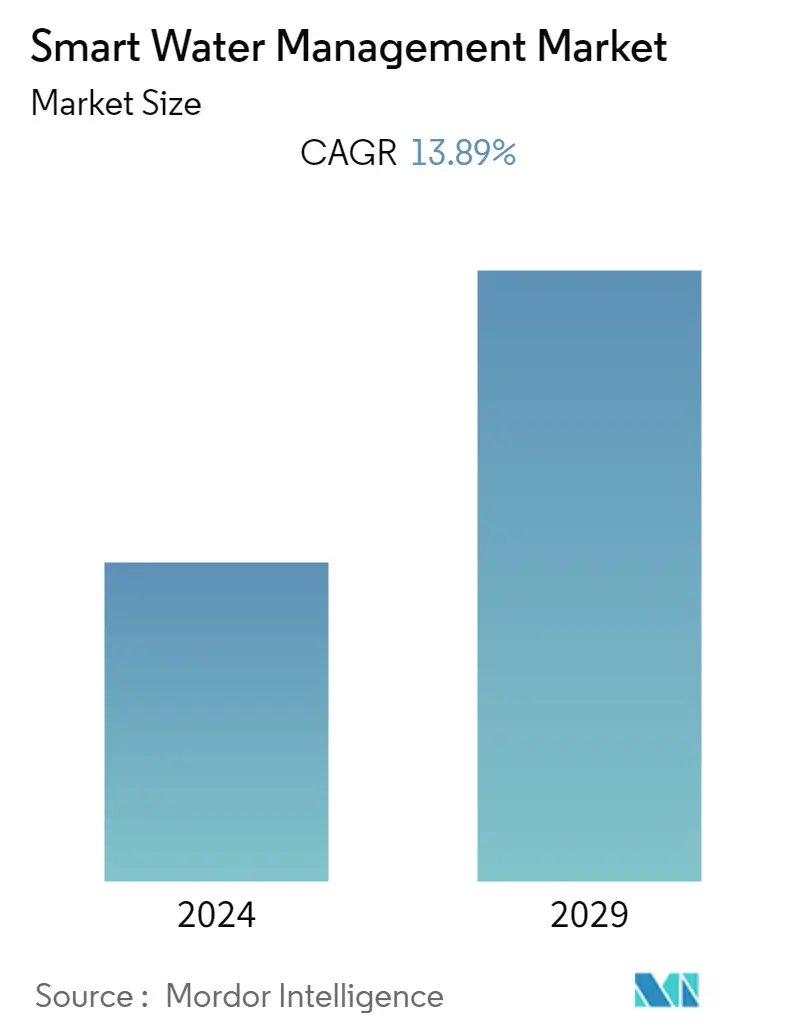

Smart Water Management Market Size

| Study Period | 2019 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | 13.89 % |

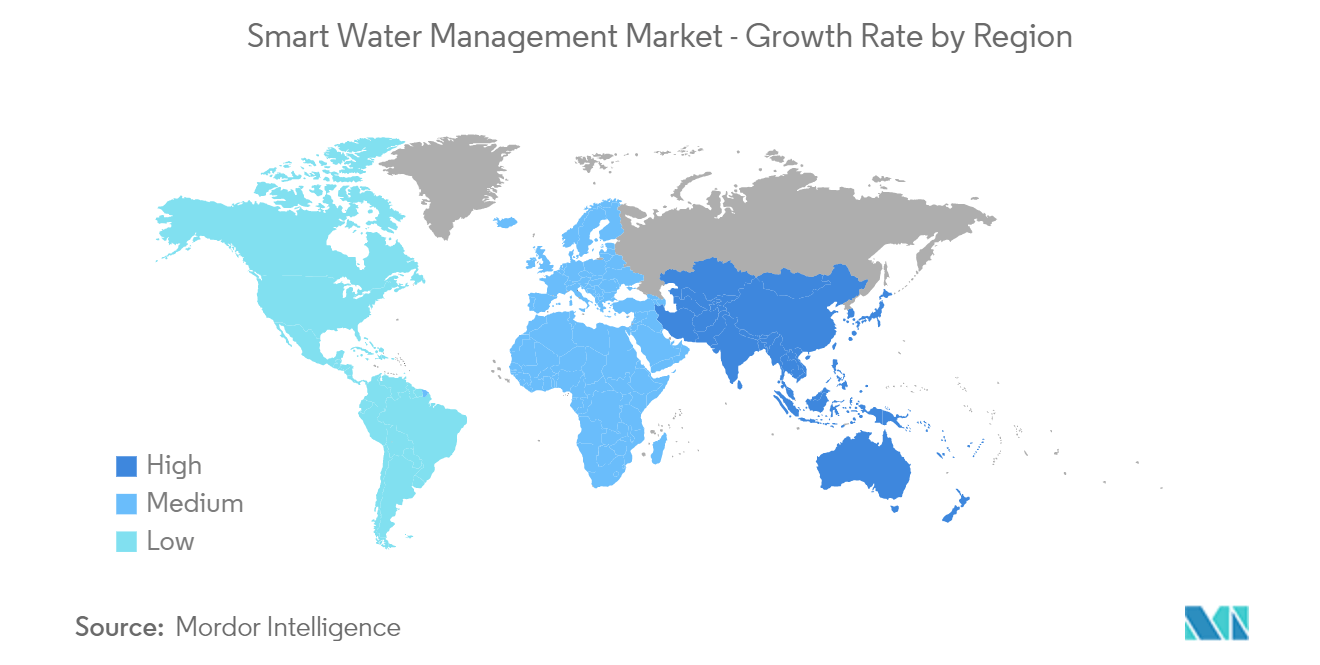

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

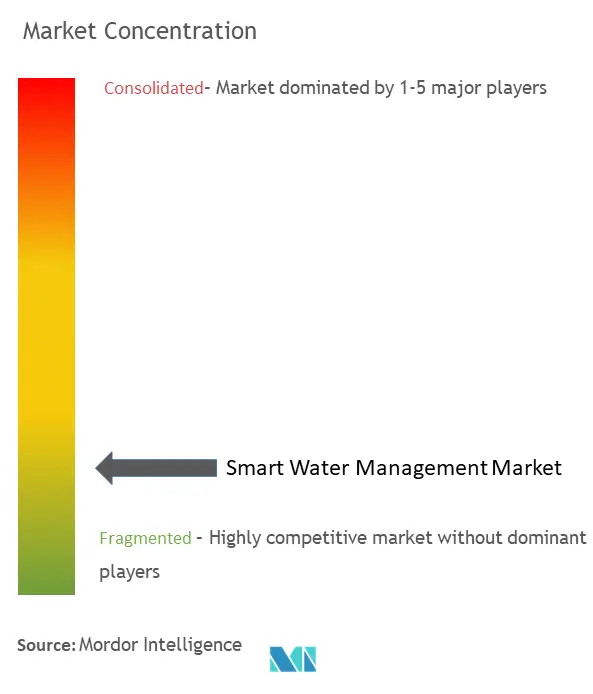

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Smart Water Management Market Analysis

The Smart Water Management Market size is expected to grow from USD 16.08 billion in 2023 to USD 30.80 billion by 2028, registering a CAGR of 13.89% during the forecast period. In recent years, owing to increasing population and urbanization, the global demand for water and the need to address the cost implications of maintaining an aging infrastructure has been the major growth factors for the smart water management market.

- Smart water management (SWM) uses information and communication technology (ICT) and real-time data and responses, which is an integral part of the solution for water management challenges. The potential application of smart systems in water management is vast and includes solutions for water quality, water quantity, efficient irrigation, leaks, pressure and flow, floods, droughts, and more.

- Smart data-driven methods for detecting water losses in public networks are becoming popular. Such solutions are based on applying the Internet of Things (IoT) and artificial intelligence (AI) techniques. In the State of Palestine, the UNDP/PAPP's Accelerator Lab partnered with a promising start-up company, FlowLess, to test a locally developed and cost-efficient smart system for detecting water losses using IoT and AI, supported by a customized web platform.

- Water infrastructure costs need to be assessed across the full water cycle and for all its major uses. As 2030 approaches, the costs of operating a new infrastructure built may exceed the annual capital cost requirements to meet those remaining unserved. When coupled with increased billing accuracy, the short-term issues in investing in smart water metering highlight a higher initial capital outlay. Traditional water management users are reluctant to switch to newer and advanced methods. The high initial cost of infrastructure and training prevails in most developing nations, hindering the market's growth.

- Post-COVID-19 pandemic, European countries focused on investing in water loss solutions. The European Union has invested in research and innovation to support a smooth transition. 79% of citizens agree that tackling climate change may lead to innovation that may make European companies more competitive, and 70% agree that water-based activity may positively affect citizens.

Smart Water Management Market Trends

Growing Need for Water Management to Drive the Market

- According to UN-Water, by 2025, 1.8 billion people may live in countries or regions with absolute water scarcity. Developing countries are most affected by flooding, water shortages, and poor water quality. Countries are working toward the United Nations' 2030 Agenda for sustainable development goals. Water targets are included across the 17 sustainable development Goals.

- According to the World Water Council, nearly four billion people are expected to face water stress by 2025. Contaminated drinking water poses a significant threat to public health, and failing dams and outdated water infrastructure also harm people. Long-lasting droughts and failing water distribution systems constitute another set of challenges to the water supply. Outdated water asset management, in such cases, restricts efficiency and puts people's lives at risk.

- With the scarcity of fresh water globally, governing bodies have made water management policies a priority agenda. The United Nations defines basic water access as having an improved water source within a 30-minute collection time. Recently, water conservation has been promoted to its sustainable development goals.

- Moreover, in November 2022, the Manitoba government announced the launch of a new water management strategy to drive future decisions, actions, and investments to safeguard the province's water ecosystems and resources while sustainably developing the economy and communities.

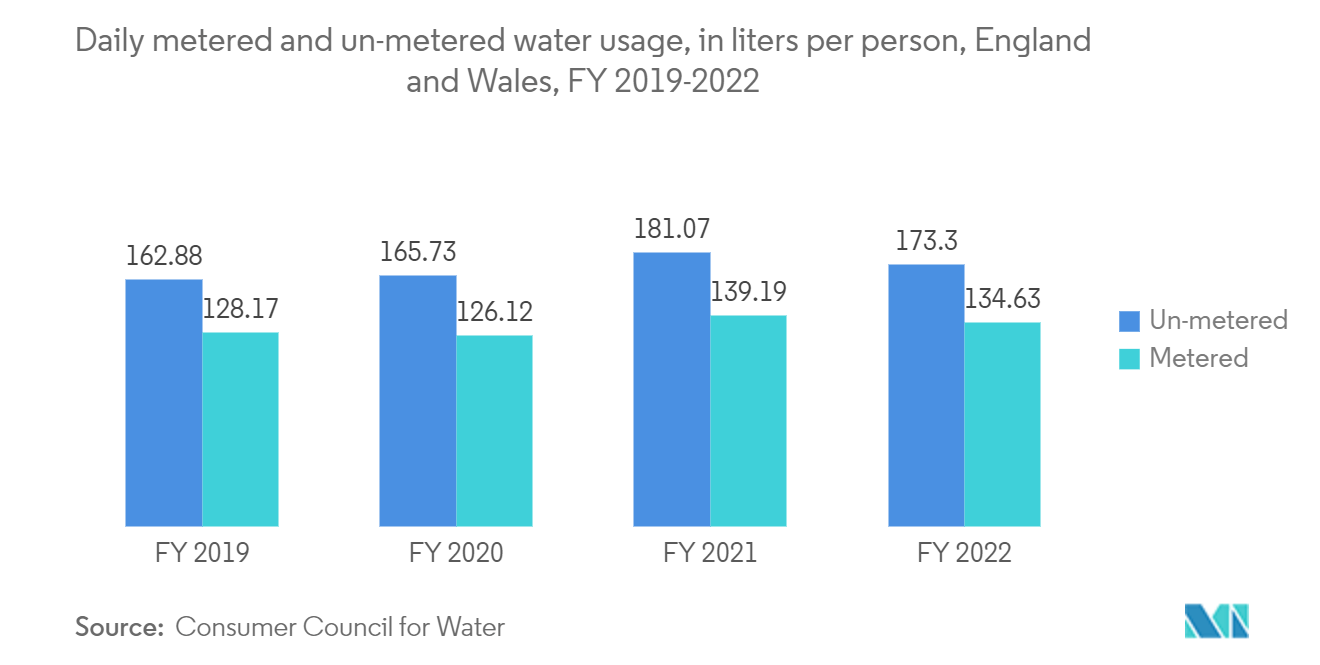

- The rising need for household water consumption further drives the need for smart water management solutions. For instance, metered consumers in England and Wales utilized an average of 135 liters per person daily compared to 173 liters per day for non-metered consumers.

Asia-Pacific is Expected to Register the Fastest Growth

- Asia-Pacific is home to more than 2.1 billion urban residents, with over two-thirds estimated to live in cities by 2050. The region comprises countries with substantial non-revenue water (NRW) losses, like India (with almost 60% of revenue losses from the total water distributed) and Singapore. Such figures signify the need for water management and indicate the potential for market growth in the region.

- The region is also witnessing demand for IoT platforms due to the growing number of connected devices and the adoption of IoT technologies for water management. For instance, Agua Water Systems, an Indian start-up, enables water usage monitoring with the help of smart solutions. The plug-and-play system utilizes artificial intelligence (AI) to analyze water usage, measure the water level in the pump, and control water distribution. Several smart wireless devices, such as motor controllers, ultrasonic sensors, and flow sensors, are used in the process.

- Consumers are upgrading their residences by adopting smart water management software and hardware. This adoption rate is rapidly increasing as software and hardware are becoming cheaper and more affordable.

- Digitization, along with the adoption of connected technologies in developing nations, is impacting all applications of solutions for smart water management by revolutionizing the way the systems for smart water management interact with the surroundings in the residential sector.

- The government in the region is launching innovative water management solutions. For instance, in March 2022, Karnataka IT Minister C N Ashwath Narayan launched India's first digital water data bank, 'AQVERIUM,' formed by AquaKraft Group Ventures. The minister said this innovation combines sustainable and green technologies, information technology, skill development, and entrepreneurship.

Smart Water Management Industry Overview

The Smart Water Management Market studied comprises several global players and emerging new players vying for attention in a fairly-contested market space. The firm concentration ratio is expected to grow more during the forecast period because several firms consider this market a lucrative opportunity to consolidate their offerings. Various companies are launching new and advanced products in the market.

In May 2023, Lumus Technology (Houston) announced its agreement with Siemens Energy to acquire assets from its water solutions portfolio, including intellectual property and trade secrets, copyrights, and research and development properties.

In April 2023, ABB announced to invest approximately USD 170 million in the United States, creating highly skilled jobs in innovation, manufacturing, and distribution operations. The company is committed to growing in the states by investing in its electrification and automation businesses that meet increased demand from end-user industries.

In April 2022, Suez Group announced the launch of AssetAdvanced, a decision-support platform. The deployment of this platform will enable water service and sanitation managers to not only expand their knowledge of current assets but also reduce risks and cost overruns from infrastructure failures, allowing them to make informed decisions on future investments.

Smart Water Management Market Leaders

ABB Ltd

IBM Corporation

SUEZ Group

Honeywell International Inc.

Schneider Electric SE (+AVEVA)

*Disclaimer: Major Players sorted in no particular order

Smart Water Management Market News

- December 2022: The Asian Development Bank (ADB) announced the approval of a USD 20 million financing package to enhance access to drinking water and irrigation services and strengthen climate resilience in Bhutan.

- March 2022: Ecopetrol SA, Accenture, and Amazon Web Services (AWS) announced the launch of a first-of-its-kind water intelligence and management solution to help advance sustainability and operational efficiencies for energy companies.

- February 2022: ABB introduced the ABB Ability Smart Solution for Wastewater. This digital solution solves wastewater treatment plant operators' challenges in achieving the lowest energy consumption and the highest operational requirements. The innovative solution comprises two main pillars, advanced process control (APC) and digital twin and simulation technology to forecast future operational needs.

Smart Water Management Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

4.1 Market Overview

4.2 Industry Attractiveness - Porter's Five Forces Analysis

4.2.1 Bargaining Power of Suppliers

4.2.2 Bargaining Power of Buyers

4.2.3 Threat of New Entrants

4.2.4 Intensity of Competitive Rivalry

4.2.5 Threat of Substitute Products and Services

4.3 Industry Value Chain Analysis

4.4 Impact of COVID-19 on the Market

5. MARKET DYNAMICS

5.1 Market Drivers

5.1.1 Growing Need to Manage the Increasing Global Demand for Water

5.1.2 Increasing Demand to Reduce Non-revenue Water (NRW) Losses

5.2 Market Restraints

5.2.1 Lack of Capital Investments to Install Infrastructure

6. MARKET SEGMENTATION

6.1 By Type

6.1.1 By Solution

6.1.1.1 Asset Management

6.1.1.2 Distribution Network Monitoring

6.1.1.3 Supervisory Control and Data Acquisition (SCADA)

6.1.1.4 Meter Data Management (MDM)

6.1.1.5 Analytics

6.1.1.6 Other Solutions

6.1.2 By Services - Managed/Professional

6.2 By End User

6.2.1 Residential

6.2.2 Commercial

6.2.3 Industrial

6.3 By Geography

6.3.1 North America

6.3.2 Europe

6.3.3 Asia-Pacific

6.3.4 Latin America

6.3.5 Middle East and Africa

7. COMPETITIVE LANDSCAPE

7.1 Company Profiles

7.1.1 ABB Ltd.

7.1.2 IBM Corporation

7.1.3 SUEZ Group

7.1.4 Honeywell International Inc.

7.1.5 Schneider Electric SE (+AVEVA)

7.1.6 Siemens AG

7.1.7 Sebata Holdings Limited

7.1.8 Hitachi Ltd.

7.1.9 Arad Group

7.1.10 TaKaDu Limited

7.1.11 Sensus Inc. (Xylem Inc.)

7.1.12 Itron Inc.

7.1.13 i2O Water Ltd.

7.1.14 Huawei Technologies Co. Ltd

7.1.15 Esri Geographic Information System Company

- *List Not Exhaustive

8. INVESTMENT ANALYSIS

9. FUTURE TRENDS

Smart Water Management Industry Segmentation

Smart water management is a technology that collects, shares, and analyzes data from water equipment and networks. Water managers use it to find leaks, lower energy usage, conserve water, predict equipment failure, and ensure regulatory compliance.

The smart water management market is segmented by type (solution (asset management, distribution network monitoring, SCADA, meter data management, analytics), services (managed services/professional services)), end-user vertical (residential, commercial, and industrial), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa). The market sizes and forecasts are provided in terms of value in USD for all the above segments.

| By Type | ||||||||

| ||||||||

| By Services - Managed/Professional |

| By End User | |

| Residential | |

| Commercial | |

| Industrial |

| By Geography | |

| North America | |

| Europe | |

| Asia-Pacific | |

| Latin America | |

| Middle East and Africa |

Smart Water Management Market Research FAQs

What is the current Smart Water Management Market size?

The Smart Water Management Market is projected to register a CAGR of 13.89% during the forecast period (2024-2029)

Who are the key players in Smart Water Management Market?

ABB Ltd, IBM Corporation, SUEZ Group , Honeywell International Inc. and Schneider Electric SE (+AVEVA) are the major companies operating in the Smart Water Management Market.

Which is the fastest growing region in Smart Water Management Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Smart Water Management Market?

In 2024, the Asia Pacific accounts for the largest market share in Smart Water Management Market.

What years does this Smart Water Management Market cover?

The report covers the Smart Water Management Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Smart Water Management Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Smart Water Management Industry Report

Statistics for the 2024 Smart Water Management market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Smart Water Management analysis includes a market forecast outlook to for 2024 to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.