Smart Washing Machine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 13.71 Billion |

| Market Size (2031) | USD 29.97 Billion |

| Growth Rate (2026 - 2031) | 16.93% CAGR |

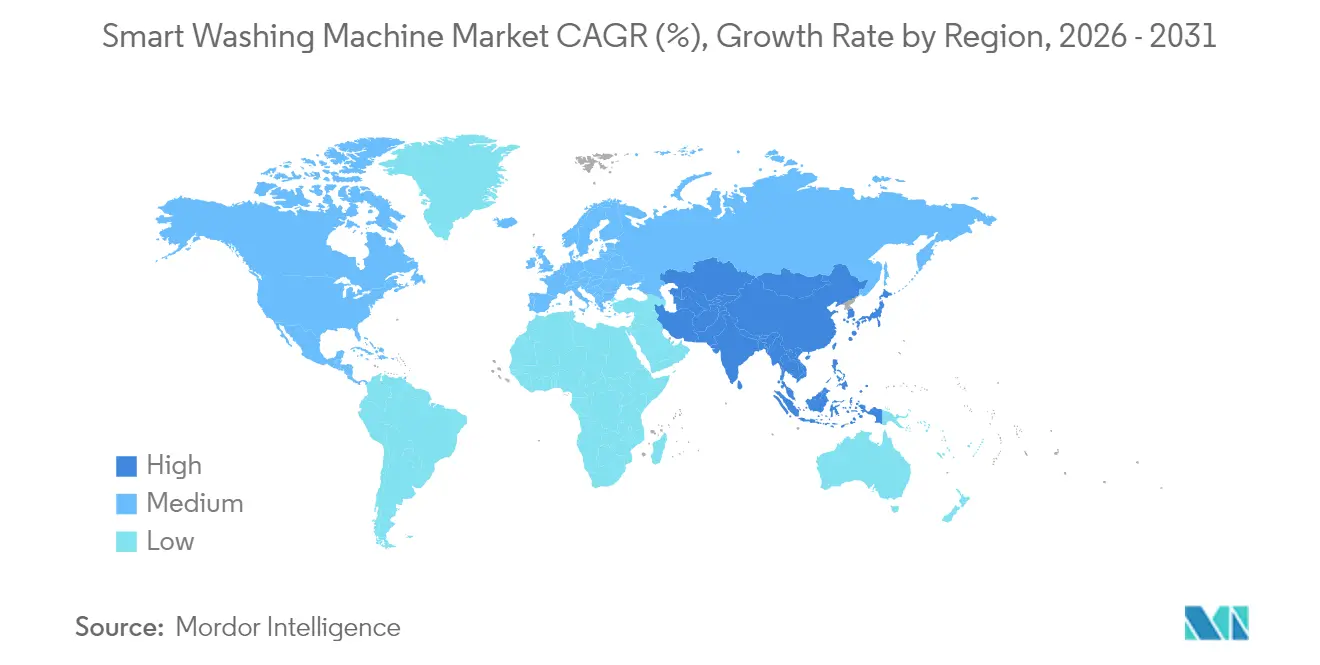

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

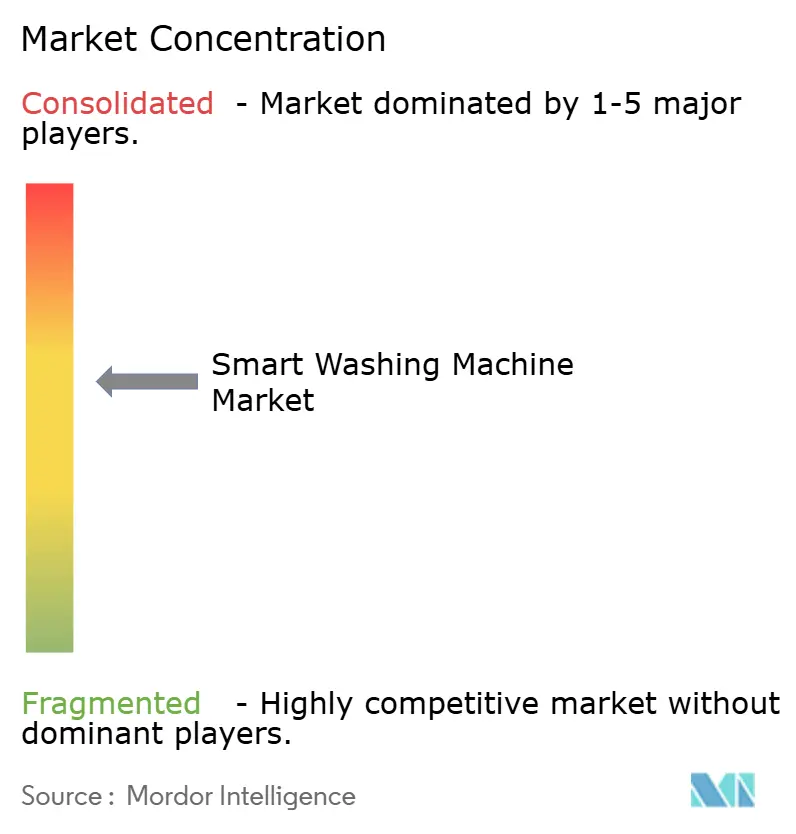

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Smart Washing Machine Market Analysis by Mordor Intelligence

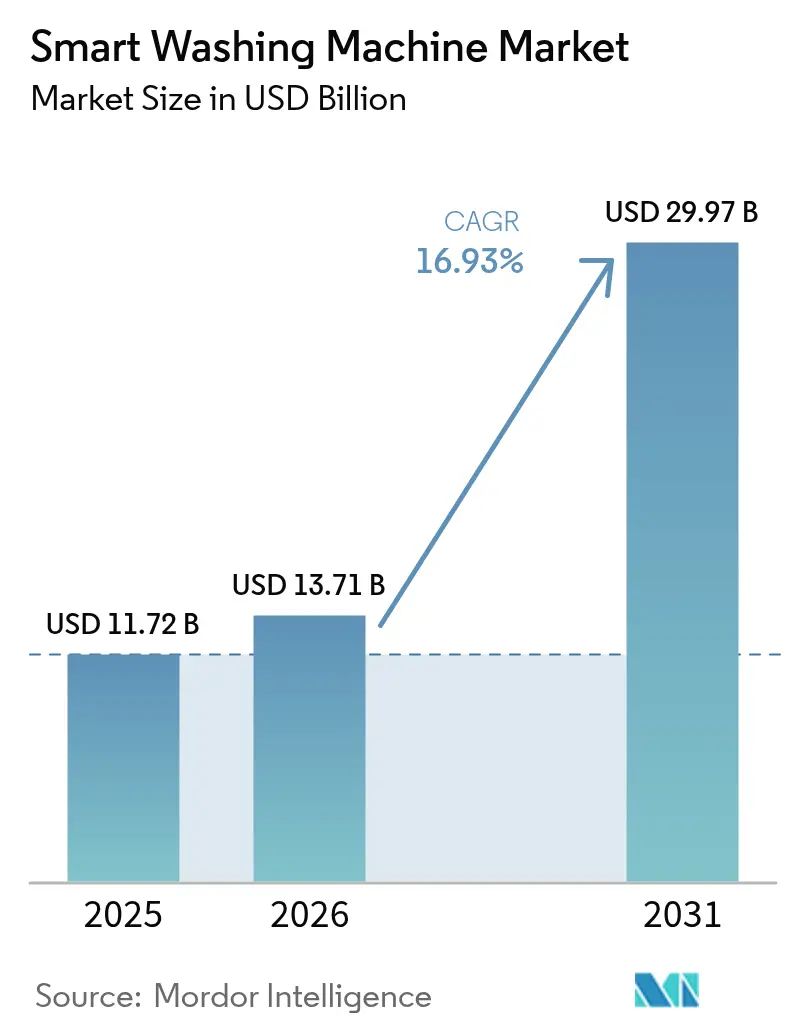

The smart washing machine market size was valued at USD 11.72 billion in 2025 and estimated to grow from USD 13.71 billion in 2026 to reach USD 29.97 billion by 2031, at a CAGR of 16.93% during the forecast period (2026-2031). Growth mirrors a shift from one-off appliance ownership toward connected-ecosystem participation, where washers operate as intelligent nodes inside broader smart homes. Adoption quickens as North American and European utilities widen demand-response incentives, on-device AI refines fabric-specific cycles, and subscription models lower the entry barrier across emerging economies. Appliance makers differentiate through firmware updates rather than simply larger drums, while property developers leverage fleet monitoring to cut service downtime. Commercial laundries and multi-family housing operators now treat connected washers as revenue-optimizing assets, reshaping replacement cycles and lifting average selling prices. Intensifying regulatory focus on water and energy efficiency also propels the smart washing machine market because connectivity enables real-time resource tracking and compliance reporting.

Key Report Takeaways

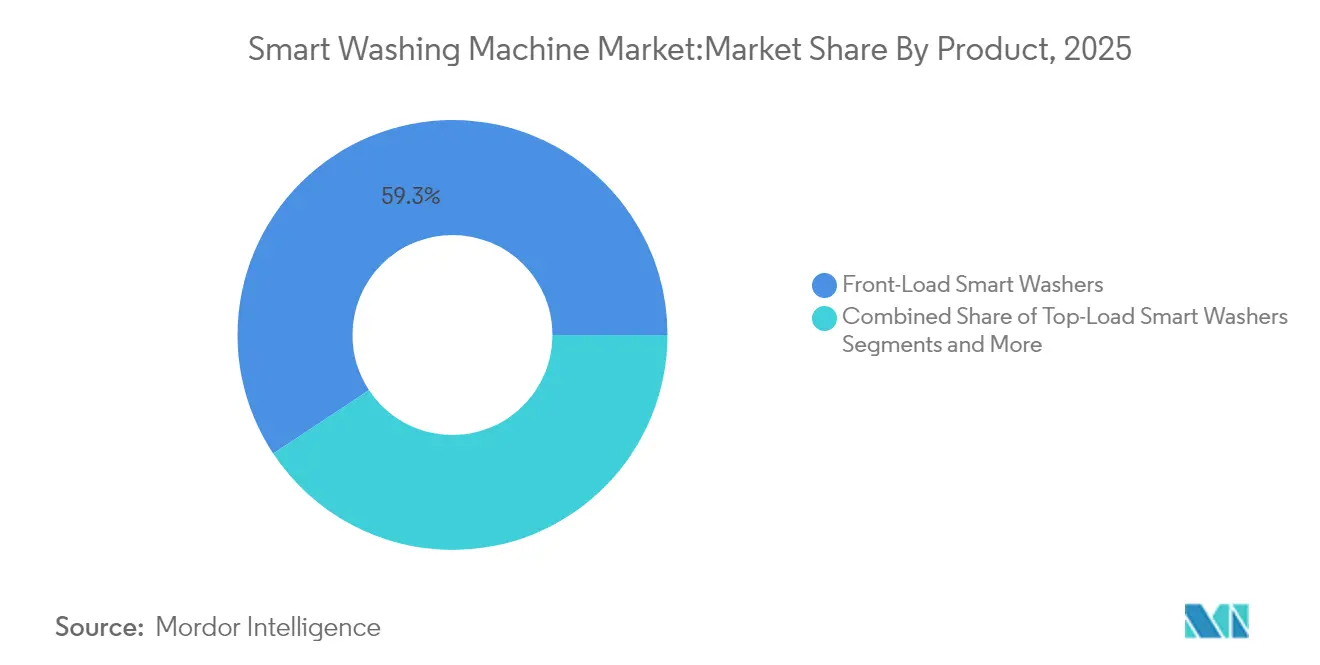

- By product type, front-load smart washers led with 59.30% revenue share of the smart washing machine market in 2025; washer-dryer combos are projected to expand at a 17.42% CAGR to 2031.

- By capacity, medium (6–8 kg) units held 54.40% of the smart washing machine market share in 2025; large (above 8 kg) units are set to grow at a 16.55% CAGR through 2031.

- By price band, mid-range (USD 501–1,000) commanded 49.20% share of the smart washing machine market size in 2025; premium (above USD 1,000) is forecast to advance at 17.08% CAGR between 2026-2031.

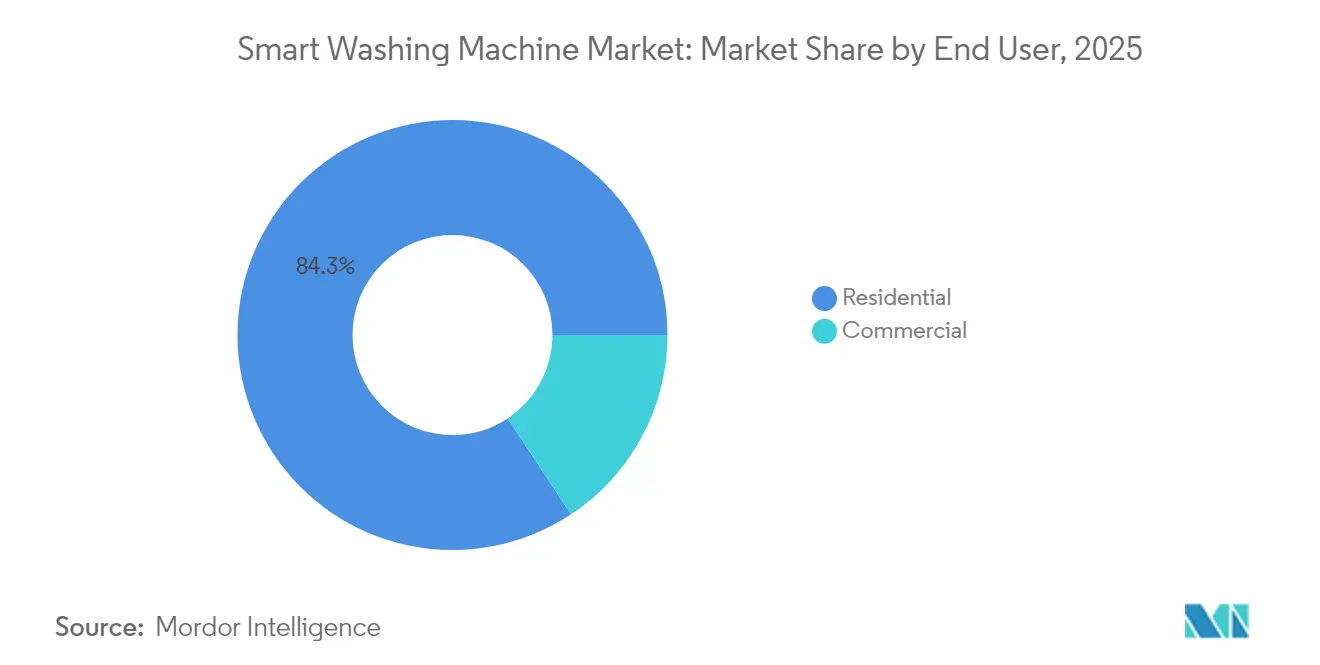

- By end user, residential applications accounted for 84.30% of the smart washing machine market size in 2025; commercial installations are rising at an 18.02% CAGR to 2031.

- By distribution channel, B2C retail held 89.10% share of the smart washing machine market in 2025; online B2C sales are climbing at an 18.33% CAGR through 2031.

- By geography, North America secured a 31.60% share of the smart washing machine market in 2025, while Asia-Pacific is projected to record a 15.31% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Smart Washing Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration with Smart-Home Ecosystems | +3.2% | Global; North America & EU lead | Medium term (2–4 years) |

| Rapid Consumer Uptake of Remote Monitoring & Predictive Maintenance | +2.8% | APAC core; spill-over to North America | Short term (≤ 2 years) |

| Proliferation of IoT-Enabled Major Appliances | +2.5% | Global, urban markets | Medium term (2–4 years) |

| Utility Incentives for Grid-Interactive, Demand-Response Washers | +2.1% | North America & EU; expanding to APAC | Long term (≥ 4 years) |

| Embedded On-Device AI for Fabric Recognition | +3.4% | Global, premium segments first | Short term (≤ 2 years) |

| Pay-Per-Wash Subscription Models | +1.8% | APAC, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Integration with Smart-Home Ecosystems

Matter 1.3, released in May 2024, formally added washing-machine support, allowing a single appliance to communicate with Amazon Alexa, Google Home, and Apple HomeKit hubs[1]Connectivity Standards Alliance, “Matter 1.3 Specification Release,” csa-iotec.org. This standardization eliminates the app fragmentation that long discouraged consumers and lets manufacturers focus on differentiated features rather than basic connectivity. Major brands such as BSH confirmed that every new washer shipped to the United States in 2025 will be Matter-ready, signaling industry commitment to open protocols. Beyond remote control, open APIs enable predictive scheduling, so washers align cycles with rooftop solar output or low-tariff utility windows, maximizing household self-consumption. Samsung further deepened interoperability by partnering with Procter & Gamble to embed Tide POD-optimized programs, proving that cross-industry collaborations can unlock tailored cleaning performance.

Rapid Consumer Uptake of Remote Monitoring & Predictive Maintenance

Predictive algorithms inside modern washers parse vibration signatures, motor torque, and temperature drift to flag anomalies weeks before failure, a capability Samsung first commercialized through its HomeCare Wizard platform. Commercial operators see clear value: GE Appliances reports that laundromats using its SmartHQ dashboard reduce service calls and cut downtime penalties substantially. Embedded microcontrollers such as STMicroelectronics’ NanoEdge AI analyze edge-level sensor data without cloud latency, making in-machine diagnostics viable even where broadband is weak. Residential users benefit from maintenance alerts that pre-order parts and recommend lighter loads, thereby extending both product and clothing life. Positive user experiences continue to spread via word-of-mouth and social media, accelerating replacement demand and enlarging the smart washing machine market.

Proliferation of IoT-Enabled Major Appliances

Network effects arise when multiple appliances are connected, allowing a washer to delay its cycle until the smart water heater finishes reheating or an electric vehicle finishes fast charging. Urban residents appreciate consolidated dashboards that visualize cumulative energy and water use, nudging them toward conservation. Manufacturers harvest anonymized data to design quieter motors and refine spin algorithms, thereby improving upcoming models and locking users into branded ecosystems. As connected fleets grow, governments view them as an asset for energy-efficiency targets, further propelling the smart washing machine market.

Utility Incentives for Grid-Interactive, Demand-Response Washers

US utilities pay households yearly stipends to enroll qualifying washers in automated demand-response programs, trimming grid peaks without costly infrastructure upgrades. In Europe, similar schemes dovetail with eco-design regulations that require connectivity for verification of claimed savings[2]European Commission, “Ecodesign Requirements for Washing Machines,” ec.europa.eu. Such coupling helps offset the premium over legacy models and shifts smart washers from early-adopter status toward mass-market acceptance. Manufacturers benefit, as rebate-eligible units sell through faster, raising economies of scale. In turn, larger production runs cut bill-of-materials cost, enabling competitive pricing that further expands the smart washing machine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-Brand Compatibility & Interoperability Issues | -1.8% | Global; fragmented ecosystems | Medium term (2–4 years) |

| High Repair & Maintenance Costs for Connected Components | -1.2% | Global; pronounced in emerging markets | Short term (≤ 2 years) |

| Stricter Cybersecurity & Data-Privacy Compliance Costs | -1.5% | EU & North America; expanding globally | Long term (≥ 4 years) |

| Water-Scarcity Regulations Limiting Drum Capacity | -0.9% | Water-stressed regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cross-Brand Compatibility & Interoperability Issues

Matter promises harmony, yet legacy appliances rarely receive firmware retrofits, forcing households into multiple apps when they mix brands. Small manufacturers hesitate to support diverse protocols, citing engineering costs that erode already thin margins. Property managers outfitting hundreds of units must juggle different dashboards, curbing large-scale smart deployments, and slowing smart washing machine market penetration. Cloud-to-cloud solutions such as the Home Connectivity Alliance Specification exist, but uptake remains limited to well-funded brands. Until seamless multi-brand orchestration arrives, interoperability friction will temper the market’s otherwise steep trajectory.

High Repair & Maintenance Costs for Connected Components

Touchscreens, Wi-Fi modules, and AI chipsets raise parts prices compared with mechanical timers, inflating out-of-warranty repair bills. In emerging markets, shipping a replacement board can take weeks, prompting frustrated users to revert to analog machines or low-feature models. Brands introduce modular designs—Samsung’s 2025 Bespoke series lets owners swap display panels within minutes—yet spare parts remain costlier than legacy knobs. Extended-service contracts soften the blow but still add to lifetime operating costs. Consequently, price-sensitive consumers may hesitate, capping near-term gains in the smart washing machine market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Combo Units Drive Space-Efficient Innovation

Front-load washers accounted for 59.30% of 2025 revenue, reflecting their lower water use and widespread acceptance in Europe and many urban centers. Combo units, however, log a 17.42% CAGR as city dwellers value one-appliance convenience; AI programs auto-sequence wash-to-dry transfers, freeing users from manual transfer steps. LG’s WashTower integrates dual sensors that adjust drying temperature to match residual moisture, reducing fabric wear. Portable smart washers advance in co-living spaces, using Bluetooth scheduling so tenants avoid peak shower hours. Commercial heavy-duty smart washers, though niche, benefit from remote diagnostics that maximize uptime, validating premium pricing in laundromats and multi-family basements.

Market anticipation surrounds Samsung’s 27-inch Bespoke AI laundry series with 7-inch touch displays that double as smart-home hubs. Design convergence blurs residential and light-commercial boundaries as operators demand consumer-grade UX while homeowners seek commercial-grade robustness. As ecosystem applications grow, the smart washing machine market share of software-rich products increases, cementing combos as a formidable challenger to traditional twin-appliance layouts.

By Capacity: Large Units Capitalize on Efficiency Trends

Medium units (6–8 kg) represent 54.40% of shipments because they align with typical household needs and cabinet dimensions. Yet, large models above 8 kg post a 16.55% CAGR, as families discover that one large weekly cycle uses fewer total resources than multiple smaller washes. Utility rebates often key off per-kilogram ratings, nudging buyers toward large, high-efficiency drums. Samsung’s 24-inch small-capacity set still appeals in Europe, where urban apartments limit footprint; it meets Class A requirements while consuming 55% less energy than earlier equivalents. Sub-6 kg models thrive in RVs, vacation cabins, and secondary residences, leveraging app alerts so owners can start a cycle before arriving.

The smart washing machine market size for large units will keep expanding as AI load-sensing negates water-waste fears, while smaller drums will linger for edge cases. Capacity diversification helps brands defend against regional water regulations and offers retailers bundles tailored to local living patterns.

By Price Band: Premium Segment Leads Technology Adoption

Premium washers above USD 1,000 are projected to grow 17.08% yearly, serving as the launchpad for AI fabric recognition, automatic detergent dosing, and voice assistance. Many vendors embed cloud licenses in the purchase price and then sell optional upgrades—Samsung’s Stain-Assist library unlocks via in-app micro-payments, extending lifetime revenue. Mid-range units (USD 501–1,000) capture volume by inheriting last-year flagship capabilities, such as antimicrobial vents or limited AI presets; Whirlpool introduced the FreshFlow Vent System at a price attractive to mainstream buyers. Economy models (≤USD 500) keep costs down by pushing intelligence to the smartphone app and omitting cameras, yet still satisfy basic Energy Star requirements. As software upgradability proliferates, price segmentation increasingly hinges on bundled features and service tiers rather than core hardware, shaping consumer perceptions of value inside the smart washing machine industry.

By End User: Commercial Segment Drives Modernization

Residential demand held 84.30% in 2025, but commercial adoption races ahead at 18.02% CAGR as property managers digitize laundry rooms. EQT Group’s WASH operates 635,000 connected machines across 82,000 sites, sustaining 98% customer retention via remote monitoring and cashless payments. Smart dashboards schedule maintenance when foot traffic is lowest, improving tenant satisfaction and raising vendor prices. Homeowners continue replacing aging top-loaders, attracted by 20% energy savings and integration with voice assistants like Amazon Alexa. Builders increasingly include connected washers in base spec sheets, branding units as part of the overall smart-home package. As lines blur, commercial-grade durability and residential-grade interfaces converge, broadening the smart washing machine market share of hybrid designs.

By Distribution Channel: Online Sales Transform Market Access

B2C/Retail still accounts for 89.10% of 2025 revenue, yet online B2C sales accelerate at 18.33% CAGR thanks to immersive configurators and same-day delivery in urban centers. Direct-to-consumer portals empower brands to bundle detergent auto-replenishment and warranty extensions at checkout, enhancing customer stickiness. Rural shoppers benefit as e-commerce bridges gaps where physical stores stock only generic models, expanding the reachable smart washing machine market. Multi-brand showrooms now include live Wi-Fi so visitors can test app control before buying, while brand-exclusive outlets focus on premium lines with white-glove installation packages. B2B direct deals thrive in hospitality and healthcare, where bulk orders require API access for building-management integration.

Geography Analysis

North America retained 31.60% of the smart washing machine market share in 2025, leveraged by high broadband penetration and utility incentives such as National Grid’s ConnectedSolutions program that pays users to shift wash cycles away from peaks. GE Appliances’ USD 490 million expansion in Kentucky exemplifies domestic investment to shorten lead times for connected models. Premium-segment adoption thrives because households value both convenience and compliance with tightening energy codes.

Asia-Pacific logs the fastest 15.31% CAGR driven by urban migration, rising disposable incomes, and government smart-city projects. Samsung’s April 2025 AI top-loaders cater to Asian preferences by merging traditional design with fabric-recognition algorithms, widening appeal. Subscription laundry models gain traction in Indonesia and Thailand, providing affordable access while familiarizing users with smart features.

Europe frames connectivity through sustainability; ecodesign rules in force since March 2021 require Eco 40-60 cycles and reparability indices. The legislation targets 12.4 TWh electricity savings and 1,464 billion L water reductions by 2030, creating demand for washers that confirm savings through cloud telemetry. Electrolux’s 2025 smart range highlights resource efficiency and fabric longevity—attributes appealing to environmentally conscious Europeans. Utilities across Germany and Italy now tie rebates to verifiable consumption data, ensuring connected models dominate future replacements.

Competitive Landscape

The smart washing machine market is moderately concentrated: the top five players command a major share of shipments, yet software prowess, not drum engineering, increasingly sets leaders apart. Samsung, LG, and Whirlpool wield global factories and brand recognition but channel more R&D into AI frameworks and cloud platforms each year. Smaller firms partner with chip vendors to embed turnkey AI, sidestepping heavy algorithm development. Cross-industry collaborations flourish—Unilever joined Samsung in October 2024 to refine detergent-optimized cycles, while semiconductor firms bundle vibration analytics with MCU reference designs. Bosch’s exploration of a Whirlpool bid signals consolidation pressure to secure both scale and digital talent [3]Reuters, “Bosch Considers Whirlpool Bid,” reuters.com.

Platform convergence dominates strategy. Brands now market washers as gateways to entire smart-home ecosystems, monetizing data through subscription services. Samsung’s Bespoke lineup permits firmware unlocks of advanced stain libraries, extending revenue beyond the initial sale. Whirlpool opens APIs to building-energy systems, courting property developers who demand whole-building dashboards. As cybersecurity threats mount, vendors publicize third-party audits and launch bug-bounty programs, turning security compliance from a cost center to a brand asset.

Smart Washing Machine Industry Leaders

LG Electronics Inc.

Samsung Electronics Co., Ltd.

Whirlpool Corporation

Haier Smart Home Co., Ltd.

Electrolux AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: GE Appliances confirmed a USD 490 million investment to consolidate washer production in Kentucky, scaling smart-model capacity.

- January 2025: Henkel introduced Smartwash, a sensor-based chemistry platform that optimizes detergent dosing per load.

- April 2025: Samsung released AI-powered top-load washers with AI Wash technology that cuts energy use up to 20%.

- July 2024: Electrolux launched a sustainability-focused smart laundry range aimed at extending garment life.

Global Smart Washing Machine Market Report Scope

This report provides a complete background analysis of the Smart Washing Machine Market, which includes an assessment of the economy, a market overview, market size estimation for key segments, and emerging trends in the market; market dynamics and key company profiles are covered in the report. The Smart Washing Machine Market is segmented Type into Top Load and Front Load, Distribution Channel into Multibrand Stores, Exclusive Stores, Online, and Other Distribution Channels, End User into Residential and Commercial, and Geography into North America, South America, Europe, Asia Pacific, and the Middle East and Africa. The report offers market size and forecast in value (USD) for all the above segments.

| Front-Load Smart Washers |

| Top-Load Smart Washers |

| Washer-Dryer Combo Units |

| Portable / Compact Smart Washers |

| Commercial Heavy-Duty Smart Washers |

| Small (Below 6 Kg) |

| Medium (6 to 8 Kg) |

| Large (Above 8 Kg) |

| Economy (≤ USD 500) |

| Mid-range (USD 501-1 000) |

| Premium ( above USD 1 000) |

| Residential |

| Commercial |

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B/Directly from the Manufacturers |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, and Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | |

| Rest of Europe | |

| Middle East And Africa | United Arab of Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East And Africa |

| By Product | Front-Load Smart Washers | |

| Top-Load Smart Washers | ||

| Washer-Dryer Combo Units | ||

| Portable / Compact Smart Washers | ||

| Commercial Heavy-Duty Smart Washers | ||

| By Capacity | Small (Below 6 Kg) | |

| Medium (6 to 8 Kg) | ||

| Large (Above 8 Kg) | ||

| By Price Band | Economy (≤ USD 500) | |

| Mid-range (USD 501-1 000) | ||

| Premium ( above USD 1 000) | ||

| By End user | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Directly from the Manufacturers | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, and Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, and Sweden) | ||

| Rest of Europe | ||

| Middle East And Africa | United Arab of Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East And Africa | ||

Key Questions Answered in the Report

What is the current smart washing machine market size?

The smart washing machine market size is USD 13.71 billion in 2026 and is expected to reach USD 29.97 billion by 2031.

Which region is growing fastest in the smart washing machine market?

Asia-Pacific is the fastest-growing region, forecast to register a 15.31% CAGR through 2031.

Which product segment is expanding most quickly?

Washer-dryer combo units are advancing at a 17.42% CAGR because they provide space-saving all-in-one convenience.

How do utility programs influence adoption?

Initiatives like National Grid’s ConnectedSolutions pay consumers to let washers shift cycles away from peak demand, effectively subsidizing the higher upfront cost of smart models.

Why is the premium segment expanding so rapidly?

Premium models include AI-driven fabric recognition, automatic detergent dosing, and over-the-air feature updates, driving a 17.08% CAGR in the >USD 1,000 price band.

What major restraint could slow growth?

Rising cybersecurity and data-privacy compliance costs pose a significant burden, especially for mid-tier brands, and can slow global rollout.

Page last updated on: