabilization contributed 53.44% to soil stabilization market share in 2025, supported by ubiquitous rollers and recyclers that fit legacy workflows. Wirtgen Group’s in-situ recyclers cut aggregate haulage and embodied emissions, helping state DOTs meet pavement-life targets. Chemical techniques—cement, lime, polymers, enzymes—address soils where compaction alone cannot hit required California Bearing Ratio thresholds. Biological stabilization is projected to deliver a 5.79% CAGR to 2031, the fastest among methods, as regulators recognize near-zero carbon binders. Peer-reviewed trials show xanthan-gum soils reach 70-80% of cement-treated unconfined compressive strength and reduce permeability by 90% in sandy matrices. Thermal and electrokinetic variants remain niche for contaminated or deep excavations. The segmentation underscores tension between mechanical simplicity and the performance-plus-carbon gains of chemical and bio options.

By Application: Infrastructure Anchors Growth, Commercial Surges

Infrastructure commanded 66.71% of revenue in 2025 as roads, railways, and airports rely on stabilized subgrades to defer resurfacing. Full-depth reclamation blends worn asphalt with binders, lowering virgin aggregate use by up to 50% while lifting pavement service life beyond 20 years. Runway designers mandate 95-100% maximum-dry-density compaction, adding cement or lime when native soils fall below strength thresholds. Commercial construction is set to grow at a 5.70% CAGR through 2031, the fastest among applications. The soil stabilization market size for commercial platforms is rising in China’s Yangtze River Delta and India’s logistics corridors, where soft silts must support automated racking systems. Hyperscale cloud providers cap differential settlement at 25 mm, steering projects to deep soil mixing and polymer-cement blends. Industrial and residential segments trail due to cyclical investment patterns and cost sensitivity.

Geography Analysis

Asia-Pacific held a 42.39% share in 2025 and is projected to climb at a 6.13% CAGR to 2031, making it the largest and fastest-growing regional slice of the soil stabilization market. China’s bond-financed road and high-speed rail rollout crosses expansive clays and loess that demand lime or cement treatment to contain seasonal swelling. India’s Bharatmala Pariyojana and rural connectivity schemes embed stabilization specs in contracts covering 34,800 km of corridors, especially across black-cotton-soil belts. ASEAN’s Master Plan on Connectivity, supported by the Asian Development Bank, earmarks soft-soil deltaic projects that deploy deep mixing and geogrid reinforcement. Japan’s seismic retrofits rely on high-pressure jet grouting beneath coastal expressways, and Australia’s mining haul roads use polymer emulsions to suppress dust on unpaved surfaces.

North America benefits from the USD 1.2 trillion Infrastructure Investment and Jobs Act; more than 7,000 schemes had reached planning or tender by 2026, many specifying in-place recycling with stabilizers to curb trucking emissions. Canada’s Investing in Canada Infrastructure Program co-funds highway upgrades where freeze-thaw cycles justify geosynthetic inserts plus chemical treatment, while Mexico’s nearshoring corridor uses lime on expansive clays to guard plant foundations.

Europe’s growth aligns with the Green Deal mandate to decarbonize construction. Germany now allows recycled concrete and steel slag in cement-stabilized bases, trimming embodied carbon. U.K. trunk roads test enzyme binders that promise 80% carbon cuts versus lime; NORDIC countries designs pair mechanical compaction with insulation to protect permafrost routes. These initiatives collectively lift the regional soil stabilization market while steering it toward low-carbon chemistries.

The Middle-East and Africa combine Gulf mega-projects—NEOM, Red Sea, Qiddiya—with donor-funded rural-access roads. Sabkha soils around the Red Sea require deep replacement or chemical binders, while African feeder roads employ laterite improvement and polymer dust suppressants financed by multilateral lenders. South America leans on Brazilian and Argentine concession models that reward lifecycle-cost savings, channeling investment into full-depth reclamation and cement-treated bases that withstand tropical rainfall and heavy freight.

Competitive Landscape

The soil stabilization industry remains moderately fragmented. Holcim’s USD 8.1 billion takeover of Sika in 2023 formed an integrated giant supplying cement, admixtures, and on-site expertise, ideal for turnkey public works. BASF and Dow exploit polymer science to offer emulsions and superabsorbent binders tailored for dust-control roads in arid zones. Wirtgen Group, under John Deere, dominates equipment through soil stabilizers and recyclers backed by a global dealer network. Niche players such as Midwest Industrial Supply and Soilworks provide lignosulfonate and biopolymer formulations that slash water usage on mining haul roads. White-space innovation resides in biological binders: Sika’s new enzyme line, AggreBind’s plant-derived formulations, and a BASF-led joint venture scaling microbial-induced calcite precipitation in the Netherlands signal rapid R&D momentum. Standards organizations ASTM and ISO are drafting test methods that will normalize performance data, indispensable for public-sector acceptance. Digitalization is also reshaping competition, with contractors integrating real-time compaction control, automated binder dosing, and drone verification to minimize rework.

Soil Stabilization Industry Leaders

Carmeuse

HOLCIM

CEMEX S.A.B. de C.V.

Sika AG

GRAYMONT

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Japanese researchers developed a cement-free soil solidifier utilizing industrial waste. This innovation enhanced soil stabilization by achieving a compressive strength exceeding 160 kN/m² and incorporating calcium hydroxide to stabilize arsenic.

- October 2024: Norditek AB secured an order from PreZero to supply a mobile recycling plant designed for soil stabilization. The solution was tailored for applications such as stabilizing contaminated clays for disposal and reinforcing land areas for housing construction.

Global Soil Stabilization Market Report Scope

Soil stabilization involves enhancing the engineering properties of soil, including strength, durability, and bearing capacity, through mechanical or chemical methods. This process is essential in construction projects to prevent foundation settlement, reduce erosion, and address issues such as swelling or high permeability. Common methods include mechanical compaction or the addition of agents like cement, lime, fly ash, or polymers to bind soil particles.

The Soil Stabilization Market is segmented by method, application, and geography. By method, the market is segmented into mechanical stabilization, chemical stabilization, biological stabilization, and other methods. By application, the market is segmented into infrastructure (roads, railways, airports), industrial, commercial, and residential. The report also covers market size and forecasts for soil stabilization in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Mechanical Stabilization |

| Chemical Stabilization |

| Biological Stabilization |

| Other Methods |

| Infrastructure (roads, railways, airports) |

| Industrial |

| Commercial |

| Residential |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Method | Mechanical Stabilization | |

| Chemical Stabilization | ||

| Biological Stabilization | ||

| Other Methods | ||

| By Application | Infrastructure (roads, railways, airports) | |

| Industrial | ||

| Commercial | ||

| Residential | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| Australia | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the soil stabilization market?

The soil stabilization market size is USD 27.23 billion in 2026 and forecast to reach USD 34.92 billion by 2031, expanding at a 5.1% CAGR from 2026.

Which method will grow fastest over the next five years?

Biological stabilization is projected to grow at a 5.79% CAGR through 2031.

Why is Asia-Pacific attracting the highest regional demand?

China’s Belt and Road, India’s highway programs, and ASEAN connectivity corridors together drive a 6.13% CAGR, the highest regional rate.

What carbon regulations are changing binder selection?

U.S. EPA low-carbon road funding, California’s Buy Clean thresholds, and the EU Carbon Removal Certification Framework all push contractors toward low-CO₂ polymers and bio-binders.

Page last updated on: