Software Defined Radio Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

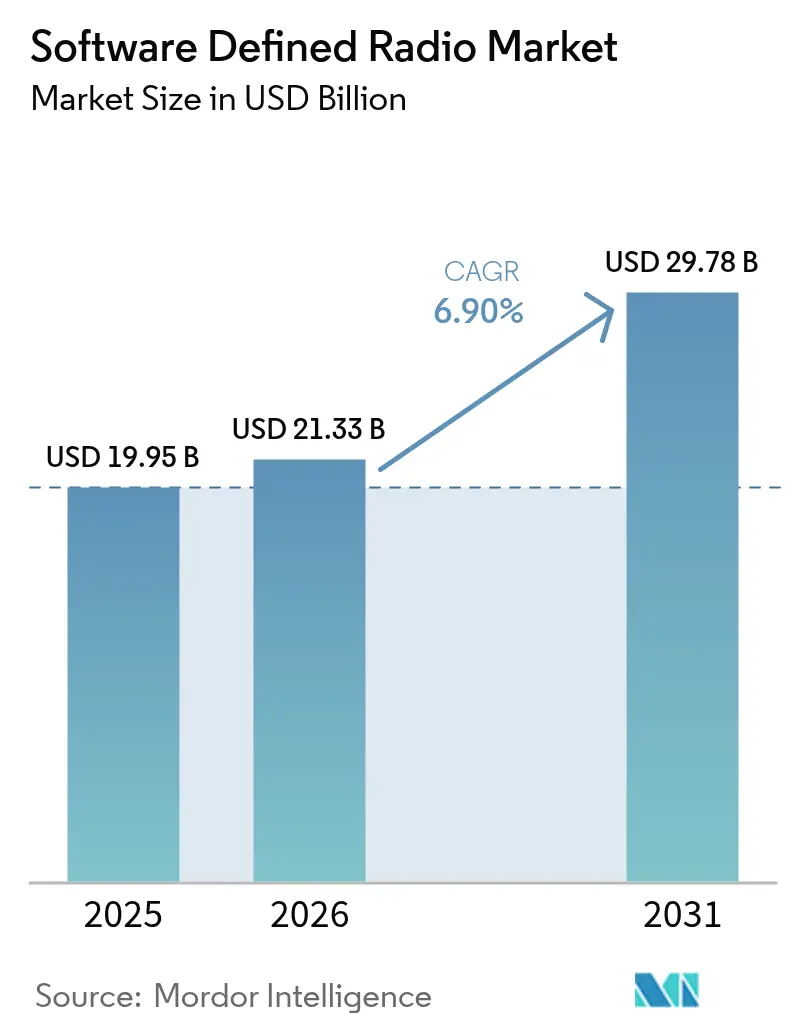

| Market Size (2026) | USD 21.33 Billion |

| Market Size (2031) | USD 29.78 Billion |

| Growth Rate (2026 - 2031) | 6.90% CAGR |

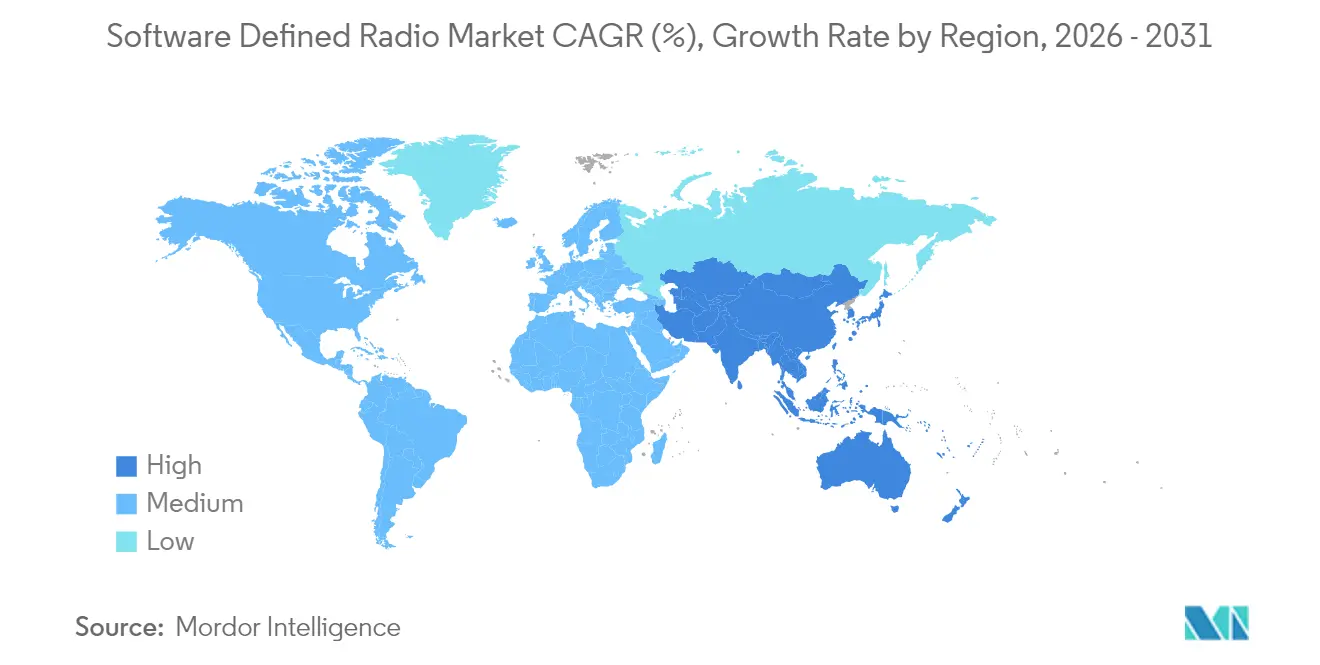

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Software Defined Radio Market Analysis by Mordor Intelligence

The software-defined radio (SDR) market size is expected to grow from USD 19.95 billion in 2025 to USD 21.33 billion in 2026 and is forecast to reach USD 29.78 billion by 2031 at 6.9% CAGR over 2026-2031. Rapid digital-transformation programs in defense, 5G and private-network rollouts, and spectrum-sharing policies underpin this growth. The market momentum is strongest where armed forces migrate to network-centric warfare architectures requiring radios that switch waveforms in seconds. At the same time, commercial operators leverage reconfigurable platforms to shorten time-to-service in Open RAN deployments. Hardware remains the revenue anchor, yet software layers drive differentiation as virtualized base-station functions reach field maturity. Regionally, North America benefits from sustained defense outlays, but Asia-Pacific is closing the gap on the back of high-velocity 5G builds and record military budgets. Export-control regimes, cyber-hardening costs, and thermal-design challenges temper the otherwise robust expansion, compelling suppliers to balance openness with security across military and enterprise ecosystems. Hence, the SDR market continues reinventing modern connectivity across land, sea, air, space, and emerging non-terrestrial networks.

Key Report Takeaways

- By end-user, government and defense held 58.12% of the software-defined radio market share in 2025, whereas the commercial segment is projected to post the fastest 8.05% CAGR through 2031.

- By component, hardware contributed 55.05% of revenue in 2025; software is forecasted to lead expansion at a 7.55% CAGR to 2031.

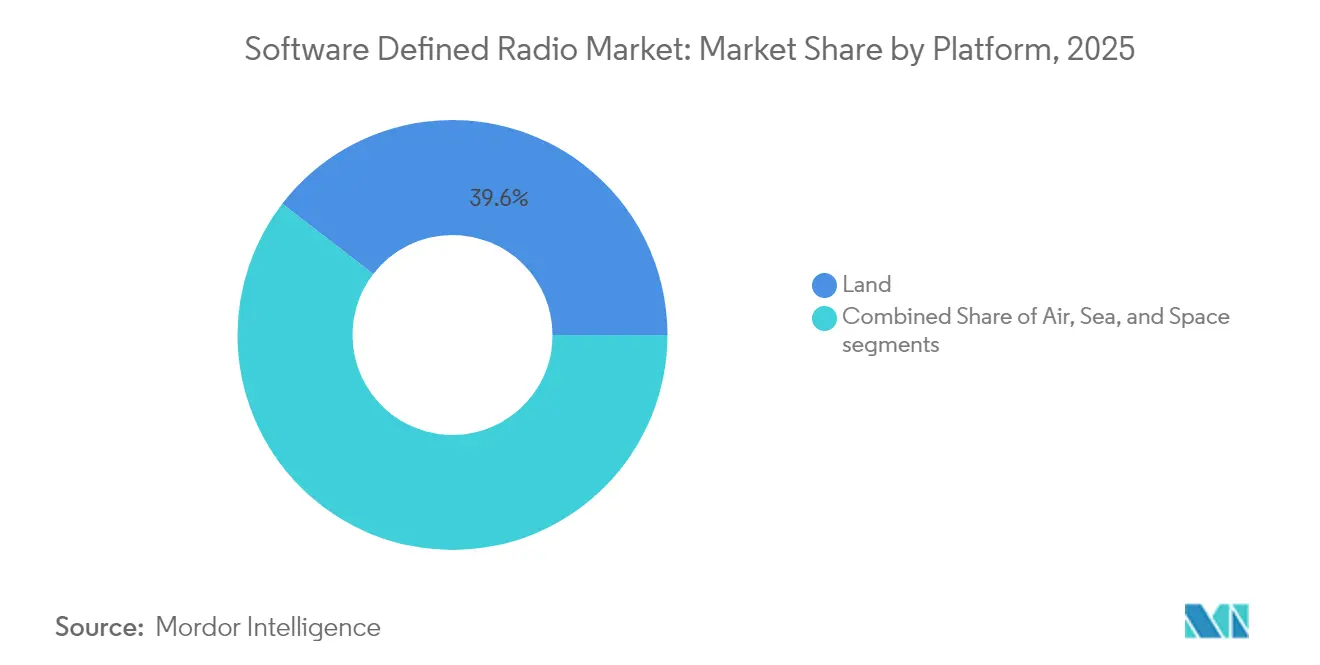

- By platform, land applications accounted for 39.55% of the software-defined radio market size in 2025, while space platforms are set to register the highest 7.95% CAGR during 2026-2031.

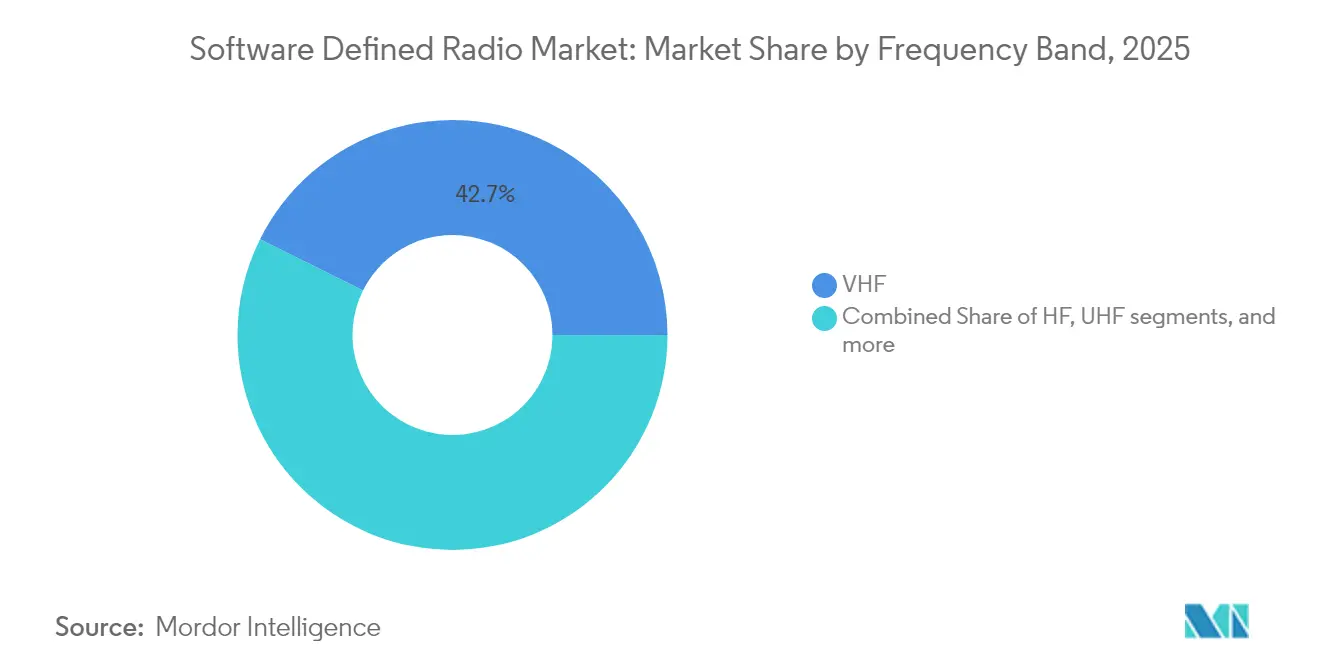

- By frequency band, the Very High Frequency (VHF) category dominated with 42.65% share in 2025; Extremely High Frequency (EHF)/mmWave bands are poised for an 8.4% CAGR to 2031.

- By geography, North America commanded 33.22% of 2025 revenue, yet Asia-Pacific is on track for the quickest 8.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Software Defined Radio Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Transition to network-centric warfare driving next-gen SDR adoption | +1.2% | NATO members, Asia-Pacific | Medium term (2-4 years) |

| Proliferation of 5G and private wireless networks boosting radio infrastructure demand | +1.0% | North America, Europe | Short term (≤ 2 years) |

| Regulatory push for dynamic spectrum access and sharing frameworks | +0.8% | North America, Europe | Long term (≥ 4 years) |

| Expansion of satellite constellations increasing demand for flexible ground terminals | +0.9% | Developed markets worldwide | Medium term (2-4 years) |

| Secure mesh communication needs in UAV swarms elevating SDR relevance | +0.7% | US, Europe, select APAC | Long term (≥ 4 years) |

| Virtualization of base stations through Open RAN accelerating SDR integration | +0.6% | Asia-Pacific, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Transition to Network-Centric Warfare Driving Next-Gen SDR Adoption

Armed forces are standardizing architectures in which every platform—from soldier radios to surface vessels—shares data across a common tactical backbone. This operational shift hinges on radios able to load new waveforms and encryption suites on demand, a requirement that places the SDR market solutions at the center of modernization budgets. The United Kingdom earmarked GBP 2.9 billion (USD 3.99 billion) to acquire such reconfigurable systems. L3Harris secured a USD 999 million US Navy MIDS JTRS contract in 2024, illustrating supplier traction.[1]L3Harris Technologies, “U.S. Navy Awards L3Harris USD 999 Million MIDS JTRS Contract,” l3harris.com Lessons from Ukraine’s fielding of CJADC2 frameworks have further validated SDR’s resilience under dense electronic-warfare environments, accelerating procurement cycles among NATO partners. The driver, therefore, extends beyond conventional communications to homeland-security grids that demand the same waveform agility.

Proliferation of 5G and Private Wireless Networks Boosting Radio Infrastructure Demand

Enterprise digitization compels factories, ports, and campuses to install private 5G systems to merge Wi-Fi, cellular, and sensor traffic on one physical layer. Because each site operates different spectrum slices, operators prefer radios that can switch bands through software, limiting truck rolls. Over 3,000 US organizations registered CBRS installations by late 2024, and AT&T committed USD 14 billion to Ericsson for Open RAN deployments that lean on software-defined radio units.[2]AT&T Corp., “AT&T, Ericsson Sign USD 14 Billion Open RAN Agreement,” att.com The same multi-band versatility is designed into 5G-NTN gateways, enabling seamless switching between terrestrial and Low Earth Orbit links. Consequently, the SDR market addresses classic macro-cell rollouts and bespoke industrial networks.

Regulatory Push for Dynamic Spectrum Access and Sharing Frameworks

Governments aim to unlock underutilized spectrum without displacing incumbent users. The US National Spectrum Strategy prioritizes automated sharing schemes anchored in cognitive radios that detect incumbents and retune autonomously. The European Commission is implementing similar goals via its Radio Spectrum Policy Programme, mandating cognitive functionality in certain bands by 2026. Defense departments complement this by allocating USD 1.8 billion from the Spectrum Relocation Fund to mature sharing technology. Such policies directly reward vendors capable of demonstrating sub-second frequency agility, reinforcing long-run demand within the software-defined radio market.

Expansion of Satellite Constellations Increasing Demand for Flexible Ground Terminals

Mega-constellations ramp from dozens to thousands of satellites, each operating multiple spot beams and occasionally switching frequencies to manage interference. Ground stations must tune across L, S, X, Ku, and Ka bands while preserving phase coherence. CesiumAstro’s SDR-1001 board exemplifies this multi-band capability. The US Space Development Agency’s missile-warning layer likewise embeds reconfigurable payloads supplied by Raytheon that demand equally adaptable gateways. Space-sector spending thus opens an incremental growth lane for the software-defined radio market amid wider defense and telecom opportunities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated capital costs associated with advanced FPGA and ADC integration | -0.8% | Global—price-sensitive markets | Short term (≤ 2 years) |

| Persistent vulnerabilities to cyber threats and electronic jamming | -0.6% | Conflict zones worldwide | Medium term (2-4 years) |

| Export regulations limiting the global deployment of reconfigurable SDR technologies | -0.5% | US and EU export destinations | Long term (≥ 4 years) |

| Thermal constraints hindering high-performance edge computing in SDR systems | -0.4% | Harsh-environment deployments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Elevated Capital Costs Associated with Advanced FPGA and ADC Integration

High-end FPGAs and GHz-class ADCs that underpin today’s wideband SDRs often exceed USD 10,000 per unit for ruggedized variants, limiting affordability for commercial clients. Additional outlays emerge from forced-air or liquid cooling required to dissipate 40-100 W per card under peak workloads. RTX and AMD are co-funding multi-chip packages aimed at doubling performance per watt, with a USD 20 million S2MARTS contract accelerating prototypes. Meanwhile, NXP’s LA9310 shows how integrated RF-DSP silicon priced near USD 250 can unlock entry-level segments. Until such alternatives scale, cost remains a headwind for broader software-defined radio market penetration outside premium defense budgets.

Persistent Vulnerabilities to Cyber Threats and Electronic Jamming

Software-defined radios rely on extensive firmware and networking stacks, creating a wider attack surface than legacy fixed-function radios. Incidents of GPS spoofing against civilian fleets and fake base-station attacks that harvest subscriber data underscore these risks. Defense primes now embed hardware roots-of-trust and waveform-level encryption, but such safeguards add cost and power draw. For enterprises, balancing affordability and cryptographic rigor is still a work in progress, constraining adoption in sectors with regulated security postures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Space Applications Drive Next-Generation Growth

Space systems accounted for a modest revenue slice in 2025, yet are projected to expand at an 7.95% CAGR, the fastest among all platforms. The software-defined radio market size for space-borne terminals is expected to climb steadily as software-reconfigurable payloads enable on-orbit beam steering and dynamic bandwidth allocation. SpainSat NG I, launched in January 2025, features a fully reprogrammable transponder that operators can retune in real time. Land platforms nevertheless held 39.55% of the software-defined radio market share in 2025, anchored by extensive armored-vehicle and manpack upgrades across NATO and Indo-Pacific armies.

The growth of space platforms spills into terrestrial segments because gateways must track dozens of Low Earth Orbit satellites simultaneously. Ground-station vendors integrate multiband SDR cards that switch between S- and Ka-bands to ensure link availability. Naval forces adopt similar gear to bridge ship-borne networks with proliferating satellite constellations. As a result, platform-agnostic architectures dominate supplier roadmaps, reinforcing cross-domain interoperability within the broader software-defined radio market.

By Component: Software Growth Accelerates Hardware Transformation

Hardware captured 55.05% of 2025 revenue; yet the software submarket is forecast to outpace at 7.55% CAGR through 2031. Operators value the ability to download new waveforms over the air rather than dispatch field technicians to swap circuit cards. Consequently, the software-defined radio market size for firmware upgrades and security patches is expanding almost in lock-step with hardware refresh cycles. Telefónica Germany’s rollout of a cloud-native RAN illustrates how containerized signal-processing functions can spin up within minutes on commercial servers.

Hardware advances remain crucial. RTX’s work with AMD targets denser FPGA fabrics that fold AI accelerators directly onto radio boards, boosting spectral-efficiency metrics while trimming latency. Modularization trends also see mezzanine daughter cards hosting frequency-conversion chains, a design that lets integrators tailor radio front-ends to mission profiles. These co-design dynamics ensure silicon innovation and code refinement progress symbiotically inside the software-defined radio market.

By Frequency Band: mmWave Technologies Lead Innovation

Very High Frequency (VHF) solutions serve legacy military and aviation networks and retain 42.65% of 2025 revenue. However, Extremely High Frequency (EHF) and mmWave deployments are accelerating at an 8.4% CAGR as operators light up 26 GHz and 39 GHz cells for urban 5G. Rohde & Schwarz unveiled a 300 GHz analyzer that aids chipset vendors in characterizing above-100 GHz prototypes. Such tools lower entry barriers for firms entering the top end of the software-defined radio market.

Higher frequencies impose stricter line-of-sight and rain-fade constraints, prompting multi-band radios that drop to sub-6 GHz links during adverse conditions. SDR enables this fall-back through adaptive modulation and automatic antenna-path selection, safeguarding quality-of-service commitments. Research at NTT achieved 280 Gbps over 300 GHz backhaul, hinting at 6G architectures where millimeter-wave small cells dominate dense metro zones. Such breakthroughs promise another innovation runway for component suppliers inside the software-defined radio market.

By End-User: Commercial Sector Challenges Defense Dominance

Government and Defense spending represented 58.12% of 2025 revenue because ministries prioritize secure, anti-jam communication. Yet commercial verticals—from manufacturing to mining—are embracing private 5G to power autonomous robots, pushing the segment toward the fastest 8.05% CAGR. The United States tallied over 3,000 CBRS installations in 2024, an early indicator of enterprise momentum. L3Harris leveraged its defense pedigree to secure the Netherlands’ USD 1.1 billion FOXTROT contract, reflecting how military-grade credibility resonates in civil tenders too.

As cloud providers bundle industrial-edge stacks with SDR-powered 5G radios, enterprises can launch networks in weeks rather than quarters. Defense agencies simultaneously adopt commercial-off-the-shelf boards to accelerate R&D and cut sustainment costs. This two-way technology flow blurs traditional boundaries, positioning the broader software-defined radio market as a single continuum catering to mission-critical and revenue-critical applications.

Geography Analysis

North America retained 33.22% of global revenue in 2025, owing to sustained Pentagon budgets and an early lead in CBRS-based private networks. The region’s suppliers locked in large orders such as L3Harris’s USD 999 million Navy MIDS JTRS program and RTX’s USD 646 million SPY-6 radar production lot. Federal Communications Commission policies that authorize shared-spectrum models further accelerate local commercialization. As defense and enterprise channels converge, the software-defined radio market in North America remains a bellwether for global standards and security certifications.

Asia-Pacific posts the highest 8.6% CAGR through 2031, propelled by record USD 411 billion regional defense spending in 2023 and aggressive 5G macro-cell and factory-floor builds. Japanese operator Sky Perfect JSAT contracted Thales for the software-defined JSAT-31 satellite, highlighting the region’s appetite for next-generation space communications. Chinese and South Korean yards outfit naval fleets with reconfigurable radios to coordinate unmanned surface vehicles, widening the addressable base for the software-defined radio market.

Europe maintains steady expansion underpinned by sovereign-secure communications mandates. The United Kingdom’s GBP 2.9 billion (USD 3.98 billion) SDR allocation and France’s Syracuse IV program exemplify sustained institutional funding. The EU’s spectrum policy targets cognitive-radio adoption by 2026, nurturing domestic demand while guiding interoperability norms. European primes also pursue export contracts in the Middle East and Africa, extending geographic reach for solutions engineered to European cybersecurity baselines.

Competitive Landscape

The industry is moderately consolidated. Three longstanding primes—L3Harris Technologies, Inc., Northrop Grumman Corporation, RTX Corporation, Thales Group, and BAE Systems plc—dominate large defense orders by Type-1 security credentials and full-spectrum support portfolios. Yet Open RAN has lowered entry barriers, enabling IT hardware makers and cloud providers to embed SDR capability into white-box radios. CesiumAstro focuses exclusively on software-defined satellite links, and Lime Microsystems supplies hobbyist-to-carrier-grade development kits, signaling a wider supplier mix.

Partnerships between silicon designers and system integrators intensify. RTX’s alliance with AMD exemplifies moves to integrate FPGA fabrics and RF front-ends at wafer scale, a path expected to collapse bill-of-materials costs and lift thermal headroom. Export-control complexities create openings for non-US firms in regions wary of licensing hurdles, prompting European houses such as Thales to acquire Israeli RF specialists to accelerate antenna innovations. Consequently, the software-defined radio market rewards agile vendors that fuse secure software stacks with supply-chain resilience.

Corporate strategies increasingly revolve around recurring software revenue. Vendors bundle waveform libraries under annual subscription, mirroring enterprise-software models that smooth earnings volatility. Competitive intensity shifts from hardware margins to code maintainability, reinforcing the premium on DevSecOps capabilities within the software-defined radio market.

Software Defined Radio Industry Leaders

L3Harris Technologies, Inc.

RTX Corporation

Thales Group

BAE Systems plc

Northrop Grumman Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Terma launched Terma SPECTRA, an SDR TT&C modem. The product was developed in partnership with the European Space Agency (ESA) and incorporates expertise in Electrical Ground Support Equipment (EGSE) and Radio Frequency Special Check-Out Equipment (RF-SCOE).

- February 2025: The Ministry of Defence signed a USD 142.4 million contract with Bharat Electronics Limited (BEL) to procure 149 software-defined radios for the Indian Coast Guard.

- July 2024: BAE Systems plc announced contracts worth USD 111 million to supply the Republic of Korea (ROK) with the SATURN (Second-generation Anti-jam Tactical Ultra-high Frequency Radio for NATO) waveform.

Global Software Defined Radio Market Report Scope

Software-defined radios (SDRs) utilize software installed on a desktop computer for signal processing. The SDRs have a receiver, transmitter, software applications, and various other auxiliary systems, which perform the functions of mixers, amplifiers, modulators/demodulators, filters, and detectors. The market's scope is limited to military applications and does not include SDR demand for commercial applications like the telecommunication industry.

The software-defined radio market is segmented by platform and geography. By platform, the market is divided into land, sea, and air. The report also covers the market sizes and forecasts in major countries across major regions. For each segment, the market size has been calculated in terms of value (USD).

| Land |

| Sea |

| Air |

| Space |

| Hardware |

| Software |

| High Frequency (HF) |

| Very High Frequency (VHF) |

| Ultra High Frequency (UHF) |

| Super High Frequency (SHF) |

| Extremely High Frequency (EHF) and mmWave |

| Government and Defense |

| Commercial |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Land | ||

| Sea | |||

| Air | |||

| Space | |||

| By Component | Hardware | ||

| Software | |||

| By Frequency Band | High Frequency (HF) | ||

| Very High Frequency (VHF) | |||

| Ultra High Frequency (UHF) | |||

| Super High Frequency (SHF) | |||

| Extremely High Frequency (EHF) and mmWave | |||

| By End-user | Government and Defense | ||

| Commercial | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| Israel | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Software Defined Radio market?

The software-defined radio (SDR) market is valued at USD 21.33 billion in 2026 and is projected to reach USD 29.78 billion by 2031.

Which segment is growing fastest within the Software Defined Radio market?

Space platforms represent the fastest-growing segment, expanding at an 7.95% CAGR as satellite operators adopt reconfigurable payloads.

Why is Asia-Pacific the fastest-growing regional market?

Military modernization and aggressive 5G deployments push Asia-Pacific to an 8.6% CAGR, outpacing other regions in both defense and commercial uptake.

How are Open RAN initiatives influencing the Software Defined Radio industry?

Open RAN splits base-station functions into software layers, elevating demand for flexible SDR radio units that can be upgraded via code rather than hardware swaps.

What challenges limit wider adoption of Software Defined Radios?

High FPGA costs, cyber-security vulnerabilities, export-control restrictions, and thermal management issues collectively curb near-term growth momentum.

Who are the leading companies in the Software Defined Radio market?

Key players include L3Harris Technologies, Inc., Northrop Grumman Corporation, BAE Systems plc, RTX Corporation, and Thales Group, all of which leverage decades of defense-radio expertise while expanding into commercial 5G and satellite domains.

Page last updated on: